Memo Published September 20, 2023 · 11 minute read

Western Reliance on Russian Fuel: A Dangerous Game

Rowen Price, Ryan Norman, & Alan Ahn

Takeaways

- The United States depends on Russia for up to 24% of our uranium enrichment. Meanwhile, Russia remains the only global commercial supplier of high assay low-enriched uranium (HALEU) necessary for many advanced reactors.

- US and EU countries purchase the majority of Russian enriched uranium and, if Russia cut off foreign exports, would face an immediate supply-demand gap for nuclear fuel that would sharply increase fuel prices and jeopardize power plants.

- The full impacts of a Russian-induced fuel disruption are uncertain because power producers have varying amounts of fuel in reserve. Overseas utilities may be especially vulnerable as European uranium inventories have been shrinking steadily for years.

- Building new domestic fuel capabilities and securing the global nuclear fuel supply chain is the only way to end Putin’s manipulation of foreign countries’ dependency and promote global security.

By 2035, there are expected to be 513 nuclear reactors operating globally—equating to 490 GW of electric output.1 To support these reactors, global demand for nuclear fuel will be on the order of 72.2 million SWU (mSWU) annually–up 30% from current demand–and Russia is set to profit.2 Currently, Russia is the largest uranium enrichment supplier on the global market and competes with enrichers in the UK, Germany, Netherlands, France, China, and the United States. Russian state-owned businesses provided 35% of global enrichment in 2021 and are projected to provide 30% of global supply in 2035.3

Long-term prices for enriched uranium, which are crucial for utilities to plan costs and build multi-year fuel contracts, are the highest since September 2012 and show no sign of coming down in the near term. Russia’s tight grip on the global enrichment market limits options for long-term contracting through at least the next four to five years.4 Prices are not expected to stabilize until 2030, following the West’s expansion of enrichment capacity.

In the near term, the US and allies will have to navigate an increasingly volatile global market for enriched uranium products where Russia holds an outsized influence on price and supply. This memo analyzes recent public and private market data to contextualize how much the West is spending on Russian enriched uranium, the projected global needs for nuclear fuels, and the amount of low-enriched uranium (LEU) fuel that is onshore in western reserves. This analysis concludes that the revenues from nuclear fuel exports to the West may be insufficient to deter Russia from restricting such exports and disrupting western energy operations.

Note: the term “SWU” means separative work units and is the metric used in the trading of enriched uranium products. It relates to the amount of enrichment effort and not to a specific quantity of uranium product.

Russia’s Revenue from Global Fuel Sales

Western countries purchase the overwhelming majority of Russian uranium

Last year, US utilities purchased processed natural uranium from Russia at a total weighted price of $168,291,200.5 US owners and operators also purchased enrichment services from Russia at an averaged price of $344 million.6 Since 2018, US utilities have spent ~$891M on processed natural uranium purchases and ~$1.8 billion on enrichment services from Russia.7 US entities also purchase conversion services from Russia that are not reflected in either of these totals, but likely contribute another $30-60 million annually.8

But wait, I’ve read that the United States spends $1B annually on Russian uranium

The US Energy Information Administration (EIA) tracks annual purchases by US entities and accounts for various types of uranium products and services. Other sources, such as trade and tariff data from the US International Trade Commission (USITC), track the customs value of uranium commodities imported into the US in each calendar year. Due to the multi-year contract pricing for many fuel products, purchases in a given year do not necessarily match the “value” of a product in the year that goods are imported. Additionally, under current law, US customers must deliver certain uranium products back to Russia–known as “returned feed”. USITC customs data contains the value of “returned feed” products and as such, can present an inflated picture of US uranium procurement.

The United States is the largest global purchaser of Russian enriched uranium. In 2022, the United States accounted for 42% of all Russian enriched uranium exports.9 This figure includes deliveries purchased in previous contract years. Comparatively, the US accounted for 3% of Russian crude oil exports and 0% of Russian natural gas exports in 2021.10

European uranium purchase trends are similar to the United States

France imported €359 million (about $377.5 million) of enriched uranium from Russia in 2022.11 In 2021, Russia provided 31% of the EU’s enriched material and services–delivering 3.19 mSWU to EU countries.12

In 2022, France (18.6%), the Netherlands (2.7%), and Germany (2%) collectively imported 23% of Russian enriched uranium and associated products. Exports also went to other countries including the United States, China, and South Korea.13 Comparatively, OECD Europe made up almost 75% of Russia’s natural gas exports and almost 50% of Russia’s oil exports in 2021 (most recent available data).14

And so…

The United States and its allies are highly dependent on Russian enriched uranium imports—for example, nearly a third of EU enriched uranium came from Russia in 2022 despite having several EU countries with significant enrichment capacity.15 The United States is especially reliant on Russian enrichment as existing domestic capacity to produce LEU cannot cover US demand. However, Russia is far from desperate for the profits brought in from such uranium sales. Rosatom, Russia’s state-backed nuclear energy corporation, generated $19B in total annual revenues in 2021—less than a tenth of the $200B that Russia is estimated to make from just exports of oil and gas annually.16 According to Rosatom, total foreign revenues for nuclear fuel cycle services and products accounted for $3.3B in 2021, a figure that includes back-end fuel cycle services.17 In comparison to oil and gas, foreign revenues for nuclear fuel services simply aren’t substantial enough to create an economic dependency. For Rosatom, Western imports provide a useful, albeit replaceable, revenue stream to supplement its broader business.

Projections on Global LEU + HALEU Demand

Meeting Global Low-Enriched Uranium (LEU) Demand

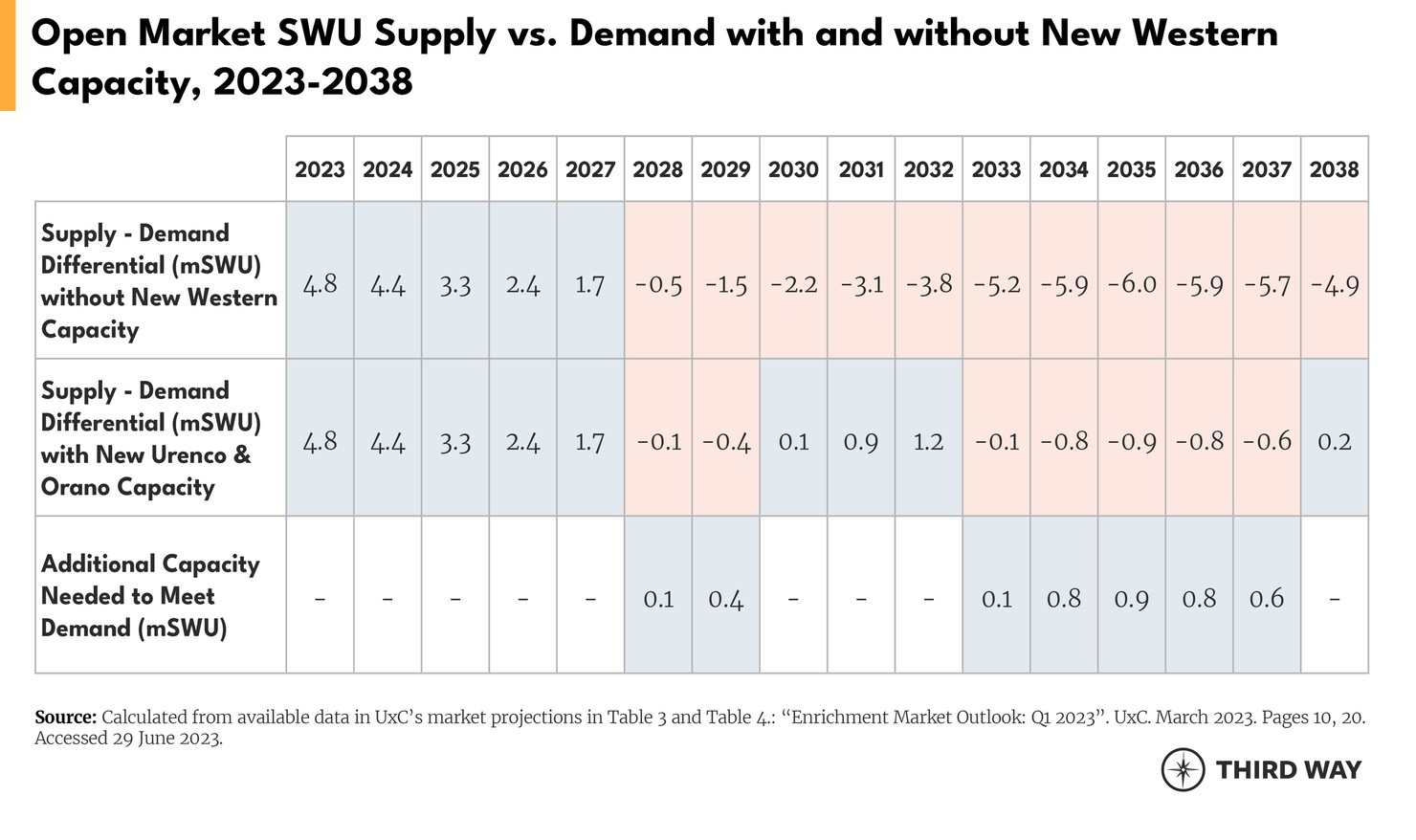

From 2023-2035 global markets will require 783 mSWU, with US needs representing 23 percent.18 Current global enrichment capacity is 55.6 mSWU /yr.19 Russia and China collectively host 54% of global capacity.20

Without new western enrichment capacity, global enrichment needs will exceed annual non-Russian supply by 6% to 20% through 2038.21 This projection assumes legislative reductions or wholesale eliminations of Russian imports from the US, Czechia, Bulgaria, Slovakia, and other countries effective in 2028.22 Western enrichers Urenco and Orano have either announced new plans to expand capacity, or are currently considering expansions that will help secure the market share no longer held by Russia. Even if Russian imports continue through most of the 2020s, new western capacity is needed to significantly reduce the supply-demand gap.23 With an immediate restriction on Russian uranium, the near-term supply-demand gap could be substantial—especially for the United States.

High Assay Low-Enriched Uranium (HALEU) Demand

In 2021, the Nuclear Energy Institute estimated that the industry’s annual HALEU need will be 600 MTU by 2035.24 HALEU demand will be far less than LEU until more advanced reactors are constructed globally or existing customers transition from LEU. However, the entirety of the existing commercial HALEU supply chain is controlled by Russia–meaning that developing the necessary capacity outside of Putin’s sphere of influence is a greater challenge than expanding existing LEU capacity in the West. Until the US and allies are able to stand up a western-controlled supply chain for HALEU, Russia will control 100% of the global commercial market for this advanced nuclear fuel.

Domestic LEU Inventories and Projected US Needs

The US has LEU inventories, but quantities vary significantly across utilities making it hard to determine precisely which nuclear power plants are most vulnerable

As of the end of 2022, owners and operators of commercial nuclear power reactors in the United States had LEU inventories equivalent to 54 million pounds of natural uranium.25 Over the last four years, US reactor fuel requirements have averaged roughly 46 million pounds of natural uranium-equivalent.26 In other words, this enriched uranium product corresponds to about 1.2 years’ worth of inventories. However, the aggregate picture is skewed by large utilities who will have more fuel stored and purchased than smaller operators. It’s likely that the continued operation of many US nuclear power plants may be immediately affected by global market disruptions in fuel supply.

The American Assured Fuel Supply (AFS) could, in theory, be used to provide emergency fuel supply to US operators. However, AFS is estimated to contain 230 MTU of LEU, about 12% of US annual requirements, a negligible amount in the event of a severe supply disruption.27 The National Nuclear Security Administration (NNSA) administers AFS, the intent of which is to provide fuel reserves for international partners in the event of global fuel market disruptions. This reserve could be used for domestic nuclear power facilities, but such quantities, as well as other nominal government stocks, would likely only support core refueling for a handful of reactors—far shy of the 93 that provide nearly 20% of total US electricity.

Projected US uranium and enrichment needs

The EIA notes that maximum anticipated US market requirements through 2032 are 402 million pounds of processed natural uranium.28 To produce LEU, the United States will need an average of 14 mSWU of enrichment annually through 2035.29 However, the only US domestic enrichment capacity is at the National Enrichment Facility (NEF) in Eunice, New Mexico. NEF’s current max production capacity of 4.9 mSWU equates to roughly a third of current US needs.

European uranium inventories are shrinking but demand is projected to increase

For the past 8 years, EU utilities have been loading more material into reactors than they have been buying, which has caused a steady drop in inventory levels.30 EU utility inventories of natural and enriched uranium in 2021 were equivalent to 95.7 million lbs.31 At the EU’s current usage of 31.8 million lbs annually, the EU’s inventory as of 2021 was sufficient for up to three years.32

Conclusion

Putin is cashing our checks, but it’s just pocket change for Russia—and that should worry us.

The global community has a dependence on Russian uranium, but it doesn’t run both ways. Rosatom’s total revenues are several orders of magnitude smaller than Russia’s oil and gas businesses. The $200 billion Russia collects annually from exports of oil and gas are 60 times greater than the $3.3 billion generated by Rosatom’s nuclear fuel-related exports. Ultimately, western countries' contributions to revenues for uranium and enrichment services are a drop in the bucket for Russia’s export portfolio.

But the current international sanctions incentivize Russia to keep fuel revenue streams open, right?

Not necessarily. Russia is on track to take an economic hit upward of $150B due to its hostilities and occupation in Ukraine.33 However, since Russian uranium fuel exports are only a comparatively small figure, the revenues that Russia would receive in the near term from new fuel purchases would be negligible in mitigating projected national losses. To be fair, Russia’s uranium business provides deeper economic benefits for Russia such as thousands of jobs across the country. However, Russia could simply find other buyers to make up for the gap in western revenues, particularly in emerging nuclear energy countries where Russia is developing early market relationships.

Further, sanctions cut both ways–for example, risking US and western control on the global financial system–but market manipulation would be an easy way for Putin to retaliate and hit western customers harder than it would hurt Russia. In fact, with increasing western interest in standing up additional supply in the United States, Europe, or other allied countries, there may be greater temptation for Putin to restrict enrichment services to the West in the near-term rather than wait until new capacity is online to shoulder the drop-off in supply.

Ultimately, new nuclear fuel production capacity is the only thing that can guarantee the energy security of the US and allies.

Russia’s nuclear fuel business is not a significant source of its revenue relative to other exports like oil and gas, but renders a distinct advantage in competing for international markets. Russian nuclear power exports are not just commercial deals, but advance the geopolitical interests of the state. For Moscow, the true value of fuel exports (and nuclear exports, more generally) is in the ability to exert control over foreign states through energy markets.

Building new nuclear fuel infrastructure in the US strengthens our energy security and reduces our dependence on Russian nuclear fuel services. It also benefits our national security interests by enabling us to exercise leadership in new nuclear technology and the fuel cycle. These efforts are critical to ensuring that the deployment of nuclear technology is done under the highest standards of safety, security, and nonproliferation internationally. Now, the US must lead the way by building out domestic fuel production and working with western allies to secure the global supply chain.