Third Way Take Published June 13, 2016 · Updated June 13, 2016 · 11 minute read

Filling the Gap: New Ideas That Get People To Save

David Brown & Tanner Daniel

Takeaways

- Having adequate savings, for emergency expenses as well as retirement, is a hallmark of being middle-class in America. So expanding personal savings is one of the surest routes to strengthening and growing the middle class.

- Ultimately, national legislation is needed to help increase personal savings in the U.S. But creative ideas are already flourishing, and—if expanded upon—these public and private sector initiatives can continue to make significant progress.

- These new products and programs show that getting individuals to save more can be as simple as changing the default setting on an employer benefit, injecting fun into the savings process, or offering a new twist on an old product.

Sometimes all you need is a nudge.

A prime example comes with saving for retirement. When employers ask their workers to opt in to a retirement plan, studies have shown they get 49% participation. Compare that to when they automatically enroll workers with the chance to opt out, 86% participate.1 That’s almost a 40-point shift in behavior with no investment in a marketing strategy—just a behavioral nudge to promote better choices.

Experts have drawn such simple yet effective solutions from the field of behavioral economics. Behavioral economist Dan Ariely writes, “Standard economics assumes that we are rational... [but] we are far less rational in our decision-making. We all make the same types of mistakes over and over, because of the basic wiring of our brains.”2 Understanding how to anticipate people’s irrational behavior—in essence—is behavioral economics and can help policymakers and employers better design policy.

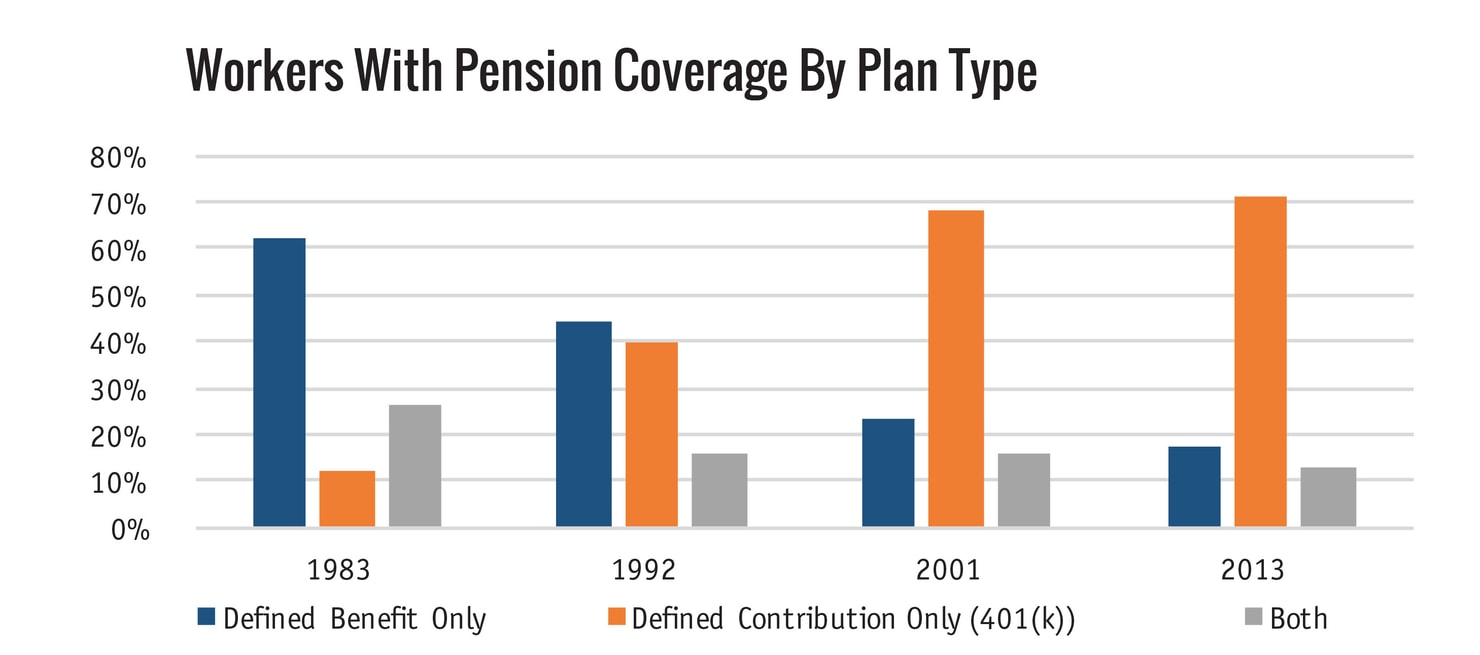

This is especially true in the area of personal savings. And behavioral nudges to encourage savings are needed now, more than ever, because of the extent to which economic change is shifting the burden to save onto individuals. As companies look to modernize their benefit packages for the fast-paced, global economy, the percentage of workers whose employers only offer defined contribution (DC) plans has swollen to 71% in 2013, up from just 12% in 1983. That’s not to say DC plans are any less effective; recent research shows that DC plans generate asset growth just as well as traditional pensions.3 But it does mean that individuals are in charge of their own retirement security more than they have been in the past.

Source: Center for Retirement Research at Boston College, http://crr.bc.edu/wp-content/uploads/1012/01/figure-15.pdf

What’s Going On: Since the 1980s, there has been a complete reversal in roles for who is responsible for planning for retirement. In the early 1980s, the most common retirement package included only a defined benefit pension. Now, employers are most likely to only offer a defined contribution plan, like a 401(k).4

Retirement preparedness isn’t the only savings objective affecting the middle class. According to recent Pew research, 41% of households lack the liquid savings to cover an unexpected $2,000 expense.5 Below we explore some of the more innovative ideas—in public policy, employer practices, and finance—that encourage people to save in retirement and nonretirement accounts.

Making savings automatic

Probably the most familiar mechanism used today to nudge people into saving more for retirement is auto enrollment. Countless studies have proven that when the default setting is to put a small percentage of a worker's paycheck into an employer-sponsored retirement plan, people save more.6 Automatically setting up employees to contribute a small percentage (often 3-4%) removes “decision paralysis,” which so often prevents people from saving anything at all.7 A feature proven to help people increase their savings is the step-child of auto-enrollment: auto-escalation, whereby companies automatically bump up workers’ contribution rates annually—or whenever they get a raise.

Another, more familiar method major banks are using to get people in the habit of saving more, not just for retirement, but more generally, is through “spend-to-save” programs. One example is Bank of America’s “Keep the Change” initiative (KTC). Each time a customer uses a Bank of America-issued debit card, KTC rounds up to the nearest dollar and automatically transfers the balance to a savings account. KTC was so popular at its outset that after only one year, 700,000 customers had opened up new checking accounts and 1 million signed on for the new savings account.8

As impressive as these numbers are, there is a limit to the effectiveness of spend-to-save given how little the change amounts to. Plus, studies have shown that when people use only their credit or debit cards when making purchases, the amount they spend increases by 10%.9 And, of course, if a purchaser carries a balance on a credit card that incurs interest, there are costs to that as well. A savings program that requires its users to spend money to reap the benefits may in fact fail to have a net-positive savings effect for some customers.

A not-so-distant relative of spend-to-save is a newer idea called Borrow and Save. This initiative, currently piloted by 14 credit unions, is reframing the way people interact with their local financial institution. Similar to spend-to-save, the goal of the program is to get people to build a modest, emergency savings account so as to avoid high-interest loans in an emergency.10 Borrow and Save works like this: if a customer needs $500 today, the credit union will lend him or her $500 plus anywhere from 5 to 50 percent more (depending on what the credit union’s savings target is). Assuming the credit union has a 50% savings target, the original loan amount would be $750, making $500 available to the borrower on day one and setting aside $250 in a locked savings account. Over a term that could last anywhere from a few months to one year, the borrower pays back the entire $750. Only after the full amount has been repaid does the borrower gain access to the $250 savings account. Given that credit unions have a national interest rate cap on loans of 18%, proponents say this program could serve as a viable alternative to payday loans.

The pilot program has proven successful enough that plans for an expanded rollout nationwide are in the works. Data from the pilot indicate that about one-third of the $3 million in assets lent out by the 14 credit unions was ultimately saved.11 Borrow and Save programs are still in their infancy so more comprehensive data on their effectiveness is unavailable.

Making savings fun

Consider this startling statistic: 16% of Americans believe that buying a lottery ticket should be considered a very important wealth-building strategy.12 While virtually no financial planners would condone such a strategy, many of them might endorse Prize-Linked Savings accounts (PLS). A fairly recent development in the United States currently running in six states, PLS accounts harness the excitement of lotteries while also getting people to stash away money and build wealth. PLS accounts are similar to traditional savings accounts; however, PLS accounts do not earn interest. Instead, that interest is pooled across PLS accounts and paid out through raffle prizes to handfuls of lucky participants. Regardless of whether or not the saver wins, the principal is preserved. Most savers end up with slightly less money than if they had bought government bonds, for example, but they are far better off than having bought losing lottery tickets.

As of December 2015, 15 states had passed legislation allowing the programs to exist.13 Given the infancy of these programs, the data on these programs’ success is limited; however, it is very apparent that PLS programs get low- to moderate-income people saving. According to one study, 75% of PLS enrollees have less than $5,000 in accumulated wealth.14 In the United Kingdom, similar products have existed since 1956 and are enormously popular. A 2006 study showed that 20-40% of U.K. citizens hold PLS bonds, which they call “Premium Bonds.”15 This accounted for nearly 4% of total household deposits in 2006.

Another set of innovations in personal savings comes from fintech (an umbrella term for innovative technologies and startups disrupting the financial services industry). Simple Bank began as a fintech startup and has since been gobbled up by BBVA Compass, the U.S. subsidiary of the Spanish mega-bank. Simple’s innovation is in the “gamification” of savings. After setting up an account, new customers are sent Simple debit cards and asked to download a smart phone application that acts as their banking hub. After customers answer a few questions about savings goals, the Simple app begins tracking spending as they use the debit card and makes it fun and easy for users to track how much they are saving. The tracking is so precise that the app alerts customers what dollar amount is “Safe-to-Spend” based on upcoming bills the customer has and how well the customer is performing on savings goals.

What’s Going On: The Simple “Safe-to-Spend” tool gives users an on-the-spot snapshot of how much cash they actually can use, all things considered (i.e. upcoming bills, rent, loan payments), so that if the user is considering a purchase, the app gives him or her a red or green light.

Simple’s CEO is rather tightlipped about his company’s success and effectiveness in getting users to save more. However, in a recent interview, he said that customer growth in their business has been so quick that if Simple were a traditional brick-and-mortar bank it would now “need 850 branches and 6,000 branch employees.”16 Also, in a 2014 blog post, prior to joining BBVA, Simple announced that it experienced 330% growth in 2013, serving more than 100,000 customers.17

Making savings accessible

In his 2014 State of the Union address, President Obama announced the launch of myRA (pronounced MY-RAH, rhymes with IRA), a program within the Treasury Department that aims to expand access to a retirement savings vehicle to millions of Americans.

The goal of myRA is to get Americans to start saving for retirement. An eligible saver (income less than $131,000 for an individual or $193,000 for couples) can create a myRA account with the U.S. Treasury. This account has no fees, no minimum balance requirement (often traditional IRA accounts have $1,000-$2,000 minimums), and a nondeductible Roth IRA tax status. Individuals can contribute up to $5,500 yearly until the account either reaches $15,000 in value or has been open 30 years. At that time, the myRA account must be rolled into a private-sector retirement account.18

The national rollout of myRA was in late 2015, so it is too early to evaluate its impact. Treasury has already conceded that myRA isn’t going to solve the retirement crisis. Rather, Treasury views myRA as a “starter account.” Secretary Jack Lew argues that when workers start to save, there’s a good chance they will continue to save.19 This is important because today, small-dollar savers are often so overwhelmed by the initial hurdles of getting started that they perpetually delay doing so. This is a classic behavioral tendency that can hopefully be corrected through an “on-ramp” like myRA that guarantees a return of principal and a sliver of interest, mollifying savers with loss aversion, and offers only one investment choice, helping along those with decision paralysis.

Another interesting development out of fintech involves a startup called Honest Dollar. Many small businesses choose to not offer 401(k) or similar traditional retirement plans to their employees because the administrative complexity is too great.20 The aim of Honest Dollar is to eliminate the hurdles associated with setting up and maintaining employee retirement accounts for small businesses. Its easy-to-use platform connects Honest Dollar to a small business’s payroll system and extracts the employee information it needs. Honest Dollar then does the administrative heavy lifting to get the employer’s retirement plan up and running.

When Honest Dollar was acquired by Goldman Sachs in early 2016, little was disclosed about the cost of the deal, how much Honest Dollar has grown, or the extent to which it has led workers to increase savings. However, Goldman did remark in a press release that by simplifying the burden small businesses face, Honest Dollar can expand employer-sponsored retirement plans to some of the 45 million American workers who currently lack access to them.21

Conclusion

For many households juggling myriad financial demands like college tuition, mortgage payments and other bills, actually saving money is a difficult task. Congress ought to look carefully and offer legislation designed to expand personal savings, both for retirement and nonretirement purposes. Third Way’s proposal for a minimum pension, for example, would substantially expand private savings for workers, by requiring a minimum 50 cent-per-hour minimum employer contribution to a retirement plan.22

But employers, banks, fintech startups, and federal agencies are showing that there are numerous innovative ways to guide ordinary Americans toward better savings habits, without legislation from Congress. As slow-moving as federal lawmaking can be, the refinement and expansion of these myriad efforts can make a significant difference.