Report Published April 21, 2016 · Updated April 21, 2016 · 14 minute read

Frontrunners: How the Fintech Revolution Is Reshaping Our Economy

Takeaways

- The term “fintech” encompasses technological innovation in any number of financial services, such as payments, insurance, lending, deposits, and raising capital.

- Fintech will revolutionize the way consumers spend and save money, allowing them more choices, more convenience, and lower fees. For businesses, fintech could mean quicker, easier access to the financing they need to expand.

- As have disruptive trends in other industries, fintech presents new challenges for regulators. They must allow enough space for innovation, while also protecting consumers from misleading products and cyber risks.

Five years from now, your whole world might be upended by a thing called “fintech”. If the geeks working at traditional banks and Silicon Valley startups have their way, you will no longer talk with a mortgage lender face-to-face to get a loan, but instead just download an app. If they have their way, check-out lines will be a thing of the past. If they have their way, your retirement investments will be made by a highly sophisticated algorithm. And if they have their way, you will receive your first small business loan without stepping foot in a bank.

Fintech is an umbrella term given to the innovative technologies and startups that are currently disrupting the financial services industry. Technology has been disrupting financial services for decades, but the trend has really picked up speed in recent years with the mass adoption of smart phones, advances in computing power, and the spread of big data.1 According to CB Insights, in 2014, investors poured nearly $14 billion into fintech, the culmination of a 46% year-over-year growth rate since 2010. Most legacy financial institutions are welcoming this disruption by forming partnerships with or acquiring startups, because the benefits to their customers are huge.2 This growth spans a vast array of financial services, but there are four areas that illustrate the extent to which the industry is both shaking up our economy and raising new regulatory questions: payments, robo-advisers, equity crowdfunding, and marketplace lending.

Whats Going On: A 2015 McKinsey study of the top 350 fintech startups shows how much revenue these companies have captured from the traditional players. Startups in financial assets and capital markets are modernizing trading platforms and tools used on Wall Street. Those involved in payments provide customers and merchants new tools for purchasing goods and sending money. Lending and financing startups provide new marketplaces linking lenders with borrowers and businesses with investors. And account management startups are changing how people save money.3

Four fintech frontrunners

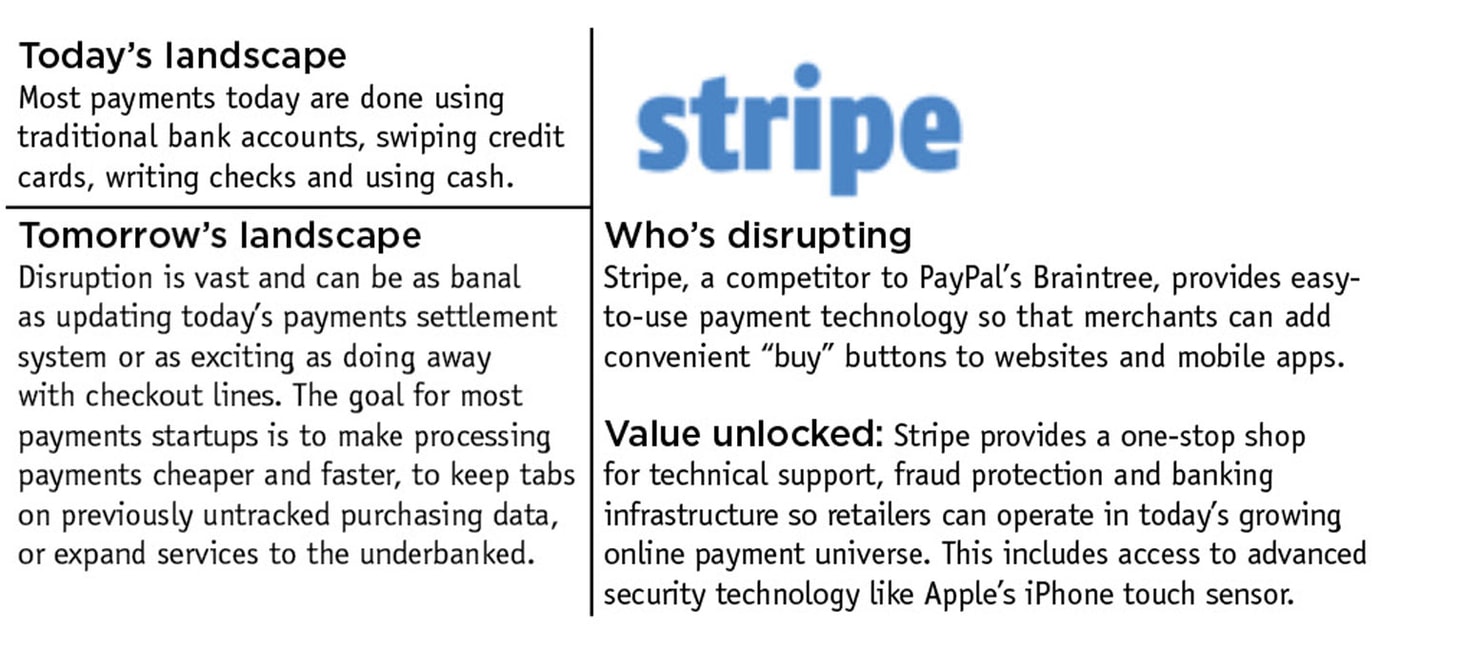

Payments

Source: “About Stripe,” Stripe. Accessed April 19, 2016. Available at: https://stripe.com/about. See also: Ari Levy, “The start-up that’s out to conquer global payments,” CNBC, May 7, 2015. Accessed April 19, 2016. Available at: http://www.cnbc.com/2015/05/07/stripe-expands-into-asia-latin-america.html.

Today, payments represent the biggest disruption in finance. This stems largely from the mass adoption of smart phone technology and the ease with which programmers can create new apps.4 The payments revolution really comes down to changes in two distinct categories: first, the customer-facing elements of payments; and second, the settlement process, which centers on the technology blockchain.

The first encapsulates the most recognizable brands in fintech today. These are ventures that allow consumers and retailers to transact in new ways, whether online (PayPal), mobile phones-to-retailer (Apple Pay), mobile phone-to-mobile phone (Venmo), or credit card-to-smart device (Square). Fundamentally, these technologies make payments more convenient—you can leave your wallet at home or pay online with just a couple clicks. And the competitiveness they bring to the payments industry stands to lower transaction costs for businesses and consumers alike.

To date, a key federal regulator for fintech startups has been the Federal Trade Commission (FTC).5 Under the Gramm-Leach-Bliley Act (1999), the FTC requires financial institutions to secure customer records and information.6 But with the passage of Dodd-Frank, greater oversight has been afforded to the Consumer Financial Protection Bureau (CFPB). One example of this came in early 2016 when the CFPB enforced a data protection penalty on Dwolla—a fintech payments company.7 Even though the $100,000 penalty was considered small, it signaled that the CFPB believes FTC regulation alone isn’t enough for mobile payments.8 Additionally, the Treasury’s Office of the Comptroller and Currency (OCC) has brought further regulatory competition to the FTC. As the chief regulator of federally chartered banks, the OCC released a March 2016 white paper on ways banks can allow “responsible innovation” across fintech (not just payments).9 Given these moves by regulators, the message is clear inside Washington: agencies are just beginning to sort out who will regulate payments and how.

The second function of payments is the back-office function. Today’s payment settlement system uses decades-old technology. Typically, with large value transfers, a sender asks its bank to transfer an amount to a specific address (using BIC and IBAN codes). Automated clearinghouses send secure messages back and forth between the two banks before the value is transferred. The upside of this system is that it is predictable and secure, thanks to the role of highly trusted clearinghouses. The downside of this system is it can take days to settle a payment between two banks.

Enter blockchain—the foundation of bitcoin—which has the ability to speed up settlements from slow to instantaneous. Blockchain technology is referred to as a distributed ledger, which eliminates the need for a central intermediary. It does so by using a bookkeeping system on multiple connected computers that record every transaction. Right now, blockchain is used almost exclusively for bitcoin transactions. However, some speculate that financial services companies could adopt blockchain for limited products and functions within two years.10 The earliest application of blockchain could include syndicated loan markets, trading in private companies, smart contracts to support trade finance, and inter-firm payments.

One benefit of blockchain technology is faster payments and settlements, which would reduce transaction costs and significantly help people living paycheck to paycheck. If workers did not have to wait up to five days for a bank to process a check, they would be less likely to rely on high-fee check cashing services to access their money.11 Another benefit of decentralized payment and recordkeeping systems like blockchain would be a more complete record of transactions. This could eliminate many payment dispute problems and allow for greater market transparency and oversight. At a recent conference held on decentralized payment systems, a CFTC commissioner speculated that the Lehman Brothers collapse could have been avoided if a decentralized payments record had existed.12

On the other hand, there is reasonable concern about fraud and consumer protection under a decentralized payment system. New blockchain-based payment and settlement systems will need to meet the same standards of “know your customer,” anti-money laundering, client asset protection, and regulatory reporting as do existing financial services providers. And blockchain-based transactions and payment systems will need to be integrated with the compliance, risk management, and operational risk controls that are in place for current financial markets processes.

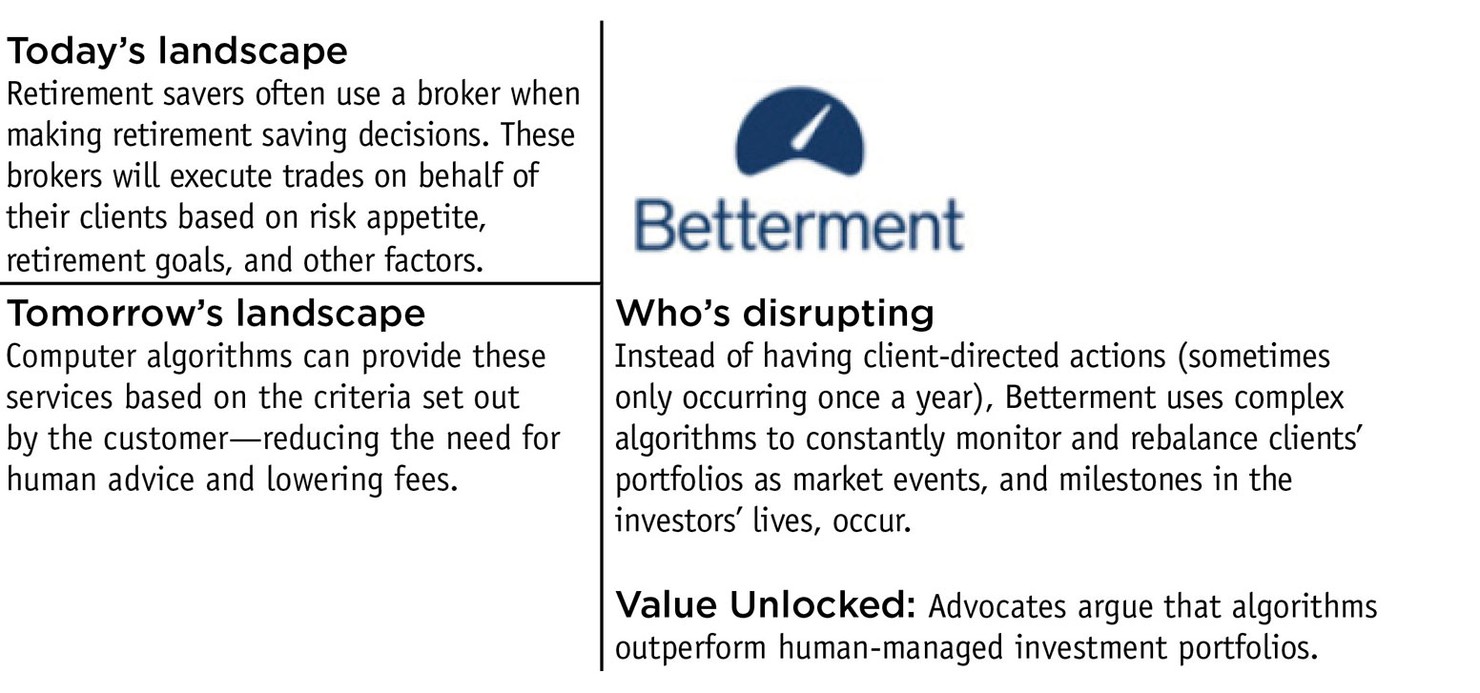

Robo-advisers

Source: Vanessa Page, “How Does Betterment Work and Make Money?” Investopedia. Accessed April 4, 2016. Available at: http://www.investopedia.com/articles/investing/081115/how-does-betterment-work-and-make-money.asp.

Today, not enough people are saving what they should for retirement. As a result, half of working-age households are at risk of failing to maintain their standard of living during retirement, according to economist Alicia Munnell.13 So doing everything possible to make saving for retirement easier and more affordable is a high priority for most policymakers. And robo-advisers may be part of the solution.

Robo-advisers are online financial services companies that manage investment portfolios. Two leaders in this space are Betterment and Wealthfront. These companies use algorithms to personalize an investment portfolio—the mix of stocks and bonds, for example—based on the customer’s age, assets, risk appetite, and other factors. Having an algorithm do the work, instead of human financial advisers, allows robo-advisers to offer fees lower than those of many traditional competitors. Interfaces can range from completely online and automated to others that offer occasional video chats with human advisers.

For workers who aren’t saving because taking the first step of setting up an Individual Retirement Account (IRA) seems too daunting—or because choosing the right mix of investments is overwhelming, robo-advisers may help get them in the game. And once they’re in, robo-advisers may help savers keep saving enough and maintain a portfolio balance that makes sense. There isn’t evidence yet that robo-advisers are changing savings behavior in aggregate, but one thing is clear—the amount of assets with robo-advisers is growing very fast. Even though total robo-adviser assets across the industry amount to only $20 billion (compared to the $17 trillion—with a T—for traditional managers), this number has been doubling every few months.14

Robo-adviser assets are held by third-party depository banks, which means that if the robo-adviser were to go under, its customers would not lose their investments. Moreover, robo-advisers are registered with the SEC as advisers and their service is considered “investment brokerage,” which exempts them from regulations pertaining to traditional broker-dealers.15 In late 2015, SEC Commissioner Kara Stein called for robo-advisers to be held to the same standards as human financial advisers.16 Yet, a recent decision by the Department of Labor (DoL)—the fiduciary rule—declines to apply financial adviser rules to robo-advisers, so long as their investment advice is generated solely by a website’s algorithms.17 The new DoL rule favorably concludes that “the marketplace for robo-advice is still evolving in ways that both appear to avoid conflicts of interest … and minimize cost.”18

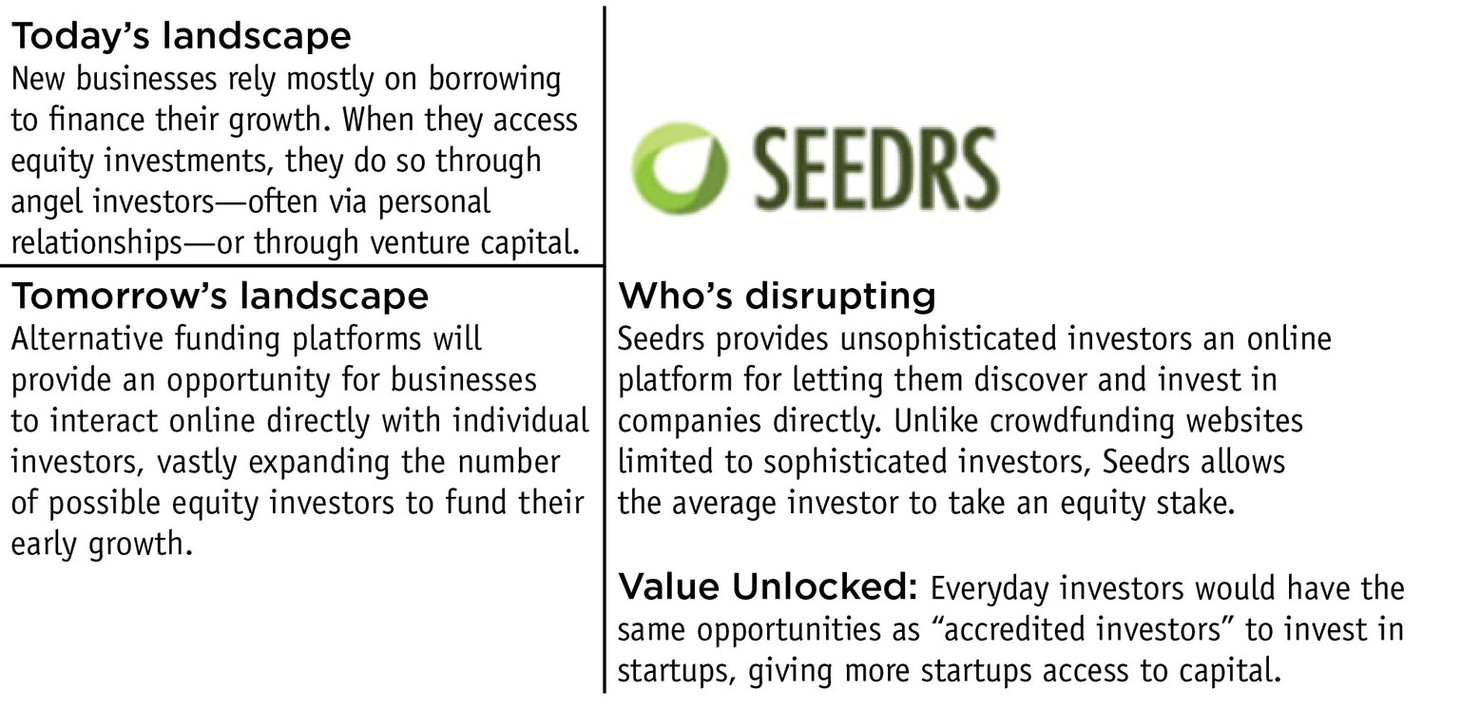

Equity crowdfunding

"Seedrs to launch in the United States following approval of JOBS Act Title III rules,” Bankless Times, November 2, 2015. Accessed April 4, 2016. Available at: http://www.banklesstimes.com/2015/11/02/seedrs-to-launch-in-the-united-states-following-approval-of-jobs-act-title-iii-rules/.

New, small businesses do not raise very much of their capital through equity.19 Instead, owners of these companies use debt, taking out business and personal loans, maxing out their credit cards, and even borrowing money from friends and family. The limited nature of the market for small business capital is why equity crowdfunding is one of the most closely watched spaces in fintech.

When new businesses do obtain early equity investments, they typically come from angel investors or a venture capital fund. The problem with these sources is that they often require a business owner to have a prior business relationship with one of these specialized investors, which leaves many promising new businesses on the sidelines.

This is where equity crowdfunding sites, like Seedrs and AngelList, come in. If you’re an investor who wants to own part of a startup, but don’t know where to look, you can go on to AngelList, form a “syndicate” with other investors, and buy into businesses looking for capital. However, longstanding securities laws have meant that investors may only buy equity in private companies like this if the investors are accredited, which requires a net worth of $1 million or income over $200,000 a year. The idea is that unregistered companies disclose less information, are therefore riskier, and suitable only to wealthier people who can bear the risk.

In an effort to expand equity crowdfunding to more investors, Congress in 2012 passed the Jumpstart Our Business Startups Act (or JOBS Act).20 Among other goals, this law aims to significantly expand the number of people eligible to invest on crowdfunding sites. At the end of 2015, the SEC completed its rule for equity crowdfunding, paving the way for fintech companies to ramp up these marketplaces.

Yet the SEC’s rule reflects that the regulator is skeptical about how much trust can be placed in ordinary, inexperienced investors. Is the “crowd” able to weed out the good investments versus the bad? Moreover, individual investors may not fully understand the risks associated with even the most promising seed-stage investments, which makes fraud a real concern. One way the SEC is trying to protect investors is by capping the total amount of capital any one company can raise through crowdfunding at $1 million per year.21

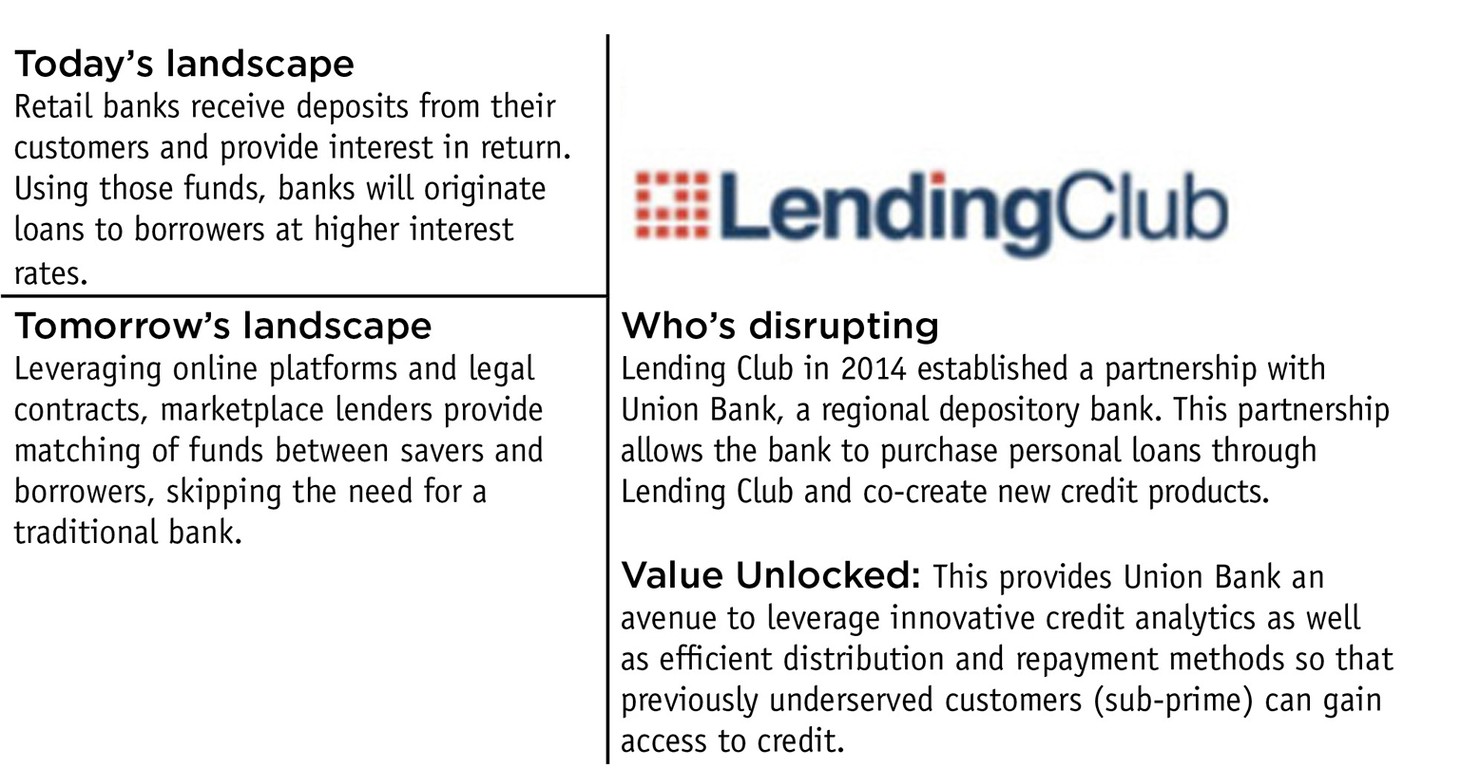

Marketplace lending

Source: JD Alois, “Lending Club & Union Bank Create Strategic Alliance,” Crowdfund Insider, May 5, 2014. Accessed April 4, 2016. Available at: http://www.crowdfundinsider.com/2014/05/37778-lending-club-union-bank-create-strategic-alliance/.

For your typical consumer or business, traditional retail banks have been the main conduit for borrowing and lending. Retail banks have physical branch locations with bankers that interact with customers. They are heavily regulated by multiple state and federal agencies, in order to guarantee depositors that their money is secure. The costs of branches, staff, and regulatory compliance have also meant that in order to make a profit, banks must lend money at interest rates well above the rates they offer depositors. This, along with a general lack of credit availability for small businesses, is the motivation for marketplace lending, sometimes also referred to as peer-to-peer lending or online business lending.22

By using an online platform, marketplace lenders like Lending Club can connect lenders and borrowers more efficiently, often leading money out to borrowers with narrower spreads than those used by retail banks—resulting in more favorable rates for the borrower. For lenders, these platforms are appealing because they offer the flexibility to pick and choose a desired risk portfolio. Plus, they gain an edge over traditional banks by offering loan decisions more quickly. Thanks to sophisticated algorithms that determine creditworthiness, applicants for a loan simply fill out an online form and can get a decision instantly. Compare that to traditional banks, which can take weeks to make a decision on a business loan application. As a result, marketplace lenders are quickly filling a void in the area of small business lending.

Marketplace lenders are subject to an extensive web of federal and state laws. These laws cover solicitation of the offering and prohibit credit discrimination and deceptive practices.23 The SEC is heavily involved in regulating marketplace lenders. When they arrived on the scene, most viewed marketplace lenders as simply venues where borrowers and savers are matched. This isn’t quite the case today. Most funders of these loans are big institutional investors that will buy up large pools of loans. In 2008, the SEC took note and issued a cease-and-desist order to Prosper—a marketplace lender—labeling its notes as securities.24 As a result of this order, all marketplace lenders became subject to securities laws.25

A recent Second Circuit Court of Appeals decision (Madden v. Midland Funding) may present a significant setback for marketplace lenders.26 The decision limits the ability of non-depository institutions to bypass state usury laws—something they previously pulled off by partnering with banks. 27On the other hand, it is possible that crowdfunding provisions of the JOBS Act will ease securities laws pertaining to marketplace lenders, allowing even faster growth in this variety of fintech.28

Conclusion

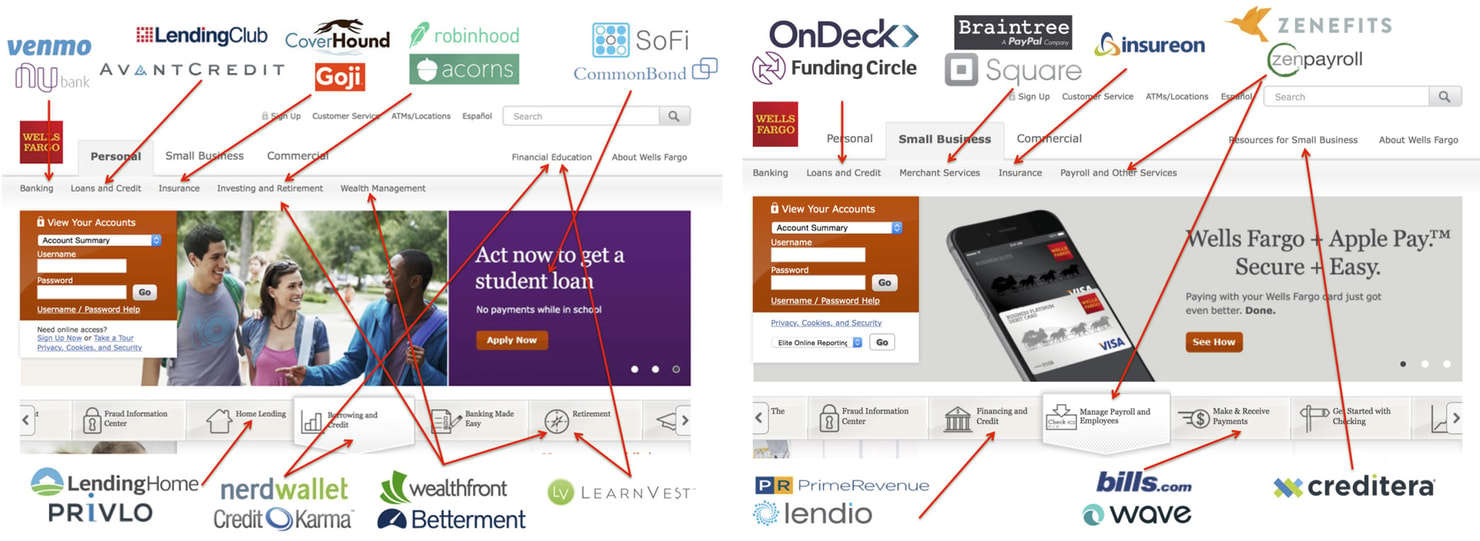

Venture capitalist Tom Loverro recently posted on his blog a screenshot (see below) he took of Wells Fargo’s homepage. Loverro drew arrows pointing to every service for which a fintech startup is competing with the mega-bank.29 There are 21 arrows. Five years out, will today’s startups have joined—or displaced—Wells Fargo as mega-providers of financial services?

Tom Loverro, Up & Right, November 16, 2014. Accessed April 4, 2016. Available at: http://tomloverro.com/day/2014/11/16.

The Kenyan economy provides a window into how much change can happen in consumer finance in just a few years. In 2007, Kenya’s biggest mobile phone carrier, Safaricom, launched a service called M-PESA. At that point most Kenyans didn’t have a bank account, and they still don’t. But now, 80% of Kenyans have basic cell phones. And with those phones, they can send money, withdraw cash at one of tens of thousands of small kiosks, or pay directly for goods or services. M-PESA, unlike the emerging smart phone apps Americans use to send their friends money, does not require a bank account.

The fast adoption of the technology was in part due to Kenya’s low bar for disruption; the limited reach of its banking sector meant few incumbent institutions and large, unmet demand for services. A November 2015 60 Minutes report labeled the technology transformational for its economy.30 Even though the M-PESA transformation is unlikely to occur here at the same pace, there is still a dramatic shift underway. If lawmakers and regulators can make sure the shift keeps moving, while maintaining consumers’ financial safety and security, it won’t be long before the United States finds its own M-PESA.