Report Published January 20, 2011 · Updated January 20, 2011 · 15 minute read

Saving Social Security

In 2015, taxes won’t cover Social Security payments. In 2025, total income for Social Security will be less than total outlays. In 2035, Social Security will take in $500 billion less than it pays out. In 2045, the Social Security Trust Funds will be $8 trillion in arrears.1 In short, without changes, the inter-generational promise of Social Security—our nation’s most important social insurance program—is a false one.

But reform of Social Security must also be addressed in a larger context. According to the Congressional Budget Office, we are expected to average only 2.1% GDP growth over the next twenty years, yet in 2030, the U.S. government is also projected to spend sixty-eight cents of every federal dollar on Social Security, Medicare, Medicaid and interest on the debt. In 1990, it was forty-four cents. In the sixty years following World War II, we built and sustained Social Security on an economy that averaged 3.4% annual growth. Now, our projected combination of anemic growth and consumption-led budgets could well spell a loss of American greatness.

In a vacuum, we could in theory continue raising payroll taxes to keep up with the baby boom retirement. But those tax and spending decisions affect the entire U.S. economy and budget. Left unchecked, these trends will leave a small portion of our federal budget devoted to education, innovation, infrastructure and national defense, squeezing our badly needed public investments and jeopardizing our security. To avert this coming crisis, Social Security reform must be achieved principally through savings in benefits, not tax increases, as we seek to rebalance the long-term U.S. budget toward investments and economic growth.

This idea brief summarizes the trouble with Social Security, and proposes a “Savings-Led” Social Security reform plan that actually increases the program’s progressivity. Our plan makes roughly two dollars in benefit reductions for every one dollar in revenue increases, and achieves solvency while enhancing economic growth.

THE PROBLEM

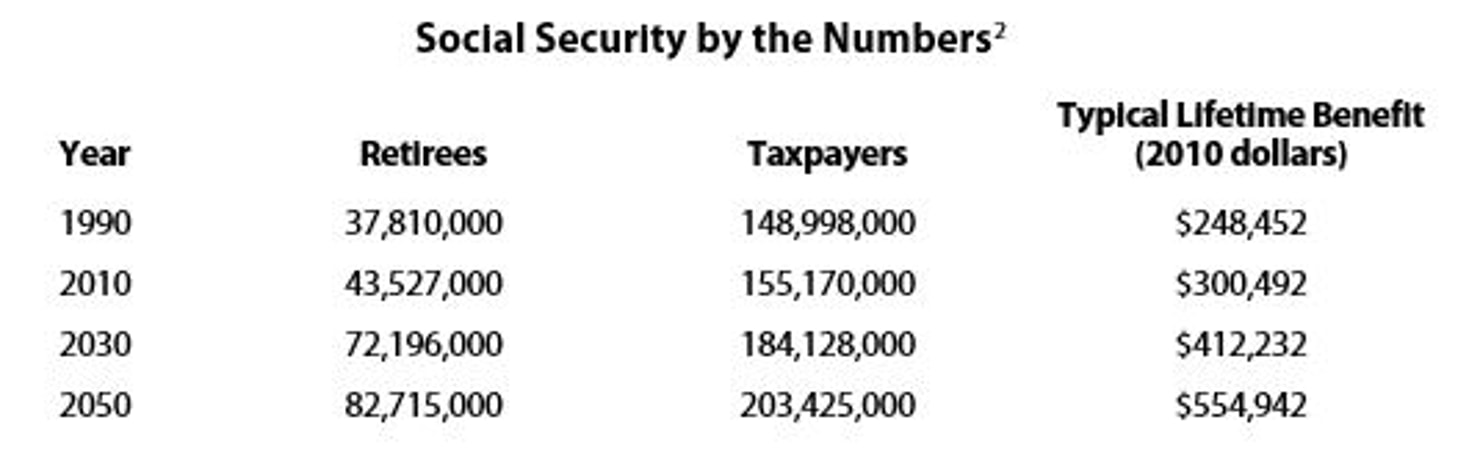

Social Security as we know it will cease to exist without changes

Chart endnote: 2

Social Security is on an unsustainable path. Under current law, the gap between income and payments will reach $500 billion in 2035, one trillion dollars in 2042, and two trillion dollars in 2051. Under changes made in 1983, the Trust Funds have been growing and will continue to grow for four more years. But that will end as more and more baby boomers retire. Anyone who hopes to be alive in 27 years won’t receive their promised benefits because the Trust Funds will be completely depleted.

The math is inexorable. Over the next 40 years, the number of retirees will nearly double. Their benefits will increase by 85% in inflation-adjusted dollars. And the number of taxpayers to pay for all this will increase by only one-third.

Here are the facts behind these numbers.

First, because the initial benefit for retirees is based on wage growth and because wages traditionally grow faster than inflation, there has been a slow rise in benefit payments over the years. For example, between 1975 and 2008, wages grew on average 0.3% faster per year than inflation. Over time and across millions of beneficiaries, that adds up to billions, and eventually trillions, of dollars in gains for retirees. That is why the average yearly benefit for a newly retired senior will be about 30% higher, in real terms, in just 20 years.

Second, senior citizens are simply living longer. A sixty-five year old in 1990 was likely to live to 82. A sixty-five year old in 2050 will likely live to 86, if current trends in mortality hold. Higher average benefits combined with more years collecting them add up to trillions in additional obligations for Social Security over the coming decades.

Finally, these trends would be more manageable if a third and crushing trend was not in evidence. The ratio of senior citizens to taxpayers is growing worse by the year. The Census Bureau projects that over the next twenty years, the number of Americans between the ages of 25 and 59 will increase by 8%, while the number of Americans seventy and above will increase by more than 80%. The way Social Security and Medicare works, those over 66 are almost completely paid for by those in the 22 to 64 age group, and really mostly by those between 25 and 59. In 2010, there were 3.5 taxpayers per Social Security recipient. By 2030, the ratio declines to 2.5 per beneficiary and holds constant for several decades.

THE SOLUTION

A Savings-Led Solution to Saving Social Security

There are many on the progressive side who believe the Social Security shortfall should be solved through the elimination of the earnings cap on FICA collections. Currently, 6.2% of wages up to a cap of $106,800 are siphoned off from both the employer and employee to provide the bulk of the funding of the Social Security Trust Fund. This wage cap is indexed to overall wage gains.

We have deep concerns about complete repeal. While we support higher taxation on upper income individuals and accept that some of it must be used to bail out entitlements like Social Security, we believe the bulk of increased taxation would be best spent on growth-oriented investments in infrastructure, education, innovation, and the like.

Moreover, against the back-drop of projected anemic U.S. economic growth projections, we believe that Social Security reform must be achieved in the context of an entitlement system that is dangerously on auto-pilot.

As noted in the summary section, in 1990, forty-four cents of every federal dollar was spent on the pure consumption line items of Medicare, Medicaid, Social Security, and interest on the debt. In 2030, sixty-eight cents of every federal dollar will go to those four budget items.3 In 2015, Social Security payments are expected to represent about a 4.9% share of the nation’s GDP; by 2035, it reaches 6.2% of GDP.4 We do not believe that the U.S. economy can thrive with roughly seven-tenths of every federal dollar paying for three entitlement programs and Chinese holders of U.S. debt. And we are similarly concerned that a 25% jump in the share of GDP devoted to Social Security is unhealthy for the economy.

Repealing the cap would represent a failure to make any choices about entitlement spending except to ignore it. It would drive the top federal tax rate that employees pay on salaries to nearly 50% without doing anything to address any other pressing spending need. It would leave little, if any, room for taxes on the wealthy for growth-oriented investments, let alone dealing with shortfalls in Medicare.

Thus, two-thirds of the funds for our plan to save Social Security come from reducing future outlays and spreading it out with modest changes over several generations. The changes we proposed on the revenue side are no less important because they would not hinder economic growth or place any additional burden on the middle class or those that employ them. Finally, our challenge was to devise a reformed system, led by savings, that protected low income senior citizens—those who rely heavily on their payments to live a dignified life in retirement. We believe we have achieved that goal.

Third Way’s proposal for incremental benefits changes and minimal revenue increase would make Social Security solvent over the next 75 years. Our plan would reduce spending by roughly $2 for every $1 in revenue increases. It would create added value for low income seniors.

In many respects, our proposal is similar in spirit and in many of the details to the reforms proposed by the co-chairs of President Obama's Fiscal Commission, Erskine Bowles and Alan Simpson. It, too, calls for a savings-led solution, and we believe the co-chairs have done a great service to the debate through their proposal.

The Major Elements of the Third Way Social Security Plan:

- Change formula to increase benefits for low income seniors

- Raise retirement age to keep pace with longevity

- Use more accurate inflation measure for COLA increases

- Reduce FICA payments for working seniors

- Create Plus accounts for young workers to supplement retirement savings

- Make all benefits subject to taxation for high income seniors

- Means-test and eliminate benefits for very high income seniors

- Increase the amount of wages subject to FICA to 90% of aggregate salaries

- Increase high-skilled immigration levels

- Bump up FICA contributions for certain temporary and undocumented immigrant

Part I of the Third Way Plan: Incremental Benefit Changes

Three areas of Social Security benefits can create the needed savings. These changes are incremental and build on past solutions or well-established policy ideas. All but one would affect future retirees to give them time to adjust. The impact on current retirees would be less than the cost of dinner out for a couple once a year.

More progressive benefits. The Social Security benefit formula should be weighted more heavily to benefit lower income seniors. As part of our belief that Social Security should fulfill its mission as a social insurance program, we would adjust the primary insurance amount formula to benefit lower income and lower-middle income seniors more.5 We would change the primary insurance amount from 90% to 95% in the first bend point; decrease it from 32% to 31% in the middle bend point, and from 15% to 12% in the third bend point. A lower income retiree with average earnings of $25,000 would receive benefits $297 greater in their initial year than today, in real dollars. A middle-income retiree with average earnings of $54,792 would receive the same benefit as before. A higher-income retiree with average earnings of $75,000 would receive a benefit that is $419 less. We estimate that these changes are essentially revenue neutral.

More accurate COLAs. Social Security payments (as well as all inflation-adjustments throughout government) should be adjusted annually using a chain-weighted consumer price index (CPI). Chain-weighting CPI lowers the cost of living adjustment for retirees by approximately 0.3%, according to the Congressional Budget Office.6 Chain-weighting assumes that when the price of one product becomes too high, consumers will substitute for a cheaper product if it’s available. For example, if the price of orange juice increases because of a crop failure in Florida, people will switch to apple juice. This is considered a more accurate measure of inflation. It has a small affect on individual benefit levels, reducing payments in year two by about $4 per month for a senior earning $15,000 in benefits in their first year of eligibility. In their seventeenth year of eligibility, that senior would receive about $86 less a month than under the current formula. Thus, every senior citizen will contribute something to the saving of the Social Security Trust Fund. In keeping with its mission as a social insurance program, seniors with larger benefits will contribute more. In the aggregate, this will reduce total benefit payments by roughly $2 trillion by year 2040 (approximately 4% of total Social Security spending).7 Chain-weighting CPI is projected to close roughly one-third of the seventy-five year shortfall for Social Security.8

Later retirement age. The retirement age to receive full Social Security benefits should be adjusted and raised. From 1980 until the present, the retirement age—either by design or by accident—has been pegged to an average life expectancy of between 17 and 18 years.9 That is, when the retirement age was 65, the typical retiring senior was expected to live until the age of 82 or 83. Gradually, the retirement age for Social Security is scheduled to increase to 67 by 2027. At that point, there is no scheduled change in the retirement age. We suggest pegging the future retirement age for full benefits to 17.5 to 17.75 years of life expectancy. This would put the retirement age in line with recent historic precedent.

According to the Congressional Budget Office, increasing the normal retirement age gradually from 67 to 70 would still allow median lifetime benefits to increase by $110,000 from the benefit level for parents in their 50s today to benefit level for their 10-year-old kids, in real dollars.”10

Under our plan, the retirement age would gradually increase to 68 from 2036 to 2041, to 69 from 2054 to 2059, and to 70 from 2072 to 2077. This would reduce total benefits by roughly $1 trillion by 2040 (approximately 2% of total Social Security spending) with significantly more savings in future years.11 Pegging the retirement age to longevity will close slightly more than one-third of the seventy-five year shortfall for Social Security.

Work rewards for seniors. Seniors who work later in their lives because they want to or need to should be able to keep more of their wages. There is little reason for them to keep paying Social Security taxes because it makes little difference in their benefits.12 And by accepting a later retirement age, they are doing their part to reduce Social Security’s shortfall. Cutting Social Security taxes in half for seniors who work past the normal retirement age would reduce revenue somewhat, but it would be paid for by the savings from the other provisions of this proposal.

Social Security Plus Accounts. Private retirement savings must be encouraged and increased at a young age. Our plan dedicates $8 billion dollars per year to private retirement accounts for people in the workforce and under the age of 30. The federal government would provide up to $500 in matching grants to employer and/or employee contributions to a 401k-style retirement account. The funds would come from an increase in the Estate Tax and would encourage retirement savings for people at a young age to create a culture of savings and to give modest early accounts time to accumulate.

Part II of the Third Way Plan: Revenue Increases

We estimate that the changes in benefits will eliminate approximately two-thirds of the 75-year shortfall. The remaining third is made up of financing changes to increase revenue into the Trust Fund and miscellaneous changes described further below.

Benefit taxes on higher income seniors. All Social Security benefits should be taxed as income for high-earning senior citizens. Currently, 85% of benefits are taxable for individual seniors with $34,000 and senior couples with $44,000 in outside income. To further Social Security’s mission as a social insurance program, we would allow 100% of benefits to be taxed for individual seniors with $50,000 and senior couples with $60,000 in outside income. As under current law, these funds would be put back into the Trust Fund.

Means-tested benefits. Social Security benefits should be means-tested and eliminated for very high-earning senior citizens. Social Security benefits would be phased out between $150,000 to $250,000 of outside income for individual seniors and $200,000 to $400,000 for senior couples. To further its mission as a social insurance program, those who should not need social security at all, should not receive it during their high-income years. These two tax changes would add about $500 billion in new revenue to the Trust Fund by 2040.

Payroll tax increase on higher income employees. Additional FICA payments should be collected for individuals and employers with earnings above the current taxable limit of $106,800. There are several possible options that would all raise roughly the same revenue while keeping the FICA payment at 6.2% of payroll for individuals and businesses up to the current cap of $106,800—adjusted for wage growth:

- Increasing the payroll tax cap so as to cover 90% of workers’ earnings. Over the years, the payroll tax cap has covered a declining share of workplace earnings. Raising the cap to roughly $190,000 by 2020 would re-establish the 90% benchmark and cover nearly one-third of the Social Security solvency shortfall.

- A new 6.2% FICA “donut hole” payment on individuals and businesses earning between $300,000 and $500,000. Thus, individuals and businesses would pay a 6.2% FICA rate on income earned and paid up to $106,800. They would pay zero on income from $106,800 to $299,999. They would once again pay 6.2% on income between $300,000 and $499,999. And they would pay zero thereafter. This would raise an additional $1.2 trillion by 2040.13

Immigration reform. FICA contributions should be increased through certain temporary immigrant worker programs. As part of immigration reform, we suggest placing a 10% FICA surcharge on H2A and H2B temporary immigrant visas. This 10% employer-paid surcharge would replace the paperwork requirements under the current statute to ensure that these low-skilled jobs are offered to American citizens. The 10% surcharge would help guarantee that non-citizen immigrant labor does not undercut citizen wages. Replacing the paperwork would end the bureaucratic hurdles that simply slow down employers and do little to prevent Americans from losing their job. Assuming 250,000 temporary workers earning an average wage of $12,000, this would raise an additional $75 billion by 2040.

In addition, FICA contributions should be increased for current undocumented workers on their path to legality. As part of immigration reform, we suggest placing a 2% FICA-fine on undocumented workers as they earn a path to legality. The fine would be on employer wages only and would be paid for ten years, and would raise an additional $40 billion by 2040.

Lastly, legal Immigration levels should be increased by 3 million above projected levels through 2040. As part of immigration reform, we suggest increasing the quota of illegal immigrants by 100,000 per year and dedicating those new immigrants to high-skilled individuals—those who have either earned a graduate degree from a U.S. university or qualified for an H1b visa. This would raise an additional $400 billion by 2040.

Conclusion

Under our plan, Social Security would be ready to thrive as a centenarian and well beyond. Every senior citizen with the exception of the very, very wealthy would receive more in benefits in inflation-adjusted dollars than they do today. Low income seniors, for whom Social Security is the difference between dignity and despair, would fare the best. And tax increases could be reserved for funding areas of growth and investment. It is possible to have a savings-led Social Security solvency plan that would make Franklin Roosevelt proud.