Report Published September 29, 2010 · Updated September 29, 2010 · 9 minute read

Reforming Federal Pensions

For an updated overview of this issue, please see our Frequently Asked Questions about Federal Retirement Reform memo.

Federal employees enjoy one of the most generous retirement plans in the country. One major part of their benefits—the Federal Employment Retirement System— has the patina of budget neutrality. FERS is financed completely through contributions to ensure that there will not be shortfalls when federal retirees receive their pension. But because of a quirk in the law dating back to 1986, contributions into the system are skewed dramatically against the taxpayer. For every one dollar that is contributed into FERS by the employee, $14 is contributed by the employer, the taxpayer. If employers and employees contributed equally to the fund as is often the case in the private sector, taxpayers would save $114 billion over ten years and $271 billion over twenty—without affecting federal pension benefit payouts.

THE PROBLEM

Financing the federal retirement system is more expensive

than it should be.

Federal retirement is funded through an antiquated formula.

Since 1987, federal employees including members of Congress have had the benefit of three guaranteed income payments in their retirement. First, like nearly all other workers, they receive Social Security. Second, like many workers, they have a 401k-style plan with an employer match (known as the Thrift Savings Plan or TSP). And third, like most public sector workers, they also receive a traditional pension through a system known as FERS (the federal employment retirement system).

This three-legged retirement system is more generous than what most other middle class families receive in retirement, but it is not opulent.1 It guarantees a comfortable, though not luxurious, retirement for long-term federal employees.

In 1986, Congress enacted FERS to replace a long-standing federal pension program known as CSRS (civil service retirement system). CSRS was more generous to employees than FERS, but with a catch. CSRS recipients did not receive Social Security and they did not contribute to Social Security payroll taxes. In 1983, as part of an effort to shore up the Social Security Trust Fund, new federal employees were placed in a new federal retirement system and they began contributing to Social Security through FICA, the payroll taxes that nearly all employees pay. This was the beginning of FERS.

At the time, lawmakers decided that the new FERS and existing CSRS employees would contribute the exact same amount for their retirement—including FICA contributions. At the time, CSRS employees contributed 7% to their retirement and so did the taxpayer. Because FERS employees would now contribute 6.2% to FICA, the new law limited the employee contribution to FERS to 0.8% of wages. And because Congress required FERS to be completely self-financed, all of the remaining contribution is made by each federal agency for its employees. This works out to 11.2% of federal employee wages, or $14 contributed by the employer for every one dollar that is contributed by the employee.

It is questionable whether there ever needed to be parity between CSRS and FERS workers in the first place, but it is absolutely unnecessary today. Only federal workers employed before 1984 are eligible for CSRS. Four out of every five federal employees today are under FERS and very soon they will all be under FERS. The problem meant to be solved by the parity requirement between CSRS and FERS no longer exists.

Private retirement plans usually split the bill evenly between employers and employees.

Social Security is funded by employers and employees each paying 6.2% of wages into the system. Under private 401(k) programs, employers and employees each make a matching contribution into an individually-directed retirement account. Federal employees and the government make matching contributions of up to 5% of wages each under the Thrift Savings Plan; most private companies don’t match as much.2 And while the costs of a traditional defined benefit pension plan such as FERS are often hidden from the employee, the cost is essentially shared. According to the Department of Labor, about 52% of all private sector pension funds (taking into account defined benefit and defined contribution plans) are contributed by the employer and 48% by the employee.3

FERS is unnecessarily expensive for taxpayers.

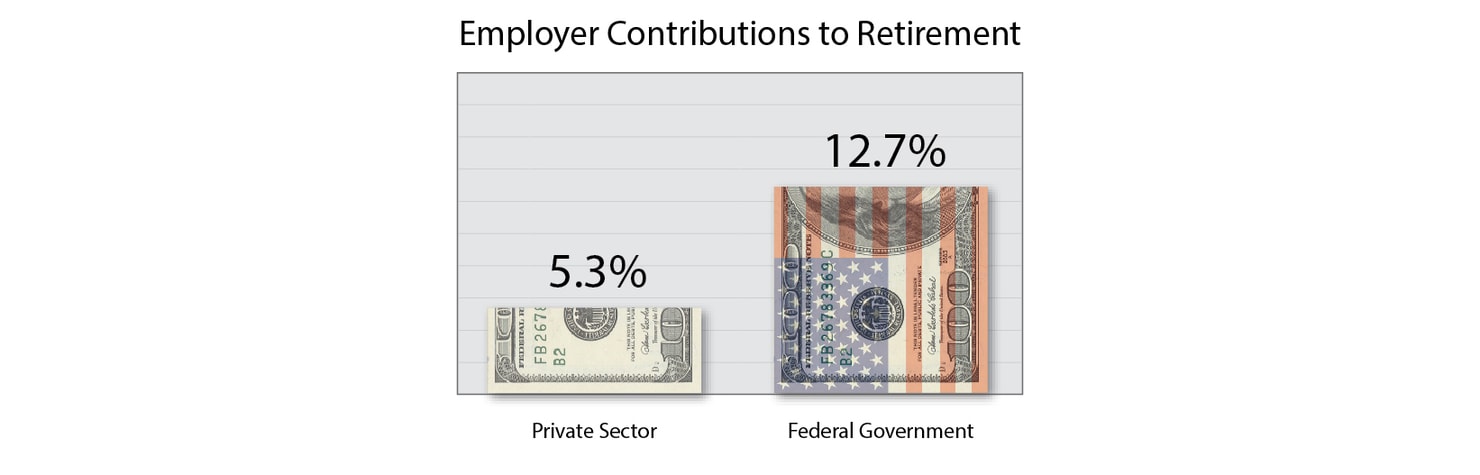

By themselves, neither FERS nor the Thrift Savings Plans differ much from their private sector counterparts. Together, however, they are much more generous than retirement packages offered by comparable private sector employers. Today, the federal government contributes a total 12.7% of wages to FERS and the Thrift Savings Plan. By comparison, private employers in similar sectors of the economy (e.g., management, professional services, and information businesses) contribute 5.3% of payroll for their workers’ retirement as show in the chart below.4 This comparison also takes into account the older age of the federal workforce, which is nearing retirement sooner and requires higher pension funding levels.5

Over the next ten years, taxpayers will contribute more than $263 billion to fund FERS, which is considerably more than what the federal government spends on college financial aid through Pell grants.6 Over the next twenty years, taxpayer contributions will reach roughly $626 billion. Employee contributions are miniscule—less than $20 billion over ten years and less than $50 billion over twenty years.

THE SOLUTION

Modernize FERS to make employers and employees equal partners.

If employers and employees were to contribute equally to FERS, taxpayers would save $114 billion over ten years, $271 billion over twenty years, and $702 billion by 2050.7

This sends an important message to the public: Congress and Feds will take the first hit.

If we are going to achieve meaningful fiscal discipline, Congress, the White House, and the federal government must take the first step and take the first significant cuts as an example to the rest of the country. Third Way polling shows that three-fourths of Americans believe that cutting government spending and getting rid of government waste is the key to balancing the federal budget.8

Federal employees will still receive fair treatment for a comfortable retirement.

Pension benefit payouts will not change whatsoever. Today, a federal employee who works for 30 years and retires with an average “high-three”* salary of $70,000—about the average wage of a federal employee—would:

- Receive a yearly pension of $23,100 that increases at CPI minus 1% each year, just as today.

- Receive Social Security payments of approximately $24,000 that increases by CPI, just as today.

- Have a TSP nest egg that would create an annuity of about $20,000 per year, just as today.

*Federal pension benefits are determined by a simple formula. It equals the average salary of the three most lucrative years of a person’s federal employments, multiplied by 1.1% (or 1.0% if the employee works for less than 20 years), and multiplied by the number of years of service. Thus, $70,000 as a “high three” multiplied by 1.1% equals $770 which is multiplied by 30 years for a total of $23,100.

This comes out to roughly $67,000 per year, or approximately the entire replacement salary of an employee’s most lucrative years on the federal payroll. And that is on top of any private savings or spouse benefits. The only change would be that federal employees would be paying for a greater portion of the funding of their pension.

Taxpayers would save hundreds of billions of dollars.

In 2011, taxpayers will pay roughly $19 billion to fund future federal pensions, while federal employees will contribute just over $1 billion. By 2030, taxpayers will fund close to $38 billion to fund future pensions, while federal employees will contribute about $3 billion.

That is simply unfair to taxpayers and a burden that would never occur in the private sector. If there were contribution parity, the savings would increase from $9 billion in 2011 to $18 billion in 2030 and over $30 billion in 2050.

CRITIQUES & RESPONSES

This will harm federal employees.

Federal employees will definitely pay a price, but only as far as they will have to accept the same arrangement offered to most workers. Pension contributions that were once financed almost exclusively by taxpayers will now be shared equally. That is the way it is done for Social Security, 401k-style retirement programs, and most private pension plans. Federal employees, through a quirk in the law that was meant to solve a problem that no longer exists, have gotten a very generous deal for the last 25 years. It is time for all federal employees to pay their fair share.

This will harm veterans and military retirees.

Not true. This covers only those in FERS—federal employees, congressional employees, members of Congress, and judicial branch employees. Military retirees are covered under a separate program administered by the Department of Defense.

Why didn’t you propose a similar change in CSRS financing?

CSRS is financing is already equally shared—7% by the employer and 7% by the employee—so there is no imbalance to rectify. Even if a contribution discrepancy did exist, there haven’t been any new CSRS-eligible employees added to the federal workforce on over 20 years. CSRS employees are quickly leaving the system and being replaced by FERS employees. Roughly four-fifths of current federal employees are under FERS and by the end of this decade very few CSRS employees will remain.

Isn’t another reason for reforming federal retirement that federal workers are paid more than private sector employees?

No, news reports that claim federal workers are overpaid compared to private workers are misleading.9 Making apples to apples comparison with the private sector doesn’t work because the characteristics of the workforce and the nature of the work are different. Generally, the federal workforce is more highly skilled than the average private employer’s workforce. Detailed analysis shows that federal employees’ salaries are roughly the same or less than private employees’ salaries.10 To address the controversy, however, the U.S. Office of Personnel Management has recently called for a new analysis of salary comparisons.11 Such detailed analysis should include a comparison of the financing for federal retirement benefits, which Third Way estimates is more generous than for comparable private workers.