Report Published November 5, 2013 · Updated November 5, 2013 · 34 minute read

How Medicare Part D Beat the Odds—and Why Policymakers Should Care

An expensive, partisan, and massive new entitlement, wrongly conceived, poorly designed, and awkwardly executed. While that sounds like charges being leveled at the Affordable Care Act, those were actually the indictments against Medicare Part D, enacted exactly 10 years ago. Today, Part D is among the most popular federal programs. It has come in well under budget. It has improved the financial and physical health of millions of seniors. It is celebrated as a government success.

How did Medicare Part D go from worst to first, and are there lessons for the Affordable Care Act—the newest vilified health care program? In this report, we examine Part D’s achievements and the critical lessons that Part D can teach policymakers as they implement the ACA and design health policy in this decade and beyond. We also suggest further ways to make Part D even better as it begins its second decade.

From the beginning, the Medicare Part D prescription drug program had a lot stacked against it. To pass, it had to overcome ideological rigidity from hands-off, laissez-faire conservatives and from liberals pushing for a government-run program. It was criticized in the press as either a government over-reach budget buster, or an industry hand-out that put company profits ahead of the health of seniors. Doubters even included a top Medicare official, who observed that such stand-alone prescription drug coverage “does not exist in nature.”1 Elected officials and challengers ran campaign ads promising to kill or substantially reform the new law.

There are no ads against Part D now. Previous opponents of the law have sought to expand it. And there is good reason. To the shock of many, the program came in under budget and has improved the health of many patients.2 It seamlessly blended competition among private health plans with regulations and public subsidies to provide all Medicare beneficiaries with the opportunity to obtain prescription drug coverage. The result is a new kind of marketplace for prescription drug coverage where none existed before.

Despite the high hurdles, Part D delivered the goods. Financially strapped Medicare beneficiaries no longer must choose between food and medicine. Seniors’ retirement savings are protected from catastrophic prescription drug costs. Their health has improved with increased access to prescription drugs. The gap in coverage from the original law, known as the donut hole, is set to be filled.

The success of using private health plans in Part D was not lost on the architects of the Affordable Care Act (ACA). Like the Federal Employees Health Benefits program, Part D was a prototype for the health insurance exchanges that began enrollment on October 1, 2013. Both Part D and these exchanges give consumers a choice of competing plans, freedom to enroll in any plan regardless of pre-existing conditions, and subsidies to make coverage affordable based on an individual’s income. Like the ACA, Part D even has an individual penalty: for every year a Medicare beneficiary waits to enroll because he is healthy and thinks he doesn’t need coverage, his premiums jump up to a higher level which he will pay for the rest of his life once he does enroll.

Medicare Part D was less popular than the ACA is now. Only 21% had a favorable view of Part D before it was implemented (compared to 35% for the ACA).3 As seniors had positive experiences with the program, the political debate changed. The ACA has already seen seven bipartisan changes.4 More changes will undoubtedly come as the politics shift in response to the public’s actual experience with the ACA.

Seeing how Part D beat the odds can help policymakers as they implement the ACA and look toward other health care policy changes. Indeed, among the greatest achievements of Part D is that many policymakers who opposed it at first became constructive allies to amend and tune it up in subsequent years.

In this report, we examine ten key achievements by breaking down the challenges, results, and lessons learned. We then also recommend ways to improve Part D based on those lessons.

Achievement #1: Fourteen Million More Seniors with Rx Coverage

Challenge: Expand and improve drug coverage.

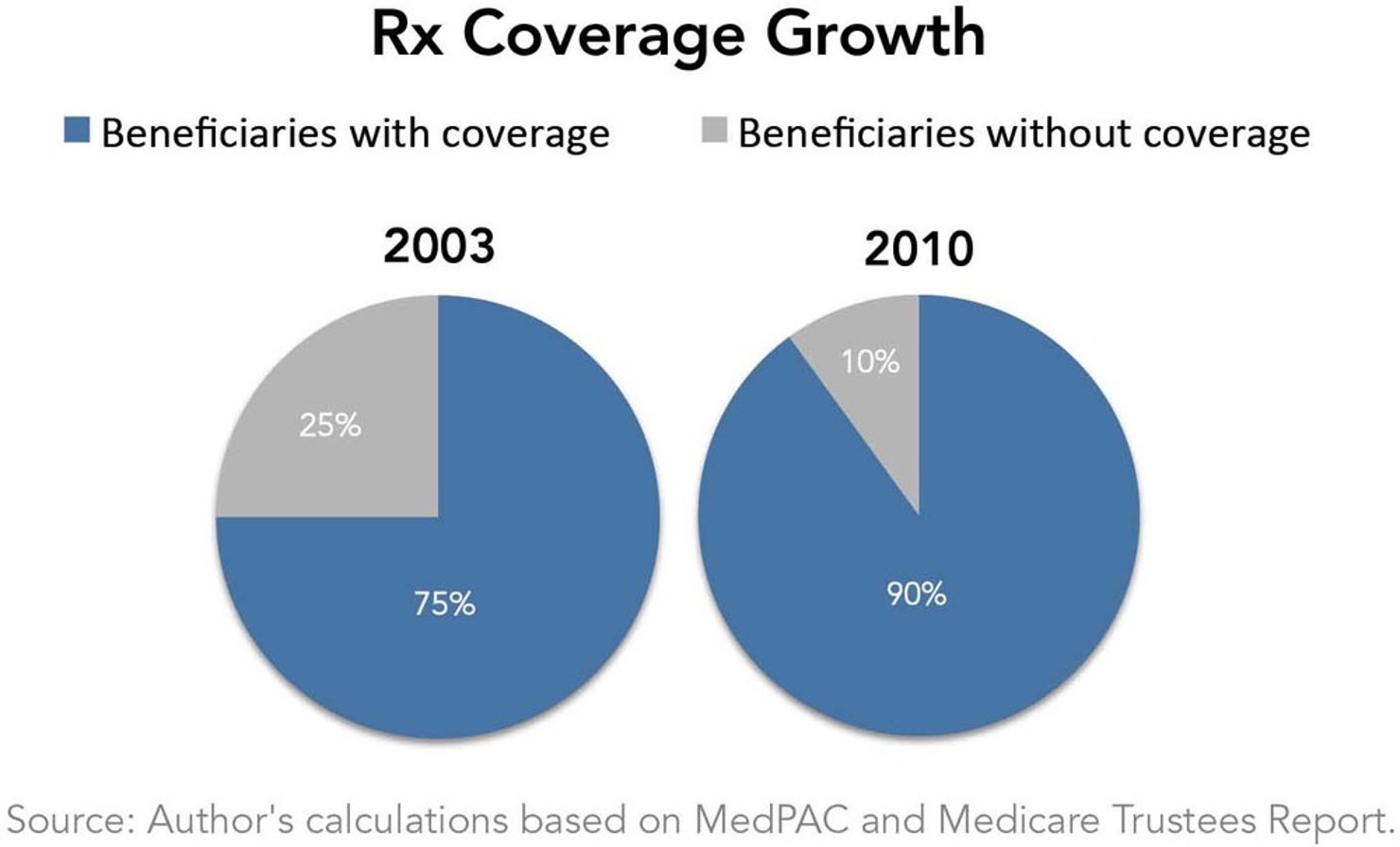

Prior to Part D’s enactment, 75% of Medicare’s beneficiaries had some sort of prescription coverage.5 The major sources included workplace health plans for retirees and older workers, private prescription drug coverage through supplemental Medigap plans that beneficiaries had purchased for themselves, Health Maintenance Organizations (HMOs), and coverage for low-income individuals through Medicaid. Consumer advocacy groups were concerned that the implementation of Part D would put beneficiaries’ coverage at risk because less comprehensive, new coverage could replace existing coverage.6

Result: Ninety percent of Medicare beneficiaries now have prescription drug coverage.7

The number of beneficiaries with drug coverage has climbed from 31.9 million to 45.6 million because of Part D.8 Medicare Part D finances coverage through three main sources: stand-alone private drug plans, Medicare Advantage private health plans, and employer or union-sponsored retiree health plans that receive a subsidy for their drug coverage.9

Not only are more people covered, the coverage is better for many beneficiaries. Coverage for drugs under Part D has no annual spending caps, which was a major problem under the prescription drug coverage offered through supplemental Medigap policies. Medigap policies, which are purchased directly by Medicare beneficiaries to provide additional financial protection against health care costs, had spending caps on beneficiaries’ annual prescription drug coverage. These caps left beneficiaries financially vulnerable if they had high drug costs.

The fears that employers would drop high-quality retiree coverage in response to Part D’s enactment didn’t materialize.10 In fact, employers made modest increases in prescription drug coverage for retirees in the second year after Part D’s enactment.11

Lesson: Expand coverage with assistance that follows the person.

Medicare Part D provides a federal payment for all types of coverage regardless of which plan the Medicare beneficiary signs up for. It also provides additional assistance for low-income beneficiaries who need extra help. This combination of widespread subsidies and additional targeted assistance has assured that most beneficiaries have coverage, and all may obtain it. A similar feature was built into the design of the ACA, which provides a tax credit for purchasing coverage through a health insurance exchange based on a sliding scale for incomes up to four times the poverty level. This tax credit follows the person, regardless of which plan they choose in an exchange, and will be critical to maintain going forward.

Achievement #2: Consumers Given More and Better Choices

Challenge: Create a marketplace for drug coverage where none existed.

Prescription drug coverage has normally been combined with comprehensive insurance benefits for employees. Employers had been offering drug coverage as a regular benefit for decades prior to Part D. But once beneficiaries retired and moved into Medicare, there was simply no precedent for a marketplace exclusively devoted to prescription drug coverage. Moreover, letting beneficiaries enroll in coverage when they needed it could mean that only sicker and more costly beneficiaries would sign up for coverage, thereby driving up the cost of coverage to the point that it would be generally unaffordable, a problem known as adverse selection.

Result: A robust market was created where beneficiaries have a wide range of choices.

Plan participation in the Part D market has been, and continues to be, robust. In 2006, every beneficiary had a choice of between 27 and 52 prescription drug plans (PDPs), depending on where they lived.12 In 2013, Part D sponsors currently offer a total of 1,045 PDPs. Beneficiaries in 32 states have between 30 and 32 PDPs; even in states with the fewest PDP offerings (Hawaii and Alaska), beneficiaries still have 23 plans to choose from.13 With such a robust market, Medicare administrators have never had to resort to the fallback plan enacted as part of the original legislation (the creation of a public drug plan for regions with fewer than two Part D plan choices).14 Health plans have also been creative with the flexibility in benefit design permitted under the law; only 4% of beneficiaries have enrolled in the benefit package designed by lawmakers as standard coverage.15

Lesson: Enable health plan competition with a stable marketplace.

Medicare Part D created an opportunity for pharmacy benefit managers (PBMs) as well as traditional health insurance plans to sign up customers directly. PBMs went from being wholesale products to retail, with access to millions of Medicare beneficiaries.

The subsidies for Part D coverage, which cover 74.5% of the premium costs for a standard benefit plan,16 have made signing up for coverage attractive to healthy and sick beneficiaries alike. The penalty for late enrollment in Part D, as well as an open enrollment period, has also discouraged some beneficiaries from waiting until they are sick to enroll.

The ACA was designed to provide the same kinds of opportunities for healthy and sick Americans alike to sign up for coverage. The exchanges must be allowed to move forward so that they allow Americans to sign up for stable coverage directly if their employer doesn’t provide it. Individuals will also pay a penalty every year that they choose not to have coverage in order to discourage the healthy from waiting until they are sick to get coverage.

Achievement #3: Nearly $200 billion Under Budget

Challenge: Create a permanent prescription drug program without runaway costs.

Some critics warned that costs were going to explode. One House Member said during the floor debate on Part D: “The enormous extra spending under this bill will be far more than projected.”17 Indeed, Medicare’s history is replete with examples of costs for new programs that exceeded projections.18 The actuary who made the original cost projection for Medicare Part A, which covers hospital costs, has said the actual experience was “165% higher than the estimate.”19

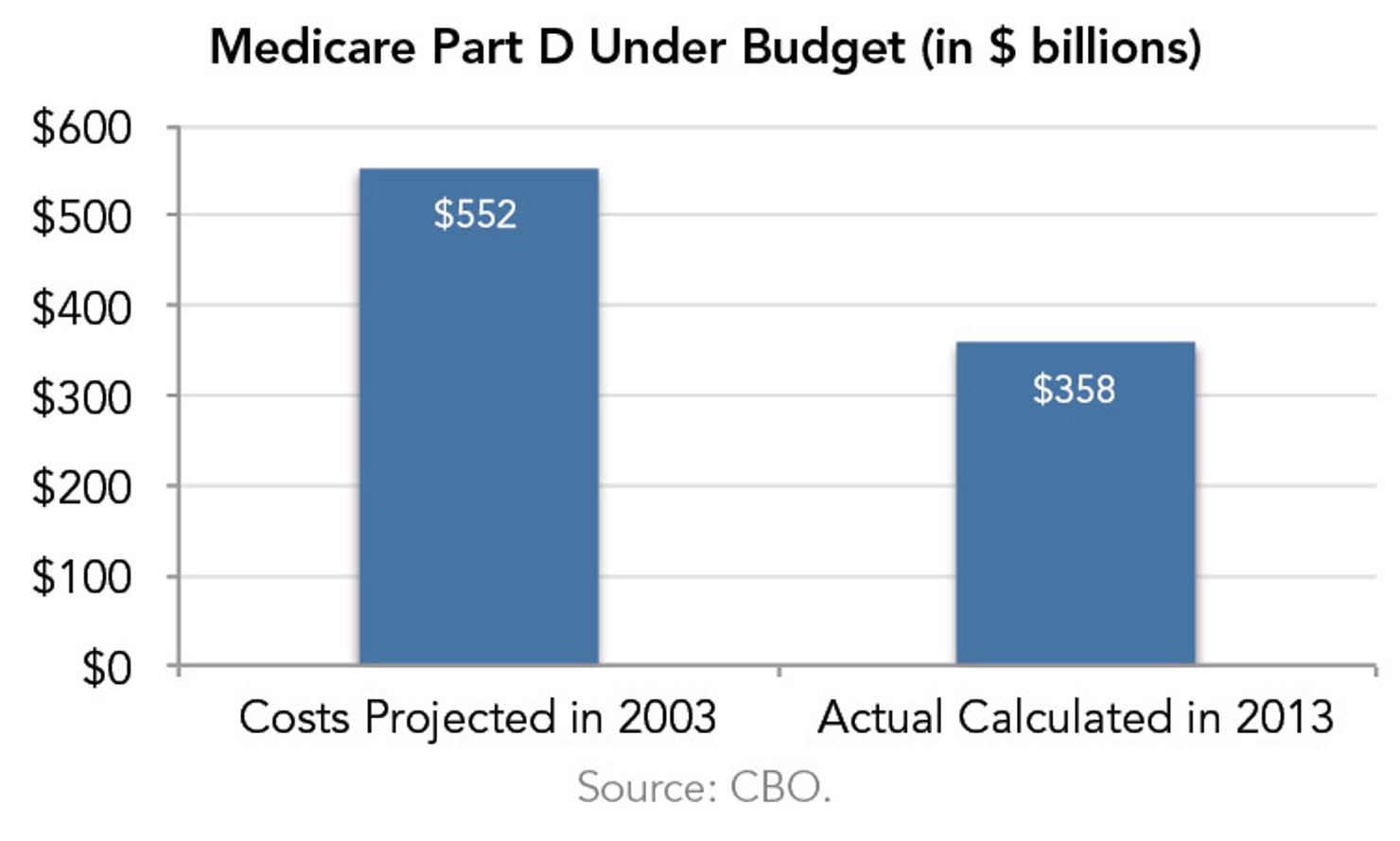

Result: Part D came in $194 billion under budget.

In 2003, the Congressional Budget Office (CBO) estimated that Part D costs over the next decade would be $552 billion.20 In March 2013, CBO estimated that Part D costs over that same time period were, in fact, just below $358 billion—nearly 35% less than initially anticipated.21 Half of these savings came from lower costs per person, in part due to the use of more generic drugs.22 The other half of the savings was from lower enrollment than projected.23

Lesson: Enable seniors and disabled Americans to make choices about their coverage.

Part D allows Medicare beneficiaries to choose the drug coverage that fits their personal budget and health care needs—just as the ACA sets out to do through the insurance exchanges. In Part D, Medicare contributes a fixed amount of money that is applied to the cost of each beneficiary’s coverage. Beneficiaries who choose more expensive plans pay the additional cost themselves. As a result, health plans have a strong incentive to negotiate with pharmaceutical manufacturers over the prescription drugs they cover. The negotiations between health plans and drug manufacturers typically occur over the rebates that manufacturers pay a health plan for giving preferential coverage of specific drugs, known as a formulary.24 The formulary and rebates determine the attractiveness of a plan in terms of specific drugs covered and the overall cost of the coverage to consumers. Specifically, plans use broad coverage of drugs and lower premium costs to attract and retain beneficiaries.

Within the health insurance exchanges under the ACA, health plans will seek new customers. This could lead to innovative new partnerships with providers that are designed to test new models of care with the goals of increasing quality, promoting value, and slowing the growth in health care spending. Preliminary evidence shows that the cost of health plans offered through the exchanges is 16% under budget.25

So, by giving beneficiaries choices about their coverage, both Part D and the ACA set up a series of mutually beneficial relationships that keep costs down. Part D’s success provides a valuable roadmap for the ACA going forward.

Achievement #4: Drug Prices Stabilized

Challenge: Restrain drug prices without resorting to price controls.

Prior to the enactment of Part D, Medicare beneficiaries without prescription drug coverage were paying high retail prices for their medicine. And beneficiaries were paying an average of half of the cost of their drugs out of their own pocket—posing significant hardships on millions of poor and middle class retirees.26

During the debate over Part D, some economists and advocates argued that purchasing drugs through an insurance plan would increase drug prices because consumers would be insulated from the price of medicine. If someone else is paying, it is only natural to worry less about the costs. Some thought that government controls on prices would be necessary to hold down costs.

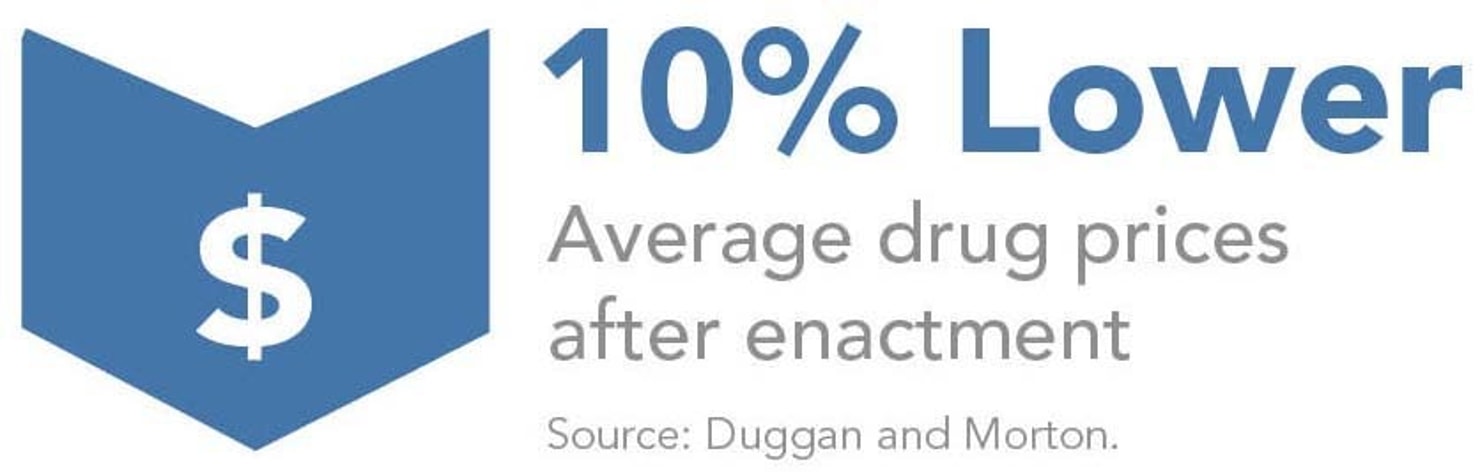

Result: Part D drove down drug prices by about 10% after enactment.27

The initial drop of 10% came within the first year of implementation as millions of beneficiaries moved into Part D plans with bulk purchasing.28 These lower prices persisted until 2009 when prices began to slowly rise again.29 But, overall, drug price increases have continued to be low. Some of the lower price growth has been due to cheaper generic substitute drugs becoming available after a large number of brand name drugs have gone off-patent. After accounting for the change due to generics, the price for all drugs purchased through Medicare Part D averaged a modest 2% increase annually from 2006 to 2010.30 Even in the most recent data for last year, the most prevalent types of Medicare Part D plans have lowered patients’ copayments for brand name drugs from between $2 to $5 per prescription, which reflects lower drug prices.31 Another indication of lower prices is the ever larger rebates that Part D plans have been negotiating from pharmaceutical manufacturers, which primarily come from brand name drugs, not generics.32 Starting at 8.6% in 2006, the average rebate has grown to 11.5% in 2011.33 In fact, the rebates have grown faster than government analysts projected. The original projection was for 6% discounts.34

Lesson: Give private health plans the incentive to negotiate lower prices and pass on the savings to consumers.

The design of Part D is not for Medicare to purchase drugs directly. Rather, Medicare contracts with participating private prescription drug plans, which then negotiate with pharmaceutical companies over drug prices. The competition among plans to attract beneficiaries with lower premiums has overcome the tendency for costs to increase when an insurance company covers health care goods and services.35 In the same way, the health insurance exchanges under the ACA will provide coverage to Americans through private health plans.

Much ink has been spilled in the debate over whether the government or the marketplace can control costs better.36 Indeed, CBO says Medicare could save money on prescription drugs by simply requiring drug companies to provide drug discounts.37 But CBO notably says that mandated discounts can reduce the amount of money available for the development of new drugs for pressing problems like Alzheimer’s and cancer.38 It is critical that this point not be lost on policymakers: existing competition and negotiation in the marketplace have been able to restrain prices and drug spending overall while balancing the need for investment in future drugs. Simply put: government control of prices would threaten that vital balance of lower prices and robust R&D. Moreover, mandated discounts for a portion of the marketplace like low-income beneficiaries would shift costs to other portions of the market, potentially causing premiums to rise for Part D beneficiaries.39

Achievement #5: Large increase in Less Costly Generic Drug Usage

Challenge: Encourage patients to use lower cost drugs, such as generics.

Prescription drug health plans negotiate rebates for brand name drugs from pharmaceutical manufacturers based on the volume of drugs that the members of each plan purchase. Critics of health plans have argued that these lucrative rebates from brand name drugs can discourage prescription drug plans from promoting the use of generics.

Result: Part D’s use of generics produced significant savings from the start and has continued as more generics have become available.

As more brand name drugs have gone off-patent, Part D plans have shifted an ever growing number of prescriptions to generic drugs, which can be seen through two measures. First, eight of every ten prescriptions are now generic, which is up 20% since 2007.40 Second, Part D plans have increased the percentage of prescriptions filled with generics where they are available, a measure known as generic efficiency. Part D plans had a generic efficiency of 96% in 2011, which is up from 90% in 2007.41

According to CBO, the increased use of generics saved $33 billion in 2007 alone.42 Encouraging generics continues to be a priority for Part D plans. They have lowered cost sharing for many generics from $5.03 on average in 2007 to $2.52 in 2013.43

Lesson: Enable health plans to encourage the use of lower-cost medicine by setting lower copayments and other means.

Part D plans have two opportunities to advance lower prescription drug costs. The first occurs as Part D plans compete to sign up customers based on their premiums, drug menu (i.e. formularies), service, and quality ratings. The second comes after enrollment when patients and doctors choose the kind of prescription needed for treatment. That second opportunity is particularly important for driving generic use.

Medicare allows Part D health plans to vary patient cost-sharing for prescriptions according to the price of the drug. Because of that, from the launch of the program in 2006, most Part D plans have deviated from the defined standard benefit set by lawmakers of 25% coinsurance for all drugs (above the deductible and below the out-of-pocket spending limit). This flexibility in benefit design lets plans encourage beneficiaries to use low-cost therapies when appropriate, as inexpensive generic drugs typically have very low cost-sharing while more expensive versions of drugs have higher copayments.44

Another reason for higher generic use is that beneficiaries’ perceptions about generics have changed. Initiatives like Consumer Report’s Best Buy Drugs have helped consumers to recognize the value of generics as viable alternatives to brand-name drugs.45 As Part D plans and PBMs have created incentives for beneficiaries to accept generics, some have also taken direct steps to change consumers’ perceptions.

Rethinking Generics

In 2006, Express Scripts pioneered an experiment in the psychology of patient decision-making to change patients’ use of lower-cost medicine. At first, it didn’t get far by simply increasing copayments in an effort to steer patients from brand-name statins like Lipitor to generic Simvastatin; only 8% of patients changed medications.46 Then, the PBM turned to the field of behavioral economics to address the non-monetary obstacles to change, such as the reticence of patients to talk with their doctors. They gave patients a simple letter to hand to their doctor requesting a switch and explained to patients “that drugs that cost more but don’t do more aren’t a better value.”47 Following a comprehensive effort, generic statin use quickly rose to over 50%.48

The success that Part D plans have had promoting the appropriate use of generics has put to rest doubts about whether they have strong enough incentives to promote generics over brand name drugs. Plans have found a strong business incentive to encourage generic use in order to keep their premiums lower and attract more customers as a result.

Now, health plans are using a similar strategy to encourage patients to use high-value networks of doctors and hospitals when choosing the care they need. Although there is no direct equivalent to generic drugs among health care providers, health plans can offer patients lower costs without sacrificing quality by setting lower copayments for high value provider networks.49 Such plans will be part of the ACA exchanges in California and elsewhere.50

Achievement #6: Fewer Costly Hospital Stays

Challenge: Prevent expensive hospital care and other avoidable complications through better use of prescription drugs.

As Congress considered expanding access to prescription drugs, some worried that prescription drugs could cause other health care problems that could add to the nation’s health care bills. For example, there was concern that inappropriate use of prescription drugs could increase the risk of adverse reactions, triggering a need for medical treatment and increasing costs to Medicare for both the drug and medical benefits.

Result: Part D actually reduced other Medicare costs.

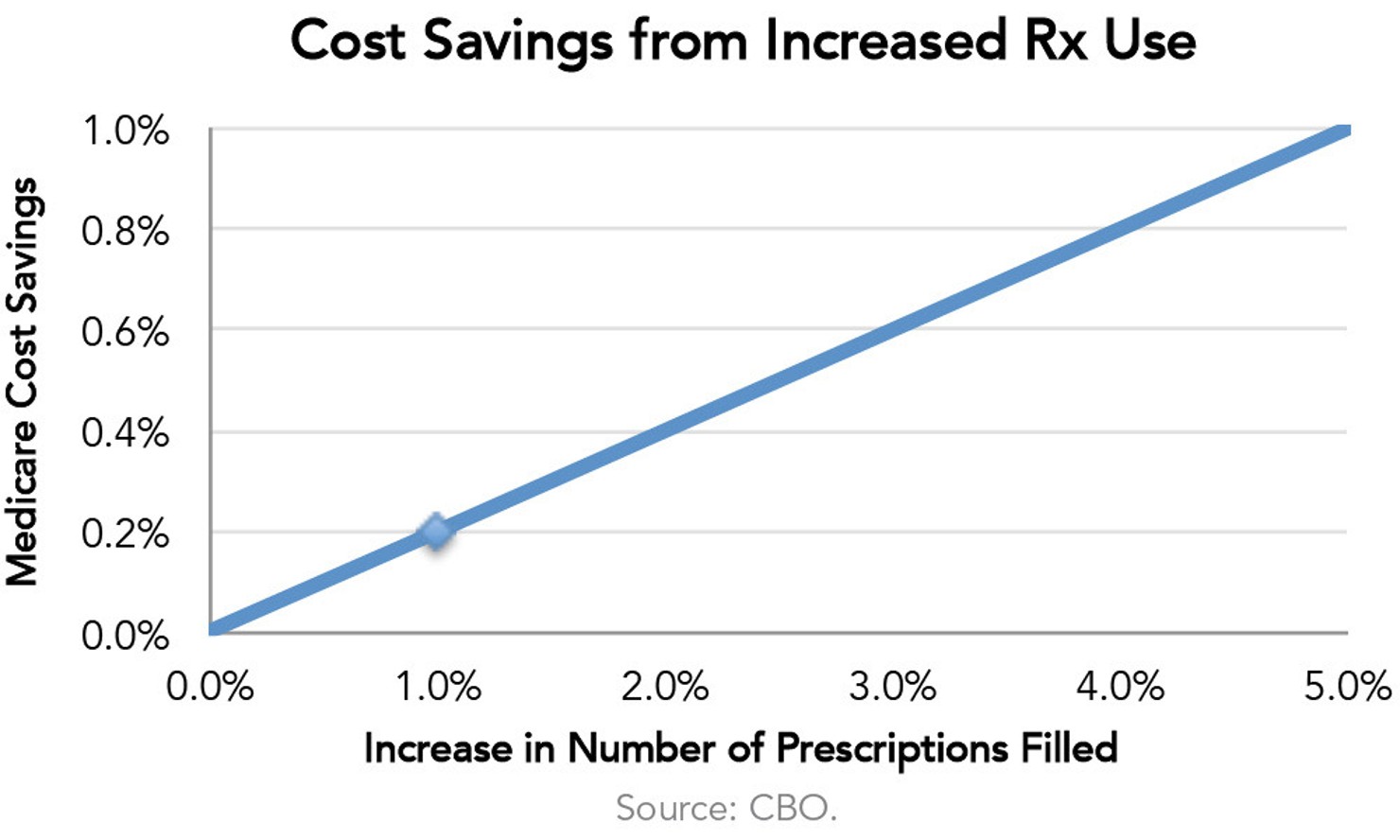

A 2011 Harvard study showed that Part D reduced Medicare beneficiaries’ total health care costs by $13 billion in 2007, which was about one-quarter of Part D’s total costs in the first year of full enrollment in the program.51 Further, Medicare patients had 20% fewer hospitalizations as a result of expanded access to drugs.52 CBO estimates that a policy producing a 1% increase in the number of prescriptions filled by beneficiaries would cause Medicare’s spending on medical services to fall by roughly 0.20%.53 For example, by working with patients one-on-one, pharmacists have aimed assistance at chronic diseases like congestive heart failure, which in turn have reduced the cost of hospitalizations for all of a patient’s problems by nearly $500 per patient over a six-month period.54 In fact, this Part D benefit, called Medication Therapy Management, has untapped potential to achieve more savings by serving more patients.55

Lesson: Health care services cannot be viewed in silos—smart policy changes in one area of health care can positively affect other areas.

Overall, Part D has improved access to prescription drugs for Medicare beneficiaries.56 Better use of prescription drugs has improved the health of many beneficiaries as well as avoided the need for a number of other health care services, both of which reduced health care costs elsewhere in Medicare.

Improving access to medicine has also helped patients manage the ill effects of chronic diseases like diabetes and hypertension. Better management of certain conditions with prescription drugs, such as asthma and high cholesterol, can also reduce the likelihood of adverse events. Thus, drug coverage through Part D has improved medication adherence rates, while simultaneously reducing the number of hospitalizations among Medicare Part D beneficiaries.57 Analyses by academic researchers found that, in aggregate, the advent of Part D reduced hospitalizations for seven conditions in 23 states by 4%.58

The ACA has set up similar efforts that seek to lower health care costs overall by increasing access to cost-saving measures. For example, paying doctors for more support and care coordination for patients with chronic diseases may yield significant savings. Oftentimes, these efforts include getting patients to make better use of medications. The ACA has also encouraged wider adoption of medical homes, which provide services and enhanced coordination in order to stop hospitalizations for preventable problems. Measures like these, which offer significant cost savings while increasing efficiency as well as improving patient care, should be expanded.59

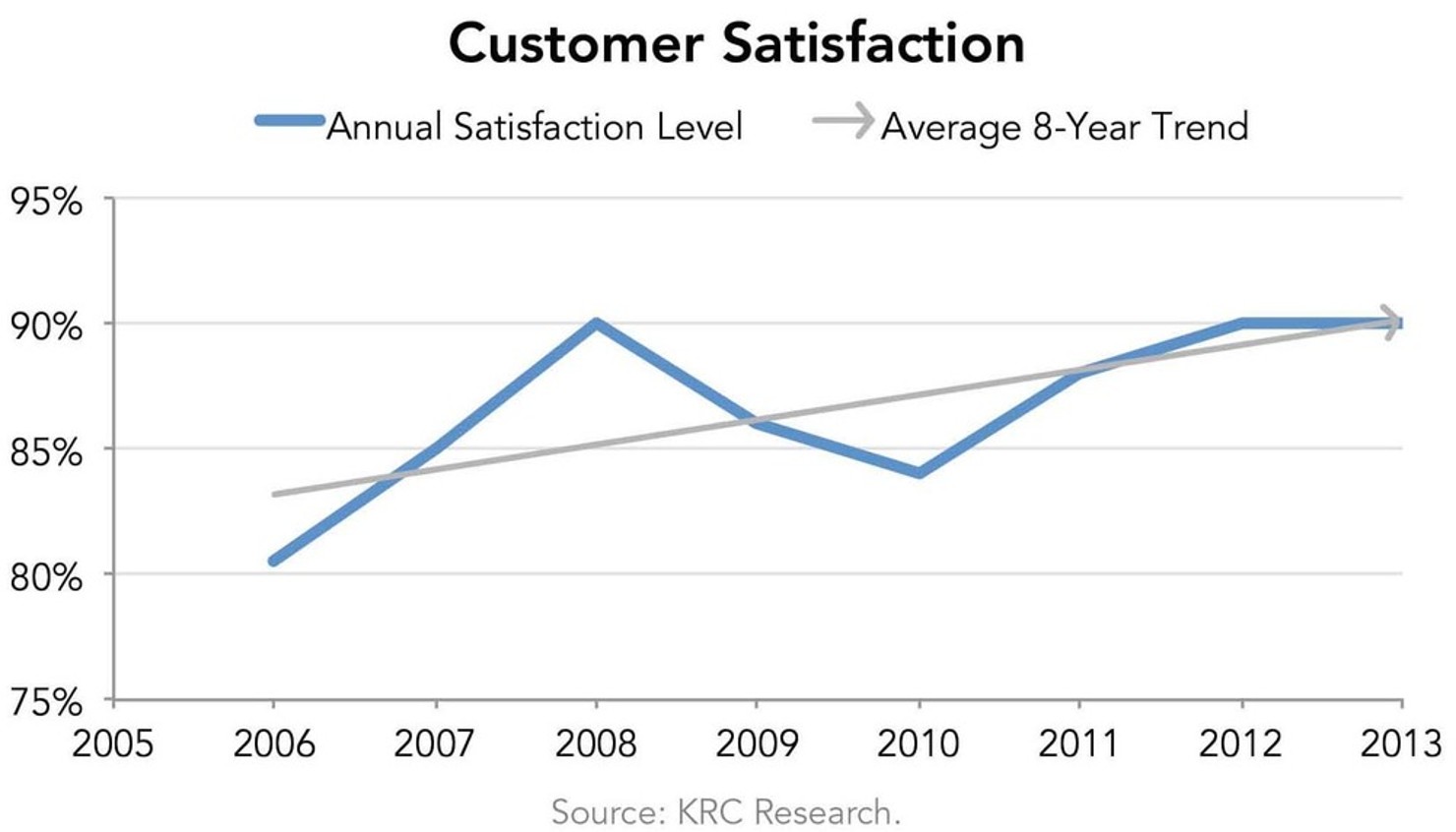

Achievement #7: Customer Satisfaction

Challenge: Keep beneficiaries happy while giving them a new way to get drug coverage that requires their active participation.

Prior to Part D, Medicare beneficiaries had very little experience shopping for their own prescription coverage. While beneficiaries could choose prescription drug coverage through supplemental Medigap coverage, the choices were limited to only three of ten types of Medigap plans.60 Moreover, federal and state laws have offered limited opportunities for beneficiaries to change coverage without facing the loss of coverage due to a pre-existing condition.

Result: 94% of beneficiaries are satisfied with Part D.61

Enrollment data demonstrates that Medicare Part D remains popular among beneficiaries, with enrollment growing from 25.8 million in 2009 to 35.2 million in 2013.62 Satisfaction surveys also show beneficiaries like the program generally and appreciate the choices. Public opinion surveys also show beneficiaries like the program and satisfaction levels have climbed since Part D’s inception.63 In a federal government survey, Part D coverage received particularly high marks: not only were 94% of all beneficiaries satisfied with the drug benefit, 95% thought the level of coverage meets their medication needs.64

Lesson: Provide consumers with a range of choices and support in making choices.

As beneficiaries became more familiar with Part D, they began to exercise their option to switch plans more frequently and save money. In the first two years, only about 6% of non-low-income beneficiaries chose to switch plans (statistics for low-income beneficiaries are different because many start in a plan that was automatically chosen for them).65 Between 2010 and 2011, 13% switched plans. Beneficiaries who switch often save money—$298 according to one study.66

Beneficiaries can get good information about their choices and ways to save money through a federal website called the Medicare Plan Finder.67 It allows individuals to enter the drugs they are taking and compare drug plan choices in their area based on their medications, quality ratings, and other measures. There is also assistance to help beneficiaries sort out their choices through federally funded Area Councils on Aging and through State Health Insurance Assistance Programs (known as SHIPs). These groups sponsor community-based programs and offer counseling that help beneficiaries choose their Part D plans each year.

A key to facilitating enrollment in the health insurance exchanges under the ACA will be websites that allows consumers to compare the price of coverage and quality ratings (to the extent they are available initially) of each health care plan. Developing web-based and other decision-support tools for consumers and on-the-ground programs (called navigators, in-person assisters, and certified application counselors) are already in the works, but more could be done. As the consumer advocacy group Families USA has argued, Congress should more fully fund the consumer assistance programs authorized under the ACA because they would “serve as a ‘one-stop’ source of assistance for consumers with any type of coverage.”68

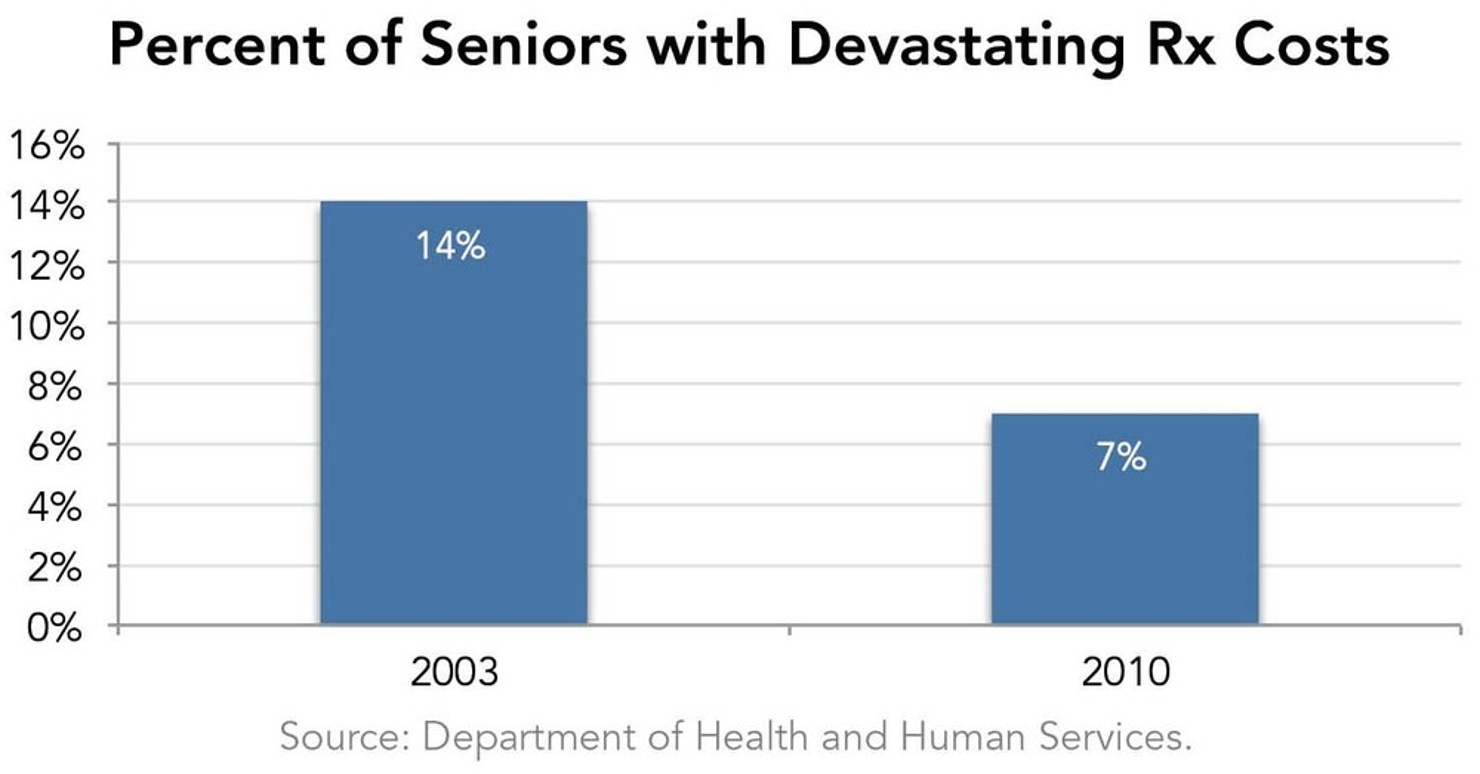

Achievement #8: Seniors Saved Money

Challenge: Protect seniors’ financial assets from catastrophic drug costs.

Prior to Part D’s enactment, Medicare had no coverage benefit for outpatient prescription drugs (certain drugs such as chemotherapy had been covered as part of hospital and physician services). As a result, some individuals had no prescription drug coverage at all, and even for those who purchased supplemental policies, medication coverage was severely limited. Most supplemental Medigap plans that included drug coverage stopped coverage after just $1,250 in drug costs per year.69 So while individuals with moderate prescription costs could buy adequate coverage, millions of beneficiaries with drug coverage still faced financially devastating drug costs.

Result: The number of Medicare beneficiaries having to pay very high drug costs dropped by half.

Medicare Part D dramatically lowered the number of beneficiaries spending more than one-fifth of their income on prescription drugs from 14% in 2003 to 7% in 2010.70 Part D coverage has made seniors’ finances more stable and less prone to bankruptcy due to drug costs. For the average senior who previously had no coverage, the result was also positive. Her out-of-pocket spending on drugs declined by nearly 50% during the first year of Part D.71

Lesson: Prioritize coverage for those most in need.

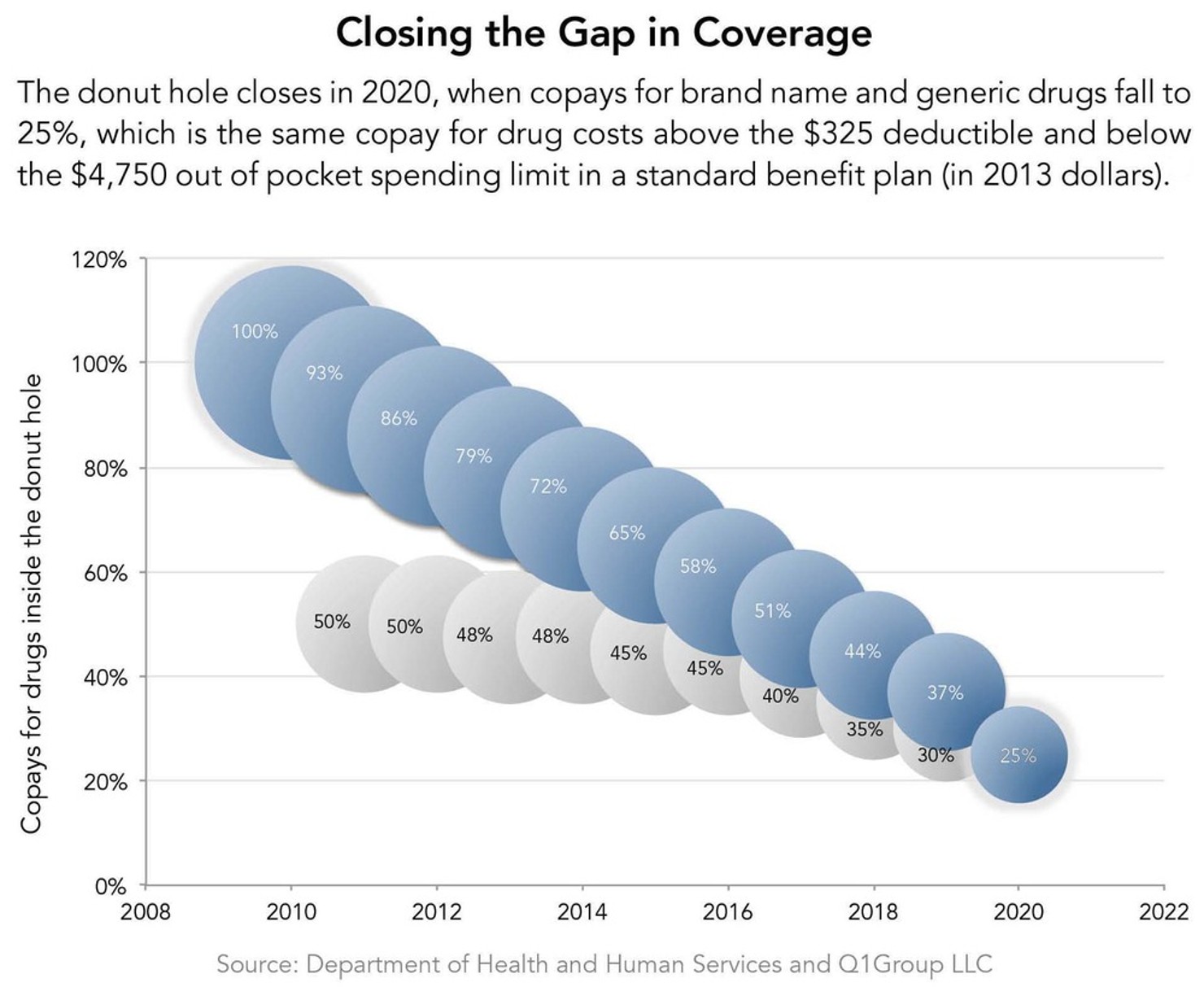

Meeting this challenge required Congress to set priorities. The first step was straightforward—Medicare Part D created a new benefit with catastrophic coverage to protect the sickest beneficiaries from high drug costs. But Congress also wanted to make Part D attractive to the majority of beneficiaries who have lower drug costs. To do that, Congress added coverage for beneficiaries with modest drug costs (above a standard deductible). Out of this combination of “front-end” coverage for modest drug costs and “back-end” coverage for high drug costs, the so-called donut hole was born. Congress simply couldn’t afford comprehensive coverage given the budget limits it had set for Part D. The gap in the original standard coverage design was for a patient’s drug expenses between $812.50 and $3,600.72 Even though many Part D plans were able to fill the donut hole through the flexibility provided under the law for designing a more attractive benefit, the debate over completely filling the donut would not be resolved until the enactment of the ACA as explained below under Achievement #10.

Achievement #9: High Levels of Participation Among Low-Income Beneficiaries

Challenge: Ensure widespread enrollment by low-income Medicare beneficiaries.

Programs for low-income Americans often fail to reach a large portion of the intended recipients. One-fourth of Americans eligible for food stamps fail to receive benefits.73 More than two-thirds of eligible Medicare beneficiaries are not enrolled in Medicare Savings Programs, which pay Medicare Part B premiums (for doctor coverage) and in some cases cover all out-of-pocket cost sharing for poor and near-poor beneficiaries.74 Enrollment in Medicaid and the Children’s Health Insurance Program, the two major health care programs for the poor, misses 35.4% of eligible adults living in or near poverty.75 Only children themselves do reasonably well among these programs, with only 14% not enrolled—a rate achieved after years of massive outreach efforts.

Result: 82% of low-income beneficiaries have Part D coverage.76

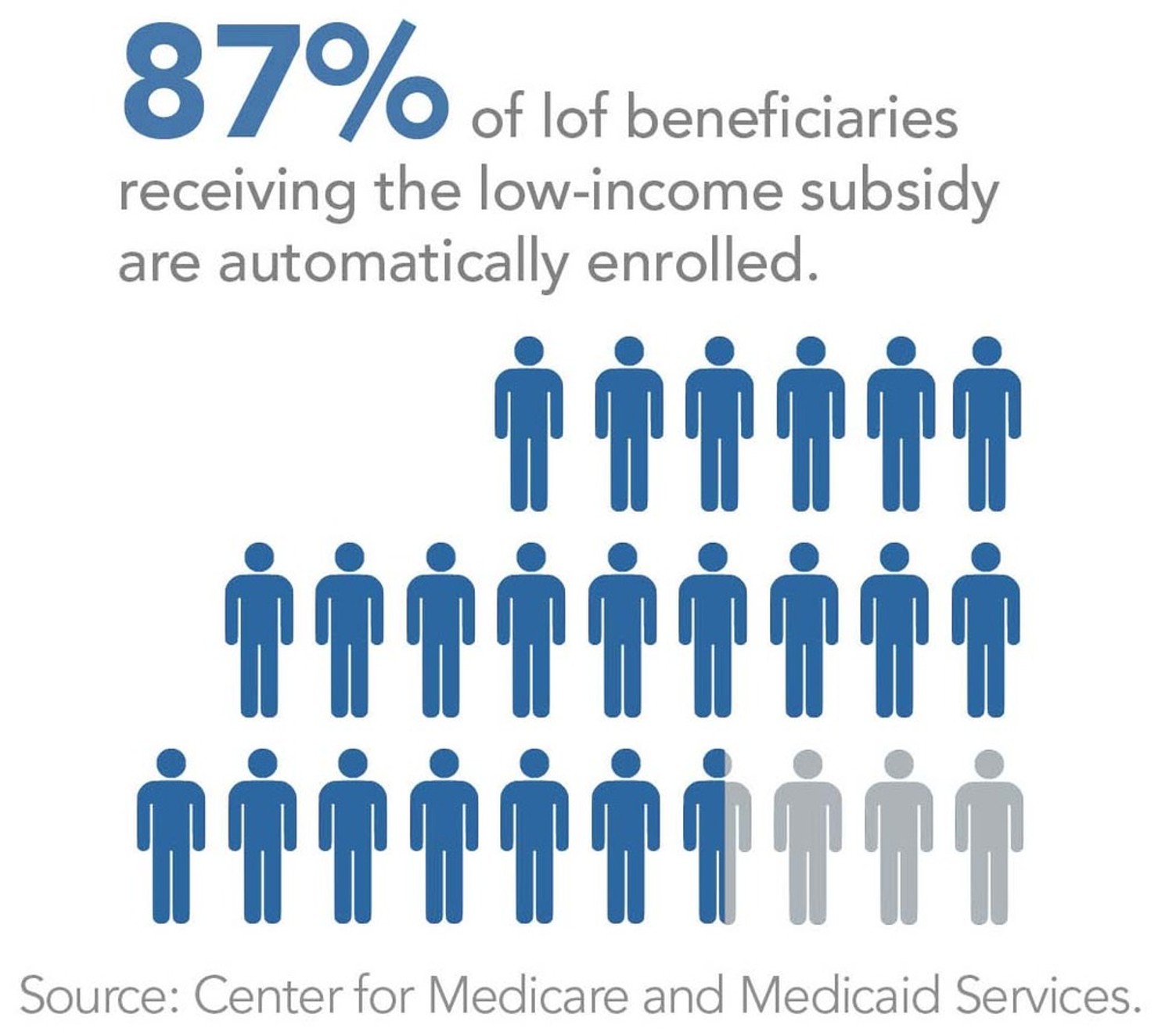

Eighty-two percent of low-income beneficiaries who are eligible for assistance have some level of prescription drug coverage. Half of those have coverage through a Part D plan with the same level of benefits as non-low-income beneficiaries.77 The other half has coverage through a Part D plan with benefits that are designed specifically for low-income beneficiaries.78 Of those beneficiaries who are receiving the low-income benefit, the vast majority are deemed to be eligible automatically because they are already enrolled in another low-income program such as Medicaid, Supplemental Security Income (SSI), or the Medicare Savings Programs.79 In 2011, 9.3 million beneficiaries, or 87%, were automatically eligible.80 The remaining 13% of low-income subsidy-eligible (1.4 million in 2011) are not deemed eligible automatically and have to apply.

Another important result that partly stemmed from covering drug costs for such a high percentage of poor elderly is that poverty rates among the elderly dropped by 7% after Part D’s implementation.81

Lesson: Use automated tools to identify eligible populations.

Automatically enrolling low-income beneficiaries saves time and money. By piggybacking on other low-income programs for the elderly, beneficiaries don’t have to fill out additional forms, and government workers don’t have to process them. Low-income beneficiaries not eligible through one of the programs noted above have to apply to the individual state Medicaid agency or the Social Security Administration for eligibility.82

This success with auto-enrollment is consistent with academic research surrounding the principle of default choice. Such practices can help people overcome what is sometimes a natural reluctance to commit to a choice, even one that is in their best interest. An apt analogy is 401(k) retirement plans: when an employer automatically enrolls its employees in a retirement plan, 86% will remain in the plan and save for retirement.83 However, when the onus is on employees to enroll, only 49% participate.84

The ACA requires larger employers with more than 200 employees to automatically enroll new hires in its health plan. This provision will help many Americans including low-income workers get coverage through their job, but more needs to be done for those who cannot. States that choose to expand Medicaid could use auto-enrollment, as the state of Wisconsin did in 2008, to enroll parents of children who were already enrolled in Medicaid or the Children’s Health Insurance Program. A national effort would auto-enroll as many as 2.5 million impoverished Americans.85

Achievement #10: Mended, Not Ended

Challenge: Part D was not perfect when it passed.

Major legislation is always a work in progress, and Part D was no exception. It was not perfect when the President signed it into law. Further, although Republicans had some initial support from some Democrats, they did not include many of the ideas Democrats had to offer. It would have been easy for Democrats to simply oppose the new law and seek to de-fund it, as Republicans are doing now with the ACA. They didn’t.

Result: Both parties have improved Medicare Part D.

Since enactment, Democrats have actually improved Part D on two occasions.86 Their first opportunity came in 2007 when they took control of Congress. They expanded coverage for low-income beneficiaries, improved health plans’ coverage of various kinds of drugs, and required prompt payment of insurance claims.87 The second round of improvements came in 2010 as part of the Affordable Care Act, which set in place annual changes that will fill the donut hole over the subsequent ten years.

Lesson: Mend it, don’t end it.

The failure of Part D could have given Democrats a political victory at the expense of seniors. But in doing so, seniors would have lost a critical new benefit, and Democrats would have a lost a key opportunity to improve the law and reap political benefits.

Ways to improve Part D

Despite its many achievements, Part D has room for improvement. By applying the lessons of its own success, Part D can improve in three areas: enrollment, low-income assistance, and beneficiary assistance with plan choices.

Enrollment

Ten percent of Medicare beneficiaries still don’t have prescription drug coverage.88 But, 44% of these beneficiaries without coverage take one or more drugs.89 A beneficiary’s decision to forgo drug coverage may not be in their financial self-interest if they are taking medications, as the cost of premiums for Part D coverage is often less than the monthly cost of a drug.90

The lesson from automatic enrollment of low-income beneficiaries can—and should—apply more broadly. Automatically opting-in all new beneficiaries into a benchmark plan (based on cost and quality) after giving them a period to make their own coverage choices would help ensure higher participation numbers overall for Part D.

This process could be designed as a fallback part of the Medicare enrollment process for all new beneficiaries. Upon enrollment, beneficiaries would receive a notice about the automatic prescription drug enrollment and their choices. Individuals would still have a chance to opt-out, but if they do not already have coverage through a job, do not select a plan, and do not affirmatively choose to opt out and go without coverage, then they would be automatically assigned to a Part D plan appropriate to their needs in their area.91

As part of considering automatic enrollment in Part D for all beneficiaries, Congress should also improve the way automatic enrollment works for low-income beneficiaries who are dually eligible for Medicare and Medicaid. Some dual eligible beneficiaries who are randomly assigned to a prescription drug plan are confused or even resentful about it. In addition, they can be automatically switched out of their plan if its premiums increase, which can disrupt their medication regimen.92 Because these same problems will occur under auto-enrollment for non-low-income beneficiaries, more attention to policy problems and consumer education for low-income beneficiaries will improve operations for the broad use of auto-enrollment.

Low-income assistance

Not only do 18% of low-income beneficiaries not have any drug coverage, half of low-income beneficiaries who are enrolled in a Part D plan are not also enrolled in the low-income subsidy program.93 As a result, they may not have a Part D plan that best fits their needs. For example, they may have to pay higher copayments for drugs than they would if they were enrolled for a low-income subsidy.94 This may be a result of beneficiaries seeking a particular plan or may be a lack of awareness that coverage with lower copayments is available. This problem has a compounding effect because when beneficiaries face high copayments for each prescription, they may not be able to afford the cost of completing a full drug treatment regimen.

Drawing from Part D’s experience with automatically enrolling dual eligible beneficiaries, the Administration should develop new ways to identify and enroll low-income consumers in the exchanges or Medicaid in states where it is available. The new data hub being developed for the Affordable Care Act implementation offers an opportunity.95 It could give the Department of Health and Human Services (HHS) access to information about Medicare beneficiaries who might qualify for assistance based on IRS income data. HHS could reach out to these potential candidates through a variety of sources including community health centers, health plans, and health care organizations. HHS could also make a matching service available to these groups so they could see if they had any contact with potential candidates. From there, the normal enrollment process would take effect and be more effective based on the pre-screening of candidates for the low-income subsidy program.

Another way to improve enrollment in Part D’s low-income subsidy program is to simplify the application process for those who are not enrolled in a program. The current asset test is designed to prevent people with significant financial assets and low-incomes from qualifying for the Medicare Savings Programs.96 But the lengthy application discourages many from even applying.97 Instead, a simple question about the lack of any asset income, which can be readily checked against tax records, would dispense with most of the asset questions.98 Once a low-income beneficiary is enrolled in a Medicare Savings Program, she will be automatically enrolled in Part D.

Beneficiary Assistance with Plan Choices

Although many beneficiaries appreciate the choices and support afforded to them by Part D, a large number still struggle with selecting the best plan and often end up paying more for coverage than necessary.99 While there are many resources available to beneficiaries to help in selecting a plan, they may not always seek out this information, and many appear to need additional assistance. For example, many beneficiaries could find a plan that would lower their total out of pocket costs or improve coverage for the drugs they take. One study shows that, nationwide, beneficiaries spent an average of $368 more per year than they would have spent had they purchased the most cost-effective plan for their medication needs. More than one-fifth of beneficiaries spent at least $500 more per year than necessary.100 While beneficiaries may be considering non-cost factors like the quality ratings or the inclusion of a particular pharmacy in a network, a problem arises when beneficiaries don’t also consider how to optimize their savings. Not only do they take money out of their own pocket, they also reduce competitive pressures to lower prices.

As Part D’s Plan Finder has already shown, when personalized information is available about diverse plan options and coverage, Medicare beneficiaries can reap benefits. The next step for Part D is to have Medicare administrators automate the process to determine how beneficiaries can save money. Just as Netflix makes recommendations about movies you might like based on the movies you watch, Medicare should make a tool available that would recommend how you can save money on drug coverage based on the drugs you use. This service would involve the development of computer software to take information about a patient’s drugs and, with their permission, analyze their choices for drug plans. This analysis would include information based on current drug usage and the risks from greater drug usage. A behavior economics research group, Ideas42, has tested a low-tech, but effective, version of this idea in which patients at the University of Wisconsin Hospital system received a personalized recommendation on a one-page letter.101 The study found that it saved beneficiaries $100 over a year.102 Medicare should build an automated version of this program as a pilot with the intent of expanding it to all beneficiaries as it becomes successful.

Conclusion

Like its Medicare Part D forerunner, the Affordable Care Act is currently a political football in Washington. But regardless of whether policymakers love or hate the ACA, they should learn from the lessons gleaned from the very similar efforts under Part D. The odds were stacked against Medicare Part D, but the program succeeded as a result of ten distinct achievements. Each of these holds lessons for policymakers as they get the ACA up and running and design new health care policies—such as reforming Medicare and Medicaid—to meet future challenges.

Subsidies based on income will be critical for expanding coverage under the ACA just as they were in Part D. Health insurance exchanges will rely on similar dynamics of competition and choice to keep costs down. And finding ways to encourage beneficiaries to seek the lowest-cost care will go a long way in determining whether the ACA is fiscally sustainable.

If you cut through the 24-hour news chatter on whether the ACA is good or bad, you might just see a way forward—via a path blazed by Medicare Part D.