Report Published April 4, 2016 · Updated April 4, 2016 · 43 minute read

GLUT: The U.S. Economy and the American Worker in the Age of Oversupply

WHAT'S NEXT?

The aftermath of the Great Recession has posed serious challenges for policy makers especially in the area of job creation, income growth, and income polarization. While the number of jobs has rebounded, the quality of jobs has not–leading to a great deal of anxiety about the future of the middle class in the face of prolonged income stagnation.

When it comes to ways out of the current dilemma, conventional economics have been tested and found wanting. Into this quandary comes valuable work by Daniel Alpert, who argues that the reason conventional economics offers such poor alternatives to policy makers is that insufficient attention has been paid to what he refers to as “oversupply” in the labor market. “The suddenness and extent of the integration of over 3 billion people into a global capitalist market, that really only hitherto consisted of about 800 million in the advanced economies, produced not only the imbalances and glut conditions that have been written about extensively since the Great Recession, but have echoed in the many crises since then.”

Oversupply, he argues, is a global phenomenon that triggers a host of other economic ills, from “… declining productivity and falling labor force participation, inflation in real estate and stock markets, the value of the U.S. dollar, and even stock buybacks, swollen executive compensation, and increasing income and wealth polarization since the recession, to say nothing of the global financial crisis itself. “

This time, Alpert argues, is really different. The phenomenon of the global oversupply of labor is not easily remedied by the private sector alone. Instead of creating the kinds of jobs that used to fuel the middle class, the private sector today is making short-term commitments and hiring more people as needed. Government, argues Alpert, needs to “step into the breach now unfilled by the private sector.”

Alpert’s paper, “GLUT: The U.S. Economy and the American Worker in the Age of Oversupply” is the latest in a series of ahead-of-the-curve, groundbreaking pieces published through Third Way’s NEXT initiative. NEXT is made up of in-depth, commissioned academic research papers that look at trends that will shape policy over the coming decades. In particular, we are aiming to unpack some of the prevailing assumptions that routinely define, and often constrain, Democratic and progressive economic and social policy debates.

In this series we seek to answer the central domestic policy challenge of the 21st century: how to ensure American middle class prosperity and individual success in an era of ever-intensifying globalization and technological upheaval. It’s the defining question of our time, and one that as a country we’re far from answering.

Each paper dives into one aspect of middle class prosperity—such as education, retirement, achievement, or the safety net. Our aim is to challenge, and ultimately change, some of the prevailing assumptions that routinely define, and often constrain, Democratic and progressive economic and social policy debates. And by doing that, we’ll be able to help push the conversation toward a new, more modern understanding of America’s middle class challenges—and spur fresh ideas for a new era.

Jonathan Cowan

President, Third Way

Dr. Elaine C. Kamarck

Resident Scholar, Third Way

* * *

“It is common sense to take a method and try it: If it fails, admit it frankly and try another. But above all, try something. The millions who are in want will not stand by silently forever while the things to satisfy their needs are within easy reach. We need enthusiasm, imagination and the ability to face facts, even unpleasant ones, bravely. We need to correct, by drastic means if necessary, the faults in our economic system from which we now suffer.”

Franklin Delano Roosevelt

May 22, 1932

Since the Great Recession there has been a tendency in economic policy circles to evaluate post-recession data and trends in light of prior understandings. Both economists and policy makers have been desperately attempting to “put the genie back in the bottle” and proceed with business as usual notwithstanding how inapplicable some of the received economic policy wisdom is to present-day realities. The foregoing tendency is reflected and magnified in one of the most politically dysfunctional periods in the history of American governance—a clash of market-oriented orthodoxy with the necessary role of the collective agent of government, and an amplification of the federalist-versus-decentralist arguments that have plagued our nation since its founding.

Just as troubling is the level of dissonance within the halls of macroeconomic academia. No longer merely a rift between the freshwater (University of Chicago and others) and the saltwater (MIT, Harvard, and others) views of the world, but a brackish sewer of dissent that not only yields little in the way of consensus, but confounds the political class and blocks effective policymaking rather than serving up pragmatic solutions. Balkanized legislatures, exacerbated by a generation of gerrymandering, are divided—whether by philosophy or self-fulfilling opinion polling—to the point of paralysis. And many of these divisions have been exported throughout much of the developed world over recent decades.

The United States is, without question, a stronger and more affluent nation that that which FDR rose to lead during the depths of the Great Depression. Yes, we have tens of Roosevelt’s “millions who are in want,” but thankfully nowhere near the level of destitution that the country saw in 1932. Today, however, we have tens, arguably tens of tens, of millions of who are in shock, stunned by the glaring uncertainties in their futures: middle-aged and middle class, even upper middle class, workers with few provisions for retirement and little hope of ever being able to save for same; job market entrants without career-building employment opportunities, facing life in a euphemistically-christened “gig economy” with its attendant instability and impermanence; college students or recent graduates facing a mountain of debt that stands between them and the ability to form a family, buy a home, and enjoy the relative comforts that an advanced education is supposed to afford.

As 2016 dawned and both the U.S. and global economies showed signs of slowing anew, we found ourselves confronted by the ineffectiveness of the more incremental solutions so far attempted to ameliorate the above-listed shocks. The problem rests, I believe, with our insufficient appreciation for how the modern U.S. economy interacts with that of the rest of the world.

It is easy to be distracted from these broader undercurrents. After all, our people live in the world of the internet, possessing smart phones and many of the smaller accoutrements of affluence our forbearers, had they been able to imagine them, would have thought to be the products of a strong and powerful people—even as economic stability, and often the pursuit of happiness itself, have been wrested from them. Such is an outcome which no earlier generation could have conceived of, brought about by the failure of many in the present generation of leaders to appreciate the titanic changes to the domestic and global economies, which require the U.S. to correct, “by drastic means, if necessary, the faults in our economic system from which we now suffer.”

The Age of Oversupply

Since 2005, when former Federal Reserve Chairman Ben Bernanke first made reference to a Global Savings Glut,1 his hypothesis has undergone both supportive and critical analysis, for the most part concurring that, yes, something odd was going on. A substantial amount of global capital was remaining unutilized or underutilized and not recycled into investment or used for consumption. By 2008, I had concluded that—if anything—Bernanke had understated the import and dimensions of his observations, and that the global economy was experiencing something that centuries of academic discourse would have thought impossible. There was, and remains, a global oversupply of labor, productive capacity, production, and capital, all (except, at times, labor) being things that were classically thought to be ever-scarce relative to the demand therefor.2 Something, indeed, had happened, and it was, I concluded, substantially related to the rather sudden emergence of the post-socialist, or semi-socialist nations (China, Russia, Brazil, India and others), into full-blown economic competition with the developed nations. As I wrote in the introduction to my 2013 book:

“In the time it takes to raise a child and pack her off to college, the world order that existed in the early 1990s has disappeared. Some three billion people who once lived in sleepy or sclerotic statist economies are now part of the global economy. Many compete directly with workers in the United States, Europe, and Japan in a world bound together by lightning-fast communications. Countries that were once poor now find themselves with huge surpluses of wealth. And the rich countries of the world, while still rich, struggle with monumental levels of debt—both private and public—and unsettling questions about whether they can compete globally.”3

The suddenness and extent of the integration of over 3 billion people into a global capitalist market, that really only hitherto consisted of about 800 million in the advanced economies, produced not only the imbalances and glut conditions that have been written about extensively since the Great Recession, but have echoed in the many crises since then. We continue to experience a low interest rate and disinflationary environment and a slew of other economic phenomena that might not typically be thought of as being associated with—but are actually triggered by— the oversupply itself. These include, among other things, declining productivity and falling labor force participation; inflation in real estate and stock markets, the value of the U.S. dollar, and even stock buybacks; swollen executive compensation; and increasing income and wealth polarization since the recession, to say nothing of the global financial crisis itself. More about all that later.

It is important to note two things related to the foregoing. First, that the classically virtuous cycle (or circle) of expanded growth, spending, savings and investment has been essentially blocked up in the U.S. by the age of oversupply. Capital is being hoarded and not reinvested in additional employment-producing assets (plants, equipment, etc.) by much of the U.S. private sector, simply because there is already an excess of global capacity relative to global demand for production. Second, that this is not a short-term phenomenon. The failure of the developed economies to recover robustly ever since the Great Recession is, in this writer’s opinion, proof positive that oversupply is not something that will be absorbed by conventional business cycle dynamics. And absent the recognition of this fact in the form of targeted policy to counter its effects, the developed economies will remain in a low-growth demi-slump for a lengthy period of time.

Let’s also take a moment to define global demand, because that is a subject that all too often proves confusing. The layperson might say, “Well, surely, there are many of our own poor and many more people in less developed countries who certainly desire a far higher standard of living—don’t they comprise a source of virtually unlimited demand for the products and services produced by the rest of us?” Economic demand is, however, measured in dollars and other currencies, not desire or desperation. To obtain a higher living standard, those less fortunate must obtain the money to do so, and, short of robbing banks, that happens principally via gainful employment.

And therein lies the insidious rub of the prevailing oversupply of labor and production. It is simply not profitable, until the excess of production relative to economic demand, for the U.S. private sector to invest in additional plants and equipment so as to employ substantially more people (As of the end of the third quarter of 2015, relative to population growth, the U.S. still remained 2.6 million jobs short of pre-recession levels on a population adjusted basis.) It is arguably equally senseless to raise the wages of those already employed as long as there remains a line of others (both domestically and, in the tradables sectors, abroad) willing to take their place. Hence the falling labor share of GDP and the net stagnant or declining real wages that have prevailed since the late 1990s.

All of this would sound rather dire and intractable were it not for the existence of that mountain of stranded global savings referred to earlier. The blocked virtuous circle of consumption/spending→profits→savings→investment→employment and ultimately back to more consumption, can be repaired, but it is foolish to expect the private sector to do so on its own. And the principal disconnect in center-right policy today is that it asks and expects the private sector to do things that are not profitable—not even at low prevailing interest rates, not even at low levels of taxation, and not even with banks stuffed full of money to lend—namely, to expand and overinvest in the face of oversupply. The private sector is not in business to lose money.

During 2014 and 2015, even as the U.S. benefitted enormously from an explosion in the volume of domestic energy supply that will soon result in the nation’s energy independence (and the subsequent collapse in global energy prices beginning in the latter part of 2015) the U.S. currect account balance resumed its march further into negative territory. As Figure 14 demonstrates, a steadily growing deficit in non-energy components of the current account is returning to peak levels last seen during the bubble era that preceded the Great Depression.

The lesson to be drawn from the above is that the United States’ global competitors (emerging and advanced economies alike) are fighting hard for whatever share they can obtain of insufficient global demand and, for the most part collectively, prevailing. And we must assume that this state of affairs will continue into the foreseeable future.

Fortunately, we have another agent that can use the stranded savings and offset the most detrimental impacts of global competition, and, in doing so, unblock the virtuous flow of capital—and that is, of course, the public sector. And we are not without the ability to, in a geopolitically realistic manner, address the global economic imbalances that have hobbled the U.S. and much of the rest of the developed world since the accelerated emergence of the post-socialist countries.

This Time Really IS Different

Yes, the solutions to our present dilemma are “Keynesian” more than they are otherwise, but one should keep in mind that John Maynard Keynes did not live to see the dismantling of his indelicately negotiated, post-World War II Bretton Woods system and the emergence of the freely floating major fiat currencies of monetarily sovereign countries such as the U.S., the U.K. and Japan, that we have today. (You can add Germany to that list, I suppose, if you view the euro as simply a deutschemark renamed and devalued, as I do.) The rules have changed since his time, and so has the world economy.

Further, during Keynes’ lifetime, the global economy was—for the most part—Western Europe, North America and, later, Japan, with the rest of the world either undeveloped, underdeveloped, or penned-in behind the growing iron curtain of socialism. Within that limited economy—and especially following the periodic ravages of war in Europe and elsewhere, together with the fact that the New World saw a nearly endless demand for labor relative to the pace of its expansion and paucity of its population relative to its resources—scarcity, not oversupply, was the main concern of economic thinking. It is not unfair to note that classical economics begins with an assumption that resources and production are universally scarce relative to demand and proceeds from there to explain how and through what mechanisms limited supply is allocated.

At the heart of what ails us is the fact that certain economists, and all too many policy makers, remain guided by a status-quo-ante that has little relevance to present day circumstances.

The enormous trade and current account imbalances that erupted in the first decade of the current century between emerging and developed countries, and the parallel enormity of the surplus racked up by Germany within the Eurozone (before the Eurocrisis) and with the rest of the world (since the Eurocrisis) are the most classic possible illustration of what Keynes said would happen if there were no international coordination of trade flows: extremes of mercantilistic behavior, huge piles of stranded foreign currency reserves, and currency manipulation/competitive devaluation. And I imagine Keynes would be fairly exercised about the euro regime itself, which served to exacerbate the problem within and among the member countries—something that could have been prevented by insisting on full fiscal and transfer union before currency union was ever attempted.5

Also rather startling to Keynes would be the nature of our globalized economy, in particular the hyper-competitiveness of extra-territorial labor, the magnitude of the worker base of low-wage manufacturing nations relative to higher-wage consuming countries, and the huge excess of global capital evidenced by near-zero interest rates in the developed world. Were he with us today, his first guess might be that there must have been a veritable catastrophe (war, epidemic or a flood of biblical proportions) that resulted in such a demand shortfall relative to supply. Eventually, he would understand that Marxism didn’t pan out well in the end, and those burdened by its variants for much of the 20th century were playing an accelerated game of catch-up, in which their own social stability and advancement of living standards were far more important to them than the potential ills arising from beggaring their trading partners in order to improve on the former.

Yet one can look to the economy of China today and note that an absence of attention to the health of one’s trading partners tends to end badly for all, disinflationary not only to the prices of goods and many services, but to the value of labor itself.

One can argue that the developed world is experiencing chronic secular stagnation, widening income and wealth inequality, or a score of other ill effects—and yet the policy choices made to combat those symptoms will remain of muted impact and unfocused on the disease of oversupply itself if we don’t fully understand what we are dealing with.

So let’s move on to the specific problems persisting in the U.S. economy, how present policy is missing the mark, and what should we be doing to “face [these] facts, even unpleasant ones, bravely?”

The Mysterious Labor Situation in the United States

Amidst a huge overhang of global labor in emerging economies, along with substantial unemployment and underemployment in Europe and elsewhere, it would appear at first blush that the United States has done rather well in the area of job creation since the Great Recession. On a nominal level, the U.S. has—albeit seven years later—restored the number of jobs lost as a result of the Great Recession, and the headline U-3 unemployment rate, at this writing, has been driven back down to 4.9% from its 10.1% peak in October 2009. The index of aggregate weekly payrolls for U.S. private employees (which is wages x hours worked x people employed) grew by 28.8% during that period, or about 4.8% per year, albeit skewed to the past three years.

But something does not feel right about this, and it is clear from both the dissatisfaction of the American people during the present presidential election cycle, as well as the underlying data, that this headline story is not even close to descriptive of what has really transpired. As Figure 2 illustrates, the headline unemployment rate since the Great Recession has fallen predominantly because of a decline in the size of the labor force relative to the employable population, a post-2000 phenomenon that accelerated enormously as a result of the Great Recession. So much so, that if you held the so-called labor force participation rate (LFPR) constant from the end of the Great Recession, the U-3 unemployment rate would be just under 10% today. Compared to the peak level of LFPR in the year 2000, unemployment would be nearly 12% today.

Now, those comparisons are not entirely fair, but they are more fair than not. It is often noted that the decline in LFPR is a factor of demographic change. And the truth is that our large baby boom generation is beginning to retire, which would tend to naturally erode overall labor force participation. But before any policy maker or candidate for high office accepts the notion of the decline in LFPR being something that is mostly related to domestic demographics, we must consider five countervailing facts with regard to the health of the U.S. labor market:

- The LFPR fell at a far more accelerated rate following the Great Recession that it had from 2000 to 2008 (see Figure 3).6

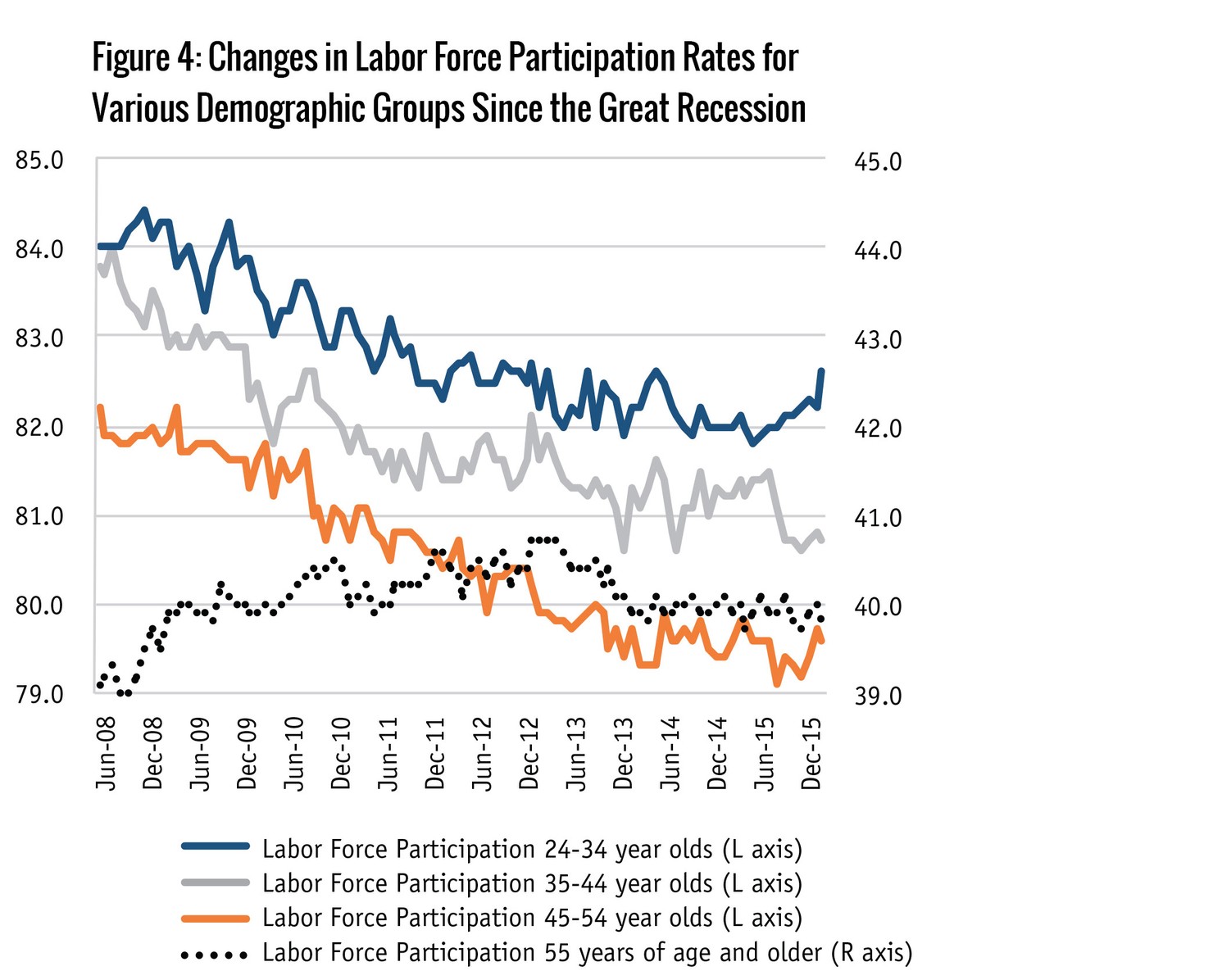

- For those in their prime earning years, the LFPR has actually fallen at a more rapid pace than that of supposedly retiring workers over 55 which has remained relatively flat (see Figure 4).7 The problem is that, while our population over 55 is larger than in prior years, and many in that cohort certainly retire, the employment-population ratio of our older workers is near all-time highs, and we have 7.2 million more workers in that group employed—to the clear detriment of younger cohorts as new employment is not keeping up with population growth. The baby boom generation isn’t going gently into the night of peaceful retirement; it is holding on to employment by its metaphorical fingernails.

- The number of workers employed full time has eroded substantially, such that today there are only 122 million Americans working full time to support a nation over 315 million people. As a percentage of those employable, full-time workers are now only 48.6%, versus 52.3% on the eve of the Great Recession.

- Of the over 12.3 million jobs created since unemployment reached its high point after the Great Recession, 47.6% have been in extreme low-wage/low-hours sectors of retail services, administration and waste management, social assistance and leisure and hospitality. In mid-2015, hourly wages on average for these four sectors stood at a little more than $16/hour and, of even greater importance, hours worked averaged just over 30 per week. As a result, annual incomes for these 43.2 million jobs averaged around $25,600/year. By comparison, only 13.2% of jobs created during the same period have been in the well-paying, goods-producing sectors (mining, manufacturing and construction), where hours averaged over 40/week, current wages averaged $26.29/hour, and annual incomes averaged $55,230/year.8

This clearly points to a condition in which the value of labor of has fallen considerably due to elevated labor slack. Part of that slack is illustrated by the number of workers forced to accept part-time employment when they wish to work part time, a level that today is 200% higher than it was at the beginning of the century and 150% higher than it was at the beginning of the Great Recession. But the fact that nearly half of post-recession job growth has been in sectors offering only a bit more than 30 hours of work a week, relative to the rest of the workforce working 39 hours a week on average, is perhaps even more telling.

Technology, the Productivity Dilemma, and the Competitive Global Labor Force

There has been considerable debate of late about the dimensions of U.S. labor slack, the point at which it will be absorbed and, above all, its causes. In nominal terms,9 the rate of job formation and the U-3 unemployment rate look as though they are returning to normal levels, but it is clear from the forgoing analysis that those headline numbers are not an accurate reflection of the true condition of labor in America. As previously noted, the true story is reflected in the unrest and anger voters are expressing towards the establishment political system.

Moreover, there are three other principal questions that need to be addressed with regard to the U.S. labor and employment situation:

- To what extent have rapid improvements in technology impaired the demand for labor, and is what we are presently experiencing merely a process of adjustment to a new paradigm?

- Why has U.S. labor productivity been flat to falling over the past two years, and how can that possibly be, given the levels of technological advancement experienced over the past quarter century?

- If the answer to the U.S. labor dilemma is not to be found in endogenous conditions such as technological substitution and an aging labor force, how do we dimension the connection between falling U.S. real wages and labor’s share of production and the matter of global labor oversupply?

Each of these questions deserves a more thorough response than the brief overview below, but I will try to hit on the most important points. As a general matter, technological advances should serve to increase productivity and, therefore, economic growth, all other things being equal. But in an age of oversupply—featuring an exogenous, low-cost labor force and insufficient global demand relative to supply—all other things are anything but equal. U.S. capital spending,10 adjusted for inflation, has been relatively flat for the past 15 years, rising only 13% from 2000 through 2104 despite a 29% growth in real U.S. GDP.11 The slowdown in expansionary investment, however, is just the headline. The components of that capital spending have changed as well, with spending on information processing equipment and intellectual property products growing by 63% during that same period, while all other capital spending actually fell by 0.1%. Figure 5 illustrates the relative capital spending levels in various categories, both private and public.

The problem appears to be that the categories in which capital spending has been increasing are those that do not give rise to employment of large numbers of employees, such as software, or for which manufacturing is substantially undertaken offshore, such as information processing equipment. (There is some good news in that such capital spending does give rise to domestic distribution and sales and servicing jobs, which are well-paying and relatively numerous—albeit constituting only about 2% of those employed in the U.S.). Quite a bit of the technology that is being invested in is, unfortunately, often not of the type that increases aggregate output but, rather, is employed to reduce labor costs in a slow-growth era in which profitability is more often increased through expense reduction rather than hard-to-generate top-line expansion.

Despite all the nifty labor-saving technology that businesses have been buying more of since the Great Recession, labor productivity has pretty much flat-lined over the past couple of years. From and after the 1982 recession, labor productivity rose rather steadily until the Great Recession. As Figure 612 demonstrates, productivity accelerated markedly, however, during the IT revolution of 1996-2002—one of the reasons that period is (save for 9/11/2001) looked back upon fondly by economists, politicians, and civilians alike. During the Great Recession, as would be expected, productivity “spiked,” reflecting not increased efficiency of labor, but rather the loss of 8.8 million jobs (6.3% of total employees), while GDP only declined by just 1.6%. This “bad productivity growth” is not of the type that is at all welcome.

But the real productivity dilemma resides in the post-recession recovery period. While U.S. economic growth during the recovery has been anemic in comparison to past recoveries—and per capita growth even worse—it has been positive. So why, amidst rising employment and economic expansion—to say nothing of the resumption of capital spending on labor-saving technology discussed above—is “good” productivity not rising? Some have gone so far as to suggest that workers have become “lazy” or that labor costs are the cause, at a time when wages are basically flat on a real basis. Neither argument holds water.

In the literature of macroeconomics, however, there is a valuable theory—part of a dust-up known among wonks as the Cambridge Capital Controversy—between certain economists at Cambridge University in the U.K. and those at the Massachusetts Institute of Technology in Cambridge, MA, among the latter Paul Samuelson and Robert Solow, both Nobel laureates. The controversy is very technical, and, I would argue, still somewhat unresolved. But in boiling this down for layman’s purposes, Samuelson and Solow posited that at different costs of capital, (interest rates, for the sake of discussion) businesses switch between the use of labor and investment in capital goods to serve shorter-term profitability goals; and that they likely “reswitch” between the two forms of expenditures over time as interest rates change. Now, Samuelson and Solow were theorizing during a period of high interest rates, which would logically reduce the desire to make capital investments as the cost of financing was high. But what of the present environment, that of near-zero and negative interest rates and an oversupply of relatively cheap labor that can be fairly easily employed part time, on an as-needed basis?

I consider it likely that businesses are not making long-term capital investments because the current condition of global production oversupply simply does not instill confidence that they will be able to improve profitability from such investments no matter how low the cost of capital may be. In other words, while order books may be full in any given month, businesses lack confidence that they will remain full—and fluctuations in economic activity since the Great Recession (in, what I have called in the past, “mini-cycles”) would seem to prove that lack of confidence accurately held. So businesses have instead been making what are actually short-term commitments to hiring more people as needed, rather than long-term commitments to additional plants and equipment. A surge in employment in the presence of very slowly growing output would, in fact, have the effect of reducing labor productivity. And I believe that is what we have been seeing in data from several recent quarters.

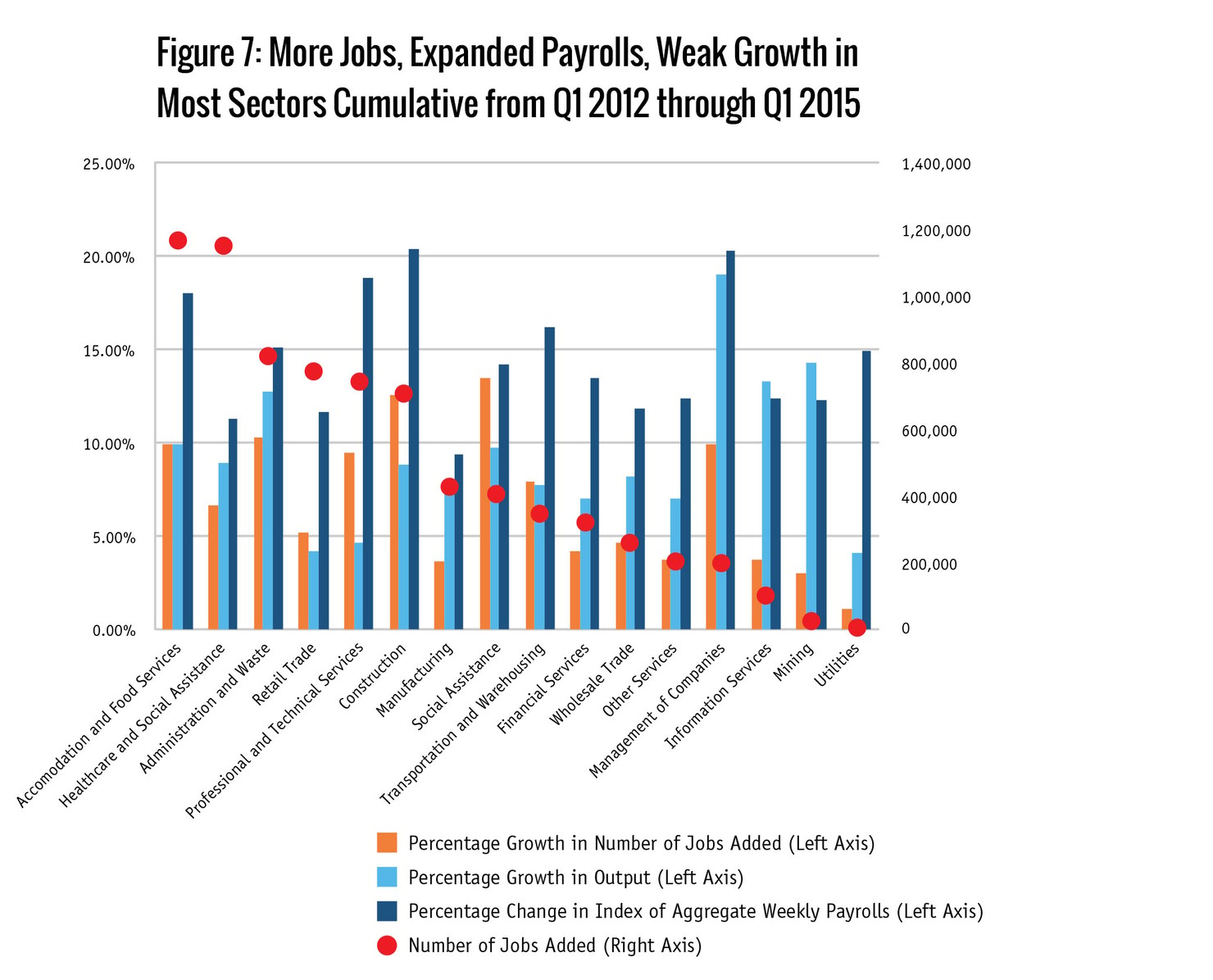

To put a finer point of this analysis, the below Figure 713 illustrates the relationship among job growth, aggregate payroll growth, and growth in output for certain sectors for the three years from the first quarter of 2012 through the first quarter of 2015. It is clear that most of the sectors in which we have seen salutary job growth have suffered dismal growth in output. Conversely, the sectors in which growth has been more robust have contributed little to overall job growth. This phenomenon appears to straddle both low-paying and high-paying sectors.

For example, the low-paying retail trade and accommodations and food services sectors have seen rates of output growth below the levels of both the pace of job growth and aggregate payroll growth in those sectors. But the same is true, and even worse, in the well-paying professional and technical services sector. Whether it is clerks and cashiers in retail, waiters in food services or professional sales staffing, all three sectors—and others—have seen a pickup in short-term and seasonal hiring in lieu of meaningful levels of capital spending. And what sector has seen (until recently) massive levels of capital investment, and high levels of output growth? Take a look at mining (and think oil and gas fracking), though it is a sector in which jobs have been created at levels far lower than the hype over that sector prior to the recent collapse in energy prices.

Finally, what is the connection between falling or flat real wages and excess global labor? While there has been some good work on the subject in academia reaching a variety of conclusions, I have found studies by Avraham Ebenstein, Ann Harrison and Margaret McMillan14 to be particularly instructive. In a recent paper, they conclude and demonstrate that there are,

“significant effects of globalization, with offshoring to low wage countries and imports both associated with wage declines for US workers … globalization has led to the reallocation of workers away from high-wage manufacturing jobs into other sectors and other occupations, with large declines in wages among workers who switch, explaining the large differences between industry and occupational analyses. While other research has focused primarily on China’s trade, we find that offshoring to China has also contributed to wage declines among U.S. workers.” [emphasis added]

I emphasize the importance of imports in this connection because, while there generally is significant focus on trade in considering the health of the U.S. economy, policy makers have had a tendency to concentrate their concerns on exports. Export volume is important but, at 13% of GDP, is not a substantial driver of U.S. economic activity, jobs/wages, or price levels. Imports, which are an equivalent to 17% of GDP, have not only the impact on jobs/wages as indicated by Ebenstein, Harrison and McMillan, but—as I will get into more deeply below—have an impact on a broad range of domestic prices that has been poorly understood until recently. Import prices are also heavily impacted by other countries’ efforts to devalue their currencies vs. the dollar, an ongoing phenomenon that has grown to alarming levels recently.

Inflation: Goods, Services, Assets, and the Strong Dollar

In addition to all of exogenous excess labor and attendant imbalances in trade, the middle class and working class are being further squeezed by a strong dollar that itself derives in from the conditions of production oversupply and excess global savings. These factors are overwhelmingly deflationary, and, with that statement, I take issue with the more vintage, expectations-focused interpretation of post-recession inflation data. The foregoing is still very much in fashion within the central banking community, but I believe that deflationary pressures have clearly moved from the transitory to the sustained, despite proclamations to the contrary. The U.S. consumer is arguably well-benefitted by lower prices for goods, but the corollary negative pressure on worker’s wages (and the threat that the post 2012 recovery in home prices—with homes the largest asset of the middle class—will ultimately prove ephemeral, as I discuss further below) is of far greater importance to households already substantially burdened by debt that becomes even more burdensome amidst falling price and wage levels.

Central banks throughout the world have been fighting valiantly to reflate their economies since the Great Recession, with less success than disappointment. That disinflation has begun to impact emerging markets, in addition to developed ones, is particularly disturbing. (China, for example has seen its annual inflation rate fall to ~1.5% from as high as 5.5% in 2011.)

Enough time has passed for us to take honest stock of the effect of extraordinary monetary easing (zero interest rate policy, coupled with quantitative easing) on the U.S. economy during and after the Great Recession. Extraordinary easing was fruitful—in the sense of offering a “shock and awe” sized crutch to the household and commercial sectors of the economy—during the recession itself and in the early part of the recovery. The Federal Reserve succeeded in stabilizing the financial sector and making investment in capital goods as attractive as possible. When increased capital spending and overall reflation did not result, the Fed redoubled its easing in an effort to make risk-free (i.e. government bond) investing as unattractive as possible, and, again, to spur investment in new and expanded productive assets. That effort (QE3) met with limited results at best and succeeded, rather, in spurring investment more in the secondary market for stocks and real estate assets, as opposed to primary investment. Whether secondary markets have bubbled or not is sort of beside the point. The point is that the economy as a whole has clearly not reflated.

So this leads us to consider whether extraordinary monetary easing was “successful” in general, and whether or not non-policy phenomena (the global oversupply of capital and production, among other things) are behind what has transpired over the last several years. There are two pretty obvious points to summon at this juncture:

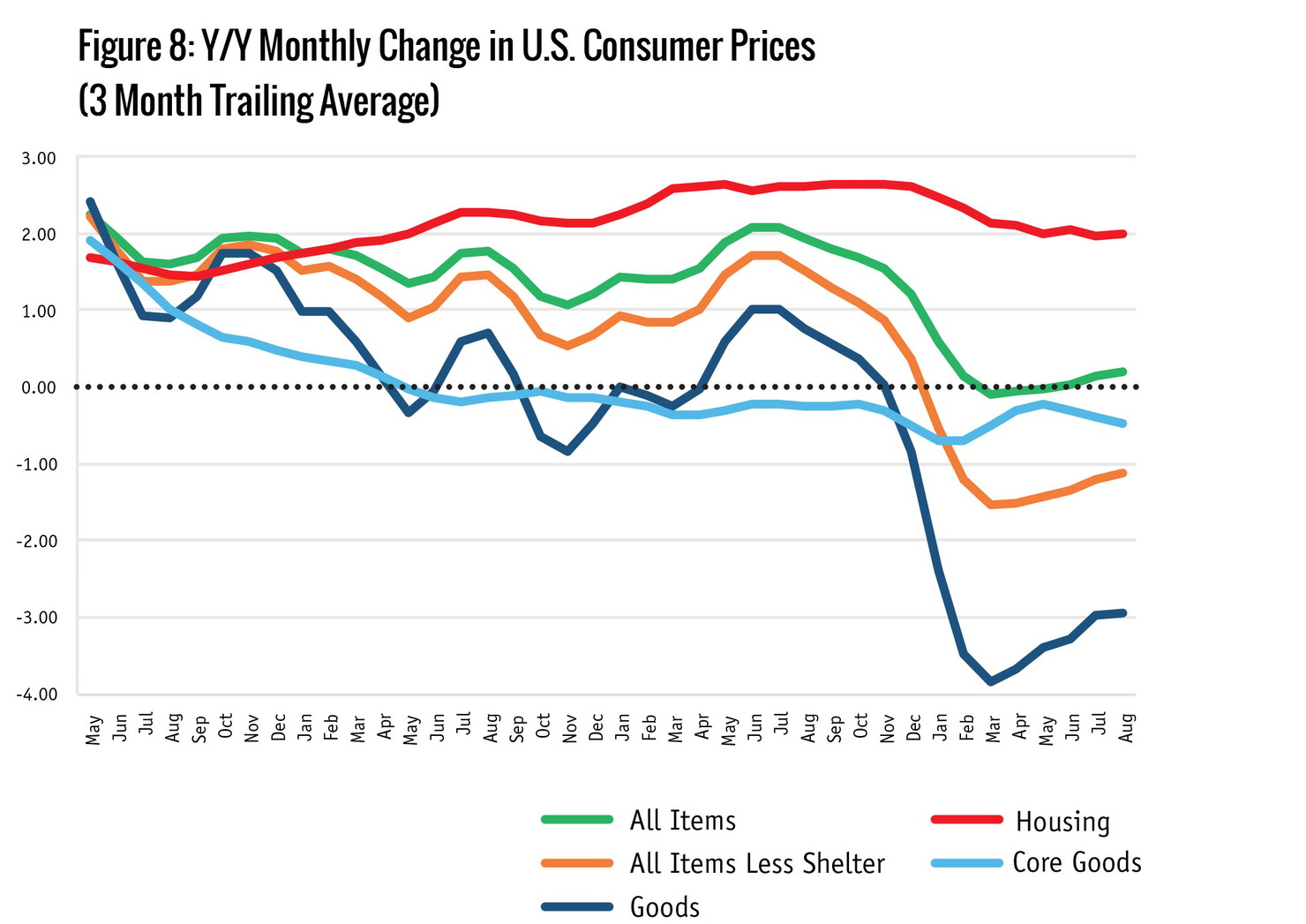

- Overall disinflation has accelerated over the past years, and core goods (all goods less food and energy) have been in sustained outright deflation since early 2013 (see Figure 8);15 and

- After the period known on Wall Street as the “taper tantrum”16 interest rates have fallen back to low levels notwithstanding that the Federal Reserve is no longer engaged in quantitative easing.

While point (1), above, might beg the question of whether or not the Fed did “enough” easing to reflate the economy, the fact that interest rates reverted to low levels when the easing stopped must at least raise the question of whether or not it was quantitative easing at all that brought down medium to long-term interest rates. As must be obvious from the foregoing, I believe that monetary policy has had a muted impact on longer-term interest rates, which—like inflation —were destined to fall regardless of policy, based upon the old-fashioned realities of non-central-bank-related supply and demand.

As Figure 8 also illustrates, what remains of inflation in the U.S. is now almost exclusively confined to the housing sector. Weak global demand, relative to supply, has done away with inflation in commodities (energy, metals, most agriculture), and the overhang of foreign labor in the tradables sectors is forcing U.S. import prices downward and encouraging our trading partners to maintain weak currencies relative to the dollar. So whatever inflation we continue to experience in the U.S. is in entirely wholly domestic sectors, the largest of which is the housing economy, constituting some 40% of the consumer price index. Inflation in medical services and tertiary education has, while declining, also proven to be a factor, although a far smaller one, owing—in large part—to the fact that prices in those sectors are connected with third-party payer systems (employer-paid health insurance systems and government-guaranteed student loans, respectively) which disconnect pricing from real supply/demand issues.

Housing prices have been rising for a number of reasons related to the after effects of the mortgage crisis and the Great Recession. While too extensive to delve into here, readers may find it useful to consider a presentation on the subject I completed in March 2015 on behalf of Westwood Capital and The Century Foundation, entitled "The 'Recovery' in U.S. Housing Prices,"17 which notes that:

“Despite a seemingly inexorable recovery in home prices since 2012 [the actual nadir of housing prices in the U.S.] such recovery is not a recovery in the demand for owner-occupied homes. Rather, it is more…(i) the knock-on effect of the mortgage bubble and crisis of the mid-2000s that has yielded a shortage of homes for sale; and (ii) historically low mortgage interest rates unique to the present macroeconomic environment. Neither of these phenomena are characteristic of a normal recovery in the housing sector and are not likely to be sustainable in the absence of other supporting factors [most particularly, wage growth]. Accordingly, it is unclear that we have reached a point of real price discovery in U.S. housing and, with deflationary pressures bearing down on the U.S. economy, whether the housing sector—as it has for the past two years—will continue in its role as nearly the only force holding service sector price growth positive.”

So, in the first quarter of 2016, we are faced with the legacy of six years of post-recession economic policy that, while seeing improvement in headline unemployment and job formation, has failed to reflate most prices and wages, failed to return growth potential to pre-recessionary trends, failed to restore household debt-to-income ratios to traditional levels, failed to reverse the enormous loss in labor force participation, failed to restore proportion of full-time to part-time jobs, and failed to stem the decline in labor’s share of GDP—while “succeeding” in temporarily inflating the prices of assets (housing, commercial properties and the values of businesses/stocks) and, derivatively therewith, increasing levels of income and wealth polarization in the United States.

The foregoing may strike one as an overly harsh indictment of economic policy since the Great Recession, but it is fundamentally correct. Because expansive fiscal policies have either remained underutilized or have been reversed due to government austerity measures, and because glaringly problematic issues of international trade have been largely ignored for either ideological or geopolitical reasons, that indictment has—somewhat unfairly—been brought down on the shoulders of monetary policy makers.

I say “somewhat unfairly” above because post-recession monetary policy has been necessarily aimed at economic stabilization and the restoration of monetary normalcy before the U.S. economy confronts its next downturn. Monetary policy has not, and cannot by itself, effect changes to the use of available capital for expansive investment, it can only—and then only at the margin—make it more attractive to obtain capital for investment. Monetary policy has not, and cannot by itself, rectify trade imbalances; it can only tinker at the margins to influence foreign exchange rates amid a myriad of other market and economic forces. And yet, in the world of economic policy, the monetary tool has been the only expansionary apparatus employed in the U.S. since the short-lived fiscal stimulus of 2009-2010.

As a result, the principal U.S. economic policy debate in 2014 and 2015, with very few exceptions, revolved around the markets’ and the media’s assessment of when the Fed was going to raise the policy rates of interest and begin to “normalize” monetary policy. Despite evident continued slack in the domestic economy and slowing in the global economy that some economists and market analysts think might drift into renewed recession, our principal obsession seems to be obtaining an “all clear” from the Fed in the form of a series of interest rate hikes. And let’s face it, hanging around at the zero lower bound of interest rates is very uncomfortable for central bankers, who depend on interest rate policy to combat recessions.

While I believe that raising interest rates in the U.S., as the Fed did in December 2015, was unwise (mostly because it strengthened the dollar against other currencies that were already being aggressively and intentionally devalued), I concede that the one symbolic increase did not really cause the market sell-off of early 2016—U.S. economic data was already deteriorating by the Fed’s December move. But having the Fed declare victory and leave the field of battle is not the same as having engaged with and overcome the forces of continued economic slump. To do that, we need to finally repair the break in the virtuous circle of savings, investment, and consumption.

Rewriting U.S. Economic Policy for the Age of Oversupply

In order to avoid more of the same sluggish economic results, in order to revitalize the middle class and reduce the levels of wealth and income polarization in the U.S., there is one thing we need to do above all else: Absorb excess labor via an intensive revitalization of our public infrastructure via public sector spending.

There are clearly many other things that the U.S. government could do to improve the domestic economic picture and improve the well-being of citizens: enhancing tax fairness, enacting a universal/single-payer healthcare, rationalizing relations with certain U.S. trading partners, improving access to higher education, continuing reform of financial institutions, raising the minimum wage, and further restructuring hopelessly underwater debts left over from the bubble of the 2000s. Some of these are controversial, others less so, but pretty much all would have some incrementally beneficial effect on the economy and people of the United States. But none of them hold a candle to the need to grow economic activity by reversing the decade’s long decline in labor’s share of GDP.

Moreover, the connection between underemployment and pretty much all of the other economic ills of the U.S. is important to appreciate. In the final sense it is only economic growth (and growth that is more widely shared) that will stabilize the U.S. economy, return it to its potential, reflate prices and wages, reduce the high levels of household debt on a real basis, and enable the country to maintain—and even expand—social benefits. And meaningful growth (sustained annual GDP growth of 3.5% to 4%) is very unlikely to resume in the U.S., for all the reasons discussed previously in this white paper, without a bold change in policy focus. Here is how to get that done.

One way of approaching this issue is to start by clarifying what the labor issue in the U.S. is not:

- It is not a supply-side issue. Well, it is an oversupply issue—but that is not how economists and politicians typically speak about the supply side. Cutting taxes and creating subsidies to encourage investment by the private sector is not effective in an environment in which the world is bedeviled by excess supply relative to aggregate demand, and the U.S. has experienced a shift abroad of the jobs involved in the production of that excess supply. For the same reason, extraordinarily low interest rates have proven unable to spur expansion of private, primary investment.

- It is not a minimum wage issue. Raising the minimum wage may, but is not certain to, serve to improve the share of production obtained by our lowest paid workers (some of whom may find themselves displaced by substitution of technology). But it will not serve to absorb the un- and under-utilized pool of labor in the U.S.

- It is not an issue of labor’s bargaining power. Yes, the union movement has been decimated in the U.S., and collective bargaining as an established right has been whittled away over the past 30 years. But as long as there is a substantial excess of labor, a revitalized union movement—as welcome as that may be—is not likely to emerge, and where it does, it may result in a displacement of jobs to non-unionized jurisdictions or abroad.

The underutilization of labor, the lack of growth, the continued falling share of labor as a percent of GDP—all of these issues and more—are the result not of depressed wages or insufficient job formation counts; they are the result of an insufficient amount of work relative to the body of labor willing to work. Increase the demand for labor, and all other issues—wage levels, price reflation, productivity and the reswitching dilemma, capital spending, and even zero interest rates—take care of themselves … it really is that simple.

The labor problem in America is one of natural causes—increased and excess competition from exogenous labor, combined with the emergence of technologies that reduce the need for labor without, in themselves, increasing aggregate production. The problem isn’t the causes; it is the lack of an effective policy response to same.

Put in terms set forth earlier in this paper, government needs to step into the breach now unfilled by the private sector to dramatically increase job-producing capital investment. Government must close the virtuous circle of capital that is otherwise blocked in the age of oversupply. And there is a screaming need for such capital investment in the improvement of the country’s dilapidated infrastructure.

And, yes, I am proposing that the U.S. government use its credit (either directly or through a newly constituted infrastructure bank) to borrow the excess capital necessary to make such investment from the overstuffed pool of excess capital sloshing around the globe and available to the U.S. at interest rates that make borrowing and investing it wisely an economic imperative, if not actually a moral one.18 And if one thing is certain about the lackluster years that have passed since the Great Recession, the capital glut is so large that the borrowing of enormous sums by the government of the U.S. will not push interest rates dramatically higher and the “printing of money” by the Fed has not debased the U.S. dollar.19 The argument I made in The Age of Oversupply20 in 2013 has stood the test of time21—the U.S. has been unable to move robustly forward amidst a slump that remains substantially unaddressed.

As I wrote back then, a five-year $1.2 trillion public investment program in transportation, energy, communications, and water infrastructure would create an additional 5.5 million jobs or more in each year of the program—directly, through the projects themselves, and indirectly, through the multiplier effect on other sectors of the economy. With the American Society of Civil Engineers telling us that our present infrastructure backlog is nearly $2.5 trillion, projects will not be hard to find. And neither will labor. Adding 5.5 million workers (assuming all were new/returning entrants to the labor force) would barely restore the labor force participation rate back to the levels of 2010, still well below levels prior to the recession.

Conclusion

In this paper I have argued the case for why the U.S. remains in an economic slump. I have addressed how certain headline economic data has been misunderstood and has misguided the path of economic policy to a significant extent since the Great Recession. I have explored “under the hood” of the U.S. economy for data that explains many of the mysteries of the U.S. economy in light of ongoing global oversupply and other factors that have changed economic realities from conditions that existing before the age of oversupply. And I have presented what I believe is the critical policy initiative that would directly address the underlying problems and restore the U.S. economy to growth and prosperity in less time than has already passed since the end of the Great Recession.

Nevertheless, we are left with a schism in American society, in government and in the academe of political economy: An inability to think outside the rigid ideological architecture of prior eras. This must end, or the U.S. will—in my mind without question—suffer the perpetual slump we have seen in Japan since they hit the wall in 1990.

This schism has become so sharp and seemingly irreconcilable, that I am reminded of the words of the Austrian-Israeli philosopher Martin Buber, writing on the differences between Christians and Jews. Buber wrote, “ … to the Christian, the Jew is the incomprehensibly obdurate man who declines to see what has happened; and to the Jew, the Christian is the incomprehensibly daring man who affirms in an unredeemed world that its redemption has been accomplished. This is a gulf which no human power can bridge.”

Let us hope and, yes, pray that divisions in matters of practical economics do not rise to the level of religious theology … I am pretty certain that Franklin Roosevelt would be horrified to think that they might. Let us have the courage to try some things that would actually work.

About the Author

Daniel Alpert is an American investment banker, think tank fellow, and author. He is best known for his writing on the credit bubble and the ensuing financial crisis of the 2000s, and his many articles and papers on the U.S. housing market, banking, regulatory matters and global macroeconomics. Alpert has been widely quoted and published in print outlets, including the Wall Street Journal, the New York Times, Reuters, the Associated Press, Bloomberg, Forbes, and Fortune. He is a frequent commentator on business news networks, including Bloomberg, CNBC and Fox Business News. He is the author of The Age of Oversupply: Confronting the Greatest Challenge to the Global Economy (Penguin Portfolio) on the effect of macroeconomic imbalances on advanced economies. Daniel Alpert is founding Managing Partner of the New York-based investment bank Westwood Capital, LLC and its affiliates and a fellow of the New York-based Century Foundation, one of the nation’s oldest think tanks.