Report Published June 18, 2015 · Updated June 18, 2015 · 30 minute read

Student Loans and Graduation from American Universities

Introduction

A college degree has been the ticket to the middle class in America. That is even truer today than it was before the Great Recession. As the connection between college and the middle class has become common knowledge in our society, more and more young people have sought a college degree while at the same time more and more middle class families have lost the ability to pay for some or all of college, and loans have surpassed grants as a way to fund college education. The result: a generation carrying a large amount of student loan debt. Is this good public policy?

In this paper, Rachel E. Dwyer, a professor at The Ohio State University, examines a key aspect of this problem: whether and to what extent student loans impact graduation from college. This is because, as Dwyer notes “Student loans, then, represent both an opportunity and a risk, just as do other forms of credit.” They can be a good investment in a young person’s future or not. Or, as Dwyer puts it, “Are loans associated with graduation or do they represent a drag on completion?”

Using data from The National Longitudinal Survey of Youth, Dwyer shows that the relationship between debt and graduation is more complex than it would appear. Her first finding is that the relationship between graduation probabilities and student indebtedness is an inverted U curve. As debt goes up, graduation possibilities increase and then flatten out at around $10,000 a year. Once beyond $10,000, the curve turns downward, indicating that “increasing amounts of debt at the highest levels do little to increase graduation probabilities.” The effect of debt on graduation also varies by family background and institution. “Debt appears to be less consequential—positively or negatively—for the graduation probabilities for more advantaged students.” Significant differences also appear between those who attend public universities and those who attend private universities. “Debt is just not very significant among students at the more advantaged college institutions.”

The implications of these findings are significant for public policy makers. Those who drop out with debt have made a “failed investment” in Dwyer’s words. This should lead us to re-evaluate the ways we finance college attendance.

Dwyer’s study of debt and graduation rates is the latest in a series of ahead-of-the-curve, groundbreaking pieces published by Third Way as part of its NEXT initiative. NEXT is made up of in-depth, commissioned academic research papers that look at trends that will shape policy over the coming decades. In particular, we are aiming to unpack some of the prevailing assumptions that routinely define, and often constrain, Democratic and progressive economic and social policy debates.

In this series we seek to answer the central domestic policy challenge of the 21st century: how to ensure American middle class prosperity and individual success in an era of ever-intensifying globalization and technological upheaval. It’s the defining question of our time, and one that as a country we’re far from answering.

Each paper dives into one aspect of middle class prosperity—such as education, retirement, achievement, or the safety net. Our aim is to challenge, and ultimately change, some of the prevailing assumptions that routinely define, and often constrain, Democratic and progressive economic and social policy debates. And by doing that, we’ll be able to help push the conversation towards a new, more modern understanding of America’s middle class challenges—and spur fresh ideas for a new era.

Jonathan Cowan

President, Third Way

Dr. Elaine C. Kamarck

Resident Scholar, Third Way

* * *

Over the past few years there has been a growing unease in American society about the high and rising volume of student loans taken on by college students. The New York Times sounded the alarm about “a generation hobbled by the soaring cost of college,”1 identifying a range of negative consequences for young adults starting out with a “hefty yoke of student loan debt,”2 including delayed homeownership and marriage, even potentially “stunting” the whole economy as young people focus on repaying debt instead of consuming.3 While concerns about college costs had simmered for decades, worries about student debt came to a head with the Great Recession and a new appreciation of the risks of indebtedness in an uncertain economy. There have been some reforms to the student loan system since then (notably, increased restraints on private lenders), but like the mortgage and consumer credit systems, the overall structure of student loans remains largely intact. Since the recession, student loan indebtedness has continued to rise and student default rates are close to 14%.4

The drumbeat of negativity about student loans begs the question: if student loans are so lousy, why do so many American college students carry debt? The answer of course is that a college degree is increasingly required to gain a middle class life. College-educated workers earn higher wages, receive more and better benefits, and often enjoy greater job security than workers who have only a high school degree.5 At the same time, college costs have increased (though not as much as many think) and students have increasingly constrained resources for paying for those costs.6 Decades of slow (or no) income growth for most Americans have left parents with less savings to dedicate to their children’s education. While grant aid given directly by colleges to students has increased, federal grant aid has declined. Many students quite reasonably decide to make up the difference with loans. Indeed, this is what they are told to do by the financial aid system.

Student loans, then, represent both an opportunity and a risk, just as do other forms of credit. Loans have allowed many students — thousands of students in several generations — to attend and complete college when they would not otherwise have been able to do so. For these students, loans are an investment, in human capital and a middle class life. This investment, like all investments, must be made without knowledge of the future, and there are risks to holding debt even for the very good cause of attaining a college degree. Unforeseen events can make it harder to pay back loans taken on with the reasonable expectation of a good return, including macro-economic shifts like an economic downturn, and personal misfortunes like job loss, illness, or divorce. Much of the media attention is on large-scale and long-term consequence across the life course and for the economy at large, but thinking of student loans as an investment with risk focuses our attention on the key good that is purportedly being purchased with student loans: the college degree. The federal financial aid system explicitly promotes loans as a tool for accessing college and getting needed support to garner that degree.

Rising Student Loan Indebtedness

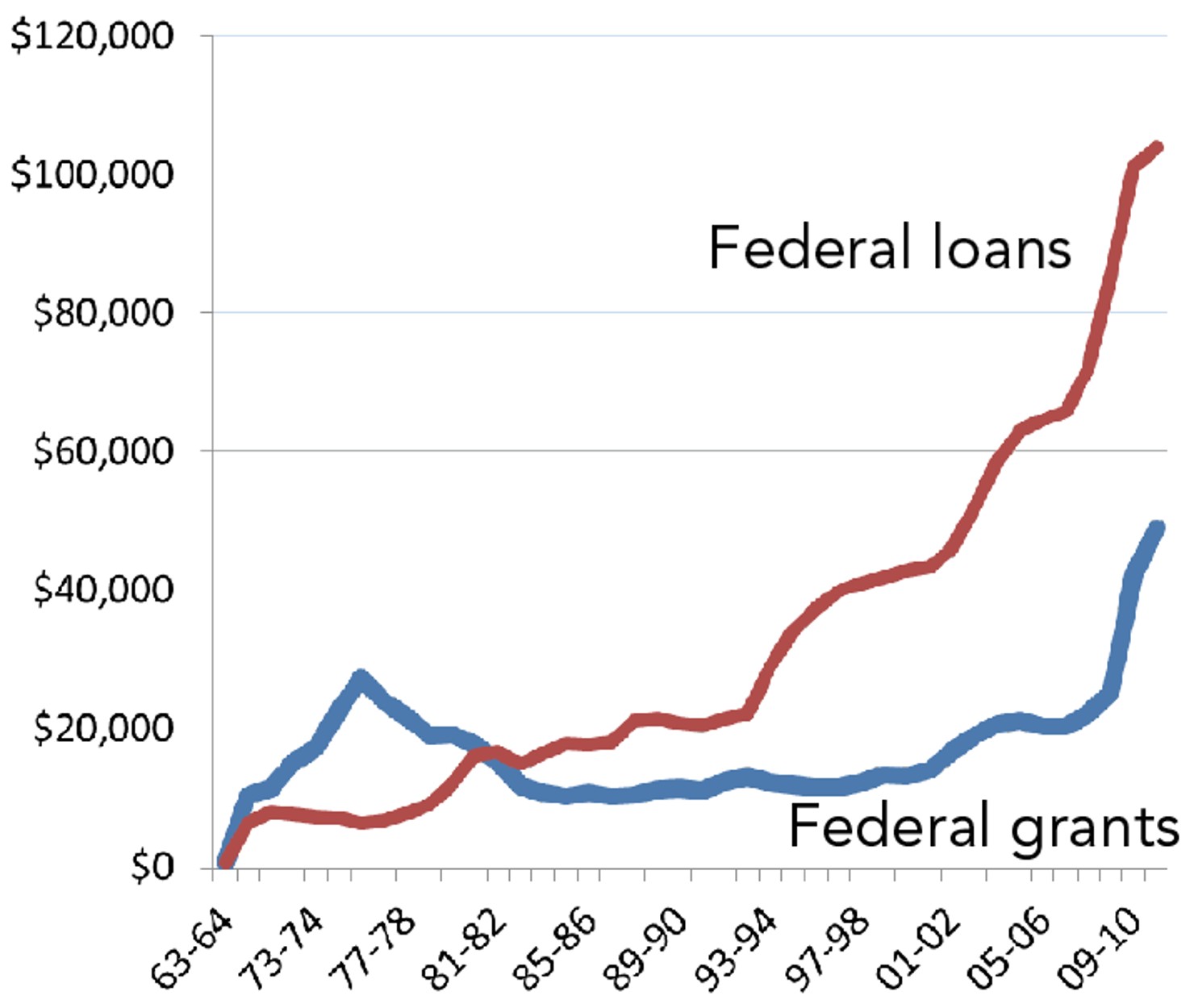

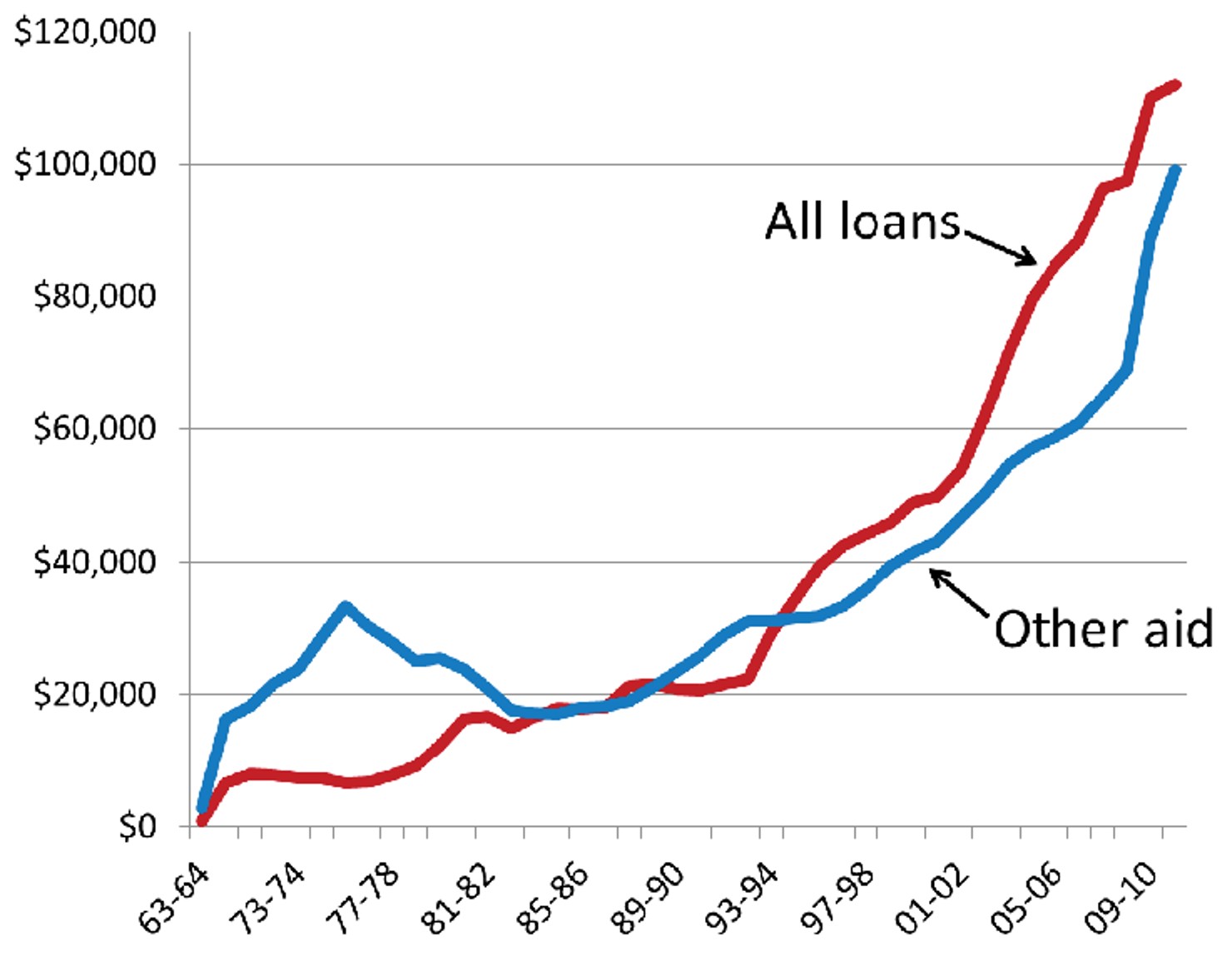

Student loans are now the main source of financial aid provided by the U.S. government to support college students. Loans became increasingly important with the neoliberal turn in American political economy in the 1980s. During the expansion of higher education in the 1960s and 1970s, the federal government provided many more dollars of grant aid than loans. Grant aid declined during the 1980s, and loans became the default policy, shifting the burden to individuals. As Figure 1 shows, loans surpassed grants and have become ever more important since. The national reckoning over debt that occurred after the Great Recession did lead to legislative action that resulted in new dollars dedicated to grant aid, but there remains a large gap between grants and loans, and it remains to be seen how long the renewed commitment to grants will last. As Figure 2 shows, other sources such as grants from colleges and universities have filled in some of the gap left by lowered federal grant aid. Yet loans stubbornly remain the largest category of aid outside of families. The gap between loans and all other aid became particularly large in the years leading up to the Great Recession in the 2000s.

Figure 1. Total federal student aid, academic years1963-64 to 2010-117

Figure 2. Total student aid from all sources, academic years1963-64 to 2010-118

The rising volume of student loans is often interpreted to represent increasing loan amounts held by student debt-holders, and this is part of the story, but the volume has also gone up because increasing percentages of students take on loans. In 1989-1990, 19% of students took out loans, increasing to about 35% in 2007-2008.9 Over time, fewer students are taking out no loans during the course their career. Why are more students taking out loans (and higher loan amounts) than ever before? One reason is the rising cost of college. Although net costs—the amounts that students actually pay (and take out loans to cover) after factoring in other types of aid such as grants and work study—have risen much less than the published “sticker price” of college, net costs are still up more than 50% since the mid-1990s, and of course those grants are still expenditures by the federal government and institutions.10 Another reason for higher student indebtedness is that we have an increasingly diverse college population, with more students coming from relatively disadvantaged families who may have limited resources to support their children. However, even students from traditionally middle class families have become more stretched since the 1980s. Increasing student loan indebtedness has coincided with economic restructuring and slow income growth that have made it more difficult for individuals and families to achieve the markers of a middle class life, including paying for their children to go to college.11 With fewer family resources available to pay for college, more students make up the difference with loans.

The U.S. higher education system, with its complex financial aid system significantly based on loans, provides opportunities for large percentages of students to enroll in college, but has been far less effective in graduating similar percentages of students. Only somewhat more than half of students (about 55-59% depending on the year and data source) who enroll at a four-year institutions graduate within six years.12 This puts the U.S. near the bottom of OECD countries in completion rates for the bachelor’s degree or equivalent.13 Low completion rates combined with high access to loans raises questions about whether and how loan-holding is associated with graduation rates. Student loans are quite easy to get for most students, as there is no check for credit-worthiness and loans are typically offered as part of a package with other kinds of support so that taking on debt is normalized as a part of the ordinary process of financial aid. At the same time, interest rates on student loans are set by a political process, and the loans cannot be discharged in a bankruptcy. Student loans are thus very easy to take out for most students, but at the cost of limitations and requirements that do not apply to other forms of credit.

Thus the big policy question that needs to be addressed is: Are loans associated with graduation or do they represent a drag on completion? Next, I present findings proposing that the relationship is more complex than it appears at first glance.*

*Dwyer, Rachel E., Laura McCloud, and Randy Hodson. 2012. “Debt and Graduation from American Universities.” Social Forces 90:1133-1155; Dwyer, Rachel E., Randy Hodson, and Laura McCloud. 2013. “Gender, Debt, and Dropping Out of College.” Gender & Society 27:30-55.

Student Loans and College Graduation

Research on student loans and college graduation has been mixed, with some research finding debt helps graduation, while other papers find students with higher levels of debt delay graduation. Dwyer, Hodson, and McCloud argue that these mixed results occur because students in fact have diverse experiences with debt, and there are especially important differences by levels of debt.14 Here we return to the idea that student loans represent an opportunity and a risk. Loans provide needed resources for students who might otherwise not be able to enroll in college. Even for students who are relatively more well-off, loans may allow them to go to a more prestigious college or a college with the right fit for their abilities and interests. Students who take out loans may work fewer hours or not at all, allowing them to focus on completing their studies. Taking on debt is thus for many students a reasonable investment in getting a college degree, a credential which is ever more important on the job market.15 (Even during the Great Recession when many young adults were hit hard, those with college degrees fared better than those with less education and lacking the crucial credential.)16 It may take time for a student loan investment to pay off in the labor market, but graduating college is a significant and relatively near-term payoff that for most reaps benefits.

Carrying debt also raises vulnerabilities however, and these risks become more readily felt when students take on particularly large loans. We argue that the risk associated with larger loan amounts is associated with diminishing returns to taking on debt to get a college degree. These diminishing returns could develop through both direct and indirect effects of student loans on graduation probabilities. In the most direct effect, large amounts of debt could become a deterrent to continuing in school. Students may feel they have to stop for a while and work either to save money or to pay down loans. In one New York Times article for example, a student at Bowling Green University in Ohio dropped out after accruing large amounts of debt, saying “[f]or me to finish it would mean borrowing more money,” something that she was unwilling to do.17 At the higher levels of debt, students may reach the borrowing limits of federal loans and shift to private loans which need to be repaid more quickly and often at worse terms. There are also more indirect effects where having high loan amounts could be a signal of other kinds of difficulties or problems that also forestall graduation. It could be that students who get into significant debt are more likely to have significant personal challenges requiring more resources that could also get in the way of graduating. In this case, loans may not be the only immediate cause of dropping out or not graduating, but one factor among many. To the extent that these more indirect effects occur, students who already face significant challenges are weighed down with another burden, that of high student debt without having a college degree. In these cases, the investment in student loans turns sour as the key goal of a college degree remains out of reach.

We tested our expectation of a positive but diminishing effect of student loans on college graduation using data from a cohort of young adults coming of age in the 2000s. The National Longitudinal Survey of Youth, 1997 Cohort (NLSY97) follows a group of young adults who were born between 1980 and 1984 who were entering the most common college going years in the early to mid-2000s, when carrying student loans became the majority experience on college campuses. The first interviews took place in 1997 when the respondents were 12-16 years old, and continued annually (very recently becoming biannual), and thus the survey provides a wealth of information on family background and the transition to adulthood, including college experiences. Students who enter college are asked detailed information about college for every term they are enrolled, including about the amount of loans they took out. Because the benefits of post-secondary education largely accrue to those with a four-year degree (rather than a two-year or only some college), we focus on the crucial outcome of attaining a bachelor’s degree. Our sample includes all students who have ever enrolled in a four-year college and we evaluate the odds that these students graduate with a four-year degree.

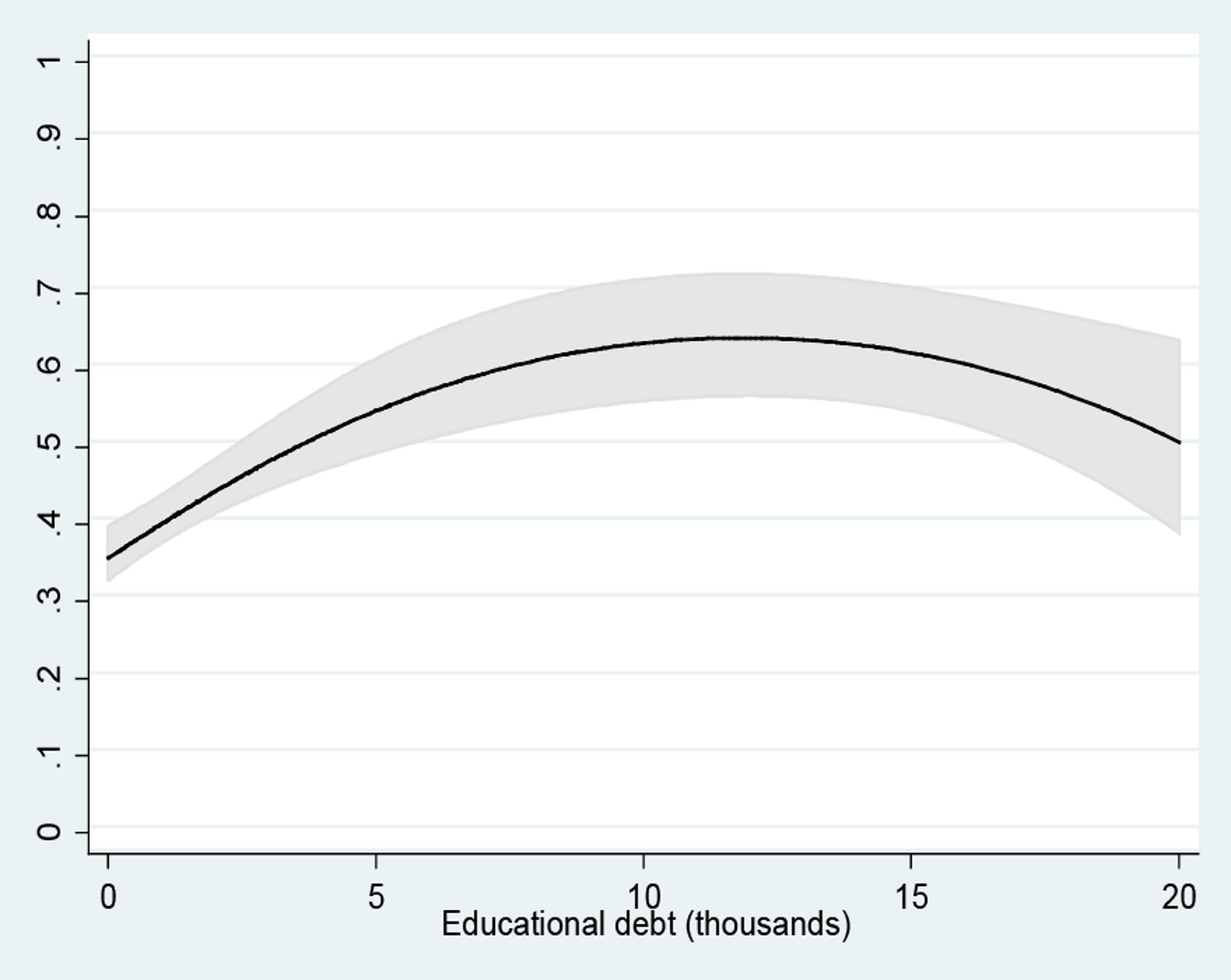

Our results support our expectations that student loans facilitate graduating at lower levels of debt, but that there are declining returns to taking on additional debt at high levels. Figure 3 shows our estimate of graduation probabilities across levels of indebtedness for young adults in the NLSY97 who ever enrolled in a four-year college. As the line on the graph goes up, graduation probabilities increase. The line flattens at high levels of debt, starting at around $10,000 a year, and turns downward at the highest levels towards $20,000. This inverted-U pattern indicates that increasing amounts of debt at the highest levels do little to increase graduation probabilities. Note that students who take on high levels of debt still have a greater chance of graduating from college than those who take on no debt. This is likely because taking on some debt indicates a certain commitment to the college enterprise. The pattern of diminishing returns at raises questions, however, about the negative consequences of becoming of highly indebted. Students at those high levels may start to have worries about whether they can afford to continue in college, and they may face significant personal challenges that are manifesting in high debt levels. Because debt is so easy to take on, there are few checks in the system that signal to a student that they are getting into trouble until the debt mounts.

Figure 3. Probability of graduating with a four-year degree across student loan levels18

College students in the United States are a highly diverse group and they attend a range of institutions. We wondered whether the positive and then diminishing returns to debt occurred for all students, or whether the pattern was concentrated in particular student populations. Next we discuss our findings for how the role of debt in college graduation varies across places and students’ family background.

Differences by College Institution and Family Background

Are all students similarly affected by debt? In our studies we have found that experiences at public universities are significantly differentiated from private colleges. The role of debt also is different for students from different social class backgrounds. Debt appears to be less consequential—positively or negatively—for the graduation probabilities for more advantaged students. Differences in the role of debt likely emerges from the varied opportunities and risks faced by students in different social positions.

The United States has a vast and differentiated public university system serving a wide diversity of students: about two-thirds of all students who enroll in a four-year college attend a public university. Students have a range of options to choose from and the promise of high-quality education at a much lower cost than many private universities. Public universities keep tuition down in part by maintaining larger enrollments, pulling in more students but charging less per student. Private universities, in contrast, typically have smaller class sizes and their budgets depend more on retaining and graduating the students they recruit. These institutional differences may lead private universities to have the resources and the motivation to provide more support for students to manage financial aid, get through college, and graduate than are available at many public colleges. This means that debt may be less consequential—positively or negatively—for students at private universities.

Debt may also be less consequential for the student population that attends private colleges compared to those who attend public universities. Students at private universities are still more financially advantaged than the average public university student. These students may have more in the way of family resources to fall back on so that even if they decide to take on debt, they do so with lower risk than less advantaged students. Private university students who are less advantaged may be different from similarly advantaged students who go to public universities. They may be higher achievers, have more non-financial family support, or have greater drive or motivation—all factors that may both make them more likely to attend a private university and be less moved by debt. (As we detail in the Appendix, we include controls in our models for some of the most significant differentiating factors between public and private student populations, but as it is difficult to fully control for such factors, we expect the differences between college types are due both to institutional factors and differences in the types of students selected into public and private colleges.)

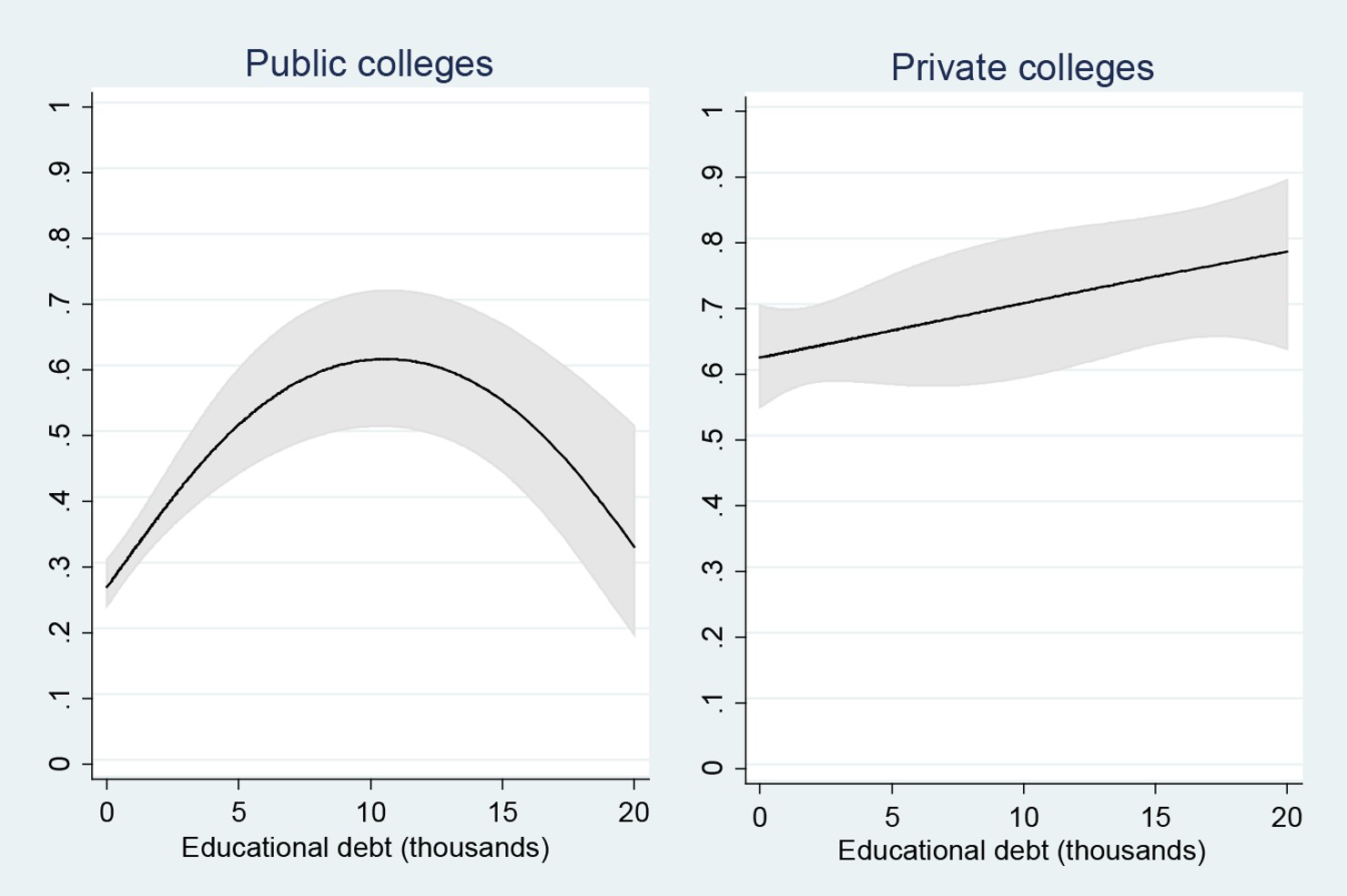

Our analyses show that in the NLSY97 cohort, the positive and then diminishing effect of student loan indebtedness is concentrated among students who attended only public universities during their time in college. Figure 4 shows that the inverted U-shape of the relationship between levels of student loans and the probability of graduating holds for public university students. At private colleges, in contrast, the line is straight and not very steep. In fact, the relationship is not even statistically significant. The line is higher, reflecting the fact that students at private universities are on average significantly more likely to graduate than students at public universities. The factors that make students at private colleges more likely to graduate appear to swamp debt as an influence on graduation probabilities. Debt is just not very significant among students at the more advantaged college institutions.

Figure 4. Probability of graduating college across student loan levels, public vs private colleges19

We have argued that one reason students at public universities are more influenced by the positives and negatives of debt-holding is the population there is more diverse. Given that the large majority of college students attend public colleges (about two-thirds), there is quite a range of experience, including both advantaged and disadvantaged students. This raises the question of whether there are distinctive experiences in debt-holding among different populations of public university students? Arguably, we should be most concerned about public universities given that the U.S. graduation crisis is concentrated in the public sector.20 Factors that influence the likelihood of graduating at public universities significantly affect the educational attainment of the whole U.S. population.

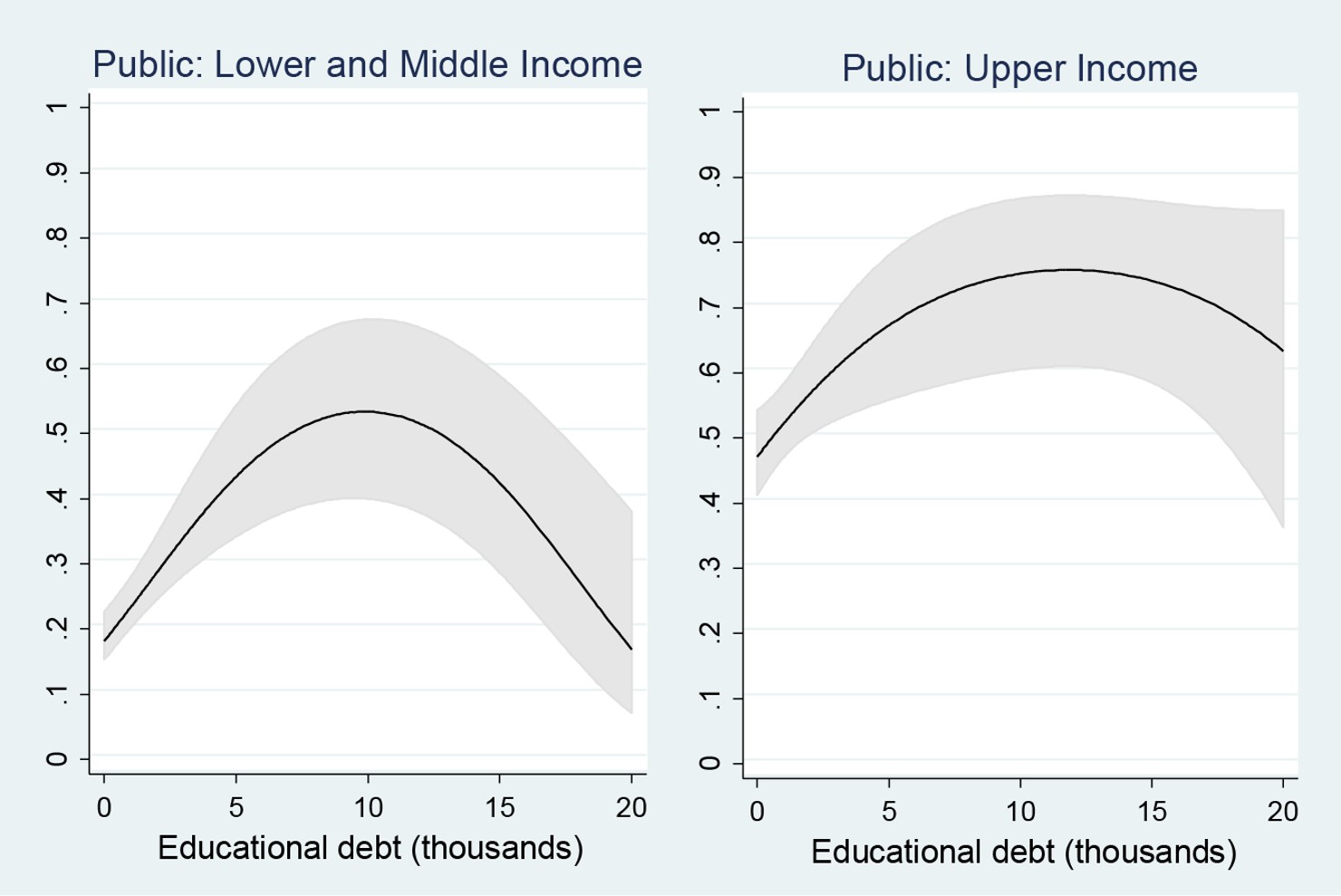

In our studies so far we have looked at debt and graduation for students from upper-income families compared to students from middle- and lower- income backgrounds. Students from more advantaged backgrounds typically have more resources to dedicate to college from a range of sources, including their families. Even those who take on debt can do so with some reassurance that their families could back them up if they got into trouble. Students from middle and lower class backgrounds are both more likely to rely on debt for the positive boost to enrollment and graduation, but are also more likely to experience negative consequences of carrying high levels of debt. We found that the effects of debt-holding within public universities are stratified by family background. Figure 5 presents results of the relationship between debt levels and college graduation for public university students separated by family background.

Both the upper-income and the middle- and lower-income populations show that inverted U-shape, but there are two important differences. The flattening of the curve happens at higher debt levels for the upper-income students compared to less-advantaged students, so that the point of diminishing returns is higher for the more-advantaged students. This is consistent with our expectation that students from higher-income backgrounds face lower risks from holding student loans compared to less-advantaged students. The curve also takes a sharper downward turn at higher levels of debt for lower- and middle-income students than for their more-advantaged peers. At the highest levels of debt, any facilitative effects have almost entirely disappeared.

Figure 5. Probability of graduating college across student loan levels, by family background in public colleges21

The intense attention to student loans in the media and public debates has raised important questions about our system of relying heavily on loans to finance educational attainment. These debates often focus on broad questions about whether a college degree is worth taking on loans to attain. Our research provides the needed caution that we cannot expect student loans to have the same effects for all students, and at all levels of debt. Especially given our highly diverse and differentiated higher education system, student loan-holding has complex and varied associations with important outcomes like graduating with a four-year degree in hand. In other research, we have also explored variation in experiences for women compared to men.22 Our discussion also highlights a problem that gets all too little attention in public conversations today: the many students who leave college with debt, but without a degree.

Dropping Out With Debt

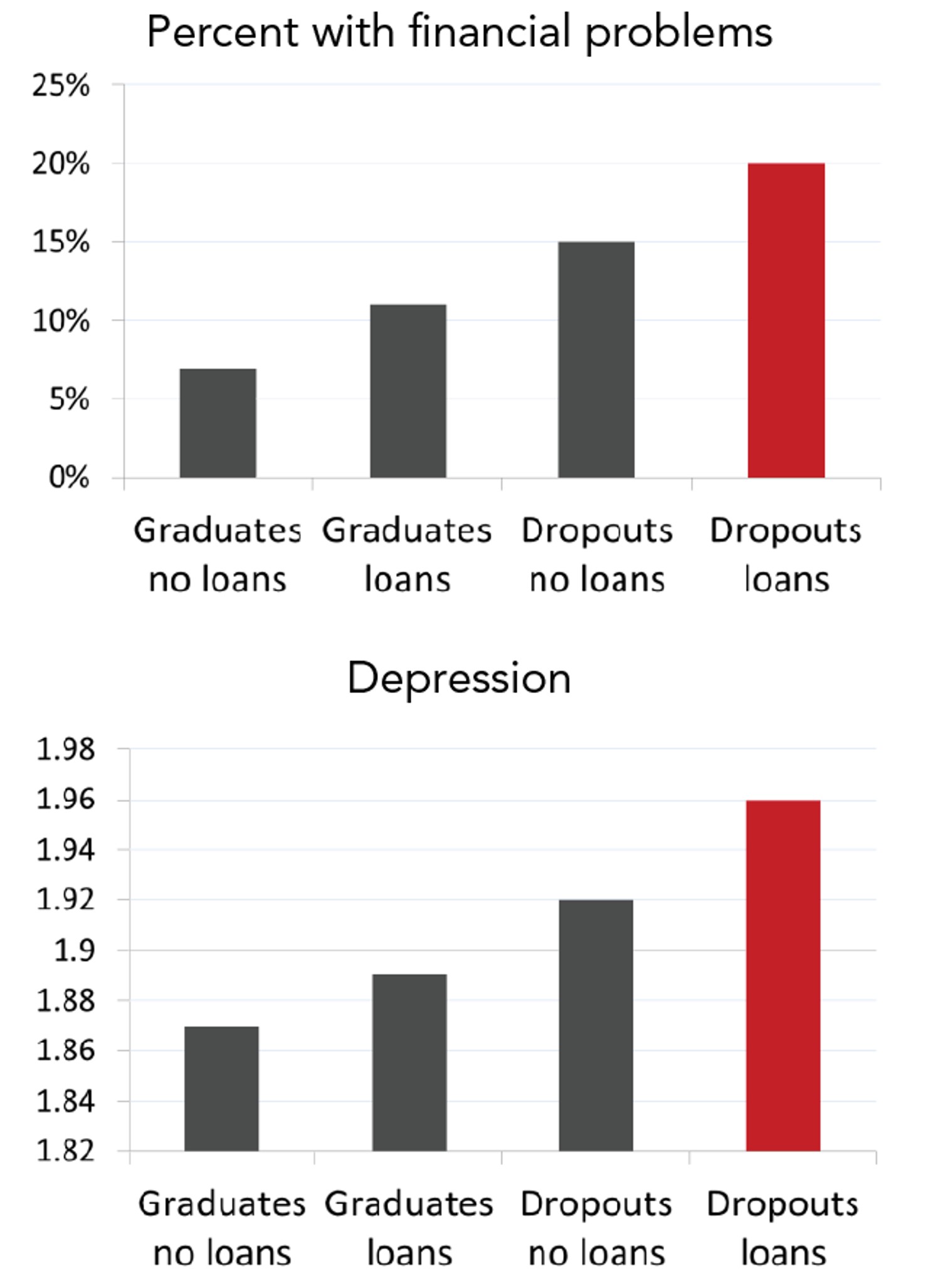

In recent decades, there has been little difference in the wage opportunities for young adults with some college versus for those with only a high school degree. Dropping out with debt thus represents a failed investment. Even when students who leave college do eventually return to finish, they have lost precious time to accrue financial gains from a college degree. Dropouts with debt must work to repay their loans without the labor market advantages of a valuable credential. Since student loans are not dischargeable in a bankruptcy, even the most financially distressed former students cannot get out from under their debt. It is perhaps not surprising then, that we find dropouts with debt have more financial problems and higher rates of anxiety and depression than dropouts without loans, and graduates with loans (Figure 6).

Figure 6. Financial problems and depression for graduates and dropouts, with and without loans23

The situation of dropouts with loans but without a degree deserves more attention that it has received in the public debate. There are a range of issues. How can we support more students who enroll in college to complete and attain that crucial college degree? How and why do students get into very high levels of debt and can we improve services to help students manage the challenging problem of paying for college? Should student loans be protected from bankruptcy even for former students in grave financial difficulties from costly medical emergencies, family problems, or other catastrophes? While it is also important to consider the situation of college graduates who carry debt, it is the many carrying debt without the degree who are likely in the worst shape.

Conclusion

Do student loans support college graduation? Our findings provide evidence that they can do so, but with the catch that there are diminishing returns at the highest levels of debt. The diminishing returns are strongest for lower- and middle-income groups at public universities, the populations that also face the most challenges in graduating with a degree. The diminishing returns are worrisome for many reasons, including because they raise the specter of dropouts carrying significant debt. To the extent that high levels of indebtedness provoke an aversion to continuing with a college career, the system that is intended to encourage college attainment ends up discouraging persistence. High levels of indebtedness may also signal other personal or financial problems that may be magnified by a high student loan bill. At the same time, the positive effects of debt for graduation show that students take on debt for the very rational and reasonable goal of securing a college degree and the greater chances of a middle class life that come along with it. Unfortunately, the opportunities and risks of using loans to pursue that goal are different for people in different social positions. As our findings show, the risks are highest for those who need the college degree the most.

The greatest investment our country makes in higher educational attainment is in the federal student loan system. As college costs have risen and family resources have become more stretched, the loan system has become ever more broad-based. We know little about the long-term consequences of large percentages of current and former college students carrying loans because loan-holding was far less normative for past generations. Here we have looked at a cohort of the oldest Millennials, coming of age in the first decade of the 21st century, and there is new evidence that debt-holding may delay important transitions like marriage and parenthood for this group.24 Today’s younger Millennials are even more likely to hold debt. These youth face a difficult labor market and increasingly privatized retirement systems that demand careful planning and individualized savings plans. At the same time, a college degree is only more important to achieving a solid and stable middle class life. We are in a sense living through a large-scale social experiment with uncertain outcomes.

Given these high stakes, we must evaluate the opportunities and risks of financing attainment in this way. These opportunities and risks accrue at two different levels that are often conflated in discussions over student debt. There are opportunities and risks for individuals deciding whether to take on debt to support college enrollment and graduation. There are also opportunities and risks for our society in relying so heavily on loans to support higher educational attainment. A concern about the reliance on debt at the system level does not necessarily imply that young people should avoid student loans, however. It is perfectly defensible to be highly critical of the overall system of student loans, while at the same time be highly supportive of many students taking out loans to get a college degree given the current system. One worry about the current debate is that students hear critiques of student loans and decide not to take out loans even if that means they also avoid college. The choice is often not really “debt versus no debt,” but “debt with a college degree versus no debt and no college degree.” When we are evaluating the choices for young people we need to be sure that we’re getting the counterfactual right.25 At the same time, just because loans may be a reasonable strategy for getting a college degree under the current system, the architecture of financial aid may be suboptimal for society at large if it undersupplies college graduates and burdens a large number of young adults with debt loads that they carry long into adulthood, suppressing consumption and savings. We may prefer instead to invest in more opportunity using methods that produce less individual and systemic risk.

Methodological Appendix

We used the National Longitudinal Survey of Youth, 1997 Cohort (NLSY97) to examine the relationship between student loan indebtedness and college graduation. The NLSY97 is funded by the Bureau of Labor Statistics to advance understanding of the life course trajectory of a cohort of young adults coming of age in the early 2000s. Similar to other studies of college graduation, we restricted the analytic sample to those 25 and older in 2007, the last year of data that we use. We focused on young adults who attended college in the past but who had either successfully graduated with a four-year degree or had dropped out by the time of the analysis, resulting in a sample of 1,898 young adults. We included only those who ever attended a four-year college.

We use logistic regression and analyze whether the respondent reports having graduated with a Bachelor’s degree by 2007. In our sample of those who ever attended college, about half had graduated from college by 2007. We measure the last loans taken while the respondent was enrolled in college because we expect the last loans will have the greatest influence on the decision to stay enrolled or leave college. The question on student loans is asked for every term enrolled: “Other than assistance you received from relatives and friends, how much did you borrow in government-subsidized loans or other types of loans while you attended this school/institution?” We find similar results when we use cumulative loans taken out across all years. To evaluate our theory that loans will have a positive and then diminishing association with college graduation implies that debt should be modeled with a nonlinear quadratic terms, we included measures for educational debt and educational debt squared. Because debt is a skewed measure, we top-coded educational debt at $20,000 — the 99th percentile.

We measure college institutional type by dividing students between those who ever attended a private college, versus those who only attended public universities. This is a conservative definition of public college attendance by focusing on those who have never attended a private college. We measure family background using parental household income in 1996 (the first year of data collection), and identify income groups based on the position of parent’s income in the 1996 national income distribution: upper-income if in the top quartile and lower- and middle-income if in the bottom three quartiles. We include measures of several respondent characteristics that prior research suggests are most likely to influence the relationship between debt and graduation as control variables in our analysis. We control for sex, race/ethnicity, marital status, and parental status while enrolled, high school Grade Point Average, whether the respondent was enrolled part-time, and whether the respondent was employed more than 20 hours per week on average during the school year.

To measure negative experiences among graduates and drop-outs, we measure depression and financial problems during the Great Recession. To measure depression, we use a five-category mental health scale in the NLSY97. Respondents are asked to report on a four-point scale how often they had the following experiences in the month before the interview: 1) felt depressed, 2) been a happy person, 3) felt down or blue, 4) felt calm and peaceful, or 5) been a nervous person. We created a scale by measuring the mean response across the five items for each respondent (with item 2 and 4 reverse coded so that all the items were scaled so that higher responses indicated worse mental health). For financial problems, we measure the percent of respondents who reported having trouble making payments.

* * *

Rachel E. Dwyer is Associate Professor of Sociology at Ohio State University. She has published widely on rising economic inequality in America and the declining fortunes of the middle class, reflected in part in growing indebtedness. Her research on social inequality has appeared in top academic outlets including the American Sociological Review, Social Forces, Social Science Research, Gender & Society, The Sociological Quarterly, and Social Problems. Her work has been supported by the National Science Foundation, a grant from the Eunice Kennedy Shriver National Institute of Child Health & Human Development awarded to the Ohio State University Institute for Population Research, and the National Endowment for Financial Education. She has served as an advisor to the Postsecondary Education Working Group of the President’s Council on Financial Capability.

With growing public debate over student debt and continuing challenges for young adults during and after the Great Recession, Dwyer’s work increasingly focuses on issues in financing college. In addition to studying debt and college completion she has (along with her co-authors) studied debt, self-concepts, and mental health. In her current work she examines the role of debt in life course transitions like marriage and becoming a parent. She is especially concerned about variations in debt experiences across different socio-economic groups and within the highly diverse higher education landscape in the United States.