Report Published April 8, 2015 · Updated April 8, 2015 · 23 minute read

Jobless Recoveries

Introduction

Why Economic Recoveries Are Different Than They Used To Be

In the last three months, the U.S. economy created more than one million jobs and median wages jumped forward—finally. It took five years from the end of the Great Recession for truly robust job and wage growth to take hold. It took so long, in fact, that a new phrase entered the lexicon—“the jobless recovery.”

Henry Siu and Nir Jaimovich may have an answer as to why. In their work presented here, Siu (University of British Columbia) and Jaimovich (Duke University) begin by looking at previous recessions and uncovered a striking pattern. “…Averaged over the three early episodes, employment turns around about four months after the recession; in the recent episodes, the average turnaround time is 21 months.” In other words, recent recessions, especially the most recent, are not your father’s recessions. Jobs recover very slowly with many people stuck in part time or lower paying jobs.

Siu and Jaimovich explain the emergence of this phenomenon by looking at the loss, over time, of “routine” jobs. They argue that “… many of the routine occupations that were once commonplace have begun to disappear, while others have become obsolete. This is because the tasks involved in these occupations, by their nature, are prime candidates to be performed by new technologies.” By showing the trends in routine and non-routine jobs through a series of recessions, they illustrate a central economic problem of our time. The 21st century economy doesn’t create the sorts of jobs we used to have. Job creation is no longer simply a function of an economy wide recovery, it poses challenges that were not part of earlier recessions.

This paper should make policy makers think hard about job creation in the information economy. It is the latest in a series of ahead-of-the-curve, groundbreaking pieces published through Third Way’s NEXT initiative. NEXT is made up of in-depth, commissioned academic research papers that look at trends that will shape policy over the coming decades. In particular, we are aiming to unpack some of the prevailing assumptions that routinely define, and often constrain, Democratic and progressive economic and social policy debates.

In this series we seek to answer the central domestic policy challenge of the 21st century: how to ensure American middle class prosperity and individual success in an era of ever-intensifying globalization and technological upheaval. It’s the defining question of our time, and one that as a country we’re far from answering.

Each paper dives into one aspect of middle class prosperity—such as education, retirement, achievement, or the safety net. Our aim is to challenge, and ultimately change, some of the prevailing assumptions that routinely define, and often constrain, Democratic and progressive economic and social policy debates. And by doing that, we’ll be able to help push the conversation towards a new, more modern understanding of America’s middle class challenges—and spur fresh ideas for a new era.

Jonathan Cowan

President, Third Way

Dr. Elaine C. Kamarck

Resident Scholar, Third Way

* * *

The Great Recession officially ended in June 2009 but it has taken many Americans years to believe it and many still don’t. On a number of dimensions, the recovery would receive strong marks. Both the Dow Jones and S&P 500 have more than doubled in value in the past five and half years. Inflation has been kept in check, hovering at around 2% per year. Real GDP growth has been solid, especially in the past two quarters; average real income earned in the United States has grown by about 7%, recouping all of the losses since the recession, and then some.

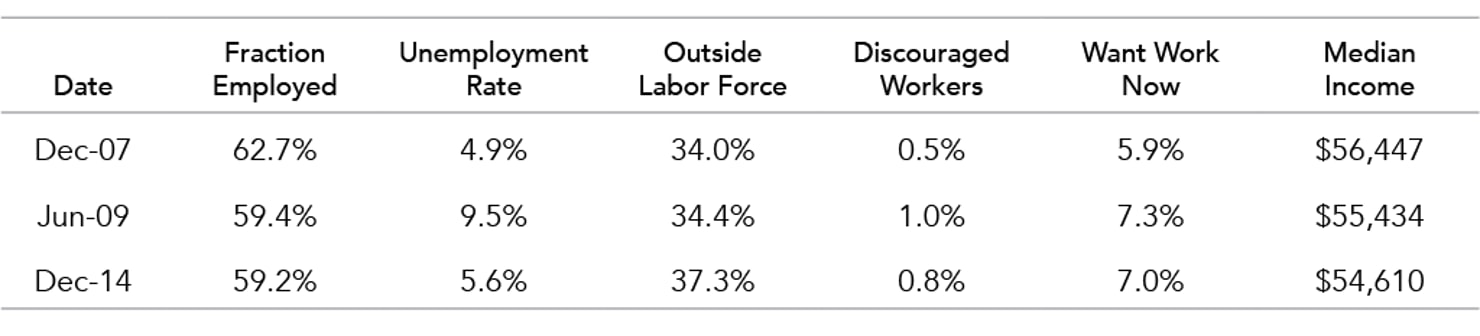

But in spite of these statistics, when it comes to the labor market, it is hard to muster a passing grade. Since the end of the recession more than a half decade ago, the U.S. labor market has still not recovered. The clearest indication of this: the fraction of the adult population that is employed. We report this statistic in the first column of Table 1. At the economic peak in December 2007, approximately 63% of American adults had a job.1 At recession’s end in June 2009, that number had fallen to 59.4%. In December 2014 (the most recent data available as of writing) it is lower still, at 59.2% — that is, a smaller fraction of the adult population is working today than at the end of the recession. Moreover, this statistic masks the deterioration in the quality of job opportunities. For instance, of those with jobs, the fraction of people working part time because they could only find part-time work more than doubled over the course of the recession. This has remained essentially unchanged since recession’s end.2

Numbers like these have given rise to a new expression, the jobless recovery. In this paper we’ll try and explain why employment opportunities no longer bounce back following recessions by looking at how the occupational structure of the economy has changed.

Table 1: Measures of Recovery following the Great Recession

Data from the Bureau of Labor Statistics, Current Population Survey and Sentier Research.

The Current State of the Labor Market

How does this dismal employment picture square with the recent positive news on the unemployment front? As of December 2014, the unemployment rate had fallen below 6%, down from a peak of almost 10% following the recession.

Each month, the U.S. Bureau of Labor Statistics surveys 60,000 households and classifies each respondent into one of three categories: employed, unemployed, and not in the labor force. A person is employed if she is engaged in any work for pay. A person is classified as unemployed if she does not have a job and has actively searched for work in the past four weeks. Finally, a person is considered outside of the labor force if she does not have a job and has not recently searched for one.

The unemployment rate is measured as the ratio of unemployed to the sum of the unemployed and employed. It excludes those outside of the labor force. As such, a fall in the unemployment rate can be a result of a “true” recovery in the sense that more unemployed have found work. However, it can also be a result of the unemployed quitting their job search all together, dropping out of the labor force.

In the case of the recent recovery, the fall in the unemployment rate is not due to improving job prospects among American adults. Instead, since June 2009 the fraction of the population not participating in the labor force has risen from 34.4% to 37.3%. This rise masks the malaise in the labor market that is untold by the unemployment statistics. So while business and economic analysts have hailed the strong job growth experienced in 2014, its important to keep this in perspective: while the economy added nearly 2.9M jobs in the past 12 months, there were also 2.3M additional adults in the United States during that time period, due simply to population growth.

Certainly, the rise in labor force non-participation observed since the recession could be a matter of choice. Perhaps American adults increasingly prefer not to work or search for work. However, this seems unlikely — at the very least — as an explanation for the entire rise in non-participation.

In fact, among the American adults that are not in the labor force, a surprisingly large fraction would rather be working. The BLS measures this in a number of ways. First, consider the fraction of people outside the labor force who are discouraged workers.3 This share doubled over the course of the recession, and is still almost three-fourths higher than it was in December 2007.

Second, in order to qualify as a discouraged worker, a person must have actively searched for work within the last 12 months. It is likely, then, that this understates the actual number of people who are discouraged by labor market conditions. This is especially true in the current environment, given the unprecedented number of individuals experiencing long-term unemployment.4 Hence, we consider an additional measure: those who are not in the labor force but defined by the BLS as wanting a job now. As Table 1 indicates, the fraction of such individuals among the group of non-participants rose from 5.9% to 7.3% over the course of the recession. Five and half years later, this is largely unchanged at 7.0%.

Overall, these statistics paint a picture of a labor market that has made little in-roads since the recession’s end.5 As a result, the rising tide of economic prosperity since 2009 has not lifted all boats. This is certainly true for America’s middle-class. This is illustrated in the final column of Table 1. Real median household income fell by about 2% over the course of the Great Recession and continued to fall until mid-2011.6 Currently, real income of the median household is still lower than at the end of the recession, representing an approximate 3.5% loss relative to 2007. This poor performance of median income, despite the economic recovery, highlights the continued widening of income inequality.7 Middle-class Americans have seen little in the way of improving job prospects or material well-being.

Jobless Recoveries

As the previous discussion illustrates, the labor market has fared poorly in the five and half years since the end of the recession. While the Great Recession was certainly not your “garden-variety” downturn, the poor performance of employment since then is not entirely new.

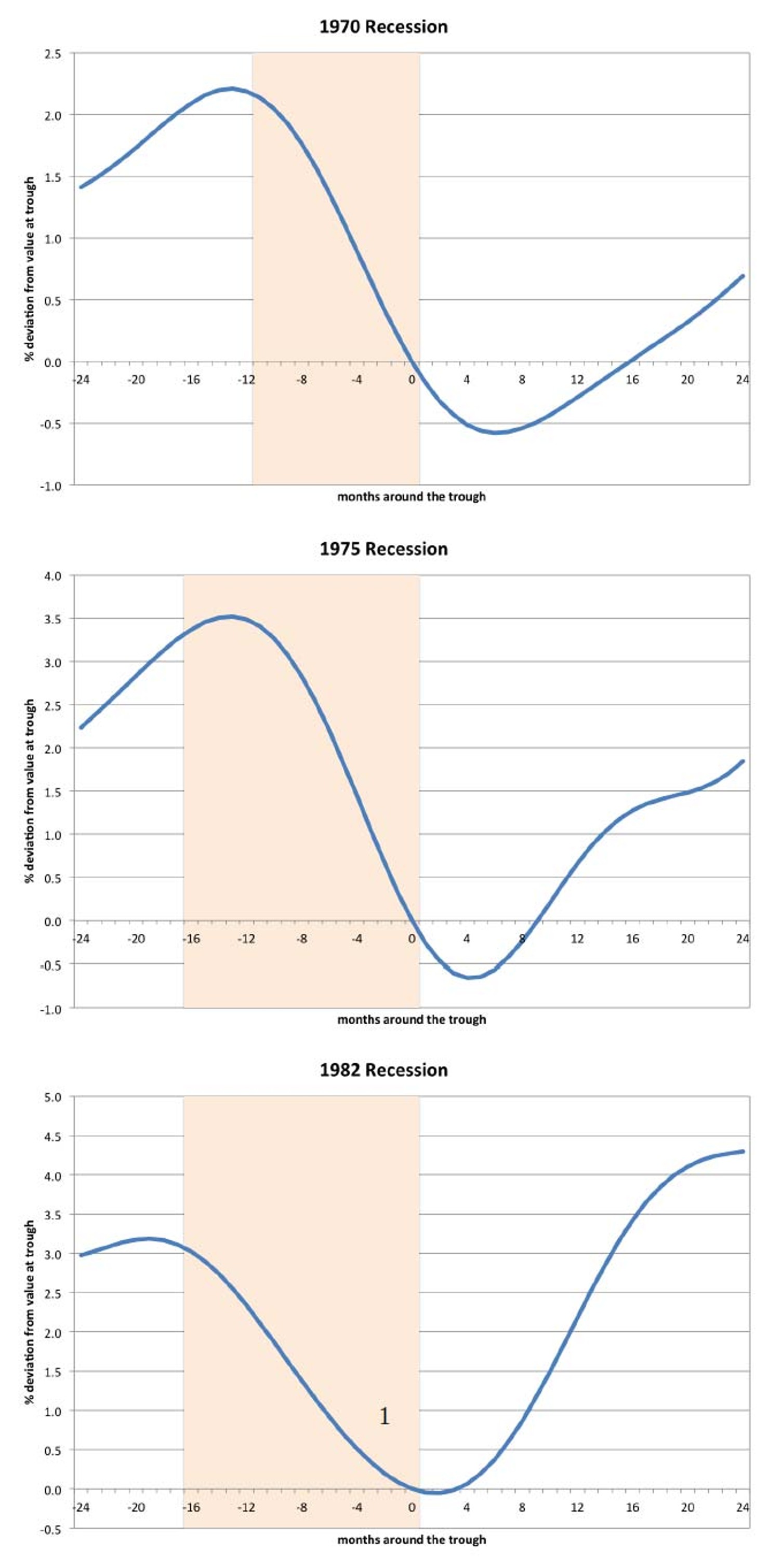

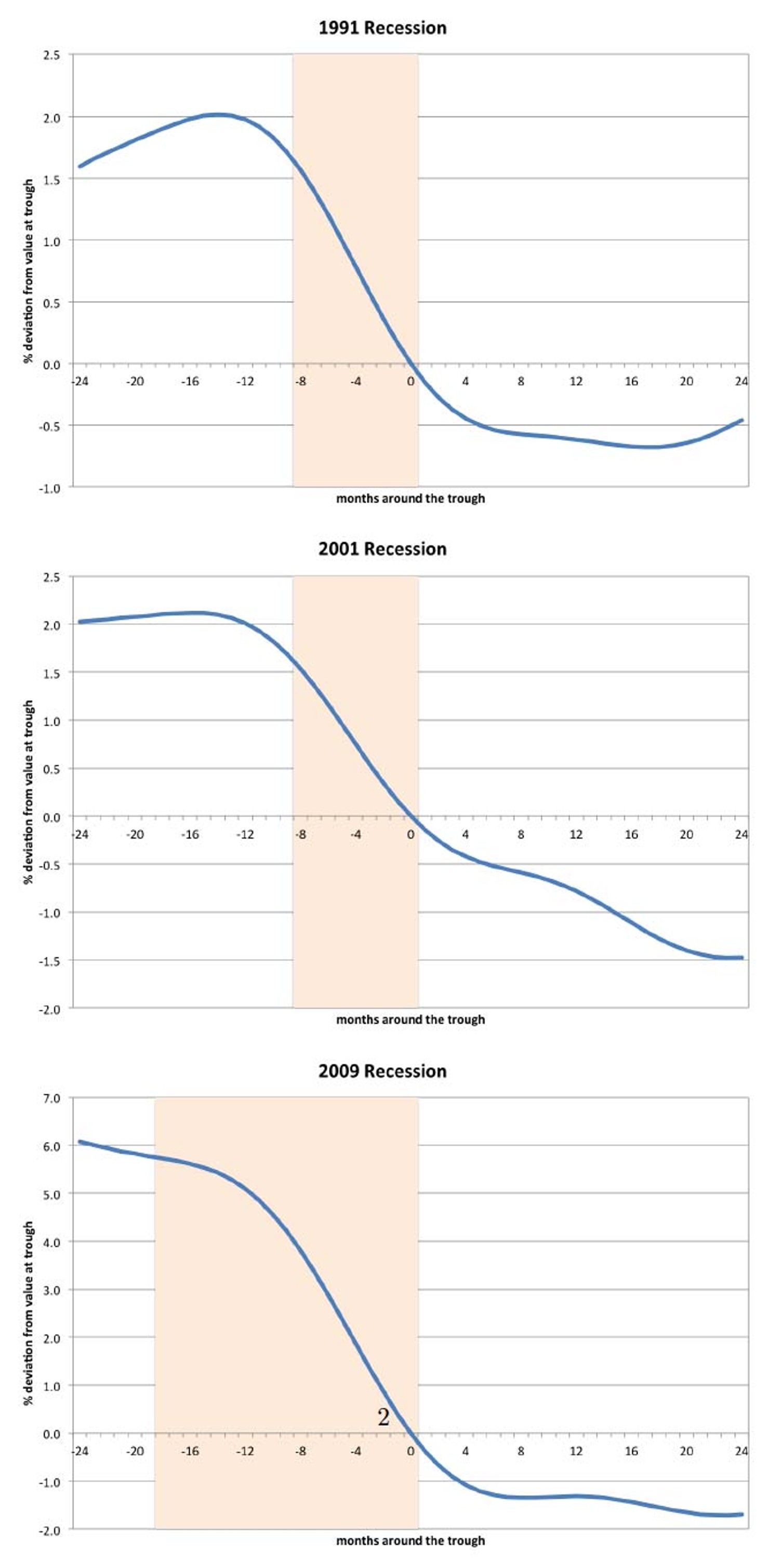

In a jobless recovery, the rebound in an economy’s income and output following recession is accompanied by a much more tepid recovery — or no recovery at all — in employment opportunities. Figures 1 and 2 illustrate this phenomenon.

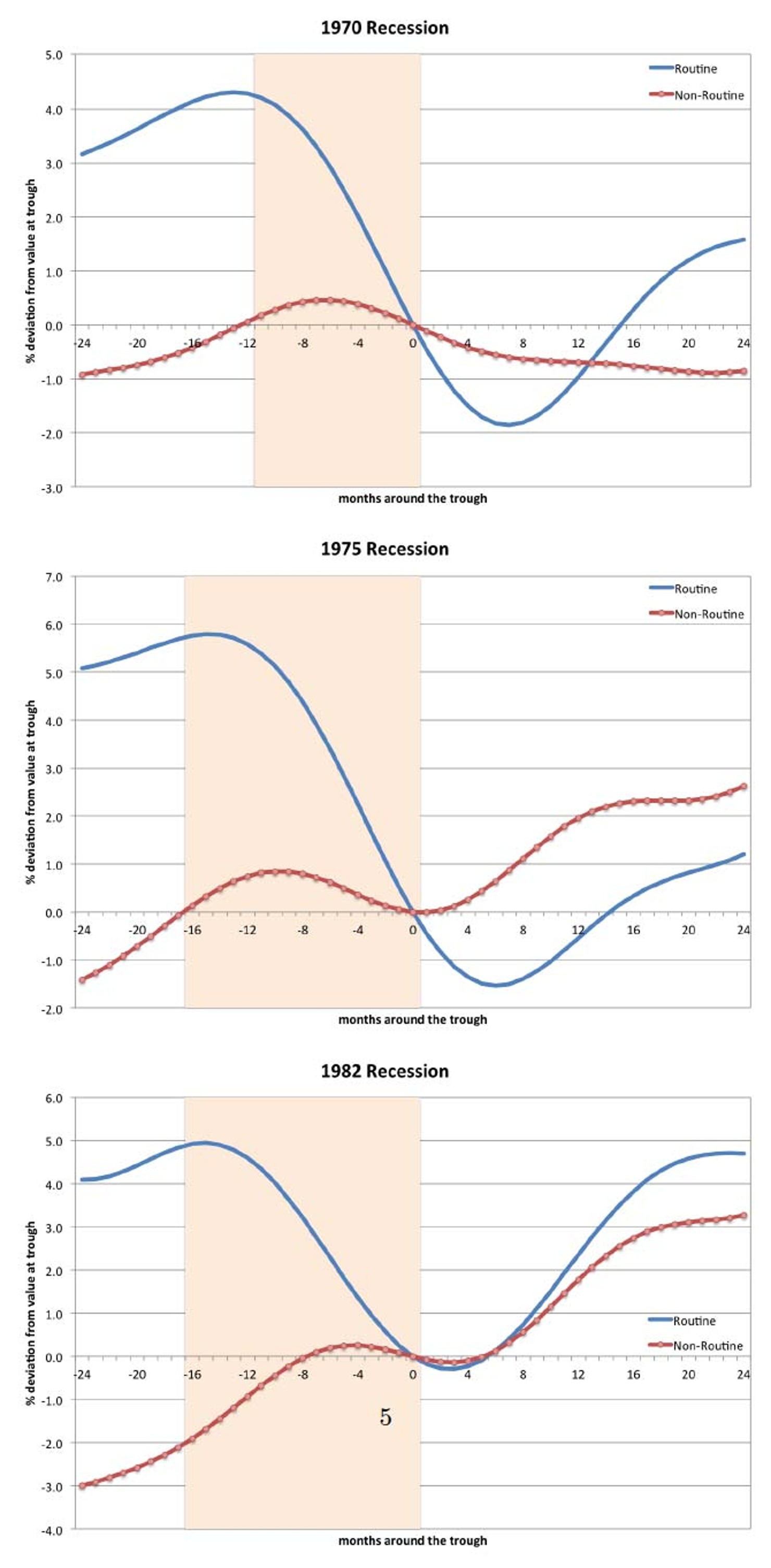

We first plot the behavior of per capita employment that was considered “typical” following economic downturns.8 Figure 1 illustrates the response after each of the 1970, 1975, and 1982 recessions.9 These responses are expressed relative to employment’s value at the end of each recession. On the horizontal axis, the end of each recession is labeled as month 0. The shaded region indicates the recession itself, from peak to trough.

Take the 1970 recession for example. During the recession, employment falls by approximately 2%. After the recession ends in month 0, employment begins to expand at the 6 month mark. The fact that employment begins its vigorous recovery within two quarters of the recovery in aggregate output is typical of the business cycle prior to the mid-1980s.10 This is true of the other two recessions in Figure 1 as well.

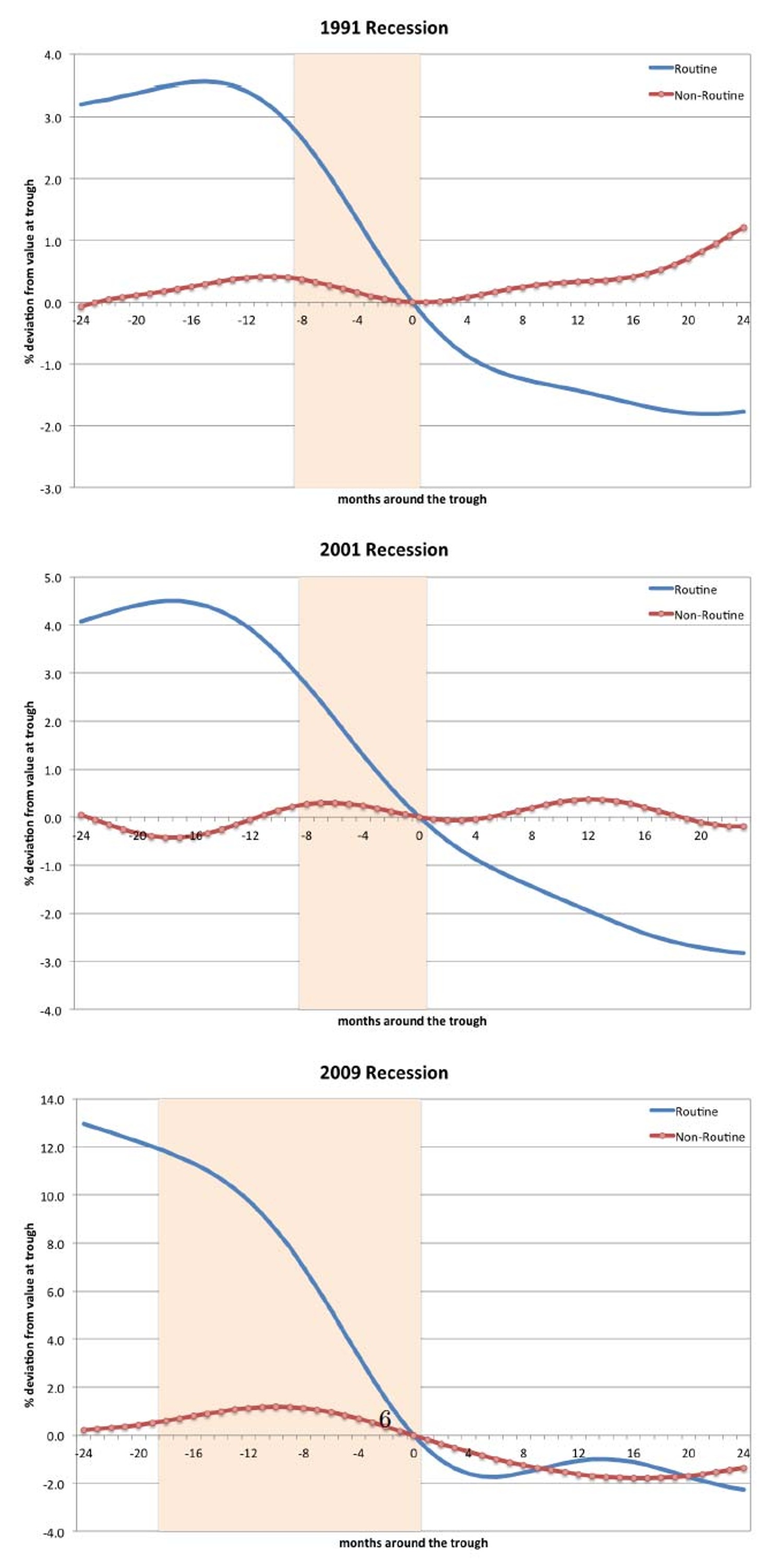

This contrasts sharply with the behavior of employment following the three most recent recessions of 1991, 2001, and 2009. Consider the 1991 episode. In the 12 months prior to month 0, employment falls by about 2%. After the recession, employment continues to decline for 17 months before beginning to rebound. The jobless recovery is even starker following the Great Recession. In the 24 months prior to the recession’s end, employment fell by 6%. It took 23 months from that point on for employment to turn around. Even to this day — more than 5 years on — employment has yet to return to its level at the end of the recession, much less to its level prior to the downturn.

Figure 1: Aggregate Employment around Early NBER Recessions

Figure 2: Aggregate Employment around Recent NBER Recessions

Data from the Bureau of Labor Statistics, Current Population Survey; See Jaimovich and Siu (2012).

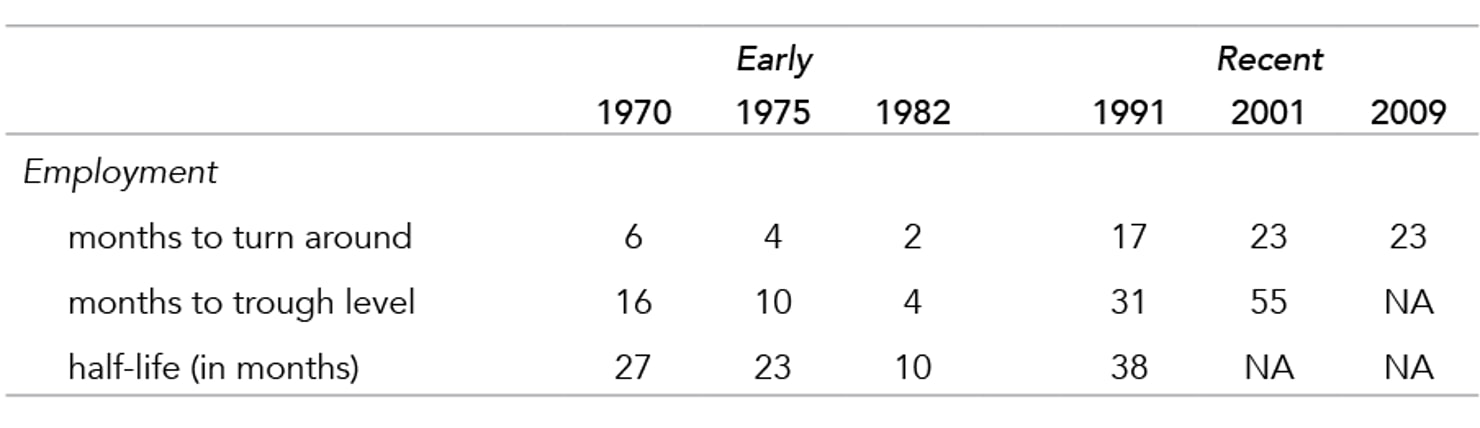

The changing nature of economic recoveries is summarized in Table 2. The first row lists the number of months it takes for employment to turn around (stop contracting and begin expanding) following each recession. The second row indicates the number of months it takes from the end of each recession (at month 0) for employment to return to its level at month 0. The third row lists a “half-life” measure: the number of months it takes from month 0 to regain half of the employment lost during the recession.

Table 2: Measures of Recovery Following Early and Recent Recessions

Data from the Bureau of Labor Statistics, Current Population Survey; See Jaimovich and Siu (2012).

The distinct break in the behavior of per capita employment representing the jobless recovery era is plainly evident. For instance, averaged over the three early episodes, employment turns around about four months after the recession; in the recent episodes, the average turnaround time is 21 months. And for the early episodes, it takes at most 27 months to recoup half of the employment lost in the recession. In the 1991 episode, it takes 38 months; employment never regained half of its loss following the 2001 recession, and has yet to do so after the Great Recession.

What is responsible for this dramatic change? Why are labor markets now struggling to recover in the wake of recessions?

A common misperception is that jobless recoveries represent a delayed recovery in hiring experienced “economy-wide.” This, however, is not the case. Instead, they can be traced to a lack of recovery in a subset of occupations in the economy: those that focus on routine tasks.

Job Polarization and the Loss of “Routine” Jobs

What are routine occupations? In the field of economics, these refer to jobs that involve a limited set of tasks. More importantly, those tasks tend to be “rule based,” in that they can be performed by following a well-defined set of instructions, and require minimal discretion.

For example, production occupations are a prime example of routine manual jobs: jobs that are both rule based and emphasize physical (as opposed to cerebral) tasks. As examples, factory workers who operate welding, fitting, and metal press machines fall into this category, as do forklift operators and home appliance repairers. Similarly, office and administrative support occupations are routine cognitive jobs that focus on rule based “brain” (as opposed to “brawn”) tasks. These include secretaries, bookkeeping and filing clerks, mail sorters, and bank tellers.

A growing literature demonstrates a profound implication of technological change on the labor market: many of the routine occupations that were once commonplace have begun to disappear, while others still have become obsolete.11 This is because the tasks involved in these occupations, by their nature, are prime candidates to be performed by new technologies.

The rapid and dramatic technological advances of the past 40 years have left an indelible mark on the modern workplace and the way that work is done. Robotics, automation, computing, information processing: these words and phrases have become part of our everyday lexicon as the processes behind them have transformed the nature of work. Technology has not only made us more productive; it has fundamentally changed the types of jobs we do, and the way that we do them.

A prominent example of this is in auto manufacturing. The genesis of modern American manufacturing is at the turn of the 20th century, when Henry Ford revolutionized the factory floor. With his implementation of the assembly line allowing workers to perform specialized tasks, Ford transformed a process once done by teams of skilled artisans (moving about the workspace, each working on a large set of tasks) into a simple and highly productive one. The efficiency of Ford’s production workers was revolutionary, and the diffusion of the assembly line throughout manufacturing ultimately led to rising factory wages, and facilitated the emergence of the storied American middle class.

Today, assembly lines and factory floors are no longer populated by human workers alone. In 1969, General Motors installed the first spot welding robot at its Lordstown, Ohio assembly plant, allowing more than 90 percent of body welding operations to be automated. In 1974, the very first microprocessor-controlled robots were introduced, allowing for increased speed and accuracy (crucial in auto manufacturing) over their hydraulic-controlled predecessors.12

The rest is history. The factory floor at American manufacturing plants are now populated by both humans and robots, with the latter doing most of the physical work. In effect, the industrial birthplace of the middle-class is now the central arena in which such job prospects are fast diminishing. The past 30 years have seen a decline of approximately 2 million workers in production occupations — representing a 20% fall — despite the fact that the working age population has increased by about 40%.

The other obvious realm of technological advance has been in computing and information processing. The mid-1970s saw the introduction of the personal computer, bringing many of the capabilities of the minicomputer and mainframe from research and academia into industrial settings. 1977 saw the introduction of the first commercially successful PCs: the Commodore PET and Apple II. The revolution gained steam in the mid-1980s when software improvements and the mouse made the PC user-friendly: think Apple’s Macintosh and Microsoft’s Windows operating system.

These technologies dramatically changed the way basic office functions are performed. Typing pools were replaced by desktop publishing and word processing. In tasks such as sorting, filing, retrieving, and calculating, the PC’s information management and processing capabilities drastically improved efficiency in secretarial and administrative jobs. Computing technology has replaced bank tellers with ATMs, travel agents with travel websites. In the past 20 years alone, the number of workers in office and administrative support occupations has fallen by 10%, in contrast to the 25% growth in the working age population.

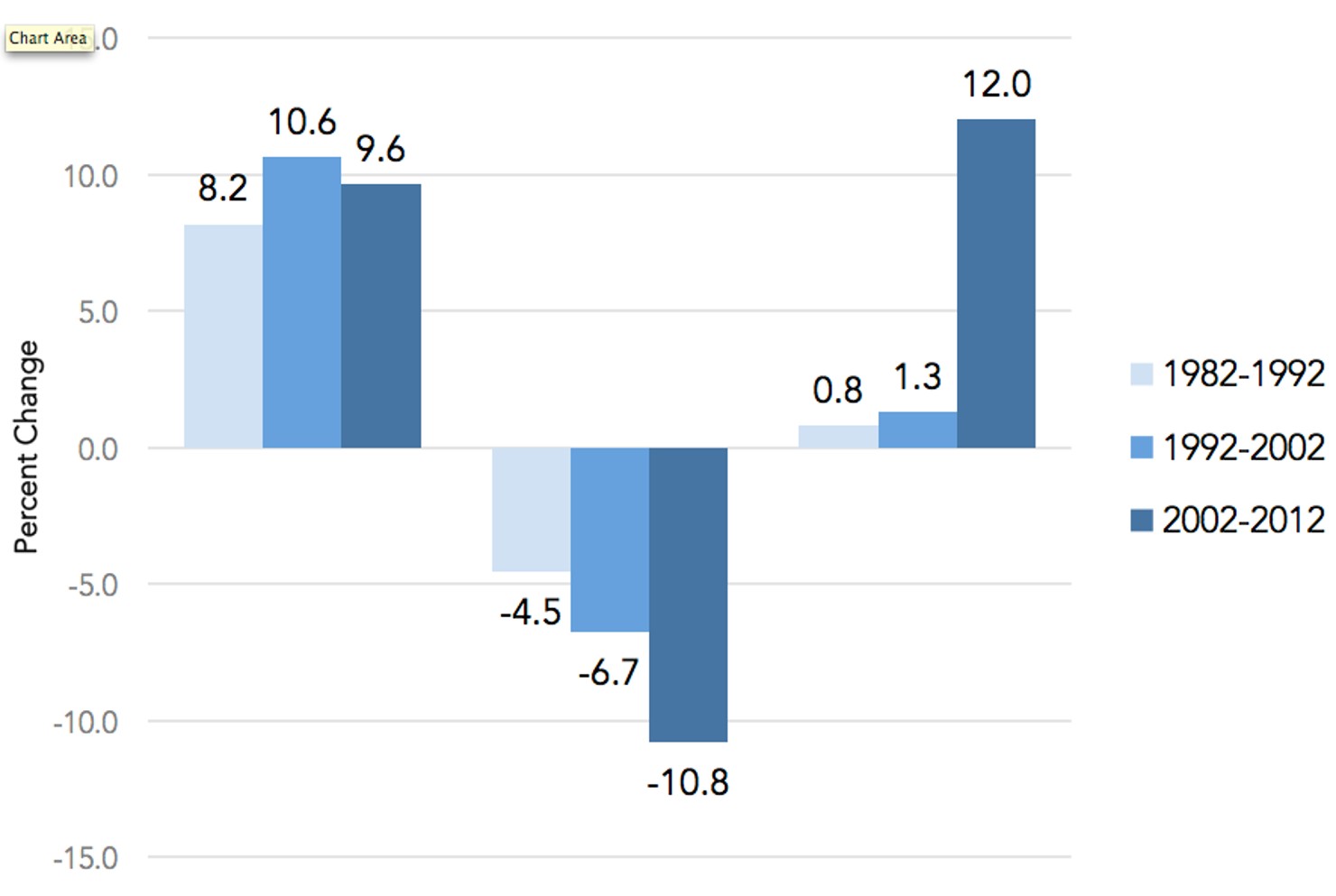

This large-scale shift in the types of jobs occupied in the economy is illustrated in Figure 3. In the figure, all U.S. occupations are divided into one of three groups. Routine occupations include both routine manual and routine cognitive jobs. The other two groups comprise occupations that focus on non-routine tasks: those that are not especially repetitive or rule-based. This means they might require flexibility (either cerebral or physical), and involve a variety of tasks. They also tend to emphasize greater degrees of human interaction, communication, or discretion. Non-routine cognitive occupations include jobs such as public relations manager, financial analyst, and computer programmer. Non-routine manual occupations include janitor, home health aide, and personal care aide.13

Each bar in Figure 3 represents the percent change in a group's share of total employment during the past three decades. Over time, the share of employment in routine occupations has been shrinking. As recently as the mid-1980s, about 1 in 3 Americans over the age of 16 was employed in a routine occupation; currently, that figure stands at 1 in 4.

Figure 3: Percent Change in Employment Shares by Occupation Group

Data from the Bureau of Labor Statistics, Current Population Survey; See Jaimovich and Siu (2012).

Moreover, these routine occupations tend to represent middle-class jobs. According to the BLS Occupational Outlook Handbook, full-time work in these occupations currently pays about $30,000-$40,000 per year. Qualification for such jobs typically requires a high school diploma, or potentially some additional specific technical or post-secondary training. These factors illustrate why the disappearance of employment in routine occupations has been associated with the shrinking middle-class. This is documented in the important body of research on job polarization.14 During the past 40 years, employment growth has been in the upper- and (more recently) in the lower-tails, or “poles,” of the wage distribution. This polarization of employment has also been accompanied by a polarization of wages, whereby real wages at the top and bottom of the distribution have been growing, while middle-skill wages have remained stagnant.15

The Role of Job Polarization in Jobless Recoveries

Interestingly, there is a tight connection between job polarization and the business cycle: the root of jobless recoveries can be traced to the disappearance of routine jobs. Prior to job polarization and advances in automation and computing, jobless recoveries did not occur.

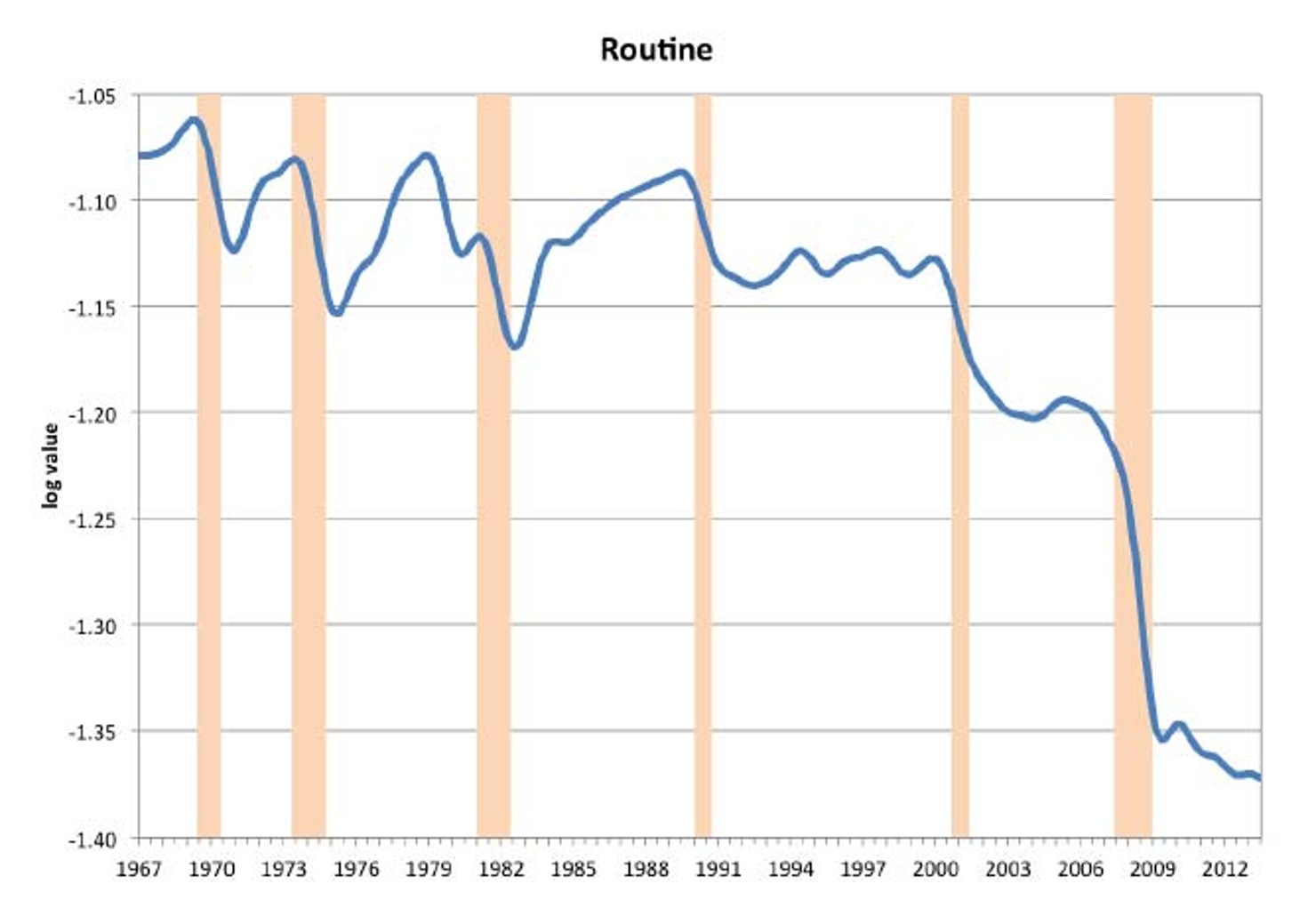

Figure 4 makes our basic point. It plots per capita employment in routine occupations, from 1967 onward.16 Since about 1990, there is an obvious decline in routine employment as it fell by approximately 29%. What is equally clear is that this fall has not happened gradually over time. The decline is concentrated in economic downturns: nearly 90% of the overall fall occurred within a 12-month window around recessions.

Following each of the 1991, 2001, and 2009 recessions, per capita employment in routine occupations fell and never recovered. This lack of recovery in routine employment accounts for the jobless recoveries experienced in the aggregate. Prior to job polarization, recessionary job losses in routine occupations were accompanied by strong routine job recoveries. This can be seen in Figure 4 following the recessions of 1970, 1975, and 1982. And prior to job polarization, jobless recoveries did not occur.

Figure 4: Employment in Routine Occupations: 1967–2013

Data from the Bureau of Labor Statistics, Current Population Survey; See Jaimovich and Siu (2012).

To make this point more evident, Figures 5 and 6 “zoom in” on employment around the three early and three recent recessions, respectively. These are analogous to the plots in Figures 1 and 2, except that total employment has been split into employment in routine and non-routine occupational groups.

In the 1970, 1975, and 1982 episodes, the recessions are clearly observed in routine occupations as employment plummets, as displayed in Figure 5. By contrast, non-routine employment was essentially unaffected by these recessions. Hence, virtually all of the job loss was accounted for by job loss in routine occupations.

More importantly, no jobless recoveries were observed in routine occupations following these recessions. Routine employment begins recovering shortly after the recession’s end, generating the recovery at the aggregate level, displayed in Figure 1. Hence, the business cycle behavior of employment prior to the job-polarization era is clearly driven by the behavior of routine employment.

It is also clear that the recession-and-recovery dynamics of aggregate employment in the recent episodes are driven by those of routine employment. Consider, for example, the 2001 recession displayed in Figure 2. Per capita employment economy-wide falls by about 2% from peak to trough, and falls a further 1.5% in the 24 months afterward. This pattern is not exhibited in non-routine occupations, as evidenced in Figure 6. During this time, non-routine employment is essentially flat. Jobless recoveries cannot be traced to the behavior of these occupations. Only routine employment exhibits the same pattern as in the aggregate, with a 4.5% fall leading up to the end of the recession, and a further 3% fall in the 24 months afterward.

In 2009, routine occupations are hit especially hard, falling about 12% from peak to trough, and a further 2.5% in the two years after. Per capita routine employment shows no recovery to date, down about 4% from the recession’s end to today. And, as is clear from Figures 4 and 6, routine occupations experience jobless recoveries following all recessions in the job polarization era.

Figure 5: Occupational Employment Around Early NBER Recessions

Figure 6: Occupational Employment Around Recent NBER Recessions

Data from the Bureau of Labor Statistics, Current Population Survey; See Jaimovich and Siu (2012).

As with the early recessions, these occupations account for the bulk of the contraction in aggregate employment. More importantly, routine occupations do not recover afterwards. In fact, employment in this occupational group never recovers: these occupations are disappearing. Hence, the jobless recovery phenomenon is due to the disappearance of routine jobs.

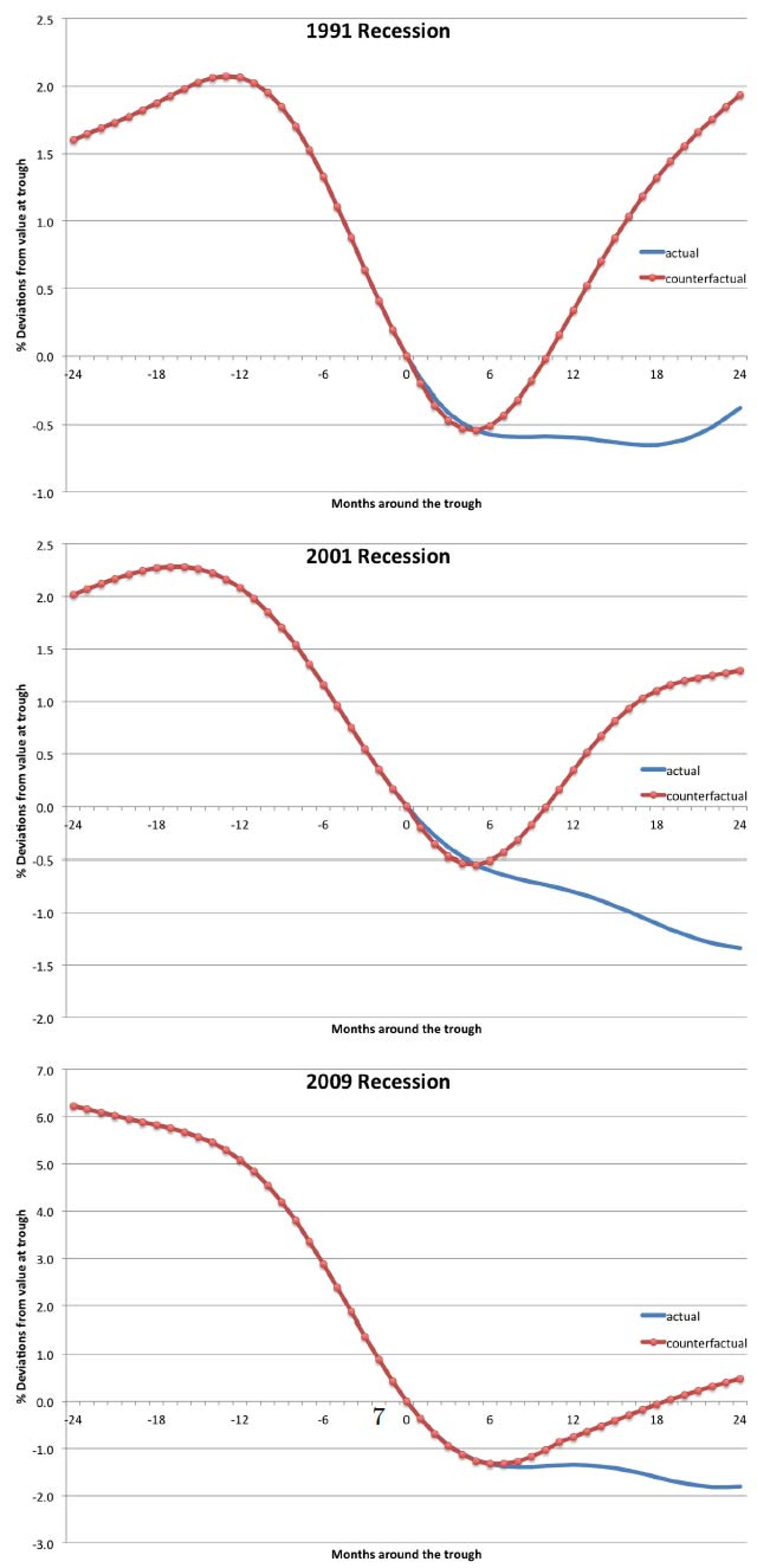

To more fully establish the link between job polarization and jobless recoveries, we consider a simple counterfactual, or “what if” exercise. We ask: What if we replace the behavior of routine employment following the recent recessions with its average behavior following the early recessions, before the advent of job polarization? What would the recoveries in aggregate employment have looked like? Would the U.S. economy still have experienced jobless recoveries if it weren’t for job polarization?17

The behavior of these counterfactual series around the recent recessions are displayed in Figure 7. The solid blue line indicates the time path of actual per capita employment. The hatched red line represents the counterfactual series. Had employment in routine occupations recovered as it did prior to job polarization, the U.S. economy would not have experienced jobless recoveries. Hence, jobless recoveries can be attributed to the lack of recovery in routine jobs.

Finally, it should be noted that job polarization and jobless recoveries are not confined to a small part of the economy, or experienced in only a limited number of industries. These phenomena are being experienced across many sectors, and by many types of individuals.

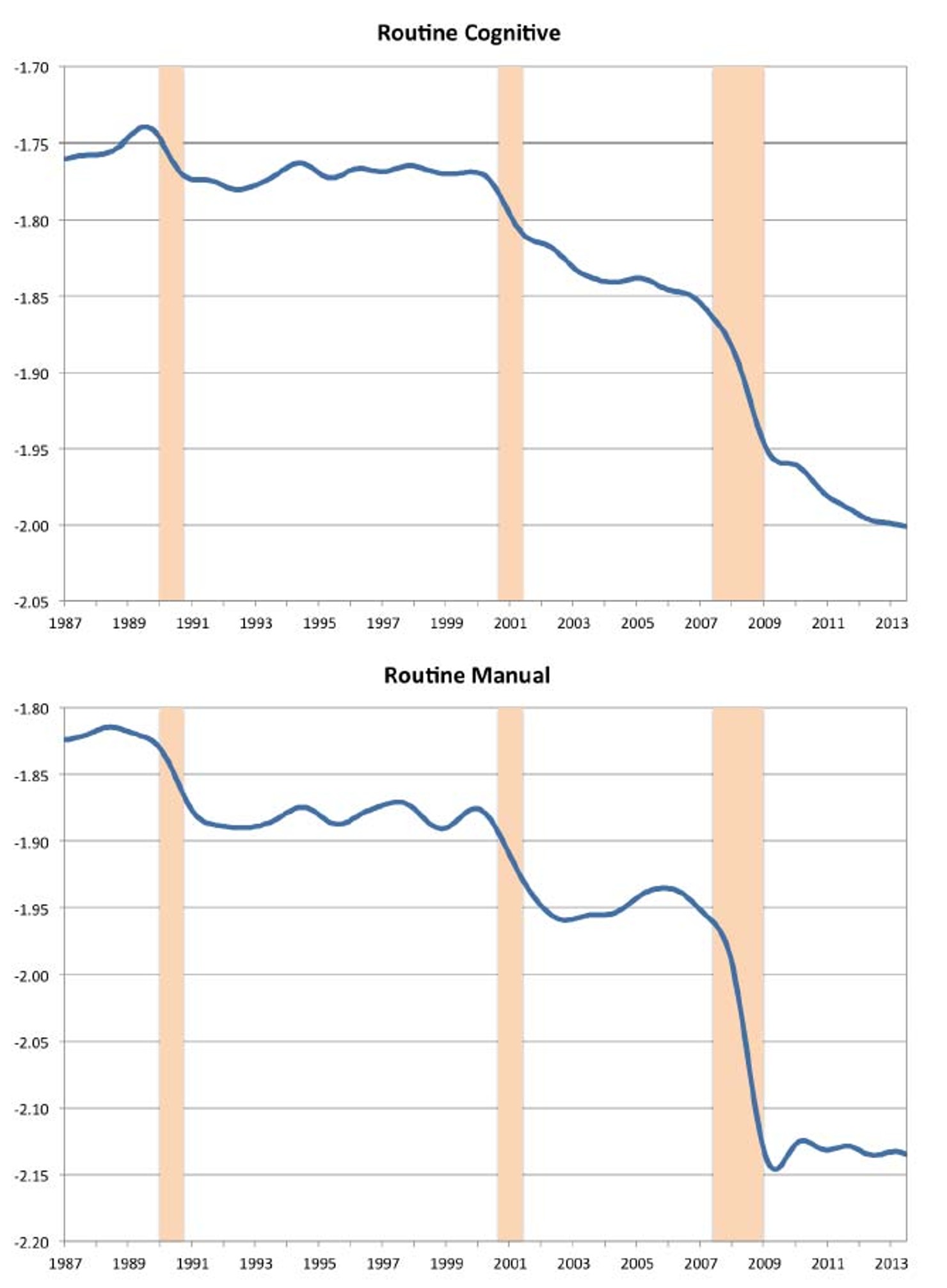

We illustrate this in Figure 8, where we plot per capita employment in routine manual and routine cognitive occupations separately. The descending staircase behavior of employment around the 1991, 2001, and 2009 recessions is obvious in both job categories. We view this as important for two reasons.

First, consider routine manual occupations. As discussed above, a prime example of this type of job includes production occupations “on the factory floor.” A popular misconception is that jobless recoveries are overwhelmingly about the decline of American manufacturing and other related “blue collar” work. But Figure 8 makes clear that this ongoing, sweeping away of jobs by successive recessions is also being felt in “white collar,” routine cognitive occupations. Given that the prime examples of these jobs are secretarial and administrative positions—and the fact that these jobs are found in all firms, throughout the economy—makes clear that jobless recoveries and the disappearance of routine jobs is widespread across many industries.

The final takeaway from Figure 8 is that these phenomena are affecting both male- and female-dominated professions. Approximately 84% of workers in routine manual occupations are men. About two thirds of routine cognitive jobs are held by women. Hence, the disappearance of these job opportunities following recessions is by no means confined to one gender or the other.

Figure 7: Actual and Counterfactual Employment Around Recent NBER Recessions

Figure 8: Employment in Routine Cognitive and Manual Occupations: 1987–2013

Data from the Bureau of Labor Statistics, Current Population Survey; See Jaimovich and Siu (2012).

Conclusions

One of the big puzzles of the U.S. economy is where the jobs have gone during the most recent economic recovery. How can it be that Real GDP and stock market valuations have recovered, and yet employment has remained flat, years since the end of the Great Recession? And how does this relate to the ongoing hollowing out of the American middle-class?

We show that over the past 40 years, structural change within the labor market has revealed itself during downturns and recoveries. The arrival of robotics, computing, and information technology has allowed for a large-scale automation of routine tasks. This has meant that the elimination of middle-wage jobs during recessions has not been accompanied by the return of such jobs afterward. This is true of both blue-collar jobs, like those in production occupations, and white-collar jobs in office and administrative support occupations. Thus, the disappearance of job opportunities in routine occupations is leading to jobless recoveries.

About the Authors

Henry Siu is an Associate Professor in the Vancouver School of Economics at the University of British Columbia, and a Faculty Research Fellow of the National Bureau of Economic Research. His research interests are at the intersection of macroeconomics and labor economics. His current work studies the impact of automation on labor market outcomes for the young and less educated, youth unemployment and its sensitivity to recessions, and the impact of the Great Depression on occupational and geographic mobility.

Henry received his B.A. in Economics from UBC and his Ph.D. in Economics from Northwestern University. He was the inaugural recipient of the Bank of Canada Governor’s Award in macroeconomic research. He has done stints as visiting scholar and consultant for the research departments of the Federal Reserve Banks of Chicago, Minneapolis, and St. Louis, the Bank of Canada, and the Reserve Bank of Australia.

Nir Jaimovich is a Professor of Economics at the Economics Department at Duke University, an associate editor of the Journal of the European Economic Association, the Review of Economics Dynamics, the Journal of Monetary Economics, and a Research Associate in the National Bureau of Economic Research (NBER) Economic Fluctuations and Growth program.