Report Published December 8, 2017 · 15 minute read

Family Caregivers Deserve a Tax Credit

Seventeen-year-old Maggie Ornstein was focused on prom, high school graduation, and college before her 49-year-old mother, Janet, suffered a debilitating brain aneurysm.1 Maggie immediately became her mother’s caregiver. As Janet spent the next five years in hospitals and long-term care facilities, Maggie handled medical bills, navigated social services, and coordinated her mother’s care. “It was two years before I took a day off from seeing her,” Maggie said. She also chose to attend college near home to continue her role caring for her mother and eventually her grandmother before she passed away. Today, Maggie balances being her mother’s primary caregiver with a demanding career as a college professor. “Caregiving is the most rewarding thing you can do in life,” Maggie says, “but it’s the hardest, too.”

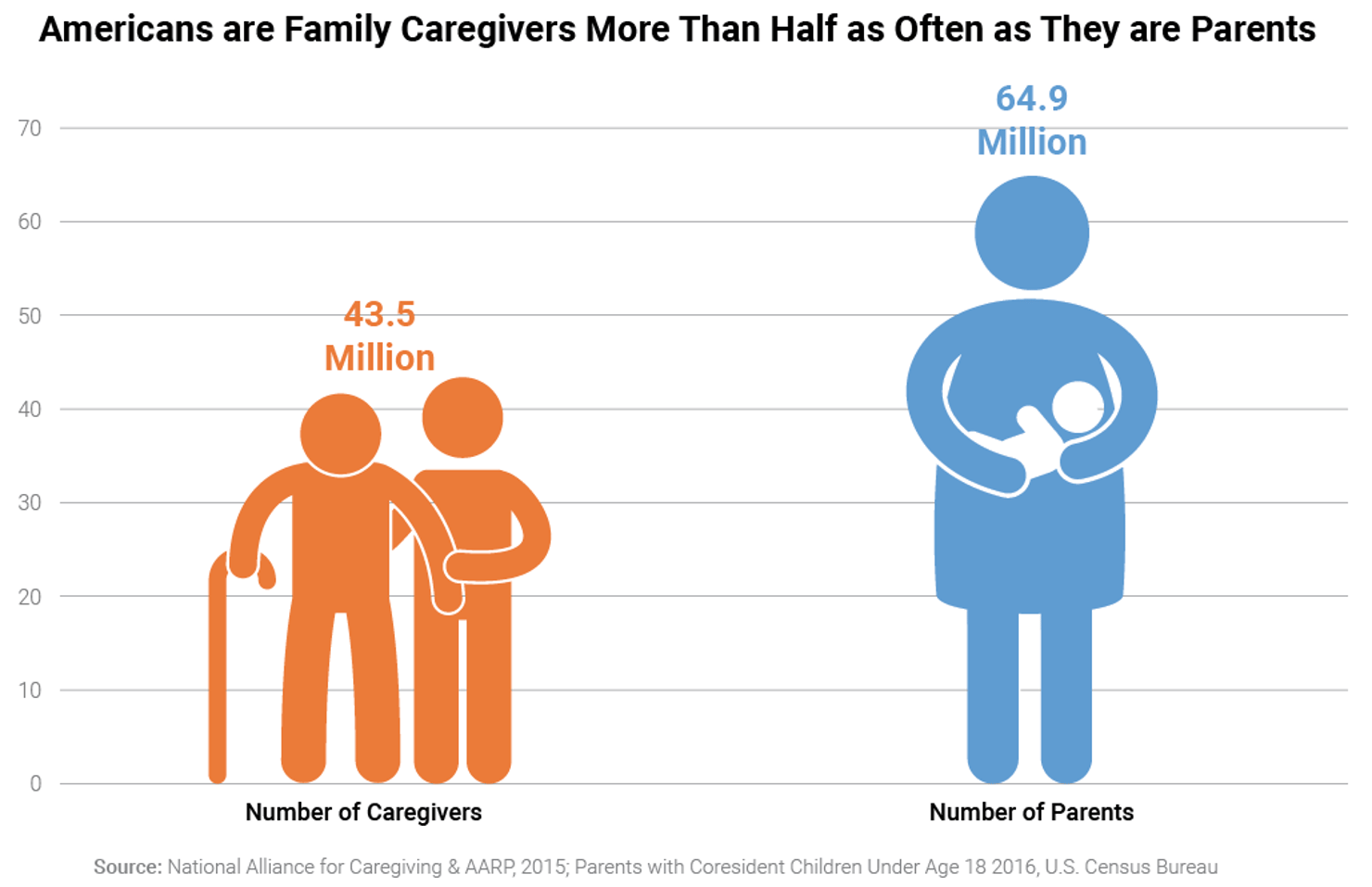

Maggie is one of 43.5 million family caregivers in the U.S. providing a wide range of unpaid assistance to an adult or child with a chronic, disabling, or serious health condition, including 3.7 million parents and other individuals caring for children with special needs.2 Caregiving may include assistance with activities of daily living (like bathing and dressing), tasks needed to live independently (like shopping and preparing meals), and complex medical/nursing tasks (like wound care and injections). The actual caregiver may be any relative, partner, friend, or neighbor who has a relationship with and provides care for someone needing assistance.3

Family caregiving has become a major and widespread responsibility for Americans, but government policy has not kept up with societal changes. The average annual expenses of a family caregiver of an adult (age 18+) are similar to the cost of parenting children. Family caregivers spent nearly 20% of their income on caregiving expenses on average in 2016.4 The income tax system generally recognizes the need to offset basic living expenses for individuals and for their dependents.5 Family caregivers, however, need and deserve similar treatment through a tax credit that helps offset caregiving expenses.

This report is divided into two sections. The first section describes the financial challenges facing family caregivers, and the second section details the proposed solution: a tax credit for family caregivers.

The Problem: Family Caregivers are Under Financial Stress

- Family caregiving in the U.S. has become a widespread and financially challenging responsibility.

- Caregiving is a basic cost of living like parenting, but caregiving costs are not supported by the tax code.

- Even with very good planning and coverage, family caregivers still face uncovered expenses.

- Long-term care insurance and Medicaid leave gaps and are inadequate to offset caregiving expenses.

1. Family caregiving in the U.S. has become a widespread and financially challenging responsibility.

In 2015, family caregivers provided 37 billion hours of care to adult care recipients, totaling about $470 billion in unpaid economic contributions.6 Indeed, family caregiving is comparable to parenting as a vital role in our society. Today, there are more than half as many family caregivers as there are parents in the United States. And those two roles often overlap. Twenty-eight percent of family caregivers have typical parenting duties plus family caregiving responsibilities while 2.7% of caregivers—6.5 million Americans—care for both an adult and a child with special needs.7

As important as family caregiving is already, its importance is increasing. The number of Americans who need personal assistance with at least one daily activity increased from 8.2 million (4.4% of the population) in 1989 to 12 million (5% of the population) in 2010.8 Of those individuals requiring assistance, the number and percentage with greater care needs is also increasing. The number of Americans ages 15 and older who need personal assistance with three or more daily activities while living with others or independently has increased from 4.6 million to 5.6 million, which is an increase from 2.2% to 2.3% of the population from 1997 to 2010 (no comparable data is available for before 1997 or after 2010).9

As a result of the greater intensity of loved ones’ needs, caregiving can be a full-time job like parenting. In 2015, 23% of family caregivers spent more than 40 hours providing care per week.10 In turn, family caregivers have to take time away from a job, which has big implications for a family’s financial situation.

The impact on family caregivers’ income is acute and unexpected.11 It hits them first with expenses they pay on behalf of loved ones. Seventy-eight percent of family caregivers use their own money to care for their loved ones, spending an average of $6,954 on caregiving costs in 2016.12

Next, they sometimes decide to leave a job or cut back hours unaware of the financial sacrifices they are making and the effect on their current or future financial security. A retirement survey has found that the percentage of retirees leaving the workforce earlier than anticipated to care for an ill spouse or family member ranged from 25% in 2008 to 14% in 2017.13 These caregivers experience intense financial losses as a result of this decision. For example, caregivers age 50+ who leave the labor force to care for a parent forego more than $300,000 in lost wages, social security benefits, and pensions. There are also significant gender differences in the financial sacrifice.14 Women lose, on average, more than $324,000, while men sacrifice under $284,000.

These demands on family caregivers will only increase in the future due to demographic changes. In 2010, the ratio of potential caregivers (individuals aged 46-64) to aging seniors (aged 80+) was about 7:1; that ratio is projected to be 4:1 by 2030 and 3:1 by 2050.15 The aging of the baby boomer generation will deliver a double whammy on family caregiving. First, between 2010 and 2030, baby boomers will be aging out of their peak caregiving years, leaving only a 1% increase in the population segment aged 45-64. Over the same time period, boomers will be aging into the period of greatest need for caregiving and will expand the 80+ aged population segment by 79%.16

The range of caregiving relationships is also changing. It is no longer the stereotypical daughters taking care of mothers. Grandparents provide care for great grandparents, millennials provide care for parents, and parents provide care for their children with special needs or adult children. While it is still true that most family caregivers provide care for their parents or grandparents (or in-laws), data suggest a steep increase in the percentage of caregivers providing care to their spouse or partner.17

Without an adequate supply of family caregivers who feel supported in their caregiving role, the U.S. will likely experience higher health care utilization and spending. When Americans get sick or have a chronic condition or a disability, they need appropriate care. Without a family caregiver, they may go without the home care services they need. This, in turn, can drive up the use of more costly health care services, such as emergency room visits or hospitalizations.18

2. Caregiving is a basic cost of living like parenting, but caregiving costs are not supported by the tax code.

The financial responsibilities of caregiving bear a lot of similarities to the financial responsibilities that comes with parenting.19 While the duration can be different (caregiving lasts four years on average compared to 18 or more years for parenting), caregivers spend comparable amounts each year on caregiving expenses as parents do raising their children as a percentage of income.20 According to a national survey of family caregivers for an adult (age 18+), they spent an average of 20% of their income on caregiving in 2016.21 By comparison, married couples in the middle third of the income range spent an average of 16% of their income on raising a child in 2015.22 It is important to note that costs vary widely by individual circumstances. For example, family caregivers in the lowest quarter of the income range spent an average of 44% of their income.23 Similarly, a single parent in the lower half of the income range spent an average of 39%.24

In addition, caregiving expense categories are comparable to parenting expenses. Approximately 60% of expenses for both parents and family caregivers are consumed by household expenses or housing, respite or child care, education, and travel or transportation.25

Caregivers and Parents Face Similar Types of Expenses

Family caregivers and parents both receive societal support to offset some of these expenses, including public insurance and other public programs, private insurance (and financial support to purchase it, for some), and support through the tax code.

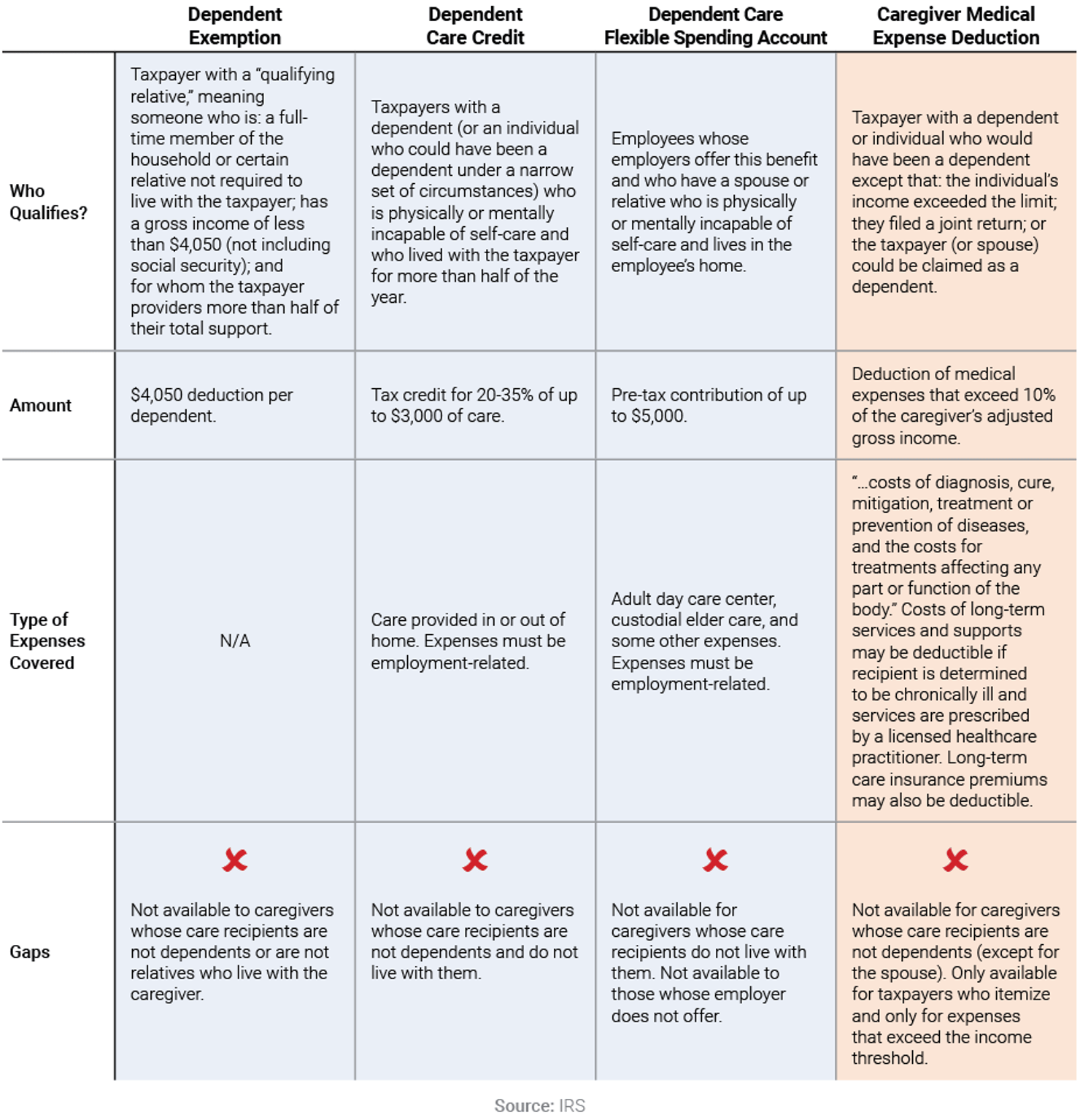

However, while support through the tax code is available for both family caregivers and parents, there are some significant gaps in the availability of these tax resources for caregivers. For example, the U.S. tax code provides support for the basic costs of parenting, offering tax credits for child dependents and for child care costs, an exemption for dependents, and tax-advantaged savings accounts for child care costs. The dependent exemption is helpful to some family caregivers who have a dependent in their household who needs caregiving, but far more parents can claim the exemption than caregivers can. As the following chart illustrates, current tax policy leaves substantial gaps in the treatment of family caregiving expenses.

Tax Code Leaves Gaps in Covered Family Caregiver Expenses

It is important to note that many of these tax benefits are also available to people receiving the care (called care recipients), assuming they have not yet become a dependent of their family caregiver. For example, care recipients may claim a personal exemption for themselves on their federal income tax return and receive a $4,050 income deduction.26 Care recipients may also deduct their own medical or long-term services and supports expenses if they exceed 10% of their adjusted gross income.27 Care recipients who are self-employed and purchase long-term care insurance through their business can deduct the entire premium as a business expense.28 And care recipients who have a disability with an onset age of under 26 may establish an ABLE account.29 ABLE accounts are tax-advantaged savings accounts funded with post-tax dollars but any income earned by the account is not taxed. The beneficiary, who is the account owner, and their family and friends may make contributions to the account.

3. Even with very good planning and coverage, family caregivers still face uncovered expenses.

Even under the best of circumstances—in which care recipients and their family caregivers have thoughtfully planned, saved, purchased long-term care insurance, and made other preparations—caregivers will likely still face uncovered expenses. As an example, consider an individual with private long-term care insurance living in Washington state, which was recently ranked number one on a national scorecard of state long-term services and supports.30 Despite good planning and a strong system of long-term services and supports, even family caregivers for this individual would face uncovered expenses.

At the beginning, the individual relies on their health insurance and personal income and assets before they qualify to use long-term care insurance benefits or during any waiting or elimination period. For example, the care recipient may need assistance with just one activity of daily living (ADL), but the long-term care insurance policy may require assistance with two ADLs before benefits are available, or the policy may require a waiting period following determination of benefit eligibility.

Once the care recipient becomes eligible for long-term care insurance benefits, the insurance pays for some long-term care expenses, while the individual and potentially the family caregiver use their personal income and assets to address expenses not covered by the policy. Very few long-term care insurance policies are comprehensive, so uncovered expenses might include costs above the daily benefit limit or specific services not covered by the policy.

Further, most long-term care insurance policies have a lifetime maximum benefit, so once those benefits are exhausted, the care recipient would likely begin spending their personal income and assets on medical and long-term services and supports expenses in order to qualify for Medicaid. During this spend-down period, the family caregiver may need to provide financial support for medical/long-term services, supports, and other costs, such as housing, food, or personal items.

Once the care recipient spends enough of their personal income and assets to qualify for Medicaid, they may rely on that coverage for some medical and long-term services and supports expenses. If the care recipient has any income over the Medicaid limit, it must be spent on medical care or long-term services and supports. At this point, the caregiver may pay for medical or long-term services and supports expenses not covered by Medicaid, as well as other expenses like housing, food, or personal items.

While careful planning and saving can ease the financial burden of a chronic, disabling, or serious health condition, few people have the wherewithal to do so. Even when they do, they can still face significant financial pressures under the current system for health care and long-term services and supports.

Caregiver Expenses Highest when Long-Term Care Coverage is Weakest

4. Long-term care insurance and Medicaid leave gaps and are inadequate to offset caregiving expenses.

Unfortunately, most Americans do not face the best-case scenario described above. For most, the sources of payment for long-term services and supports are often inadequate. The prevalence of private long-term care insurance has declined, retiree savings are not adequate, and Medicaid requires that beneficiaries spend down their assets to qualify—and Medicaid’s long-term services and supports benefit may not cover all the services an individual requires. All of these factors increase the financial demands on family caregivers.

Long-term care insurance policies are not widely used and coverage rates are falling. In 2014, just 11% of Americans aged 65 and older and 5% of Americans aged 55-60 owned long-term care insurance policies.31 These low coverage rates are likely driven by expensive premiums and lack of coverage standardization, forcing consumers to make complex policy design decisions with little information. This inevitably creates gaps as they attempt to balance coverage comprehensiveness with premium costs.

Without purchasing their own private long-term care insurance, Americans may next rely on their retirement savings to pay for long-term services and supports. Yet only 56.5% of Americans aged 60-64 are projected to have enough money for retirement and the cost of long-term care.32 Those at younger ages are similarly not saving enough for retirement. This lack of savings is an even bigger problem for people who develop disabilities at a younger age.

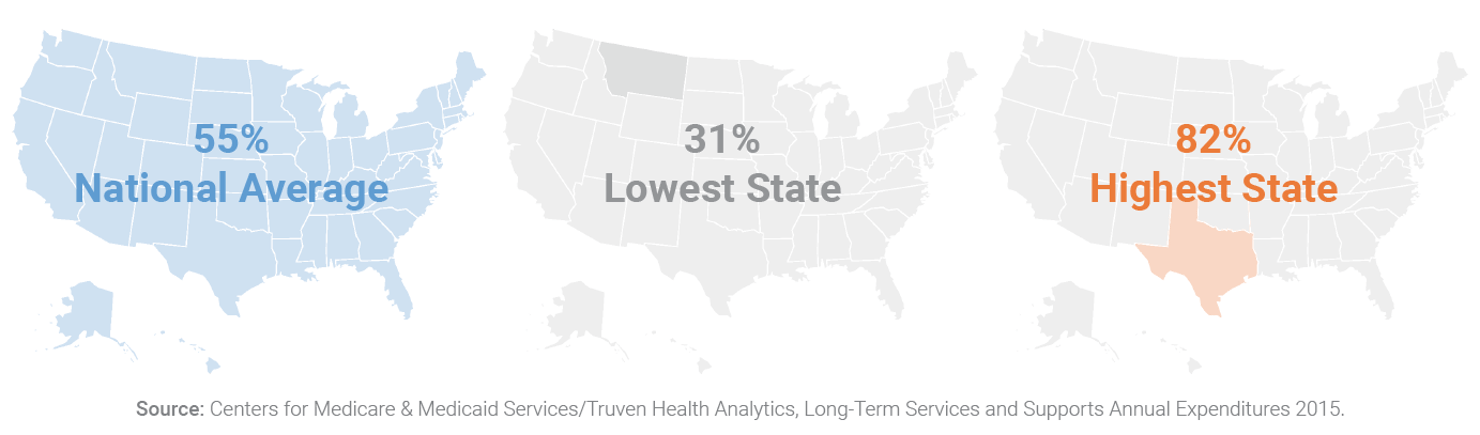

When long-term care insurance benefits and retirement savings are exhausted or nonexistent, most Americans rely on Medicaid to cover necessary nursing home care—and in some states, home- and community-based services. Individuals may become eligible for Medicaid when they have exhausted all other financial options. However, state Medicaid spending on home and community-based long-term services and supports is highly variable. In some states, Medicaid’s home- and community-based services coverage may be fairly comprehensive. In other states, there may be little available home- and community-based services and/or service offerings may be incompatible with beneficiary needs. Furthermore, in all states, beneficiaries must meet a specific financial and level of care needs to be eligible.

Medicaid Spending for Home and Community-Based Long-Term Services and Supports Varies Widely Among States

The Solution: A Tax Credit for Family Caregivers

We need to better align incentives to support family caregivers—and that starts with the tax code. A family caregiver tax credit as proposed by Senators Joni Ernst (D-IA) and Michael Bennet (D-CO) and Representatives Tom Reed (R-NY) and Linda Sanchez (D-CA) in the Credit for Caring Act (S. 1151, H.R. 2505) would provide targeted assistance for family caregivers who incur out-of-pocket expenses due to their caregiving.33

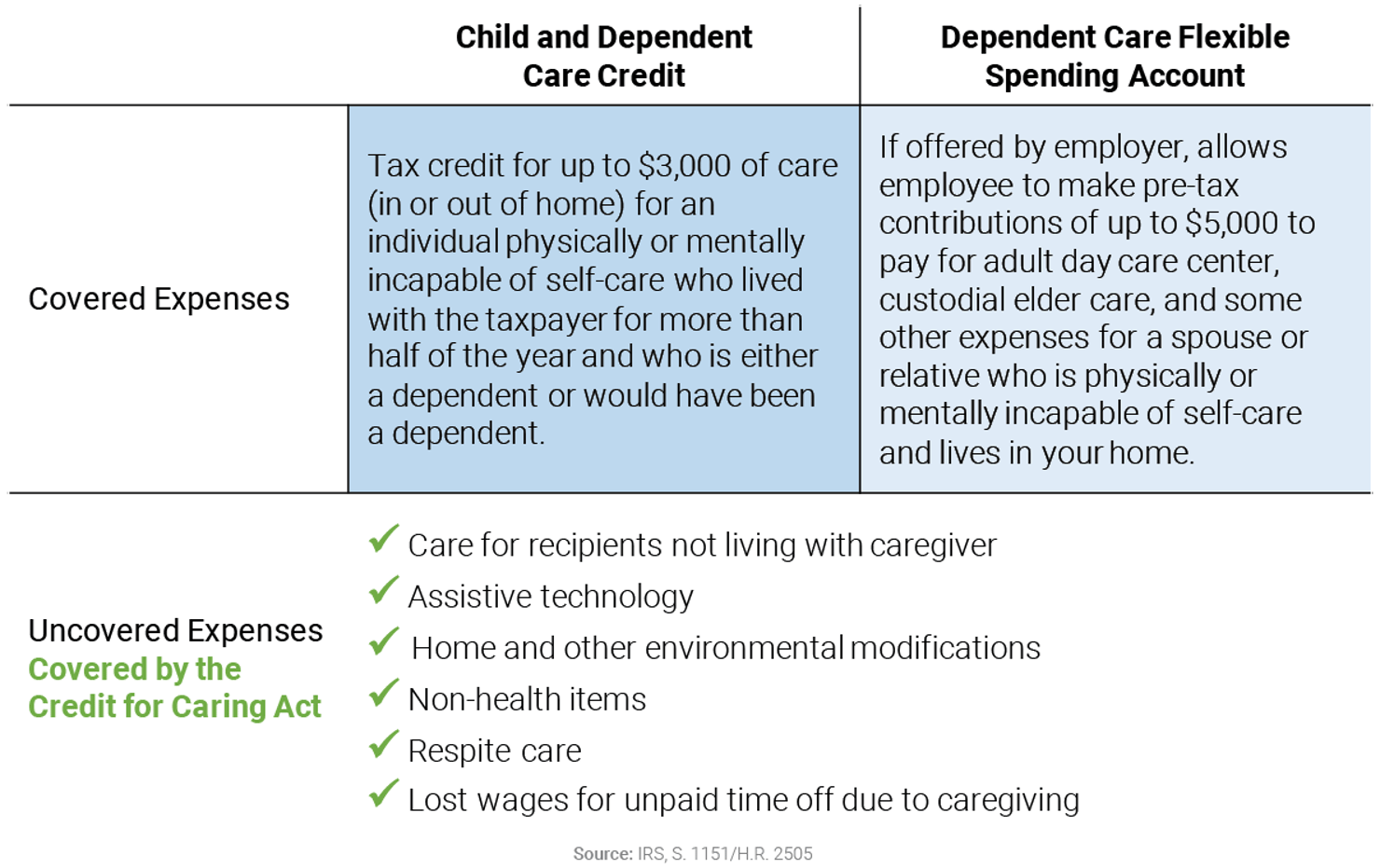

Specifically, the Credit for Caring Act would provide a nonrefundable tax credit for 30% of qualified caregiving expenses that exceed $2,000 up to a maximum credit of $3,000, depending on the caregiver’s income. Eligible family caregivers must have an income of at least $7,500 per year and must incur expenses for care provided to a spouse or other relative, including children, siblings, parents, stepparents, grandparents, and any in-law relatives who fall into one of those categories.34 The care recipient need not be a dependent and also need not live with the taxpayer.35 This more expansive definition covers more family caregivers than existing tax vehicles, which largely require the care recipient to be a dependent of the caregiver.

In addition, the Credit for Caring Act would provide a tax credit for a broad range of expenses incurred by family caregivers. These include direct care workers, assistive technologies and devices, home modifications, health maintenance tasks, transportation of the care recipient, non-health items, caregivers’ travel costs, and more.36 Some of these expenditures are uncovered by existing tax vehicles, meaning that the Credit for Caring Act fills in gaps in current tax policy.

Credit for Caring Act Helps Offset Caregiver Expenses

Financial support is only one of the solutions needed for supporting caregiving in the U.S. For a look at addressing additional needs, please see the companion Third Way report: “A Comprehensive Strategy to Support Family Caregivers.”37

Conclusion

Family caregivers play as broad and distinct of a societal role as parents. Many of them are even parenting children at the same time as they are caring for older family members. The expenses family caregivers incur related to the care they provide should count as basic living expenses just as expenses of parents do. They face wide gaps in the current tax treatment of family caregiving expenses because care recipients are often not dependents or relatives who live with the caregiver. Family caregivers deserve a tax credit for the critical role they play in our society.