Report Published April 15, 2020 · 22 minute read

A Broken “Promise”? How College Promise Programs Can Impact High-Achieving, Middle-Income Students

This report is based on research conducted with Maggie Fay and Negar Farakish in partnership with the Community College Research Center, Teachers College, Columbia University.

In the lead-up to the 2020 election, a wide range of progressive and moderate candidates have voiced support for “free college” or “college promise” programs, which guarantee that students who meet specified eligibility criteria can attend college either tuition- or debt-free. This isn’t a new idea: nearly 300 college promise programs already exist across the country.1 Many of these promise programs and proposals restrict their benefits to the community college sector, following the lead of President Obama’s “America’s College Promise” proposal, which aimed to create a $60 billion matching grant program to make the first two years of community college free.2

Community college promise programs have broad political appeal because they satisfy concerns related to both equity and cost: they target financial benefits at disadvantaged students and have program costs that are relatively low.3 To further incentivize associate degree completion and pursuit of a bachelor’s degree, some community college promise programs continue to provide aid for beneficiaries after they transfer to a four-year college.4 Research suggests that community college promise programs can indeed improve degree attainment and economic mobility for their target audience of low-income or academically-underprepared students—the type of students who are less likely to directly enter four-year college after high school.5 However, the impact of these programs on non-target students—in particular, academically well-prepared middle-income students—has not been fully considered.

While community college promise programs can increase access, they may also introduce unintended consequences if they lead students who were likely to attend four-year schools (“four-year-eligible students”) to instead downshift their enrollment into two-year schools. To understand the extent of such unintended consequences and their potential impacts on students’ economic mobility, this paper builds off previous research I conducted on the American Honors community college program by integrating new publicly-available data from Opportunity Insights, a research organization that uses big data to inform policy solutions aimed at increasing economic opportunity and upward mobility in the US.

First, I review prior work that suggests diverting four-year-eligible students into the community college pathway could dampen bachelor’s degree attainment. Next, I summarize the experiences and college outcomes of four-year-eligible students in our study who opted for the community college pathway instead. I then layer these results with Opportunity Insights data regarding the likely economic mobility consequences of these enrollment decisions for the students in our sample and build on these findings to lay out a series of related policy recommendations.

Four-Year-Eligible Students and the Community College Pathway

Community college promise programs are primarily designed to broaden college access for lower-income or academically-underprepared students. However, such programs may also appeal to middle-income students who are academically eligible to enter a four-year college but are concerned about financing all four years. Indeed, researchers have found that very small amounts of grant aid can attract academically prepared middle-income students to enroll in less-selective colleges than they would otherwise attend.6

Small amounts of grant aid can attract academically prepared middle-income students to enroll in less-selective colleges than they would otherwise attend.

For example, in 2009, Knox County, Tennessee, introduced “Knox Achieves,” a community college promise program worth under $1,000 per year for the average beneficiary. Overall, the program increased students’ likelihood of college enrollment by an impressive 24.2 percentage points, which was largely driven by a 29.6 percentage point increase in the likelihood of community college enrollment. However, the restriction of benefits to the two-year sector also had the unintended consequence of encouraging middle-income and higher-achieving students to lower their sights from four-year to two-year enrollment.7

Why should we worry about bachelor’s-aspiring middle-income students who want to save money by beginning at a community college? While the upfront economic savings of community college promise programs seem compelling, many bachelor’s-aspiring students who begin at a two-year college never ultimately move beyond it. In fact, about 80% of community college students intend to earn a bachelor’s degree eventually, but only 17% end up doing so.8 These low rates could be due in part to academic under-preparation or severe financial need among many community college entrants. However, even for a middle-income student who is well-qualified to attend a four-year college, taking the community college pathway reduces their chance of earning a bachelor’s degree by 20 to 40 percentage points.9

For a middle-income student who is well-qualified to attend a four-year college, taking the community college pathway reduces their chance of earning a bachelor’s degree by 20 to 40 percentage points.

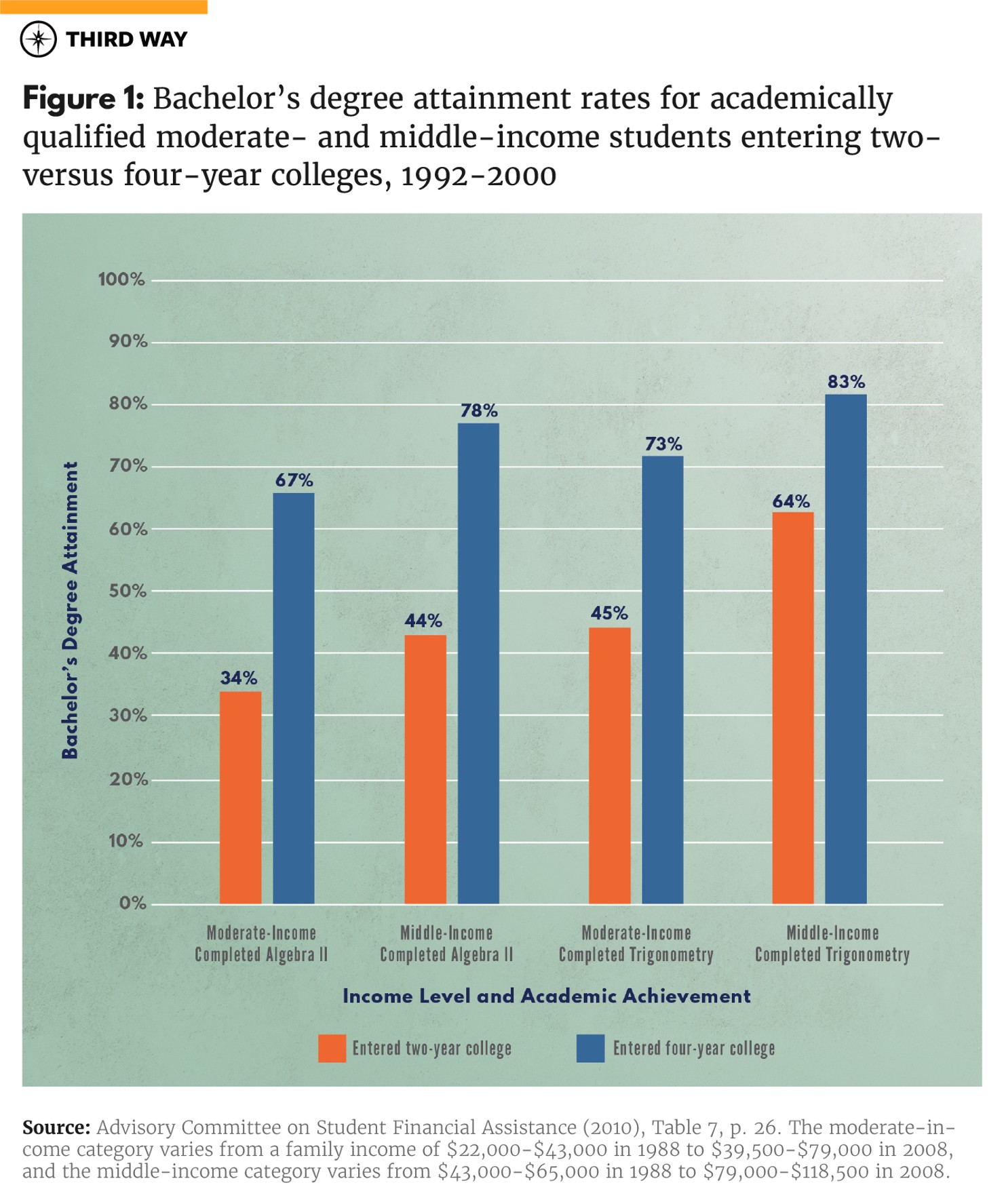

For example, Figure 1 shows national bachelor’s degree completion rates for four-year-eligible students with varying levels of family income and academic preparation (indicated by their attainment in high school math courses), and illustrates how those completion rates vary depending on students’ choice to initially enter a two-year college versus a four-year college. At the lower end of the spectrum, “Moderate-Income, Completed Algebra II,” students are typically just above the cutoff to receive a federal Pell Grant, and should be academically eligible to attend a range of less selective four-year colleges. Within this group, those who chose to enter a community college were 33 percentage points less likely to earn a bachelor’s degree within eight years, compared to those who chose to enter a four-year college (34% versus 67%). At the upper end of the spectrum, “Middle-Income, Completed Trigonometry,” students have completed higher-level math coursework and should have economic and academic access to more selective four-year colleges. Within this group, 83% of students earned a bachelor’s degree if they directly entered a four-year college, while only 64% earned a bachelor’s degree if they took the community college route to a four-year degree—a 19 percentage point difference.

Source: Advisory Committee on Student Financial Assistance (2010), Table 7, p. 26. The moderate-income category varies from a family income of $22,000-$43,000 in 1988 to $39,500-$79,000 in 2008, and the middle-income category varies from $43,000-$65,000 in 1988 to $79,000-$118,500 in 2008.

Overall, prior research suggests that promise programs that restrict benefits to the two-year sector could sway academically qualified middle-income students away from the four-year and into the two-year sector. But why would these students choose community college? In the next section, we draw on our larger study of the community college American Honors (AH) program to bring students’ voices and perspectives into the picture.10

Why Did American Honors Students Choose Community College?

We were initially drawn to study the American Honors program because it aimed to dramatically improve the likelihood of successful four-year transfer among bachelor’s-aspiring students on the community college pathway. If the program was indeed successful in doing so, then it could provide a scalable model for improving the affordability of four-year degrees, which could be cost-effectively reinforced and supported through community college promise programs across the country.

AH was launched in 2014 by the for-profit company Quad Learning and quickly spread to community colleges in several states. In return for paying a tuition premium that boosted their community college bill by about 50%, AH students benefited from an exceptionally high-quality and well-supported community college experience that still cost only about 40% of the price they would have paid at nearby four-year colleges.11 AH students enrolled in rigorous and engaging honors courses with small class sizes and received proactive and intensive advising, which included personal and logistical support with the process of researching, selecting, and applying to four-year college transfer destinations. AH advisors urged their students to “dream big” and reach for highly-selective colleges; indeed, the AH program hoped its community college students would ultimately graduate from much more selective destinations than their peers who directly enrolled in a four-year college. While the program was initially designed with high-achieving low-income students in mind, the students drawn to AH were predominantly middle-income due to the program’s academic admissions requirements and higher tuition.12

As part of our larger study, we interviewed 60 high-achieving, transfer-oriented students at six community colleges in four states who had graduated from a US-based high school before directly entering community college.13 About 70% were enrolled in AH, and the remainder were identified by college staff as similarly high-achieving students who intended to transfer.14

Interviewees expressed several key reasons for choosing to enter community college, including: (1) financial considerations, (2) the desire for a slower introduction to college life, including a personal preference to stay closer to home, and (3) the belief that community college offerings were equivalent to those of competing four-year colleges. The latter two reasons were often intertwined with financial considerations.

Almost half of interviewees said they were initially planning to enroll directly in a four-year college after high school, but then discovered their financial aid package was insufficient to cover the full cost of college. Two-thirds of interviewees lived in states with community college promise programs; of these forty students, nine spontaneously mentioned the state-sponsored community college scholarship as a factor in their decision to attend community college. One student recounted:

So when I was looking at colleges, I decided to apply to the various schools. I got into all my schools, and my mother said apply to [this community college] just in case, because I was offered a scholarship to the [state community college scholarship] program. . . And when it came down to financial aid, my parents, they have a higher income, but we have a lot of brothers and sisters, so I didn’t get a lot of financial aid, and the [state community college scholarship] program was free, and I was just like, “This is a better option for myself.” You know, my parents don’t have to worry about how they are going to pay for my school.

Although some students expressed that community college was the only financially feasible choice for them, most interviewees instead viewed it as the most financially responsible choice, pointing to the desirability of making “a better investment financially” or avoiding loan debt. Many students weren’t yet sure of their goals, and felt it was more financially responsible to explore and define them at an inexpensive community college. About one-third of interviewees articulated the need or desire to stay close to their home or family, primarily (although not exclusively) in order to save money on living costs. About a quarter of interviewees also believed it was financially responsible to attend community college because it offered an equivalent academic experience to the first year or two of a university. For example, one student noted: “I didn’t want to be like my brother and rack up $100,000 in debt and be able to do nothing with it. I don’t know it’s—what am I trying to say?—The class credits are pretty much the same, so might as well spend a little less getting those credits out of the way.”

As high school students, several interviewees had been unsure whether the community college would offer a sufficiently high-quality academic experience but were reassured by the idea that they could attend the college’s honors program. For example, one student recounted:

I didn’t want to feel like I was taking the easy way out. I got accepted into two other universities, so I knew that I could go to a university and be there. And there’s such a stigma about community colleges… And I was worried about that. It kind of, it didn’t halt me; it just kind of sat in my heart. Like, “am I giving up?”… But [the honors program], they made me feel better about it… They kind of took away that stigma.

On the other hand, another quarter of students chose to enroll in community college despite suspecting the experience would not be academically equivalent. As high school students, they heard messages such as: “It’s the thirteenth grade. Don’t go there. It’s too easy,” or, “Only the people who can’t get into any other colleges go there,” or even, “You’re smarter than that.” Primarily due to financial reasons, these students ended up enrolling at the community college anyway, and to their surprise, most reported being pleased with the academic experience. These students felt vindicated by their choice to attend a cheaper college, which they now believed supplied an equivalent or even superior experience. As one student said:

When I came here, it was a totally different thing from what I was thinking about. Professors here are really good, and really challenging. And I feel like I’m prepared for a four-year. I don’t feel any different. Even my friends from four-year universities ask me to tutor them in certain subjects sometimes. It’s not much of a difference; it’s just that I commute.

The Economic Implications of Choosing a High-Quality Community College Program Over Directly Entering a Four-Year College

Many of our interviewees believed they made “a good investment” or “the right choice” by choosing community college over a four-year college. Our larger study, which examined the college enrollment patterns of nearly 12,000 AH applicants, found that AH students indeed had substantially higher rates of persistence and transfer to four-year colleges in comparison to peers with similar economic and academic circumstances who entered the same community colleges outside the AH program.15 However, when compared to peers with similar economic and academic circumstances who directly entered four-year colleges, AH students had substantially lower rates of persistence and eventual four-year college enrollment. For example, three years after entering community college, only 66% of AH entrants were still enrolled at any college, compared to 80% of their peers who directly entered four-year college; in addition, only 54% of AH entrants were currently enrolled in a four-year college, compared to 73% of their direct-entry peers.16

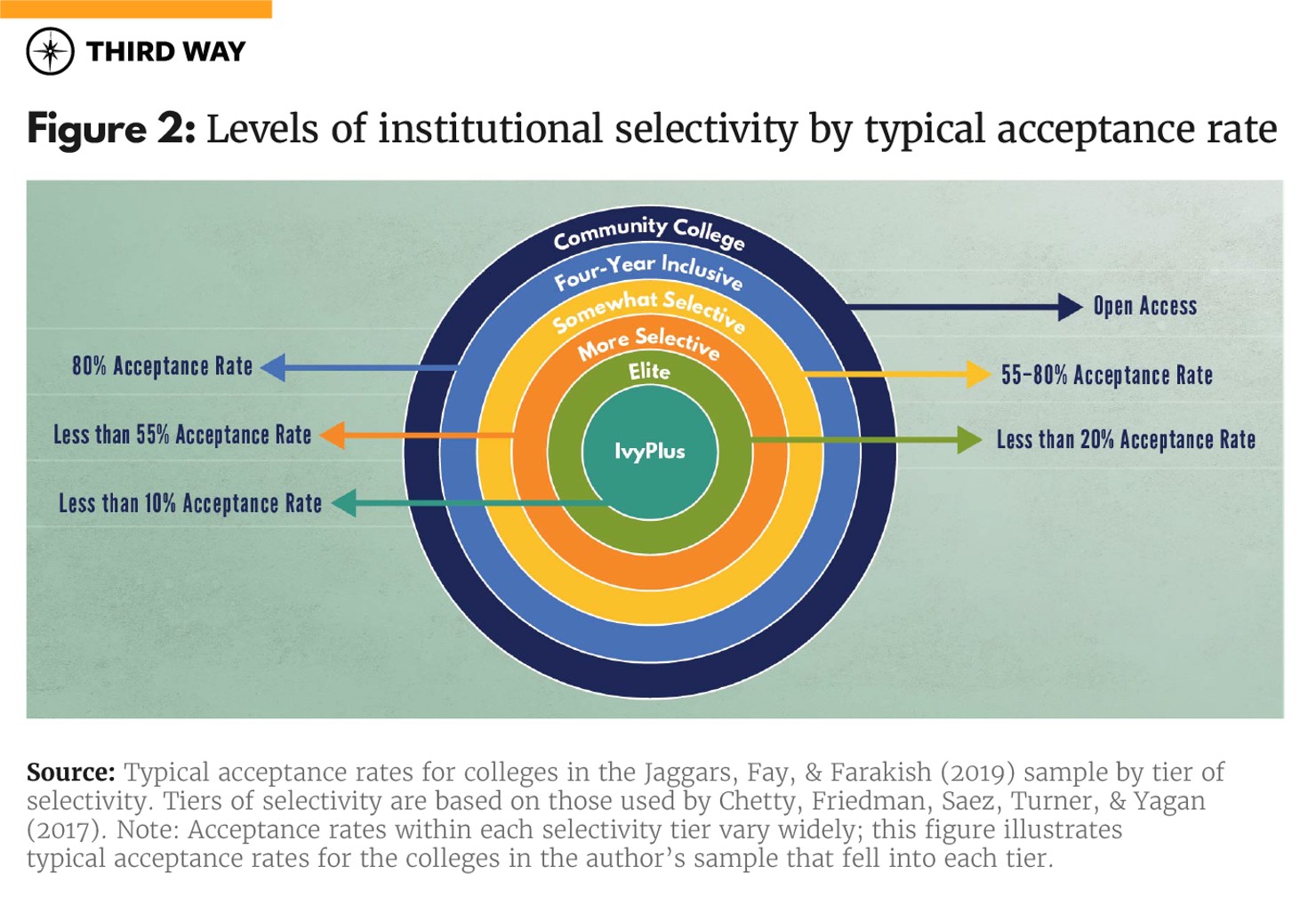

AH program designers also hoped their community college students would ultimately attend more-selective destinations than their direct-entry peers—an important goal, given that low- and middle-income students’ chances for economic stability and mobility are highly dependent on their college’s selectivity.17 Selective colleges confer more instructional resources per student and offer both a higher likelihood of graduation and superior positioning in the labor market for their graduates. These benefits increase with each rising level of selectivity, from Community College (open access), to Four-Year Inclusive (accepting 80% or more of applicants), to Somewhat Selective (admitting around 55%-80%), to More Selective (admitting 55% or less of applicants), to Elite (highly competitive colleges such as Amherst College, Georgetown, or UCLA, which typically have acceptance rates in the teens), and up to the most selective IvyPlus tier (the Ivy League plus Stanford, MIT, University of Chicago, and Duke, which typically have acceptance rates in the single digits). By providing intensive support for four-year college exploration and selection, AH staff hoped their students would stream into Elite or IvyPlus colleges. However, regardless of their pathway of entry, both AH transfers and their direct-entry peers ultimately gravitated to the same set of in-state, Somewhat Selective or More Selective four-year colleges, with only a small handful of each population attending an Elite or IvyPlus college.

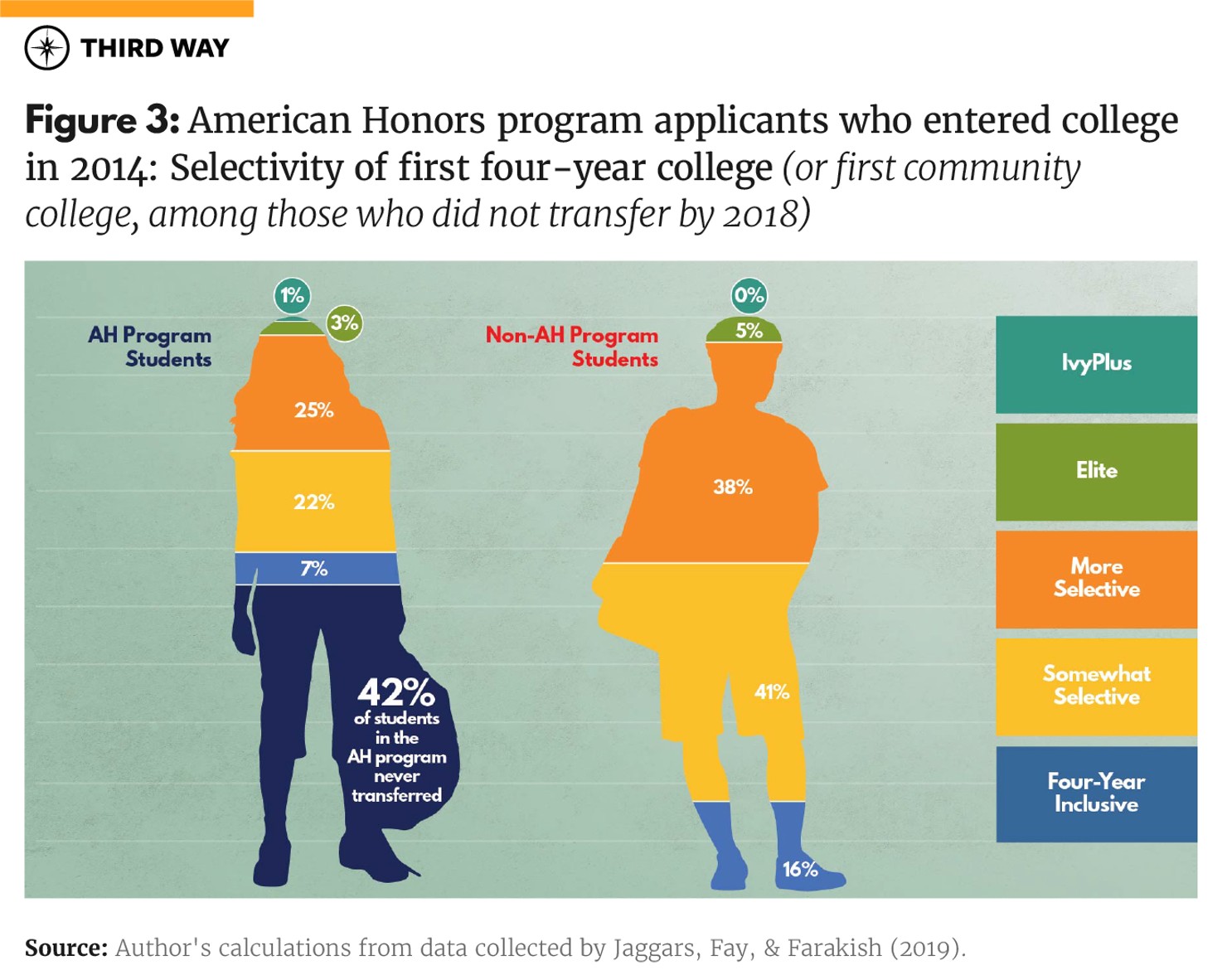

Yet while the distribution of four-year college selectivity was similar between AH entrants who ever transferred and their direct-entry peers, Figure 3 shows that because 42% of AH entrants never transferred to any four-year college, they had much lower rates of enrollment in selective colleges. For example, among AH applicants who entered college in 2014, 38% of those who directly entered a four-year college went to a More Selective institution, while only 25% of AH entrants eventually transferred to a More Selective college.

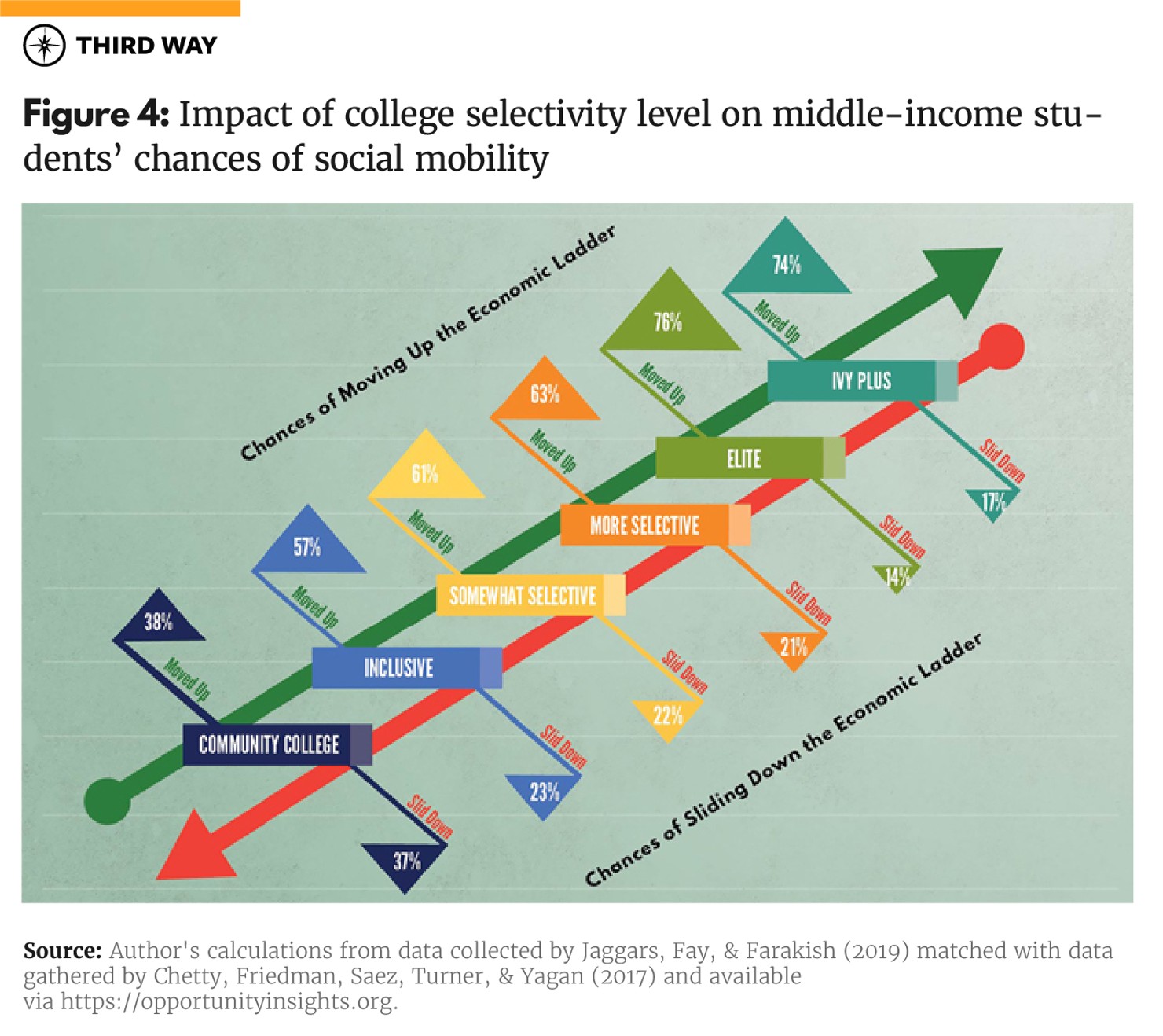

To get a sense of how rates of transfer to selective college could impact future economic outcomes for students in our sample, we match each student’s first four-year college with “College Mobility Report Card” data produced by Raj Chetty’s Opportunity Insights research team based at Harvard University.18 Chetty’s team worked with the Internal Revenue Service to track the long-term economic outcomes of almost every student in the nation born between 1980–1982, a cohort that typically entered college around 1998–2001. The Mobility Report Cards include college-specific data on the proportion of students from each income quintile who “moved up” or “slid down” the economic ladder—representing an increase or decrease in income level due to attending that school. Here we focus on each college’s middle-income population metrics, because this income bracket roughly corresponds with the students in our own study.19 For each college attended by a student in our sample, we examine its Mobility Report Card in terms of the proportion of students from middle-income families who eventually “moved up” to become upper-middle income or rich as adults, as well as the proportion who eventually “slid down” and became lower-middle income or poor as adults.

For students in our sample who never attended a four-year college, their prospects of economic mobility were mediocre: their community colleges’ Mobility Report Cards indicated that entering middle-income students have a 38% chance of moving up the economic ladder, but a nearly equal chance (37%) of sliding down it.20 Transferring to an Inclusive four-year college improved their outlook: for the Inclusive colleges attended by students in our sample, middle-income students have a 57% chance of moving up the ladder and a 23% chance of sliding down. Figure 4 shows that the odds of economic mobility continue to improve for our students as they move up the ranks of college selectivity, with students in our sample who attended Elite colleges being over five times more likely to experience upward mobility than to face economic decline.

Aggregating across colleges with different selectivity levels, direct four-year entrants in our 2014 cohort attended colleges with moderately good Mobility Report Cards: middle-income students entering these colleges have a 62% chance of moving up the economic ladder and a 22% chance of sliding down. For AH enrollees, due to the large proportion who never moved past community college, their colleges’ Mobility Report Cards were substantially weaker: middle-income students entering those colleges have a 50% chance of moving up, and a 27% chance of sliding down the economic ladder.

Policy Implications

Students in our study fell into the demographic that feels most “squeezed” in regards to college: those whose families make too much money to qualify for federal need-based Pell Grants, but who cannot afford to pay for college without taking out substantial loans.21 On average, taking out a loan to attend a public or non-profit four-year college represents an excellent investment which will pay off handsomely over time.22 Yet middle-income students in our study were highly loan-averse—or, as they framed it, “financially responsible.” By declining to take on the loans required to immediately enter a four-year college, AH students believed they were making the “smarter choice” compared to peers who directly entered four-year college. Their instincts weren’t entirely off base: indeed, AH students who successfully transferred to a four-year college will likely reap the same economic benefits as their direct-entry peers, while dealing with substantially less loan debt.23 But unfortunately, many AH students never transferred, which substantially diminished their likelihood of moving up the economic ladder—and even worse, increased their likelihood of sliding down it.

Our results suggest several implications for policymakers, specifically when it comes to providing education on the long-term economic ramifications of college choice, honing rhetoric around college loans, promoting investment in community colleges, and designing the terms of “college promise” and other college financing policies.

First, in order to help potential college students understand the costs and benefits of different colleges and associated financing options, all high school students need more in-depth education on college selection and financing. While the literature persuasively shows that low-income students are deeply ill-informed about their options, our study indicates that some well-qualified middle-income students (including those with college-educated parents) are just as confused.24 As high schoolers, students in our sample were unaware of the economic benefits of college selectivity, and none followed the economists’ recommended approach of applying to a range of “safety,” “match,” and “reach” schools, and then entering the most-selective option that would admit them.25 To help all students better understand the range of college choices available to them, states should consider integrating education on college choice and financial aid into high school curricula. Many states have already instituted high school “transition curricula,” which focus on helping underprepared high school students improve their math or English skills in order to enter college.26 Transition curricula could be expanded to include information on college choice and financing, with an emphasis on “responsible borrowing.” For example, as a math exercise, students could examine information on a variety of in-state institutions in terms of their graduation rates, typical post-graduation loan balances and monthly payments, and typical post-graduation salaries, and calculate the best long-term “return on investment.”

Second, politicians need to be cautious in their rhetoric around the “student debt crisis.” In particular, centering a higher education policy platform on student loan forgiveness suggests that loan debt is the most terrifying and insoluble problem facing the middle class—and middle-income students in our sample took such messages to heart. Yet the reality for most student loan borrowers is quite different: the largest-balance borrowers are highly able and likely to pay off their balances. The borrowers most likely to be in trouble, on the other hand, are those with small balances who didn’t complete college, and those who attended expensive for-profit colleges with subpar economic returns.27 While student loans and college financing certainly need policymakers’ attention, it is counterproductive to frighten well-qualified students away from what would likely represent manageable loan debt incurred through direct entry into a four-year college, and toward a riskier community college transfer pathway that lowers their chances of ultimately receiving a bachelor’s degree. Rather than emphasizing a “debt crisis,” politicians can emphasize a commitment to “college affordability” and talk about the many policy tactics which can promote it. For the field of 2020 presidential candidates, strengthening and simplifying current federal affordability programs (including the Pell Grant, loan repayment structures, and the Public Service Loan Forgiveness program) should be a central plank in their platforms.28 In addition, the federal government might consider instituting a partnership with states, in which the government offers block grants based on states’ per-student spending on higher education.29

Third, in terms of investment in community college, our larger study found that the AH program cost an additional $2,200 per student per year, and resulted in transfer outcomes that were substantially stronger than that of similar students entering community college through a more traditional route.30 Those findings suggest that investments in community college designed to create an experience similar to that of AH—in which students were involved in pedagogically-engaging and rigorous coursework, had highly supportive advisors, and enjoyed extensive assistance with the four-year transfer college search and application process—could pay off by increasing students’ rates of persistence, transfer, and eventual economic outlook. Yet institutional-specific investments may go only so far: despite their exceptional community college experience, AH enrollees’ economic outlooks were substantially weaker than those of similar students who directly entered four-year college—because 42% of them never ended up transferring to a four-year college. To repair the transfer system more broadly, states can play a key role by creating statewide infrastructures, policies, and incentives for the state’s four-year and two-year colleges to work together in developing robust transfer pathways.31 For example, Ohio requires public four-year colleges to accept community college students who have earned at least 60 credits with a 2.0 GPA and has created a common course numbering system and a common set of learning objectives for a large set of introductory college-level courses, which guarantees the courses will seamlessly transfer across all the state’s public colleges.32

Finally, in terms of designing college promise programs and other college financing policies, policymakers should avoid incentivizing the community college pathway for four-year-eligible students. For example, rather than branding a policy as “free community college” or a “community college promise,” policymakers could guarantee a smaller “first-dollar” scholarship (which means that the scholarship money is applied to tuition costs before other eligible state and federal grants) to any student under an established middle-income threshold who attends any two-year or four-year college. First-dollar scholarships are useful for three reasons. First, they provide the strongest benefits to low-income students: for those who receive Pell Grants and attend community college, the combined scholarship and Pell Grant help offset lost wages due to college attendance, which helps students to stay in college and graduate on time.33 Second, because the dollar amount of a first-dollar scholarship remains the same across a variety of family incomes and college choices, it simplifies budgeting for both policymakers and individual families. And third, students are highly responsive to the notion of a “scholarship,” a term which sways their college decision-making with a strength disproportionate to its actual economic value.34 Keeping that fact in mind, policymakers can avoid incentivizing community college for four-year-eligible students by making the scholarship value higher for those who attend four-year college. For example, students might be guaranteed $1,500 per year if they attend community college, or $3,000 per year if they attend a four-year college.35

Conclusion

Today’s middle-income students are highly loan-averse, which makes them particularly susceptible to community college promise programs that incentivize them to downgrade their college aspirations to the two-year sector—which in turn reduces their chances of earning a bachelor’s degree and increases their chances of sliding down the economic ladder. To counter this trend, in this brief we recommend that policymakers:

- Integrate education on college choice and financing into states’ high school curricula;

- Tone down the rhetoric around the “student debt crisis,” and instead focus on improving “college affordability”;

- Provide incentives and supports for two- and four-year colleges to work together to create a more seamless transfer pathway; and

- Provide modest, portable first-dollar scholarships to low- and middle-income students and make these scholarships higher in value for students who attend four-year college to offset incentivization of the community college pathway for four-year-eligible students.