Memo Published April 18, 2023 · 19 minute read

Geothermal: Policies to Help America Lead

Robert Fourqurean & Sagatom Saha

Takeaways

- The US should not miss out on the opportunity to build a globally competitive geothermal industry. Today, the US has a lead in the technology space, representing 25% of the market with the ability to capitalize on its early advantage. However, other countries are prioritizing geothermal and could overtake US investments.

- The geothermal market opportunity is significant: The global market addressable by US firms is conservatively estimated to be $1.5 trillion through mid-century creating 100,000 jobs. The actual size of the market could be much larger if critical innovations, such as enhanced geothermal systems (EGS), deep drilling, and well materials innovations, take off.

- The Inflation Reduction Act provides substantial incentives for geothermal domestically but more can be done, from de-risking financing for early-stage projects to enhancing market signals to accelerate deployment of technologies that are already at commercial scale. Additionally, directing US commercial diplomacy towards emerging geothermal technologies can translate domestic build-out into a globally competitive industry, with the most promising initial markets in Southeast Asia, Sub Saharan Africa, and Latin America.

Why the US Should Compete in the Geothermal Market

Geothermal power, with the passage of the Bipartisan Infrastructure Law (BIL) and Inflation Reduction Act (IRA), is at a turning point. Previous legislation primarily directed federal benefits at wind and solar. While wind and solar will be the backbone technologies that drive power-sector decarbonization throughout most of the world, geothermal can nonetheless provide essential value by supplying firm, dispatchable electricity to complement and drive increasing penetration of variable wind and solar. Furthermore, in addition to its grid balancing benefits, geothermal can generate low to medium temperature industrial heat to help decarbonize hard-to-abate industrial sectors and produce lithium as a by-product. Lithium is a critical input for battery storage and electric vehicle batteries, and its availability and affordability will be critical determinants of the speed of the energy transition.

The BIL and IRA respectively provide $84 million for enhanced geothermal systems (EGS) demonstration projects and extend popular, critical tax credits to geothermal deployment. These incentives will accelerate the commercialization of geothermal systems in the US, creating economic growth and well-paying jobs. But more can be done to supercharge these investments and promote technology diffusion–that is, internationalize the US down payment in geothermal across the globe to create even more jobs at home and help other countries decarbonize with the firm, dispatchable power that geothermal provides.

On March 21, 2023, Third Way and Boston Consulting Group released the second phase of a groundbreaking report examining the value chains, segment by segment, of an additional four clean technologies, including geothermal, to identify where the US can build and maintain durable competitive advantages in the global markets through strong exports. The study focused mainly on geothermal power as well as some industrial and district heating applications and found that US firms are well positioned to capture the growing geothermal market opportunity. The US’s early advantage stems from several factors, which include an early lead in intellectual property (IP) and a strong oil and gas (O&G) workforce that can be re-skilled.

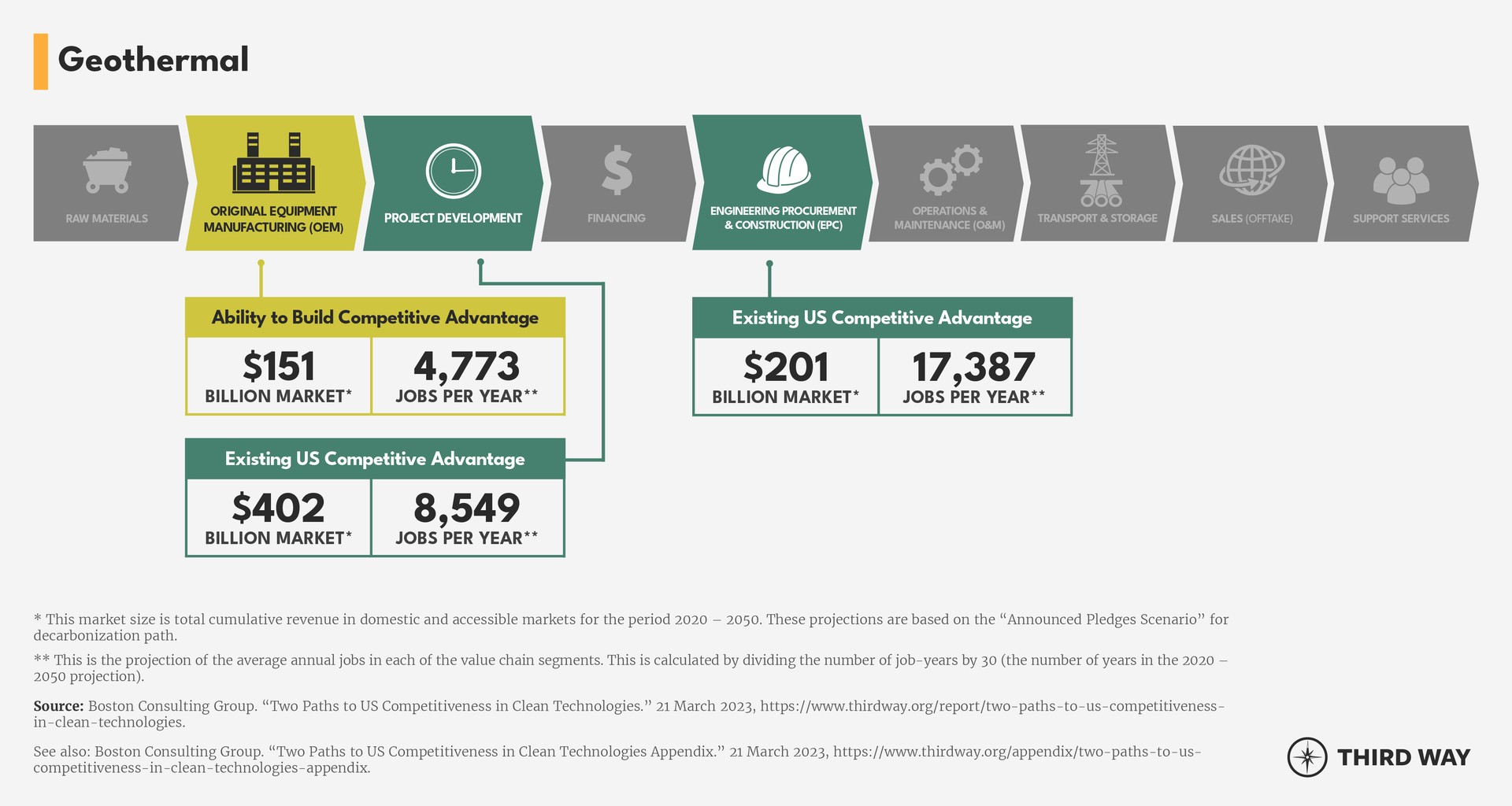

BCG found that the US has a particular competitive advantage in project development and engineering, procurement, and construction (EPC); with potential to break into the original equipment manufacturing (OEM) industry. All three of these value chain segments represent rich markets totaling in the hundreds of billions of dollars and thousands of US jobs. These segments are highly exportable given their reliance on extremely complex processes that few countries and firms can match the US in.

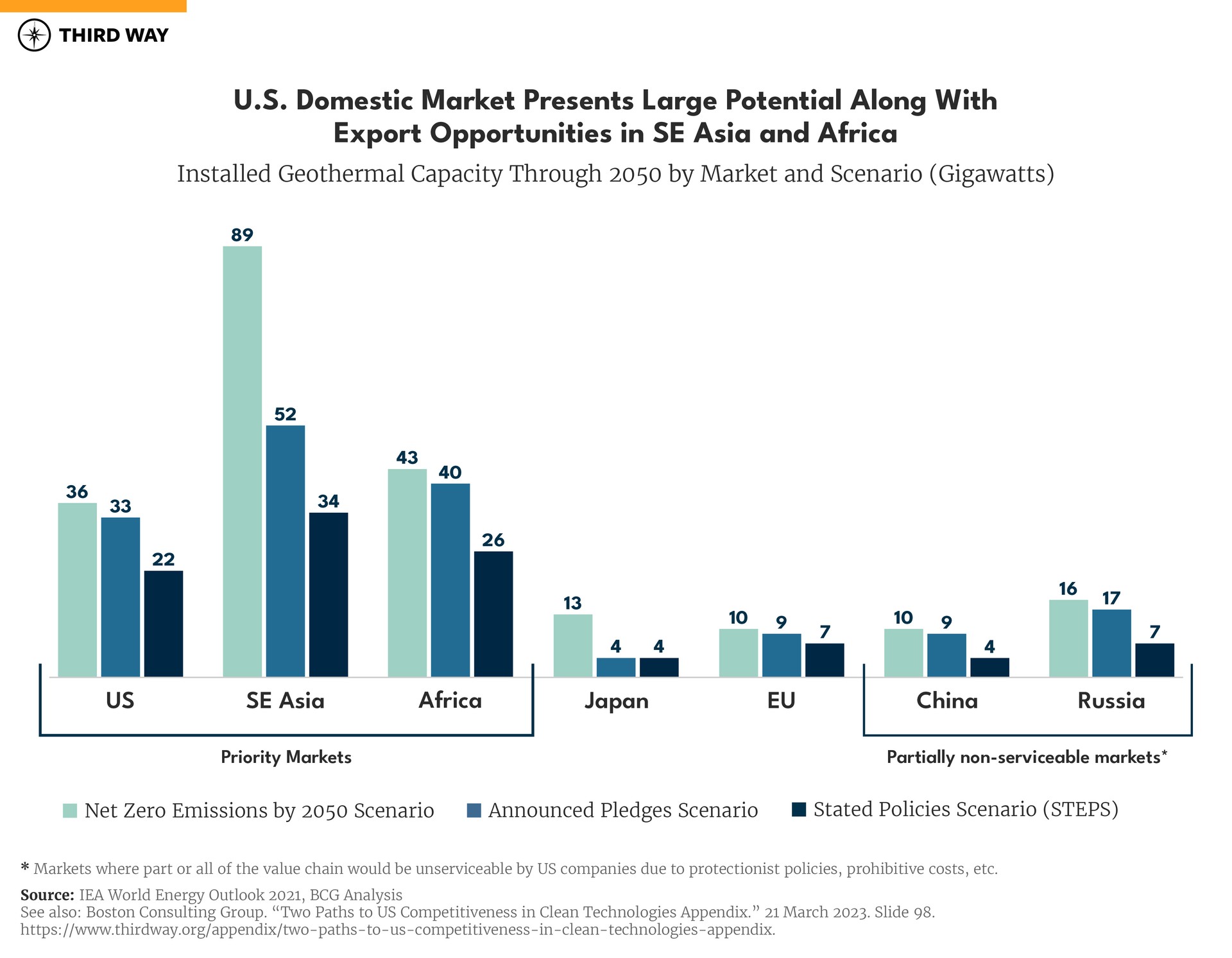

Still, the US lead is hardly a done deal: Other countries are innovating to catch up, with New Zealand, Indonesia, Turkey, and Kenya seeing the same opportunity and making investments accordingly. According to BCG analysis, through 2050, the US is expected to capture $250 billion in a total $1.2 trillion global export market. However, these estimates can be expanded if we capitalize on export opportunities through innovation and policy changes.

Policy Recommendations

Technology Wide

Innovative technologies and a supportive policy landscape could provide the launching pad necessary to commercialize geothermal. However, while the benefits in recent legislation provide a firm foundation, more is necessary to retain and build the US first-mover advantage. Additional federal support should follow a six-pronged strategy that: 1) quickly commercializes and demonstrates innovations, 2) de-risks finance for early projects, 3) overcomes barriers to domestic deployment like burdensome permitting processes, 4) creates strong demand signals for firm clean energy resources, 5) improves the availability and sharing of sub-surface geologic data, and 6) better leverages the tools of US commercial diplomacy to capture market opportunities for emerging technologies.

Big Wins for Geothermal

- Energy Act of 2020: Passed at the end of the Trump Administration, the Energy Act of 2020 extended and increased innovation funding authorizations for a diversified suite of emerging clean technologies, including geothermal. The legislation authorized through 2025 the Energy Department’s geothermal R&D program, reauthorized funding for three new Frontier Observatory for Research in Geothermal Energy (FORGE) demonstration projects, and modified the definition of renewable energy for programs authorized through the Energy Policy Act of 2005 to recognize power produced by geothermal resources as renewable energy rather than energy efficiency.

- Bipartisan Infrastructure Law: The BIL provided up to $84 million for geothermal demonstration pilot projects, $74 million of which was recently made available to fund up to 7 EGS and next-generation geothermal energy projects.

- Inflation Reduction Act: The IRA expanded tax credits traditionally reserved for wind and solar to include geothermal. In the near term, BCG determined the extended tax credits provided by the IRA will lower the levelized cost of electricity (LCOE) of geothermal by 40% making projects competitive with fossil fuel generators.

- Energy Earthshot Initiative: Announced in 2022, the Department of Energy’s (DOE) Enhanced Geothermal Shot brought awareness to the technology and set a department-wide goal of reducing the average national cost of EGS projects by 90%, to $45/MWh by 2035.

Accelerate commercialization and deployment of geothermal innovations. De-risking private investment and commercializing more geothermal technologies at home is critical to beating competitors in international markets later on. Geothermal projects already carry relatively higher fixed capital costs. When combined with the exploration risk, investors are disincentivized to support new projects. However, when that risk is minimized and projects become more profitable, deployment accelerates, giving domestic developers more opportunities to learn, enhance their industry know-how, and achieve economies of scale.

Increasing public funding for research and development to $216 million as requested by the Energy Department for FY24 is a strong first step in reducing investment risk. Supporting more programs through the Geothermal Technologies Office (GTO), Office of Science, and facilities like FORGE will develop better downhole materials and technologies – lowering failure rates and bringing more geothermal innovations to market. Additionally, Congress should focus on increasing demonstration grant funding for technologies that will drive durable competitive advantages and can be exported – like EGS and supercritical drilling technologies that have the potential to bring geothermal virtually anywhere. The US should also expand support for geothermal-lithium extraction projects that separate dissolved minerals from the hot brine produced by geothermal power plants. Geothermal brine could account for as much as 60% of global lithium production by 2025, and the Salton Sea in California alone could produce 600,000 metric tons annually, worth $6-12 billion, from its geothermal waters. Congress should also seek to sustain and even increase these investments well through the end of the decade to achieve the goals outlined in the Enhanced Geothermal Shot, which runs through 2035.

De-risk financing for early-stage projects. Creative financing can de-risk demonstration and early-stage commercialization, giving US companies the confidence to develop faster. This could be accomplished by DOE reimplementing and Congress supporting risk insurance and cost-sharing programs through GTO like those phased out in the 1980s, such as the Program Research Development Announcement (PRDA, 1976), Program Opportunity Notice (PON, 1979), and User-Coupled Confirmation Drilling Program (UCDP, 1980). Additionally, access to DOE financing programs specifically for geothermal energy projects like the 1974 Geothermal Loan Guarantee Program and 1980 Loans for Geothermal Reservoir Confirmation Program may also be helpful. Improved versions of these programs could ensure percentages of available loan authorities are applied to independent stages of EGS development like lease acquisition, exploratory drilling, development drilling, or power plant construction. While DOE’s Loan Programs Office currently provides loan guarantees for clean energy projects, including geothermal technologies, available funds are not specifically parsed out for different technologies or stages of project development, and for the most part come with additional statutory requirements that are absent from these prior programs, such as innovation or site-specific stipulations. These loans would have an even greater impact if they could be paired with or converted into grants supported by a Congressionally appropriated geothermal risk reduction fund, to offset exploratory drilling risks, making public and private debt more feasible for the industry.

Streamline barriers to domestic deployment. A favorable permitting and regulatory environment can unlock geothermal deployment, facilitate learning, and help US companies achieve economies of scale. According to BCG, it takes an average of 7-10 years to develop geothermal plants, and 4-6 of those years are spent mainly on well permitting. In contrast, the average deployment timelines for both O&G and utility-scale wind and solar projects are 2-6 years. Longer timelines compound the cost of capital, with financing making up 30% of geothermal’s already high capital costs. When compared to 2-7% for wind and solar, the appetite for private investment into firm geothermal energy can diminish in favor of other, more variable energy technologies.

Anything we can do to reduce time and cost associated with being able to drill for the purposes of geothermal energy is something that we’re very excited about.

- Colorado Governor Jared Polis (D), who leads the Western Governors’ Association’s geothermal technology initiative The Heat Beneath Our Feet, in an interview with Stateline

Easing permitting and the implementation of an efficient regulatory environment could decrease timelines by 25-50% and increase geothermal capacity by as much as 15-20 times by 2050 as new technologies like EGS and supercritical drilling unlock vast untapped US reservoirs. The US could allow for streamlined review through continued support for development of a geothermal-specific Renewable Energy Coordination Office (RECO) as outlined in the 2021 MOU to Improve Public Land Renewable Energy Project Permit Coordination. Such a RECO could be designed to raise awareness and harmonize geothermal regulations and permitting requirements as well as provide centralized information sharing opportunities between federal, state, and local permitting agencies. This interagency office could create templates for new wells to speed approvals and target lease approvals on specific federal land for geothermal projects. Such an office could also ensure streamlining does not come at the expense of seeking social license and community engagement. Additional Department of Interior and Bureau of Land Management funding would be essential to supporting such an office.

Create demand signals for firm clean energy resources. Enhanced market signals could help the US pull further ahead in global geothermal energy development. Setting Clean Electricity Standards that include sub-targets for clean, dispatchable, baseload power would incentivize the utility-wide adoption of more geothermal projects, in turn reducing carbon pollution and increasing grid reliability. These standards could be modeled similar to California Public Utilities Commission Integrated Resource Planning mandates that require certain percentages of new clean energy generation to come from firm, zero-emitting sources like geothermal. Standard-setting efforts should be paired with better access to grid interconnection points.

Whether it is used for heating our homes or keeping the lights on, geothermal provides clean and always-on energy that requires no external backup.

- Senator Lisa Murkowski (R-AK) highlighting the capabilities of geothermal energy during a Senate Energy and Natural Resources Committee hearing, June 20, 2019

Geothermal energy projects can also reduce fossil fuel consumption in direct and district heating applications. District and direct heat from geothermal reservoirs could provide most of residential heating and up to 50% of industrial heat demand. Including heating and cooling in emissions standards could shift market demand and focus private investment to develop more efficient industrial-scale geothermal heating technologies. In addition, setting government procurement contracts to purchase geothermal heating and power generation for public buildings and assets could stimulate stepping-stone markets.

Improve sub-surface geological data at home and abroad. A better understanding of the ‘heat beneath our feet’ would guarantee US companies a higher rate of success in the development of viable geothermal projects. Like an oil and gas operation, a geothermal project needs to identify, tap into, and efficiently use energy resources buried deep underground. But lack of quality data characterizing the subsurface makes exploration and geothermal development more expensive and uncertain – with most of the risk for geothermal being concentrated in the exploration phase. Reducing that risk would improve the odds of sites selected for geothermal drilling having the heat and permeability necessary for a viable project. Robust geologic mapping, geochemical surveys, and subsurface characterization assessments can provide that assurance.

However, the US has historically underfunded its geologic data collection efforts. United States Geological Survey (USGS) geothermal resource assessments are outdated and have not comprehensively considered innovations like EGS and other next-generation technologies throughout the entire US, which might add hundreds of GWs to potential capacity. Increased sustained funding to USGS and the Department of Interior could support updates to existing geothermal resource assessments, as well as a centralized database of surveys, core information, subsurface imaging, current wells, and other play fairways analysis data critical to the industry. The modern database could build upon geologic data gathered by industry and state institutions to improve the timely input of data easily accessible to developers.

The US could prioritize subsurface analysis and data in its international programs and technical assistance. The State Department’s Bureau of Energy Resources already prioritizes sustainable mining work and could expand this work to share best practices on subsoil data collection starting with strong potential geothermal markets, such as Indonesia, Kenya, and Mexico. The Interior Department already does similar work in mining and oil and gas exploration. Coordination of such US efforts could occur under existing multilateral frameworks such as the Partnership for Transatlantic Energy and Climate Cooperation (P-TECC), as well as the Net-Zero World Initiative. Helping other countries maximize their geothermal technologies expands the potential market for leading US geothermal companies.

Direct US commercial diplomacy toward emerging technology opportunities. Linking commercial and climate diplomacy can supercharge the global market for innovative, net-zero-enabling technologies if the United States directs additional staff, training, and export financing resources toward this effort. While the US has a comparative advantage in highly exportable segments of the geothermal value chain, simply having ripe conditions for exports does not mean they will take off. Rather, US companies’ ability to export new, innovative technologies like geothermal will be highly dependent on US government policy and support, especially given competition from other governments.

The Commerce Department houses its own foreign service charged with advancing US commercial diplomacy and promoting US exports. However, this diplomatic corps is a fraction of the size of the State Department equivalent and generally directs its time and attention at near-term opportunities, which biases resources away from more innovative opportunities, in which China does not yet have commanding, perhaps insurmountable, lead. Expanding the ranks of the Foreign Commercial Service and training its officers to prioritize novel cleantech solutions, such as geothermal, would help the US capitalize on and maintain its advantage in one of the fastest-growing segments of the global economy.

The Departments of Commerce and State should regularly equip US embassies with market analysis outlining priority markets and value chain sectors, in which domestic manufacturing developments can translate into exports. This report represents one effort to provide an actionable level of specificity. The State and Commerce Department can also prioritize high-level deals and announcements with strategic markets to kickstart the geothermal export pipeline. Global efforts to advance climate ambition with a focus on firm, dispatchable electricity and decarbonizing heating and industry will help advance geothermal. The Departments of Commerce, State, and Interior, and USGS should coordinate efforts to provide technical assistance to partner countries and identify potential project sites abroad.

The Energy Department can expand its Net-Zero World Initiative, through which US national laboratories assist countries with highly tailored, technical decarbonization roadmaps. Indonesia is already a partner country, but expanding the initiative to include other prospective geothermal markets would give US companies first-mover advantages.

Project Development

At $402 billion of the global geothermal market addressable by the US, project development is the largest value chain segment driving America's competitive advantage. Strong domestic O&G players provide crossover experience and requisite technology to support dominant geothermal project developers. Innovation and field experience in mapping, drilling, and hydraulic stimulation have created a mature market especially given low levels of deployment in the rest of the world. If the US capitalized on this value chain segment and provided domestic players with the valuable learning experience associated with bringing geothermal technologies to scale, we could stay competitive and capture more of the global market share.

Project development, while the largest value chain segment, also possesses the bulk of the risk (50%) and cost (40%) associated with geothermal projects. De-risking the sector requires giving domestic developers more opportunities to scale and learn. Speeding up deployment rates would require a favorable permitting environment for geothermal projects as outlined previously. This could be complemented by efforts to set new geothermal lease targets on federal lands and require the Bureau of Land Management to hold auctions more frequently than every two years. Also, supply-side policy actions like additional loan guarantee programs, risk insurance, and tax credits would incentivize more private investment. Furthermore, facilitating partnerships with O&G companies would attract the capital and transfer expertise needed to build off the origins of our competitive advantage and scale faster.

Success may depend on our ability to unlock EGS resources. Utilizing the same stimulation and deep drilling technologies as O&G, the US is the current leader in EGS project development. However, countries like Iceland, Japan, and Indonesia are investing heavily, threatening this lead. The US project development value chain sector for geothermal is estimated to create 18,000 jobs by 2050, paying an average salary of $100,000 annually. Policies that build upon our existing competitive advantage in the industry would see that number grow.

Engineering, Procurement, and Construction (EPC)

Highly integrated with project development, EPC represents a global market opportunity addressable by the US of $201 billion with the potential to create 40,000 jobs paying average annual salaries of $85,000 through 2050. Geothermal project sites vary based on the unique system characteristics of the area, and the US leads in its ability to adapt projects to custom geologic and technological features. This competitive advantage, combined with the ability to coordinate more efficiently with other developers, reduced operational costs, and experience designing next-generation hybrid plants, enables US players to garner premiums for experienced engineering.

Procuring geothermal projects for relevant government facilities, like national labs and military bases, would function as critical advanced market commitments and deploy more projects in various unique regions across the country. Coupled with a streamlined permitting process, geothermal deployment at government facilities would grant domestic EPC firms more opportunities to build geothermal experience alongside project developers, growing future potential global EPC market value.

Original Equipment Manufacturing (OEM)

Currently in a less competitive position, the US addressable OEM global market share is estimated to be $151 billion through 2050. However, as domestic industries shift their focus from mature technologies to emerging ones, the US can reclaim lost global market share and seize the leadership position.

There already exists a highly concentrated global market of OEMs in countries like Japan and Israel with many focused and well-established mature technologies like flash and binary turbines. But growth potential exists with the development of new technologies like low-enthalpy turbines and heat-resistant downhole materials. The US lags behind China, Japan, and South Korea in patent activity of geothermal technologies. But US institutions provide higher quality research, especially in areas like drilling and exploration, power generation, heat exchangers, fluid flow, heat pumps, and mining. With the right R&D support, the US can lead a new wave of geothermal technologies.

To become leaders in OEM, the US should focus on policies that spur and incentivize the R&D of new tools, technologies, and equipment. Federal R&D funding will be helpful in developing technology breakthroughs important to develop initial IP that can quickly commercialize. National labs, universities, and the private sector should continue to work together to develop these breakthroughs. The domestic OEM value chain is expected to create 10,000 jobs with average salaries of $95,000 through 2050. Expanding US R&D capacity can grow that number considerably.

Once new geothermal technologies are developed it will be important to make sure they are manufactured in America. The $10 billion in 48C manufacturing tax credits, provided by the IRA, extends a 30% tax credit for investments made in clean energy manufacturing facilities, including geothermal. Continuing the 48C tax credit in the future would incentivize domestic manufacturers to scale up production of the next generation of geothermal technologies, help build moats around intellectual property rights over technologies and manufacturing processes, and enable the US to take the lead in the global geothermal OEM market.

Impacts from Policy Recommendations

To be sure, geothermal will not be the primary driver of the clean energy transition in most countries around the world, but it can provide essential benefits that accelerate decarbonization. It can provide clean heat and firm electricity that other cleantech solutions cannot and expand lithium production to assuage other bottlenecks that might otherwise impede the transition. Moreover, the US can lead the market, creating as many as 100,000 jobs through 2050 or even more if it can get the export market off the ground.

Achieving this full potential will depend on myriad policy decisions that the US takes today. These decisions include implementation of BIL and IRA programs, follow-up legislation, executive actions targeted at firm power generation and decarbonization of hard-to-abate sectors, as well as new directions in foreign policy that include better aligning commercial diplomacy and international climate policy. Such a strategy would likely require several years of dedicated effort and unprecedented workforce training, interagency processes, and even more funding across departments and agencies. Still, the world can benefit if America leads.