Memo Published July 20, 2023 · 13 minute read

Solar Power: Policies to Help America Lead

Takeaways

- The US has a significant opportunity to boost competitiveness and increase energy security through accelerated growth in the solar industry. It is one of the largest sources of renewable energy globally.

- Economic incentives for solar in the Inflation Reduction Act (IRA) are a positive step toward building US competitiveness. Investment and production tax credits, along with several measures to expand residential and commercial solar buildout, are substantial. These provisions are designed to drive costs down and stimulate manufacturing and deployment.

- The US must continue to expand on innovation and technical leadership in solar to reduce reliance on future imports of critical solar components, especially for the next generation of wafers, cells, modules, and solar manufacturing equipment that China does not yet dominate. Manufacturing tax credits will provide important assistance to reach scale and enable more innovation.

- Finally, US companies are leaders in project development and are poised to excel in solar panel manufacturing. US firms and workers – with the right tools and resources – could substantially substitute imports, expand our lead on thin film solar modules, and gain footholds in export markets in these strategic value chain segments. However, ongoing workforce development and expansive use of apprenticeships are needed for US industries to reach their growth potential.

Why the US Should Compete in the Solar Market

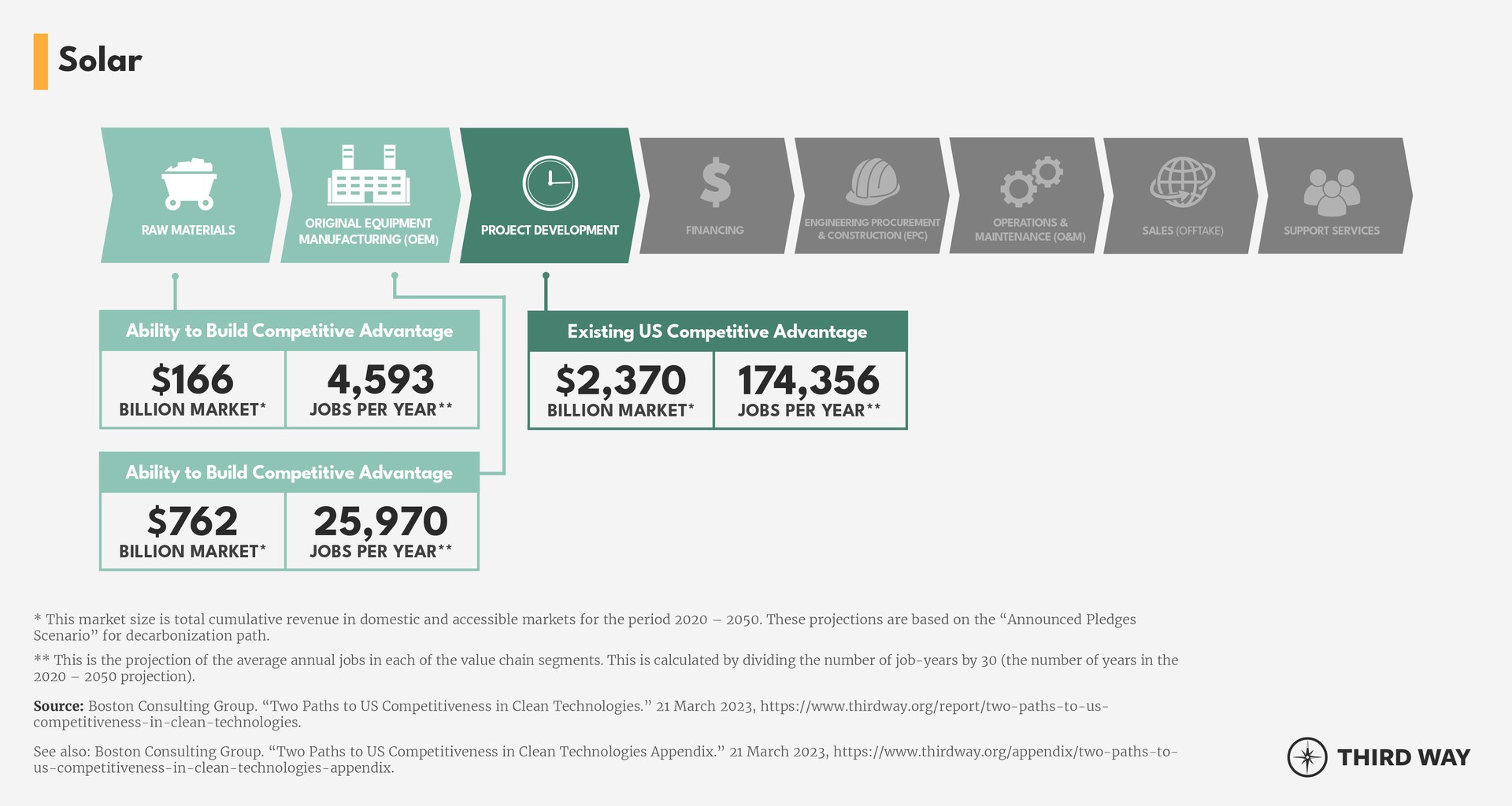

The size of the market opportunity and job creation are substantial. Between 2020 and 2050, solar will have an addressable market value of $4 – 5 trillion. Average annual job gains of 175,000 are expected in solar project development between now and 2050. The COVID-19 pandemic and recent geopolitical tensions have laid bare the risk in depending on a single country or region for goods and services at the center of national goals. To achieve the Biden Administration’s target of clean electricity by 2035, solar would need to account for a 40% share of US electricity supply compared to just 4% today. Even though solar is growing rapidly, deployment still needs to accelerate to achieve the US goal. The US already has experience and other advantages when it comes to developing and constructing solar installations here at home. If the country is to rapidly expand the use of solar power, however, we should try to strengthen our hand in these and other areas of the solar energy value chain, to maximize the benefits of solar growth for more American businesses and workers and minimize reliance on less reliable trading partners.

The US is actually a leader in the production of solar panels made from thin film, especially cadmium telluride technology, and can continue to build on that. Solar panels made from polysilicon account for 96% of global shipments, and about 50% of domestic shipments. In terms of international demand, US manufacturing of polysilicon is way behind the competition. The US is dependent on China and Southeast Asia for all upstream supply chain segments for polysilicon semiconductors. Over 95% of global output of silicon wafers – used for the production of solar cells – takes place in China. About 75% of the silicon solar cells used in the production of solar modules that are installed in the US are made by subsidiaries of Chinese companies located in just three Southeast Asian countries: Vietnam, Malaysia, and Thailand.

This over-dependence on distant suppliers is risky and subject to supply chain disruptions that could slow deployment, derail US climate goals, and threaten the US clean energy economy. Support for domestic manufacturing will reduce this supply chain risk. At the same time, the US can build upon the Inflation Reduction Act and expand R&D investments in innovations such as automation to make US production cheaper. Both activities will allow the US to reap the economic and jobs benefits from solar’s central role in global decarbonization going forward.

The IRA and IIJA provisions can help the US develop a robust domestic supply chain by subsidizing component manufacturing across each step – polysilicon, wafer, cell, module – along with providing tax incentives to developers, tied to key domestic content requirements, to spur domestic manufacturing.

-Boston Consulting Group. Two Paths to US Competitiveness in Clean Energy Technologies.

Congress and the Biden Administration recognize the urgency of the solar challenge and the imperative that the US regain competitiveness in this industry. The IRA provides significant incentives that will lower the cost of production, boost investment, and allow for an acceleration in deployment. According to a new BCG analysis that assessed the IRA impacts, as well as the Bipartisan Infrastructure Law (BIL), these policies are projected to:

- Decrease the solar levelized cost of energy (LCOE) by 40%,

- Make US-produced modules 25-40% cheaper as compared to historical imports, and

- Increase solar capacity by 30-40% by 2030.

Policy Recommendations

Even with the IRA in hand, more can be done to supercharge US solar manufacturing and accelerate domestic deployment. The US has a competitive advantage in solar project development, with the ability to build a competitive advantage in raw materials and manufacturing. The US can take three regulatory and policy actions to expand and jumpstart US competitiveness in these key segments of the solar value chain, as well as steps to build an enduring technology-wide advantage in this growing sector of the global economy.

Technology-Wide

Address the regulatory barriers confronting US firms and workers in the solar industry.

There are several regulatory issues that affect the domestic solar industry today. First, the United States has kept in place import tariffs on Chinese solar components and panels, which has led to an increase in the relative attractiveness of domestic solar-panel manufacturing. At the same time, the US Department of Commerce has undertaken an investigation into whether Chinese companies have circumvented those tariffs using "pass-through" countries in Southeast Asia. The Biden Administration has imposed a two-year tariff moratorium to maintain access to inexpensive foreign panels as the domestic supply chain ramps up with the help of new incentives in the IRA and BIL. Tariffs advantage and disadvantage different segments of the domestic supply chain. Resolving these trade issues would inject much-needed certainty and confidence into the US market. For now, taking a "pause" allows for the ongoing buildout of solar installations as these trade challenges are sorted out. Our strategic approach should be to resolve these issues with transparency, ensure that any anti-competitive behavior is penalized, and seek a level playing field across the supply chain segments.

Producers don’t want to rely upon unstable sources.

- James May, Former CEO of REC SiliconNote: REC Silicon recently restarted solar-grade polysilicon production at their facility in Moses Lake, Washington.

Streamline permitting and make progress toward grid modernization

Congress should reach a bipartisan deal on permitting reform and work with state and local government officials, as well as utilities, to break through these bottlenecks, thereby releasing more renewable capacity on the grid. The urgency to reduce barriers to grid expansion, enhanced transmission planning, and interconnections between regions cannot be overstated. Without a wholesale improvement in the electrification infrastructure, efficiencies from more solar deployment cannot be harvested. More than 600 GW of solar capacity is backed up in the interconnection queue with wait time dragging out to nearly 4 years before becoming operational. BCG found that our ongoing and rapid deployment of solar installations here at home is a critical aspect of building a stable foundation for demand, as well as in project development, This, in turn, should provide a much better opportunity at exporting these services and bringing home more of the global market share.

Expand and accelerate a comprehensive approach to solar workforce development and training.

Expanding engineering and solar-focused training programs across the value chain segments would allow for workforce growth capable of delivering a decarbonized grid by 2035. The solar credits in the IRA do incentivize companies to provide prevailing wages and hire apprentices and this will provide for greater workforce growth, but additional policy, including expanded support for jobs reskilling and registered apprenticeship programs, will be necessary to ensure that labor supply can match demand in a tight market. Ultimately, progress on immigration and targeted visa programs for solar workers will help ease this pressure. More workers are critical to the success of accelerated solar deployment.

Raw Materials and Inputs

Stimulate domestic production of polysilicon and thin film technology

Polysilicon is the primary raw material for silicon photovoltaic solar cells, while thin-film cells start by refining cadmium and tellurium into powders that can be put directly onto a glass sheet. A viable US solar industry starts with raw materials and other inputs to manufacture, deliver, install, and operate solar facilities. The US cannot afford to be completely dependent on other countries for polysilicon or limit its R&D on next-generation technologies that use more accessible materials. The US is currently the world’s leader in thin film technology. It is important for US-based companies to push toward greater production capacity across multiple fronts. For the US to move back into the production of downstream solar components – wafers, modules, and cells – both polysilicon and thin film capacity needs to grow. BCG estimates that the US market for polysilicon alone could be nearly $200 billion through 2050, making production and processing worthy of consideration for US expansion.

The growth of thin film solar panels is providing a global competitive edge to the biggest solar manufacturer in the US, First Solar. A global market report released in January 2023 projects that the global cadmium telluride market (thin film) could grow at a compound annual rate of 12.5% between now and 2028.

According to the Department of Energy’s recent solar supply chain report, while the cost to produce a domestic thin film solar module is competitive with Southeast Asia, polysilicon production is not. This report was released prior to the enactment of the IRA. This law now provides both investment and production tax credits to revitalize domestic polysilicon production as well as expand leadership in thin film production.

The Solar Energy Technologies Office at DOE provides research funding for manufacturing competitiveness and solar cell efficiency. More funding for solar R&D is needed to ensure the US has competitive leadership, including near cost-competitive commercial manufacturing processes, and in emerging technologies that have increasing promise to be commercialized. Recycling of polysilicon is also an activity that could be stimulated with government loan programs that derisk the projects and enhance private investment returns. Without support, growth in recycling may not reach the take-off stage.

Manufacturing

Expand support for manufacturing investment

Manufacturing incentives are key to rapid deployment of solar installations and can help US businesses secure more of a lucrative OEM market. BCG estimates the addressable OEM market is over $700 billion through 2050, with average annual job gains of 26,000 during the 30-year period. The IRA put in place a valuable advanced manufacturing tax credit (45X) that focuses on incentivizing production for wind, solar, and batteries. This tax credit has no funding limit.

The 48C tax credit, which provides a 30% ITC to clean energy manufacturing facilities, can help stimulate businesses to build new solar wafers, cells, and modules here in the US. This helps to grow our scientific and manufacturing expertise, retaining intellectual property rights over technologies and manufacturing processes, and providing opportunities for thousands of American workers.

However, this tax credit is one of the few in the IRA that is capped, with only $10 billion in funding that firms must apply and compete for. Expanded funding for the 48C tax credit would deliver positive results. Further, the Energy Department should simplify the application process and shorten the review process so firms can quickly make final investment decisions.

IRA tax credits go a long way to lower high upfront capital expenditures, but more can be done to incentivize investments. The federal government can leverage its procurement power to build stepping-stone markets for homegrown manufacturing and further derisk investment by providing low-cost loans and loan guarantees through the EPA’s new Greenhouse Gas Reduction Fund (GGRF) and the various offerings of the Energy Department’s Loan Programs Office. The GGRF does require EPA to spend all $27 billion before October 1, 2024. Extending this deadline to ensure the funding is dispersed in an orderly fashion would be beneficial.

South Korean-based solar manufacturer Hanwha Q CELLS recently announced a $2.5 billion investment to expand its Dalton, Georgia solar plant and to build an additional plant in northwest Atlanta. The investment not only plans to bring 2,500 jobs to Georgia, but represents the largest single investment in solar manufacturing in the U.S.

According to John Podesta, senior advisor to the president for clean energy innovation and implementation, Hanwha Q CELLS is on the road to produce 30% of all U.S. demand for solar panels by 2027.

-Savannah Morning News, January 11, 2023

In addition to the 45X tax credit, it is difficult to assess whether the IRA provisions will be enough to ensure manufacturing at scale. A recent study of the clean energy policy impacts undertaken by Boston Consulting Group indicates that several additional actions will unlock manufacturing at scale. These include an ongoing evaluation of the Section 301 tariffs which are currently on "pause," reviewing existing stringent certifications for PV manufacturing equipment, and funding research in manufacturing innovations.

Project Development

Globally, project development for solar is a $2.0 - 2.5 trillion market through 2050. The US has the second-largest deployed solar capacity globally and has gained significant experience developing utility-scale solar projects. US project developers currently capture 75% of the domestic market. The expertise of big players like NextEra, which has 28 GW of renewable energy capacity, represents substantial scale that can be leveraged in global markets. Project development for solar installations is a huge opportunity, generating significant market value and job creation. Technical leadership on effective and efficient project management is a business that our major developers can export globally.

Many of our allies and trading partners are actively gearing up for renewable energy growth with government support to address the same security concerns that the US faces. One way to scale up domestic production and innovation efforts is to expand our commercial diplomacy. While the US may be competitive in one value chain segment, like project development, a trading partner may be competitive in engineering, procurement, and construction. The Departments of Commerce, State, and Energy are poised to expand existing clean energy and climate partnerships with Korea, Japan, the EU, and India, among other countries, to find mutually beneficial opportunities for supply chain coordination.

Impacts from Policy Recommendations

As one of the more mature technologies of those BCG assessed, solar presents a large domestic growth opportunity even if the global market is more competitive. Should US companies develop innovation pathways for solar, especially in the OEM value chain segment, it could open avenues for a lower cost structure and an ability to compete strongly in export markets.

Both the Bipartisan Infrastructure Law and the Inflation Reduction Act boosted the competitiveness of American solar manufacturers, project developers, and those companies charged with operating and maintaining the ever-growing number of solar facilities across the country. We can achieve the full potential of this legislation if America leads.