Memo Published March 17, 2023 · 20 minute read

Clean Hydrogen: Policies to Help America Lead

Dr. Rudra V. Kapila, Alexander Laska, & Nicholas Montoni, Ph.D.

Takeaways

- Clean hydrogen will play an outsized role in decarbonizing hard-to-electrify sectors of the economy. The more we do now to ensure that the US can grow a durable competitive advantage in the global market for clean hydrogen, the more of that market will be captured by US companies and the more jobs in the clean hydrogen value chain will be filled by American workers.

- Commercial diplomacy and trade policy actions are critical for US market access to European purchasers. Designing domestic regulations and incentives t0 reflect the opportunities and limitations of export markets would yield a stronger US hydrogen sales pace and domestic job growth.

- The US needs significant investment in hydrogen-specific equipment for leakage detection. Safe and effective hydrogen production, transport, and storage will give the US a competitive advantage as these technologies will generate substantial demand in global markets.

- Even more investment is needed in liquid organic hydrogen carriers, storage networks, newly designed and repurposed pipelines, and port infrastructure to make the US a leading global supplier. Since these transport and storage technologies are still nascent, the US has time on its side to gain a competitive edge.

Why the US Should Compete in the Clean Hydrogen Market

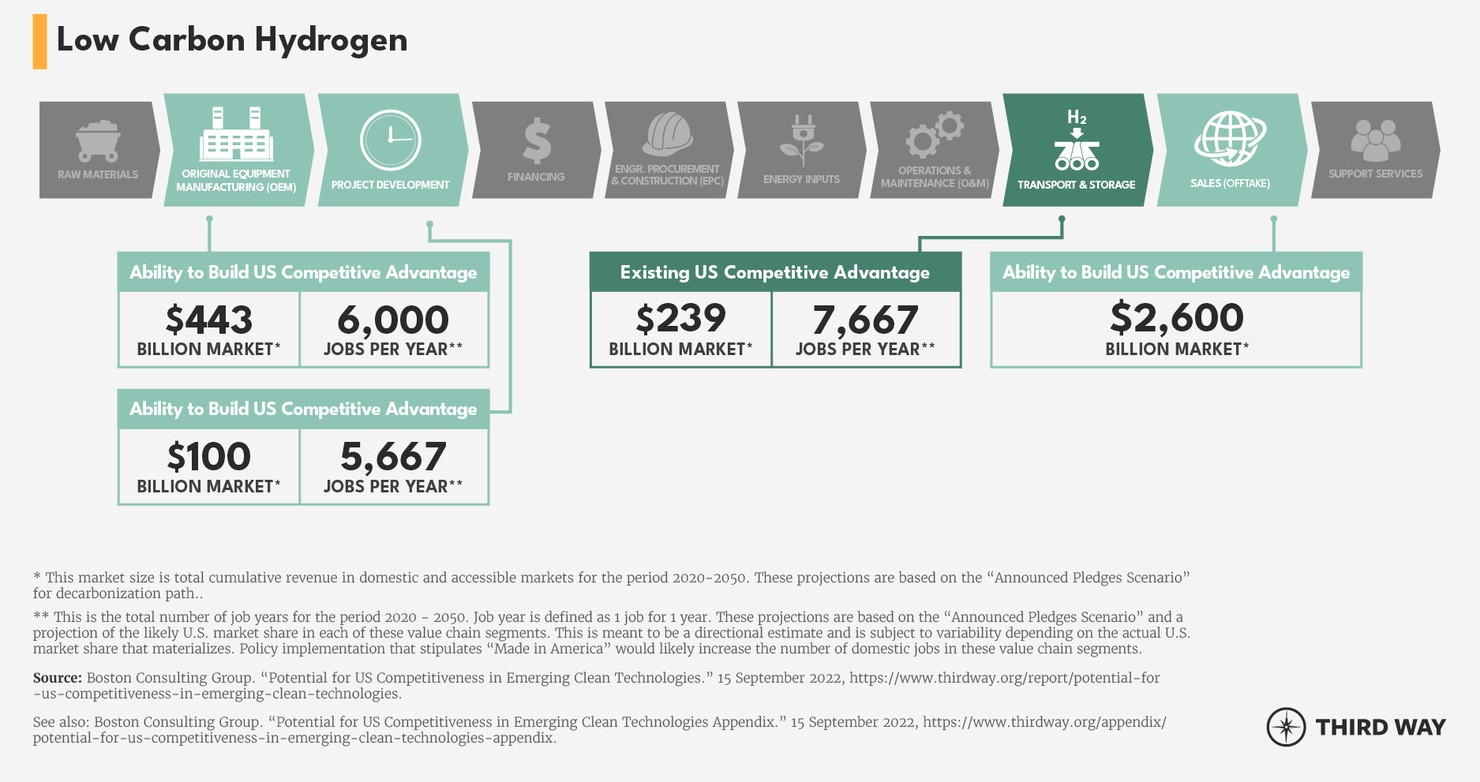

In September 2022, Boston Consulting Group (BCG) released a groundbreaking report assessing the potential for the United States to compete in the global market for six clean energy technologies including clean hydrogen. Their analysis found that the US is most likely to be globally competitive in four segments of the clean hydrogen value chain: original equipment manufacturing (OEM), project development, transport and storage, and offtake. Securing American leadership in these four value chain segments can grow the US economy by trillions of dollars and provide meaningful opportunities for tens of thousands of American workers.

The global output of low-carbon hydrogen is expected to reach nearly 200 megatons (Mt) by 2050, a significant leap from just 3 Mt in 2020. Among the four key value chain segments, the market for hydrogen is projected to cumulate to over $3 trillion between 2020 and 2050. The global demand for clean hydrogen will create over 540,000 annual jobs between now and 2050. This includes high-paying jobs in project development that will generally require a bachelor’s degree, as well as construction jobs in transport and storage that will not require higher levels of education. Similarly, there will be a high demand for workers across the entire hydrogen value chain with transferrable skills-sets in risk management and technical expertise from current oil and gas sectors, as well as chemical production industries. This includes a need in areas of engineering, operations, procurement/supply chain management, HR, finance, technicians, etc. That’s a significant opportunity for economic growth, and the US should be helping its businesses and workers compete for a large share of it.

Additionally, low-carbon hydrogen is poised to play an important role in decarbonizing our economy, particularly in heavy-duty transportation and bulk chemical production. BCG estimates that clean hydrogen will reduce emissions by up to 5 gigatons each year by 2050; American leadership in this industry could help get low-carbon hydrogen into the economy to achieve our emissions goals faster and more affordably.

The US can take a number of steps to enhance its competitive advantage in this market. For one, the US should leverage all available types of carbon-free electricity for clean hydrogen production, including nuclear power. The US also must embark on a policy agenda to decrease the lifecycle carbon intensity of hydrogen production from fossil fuels with carbon capture, in order to ensure hydrogen produced in the US can be sold into Europe and other markets that are enacting strong clean hydrogen standards. For example, the European Union (EU) is currently proposing a Carbon Border Adjustment Mechanism (CBAM), which essentially involves the implementation of a border tax on imported goods depending on the carbon intensity of their production. With this context, the carbon intensity of domestic hydrogen production will have a huge bearing on US exports of related transportation products (e.g., ammonia for shipping or sustainable aviation fuels) and whether or not those products would be eligible for European markets.

With the support of federal funding and regulatory policy, the US could develop new electrolyzer technologies faster than our competitors, invest in the clean hydrogen workforce, and export more hydrogen storage and transport infrastructure. US industry players can also detect, prevent, and mitigate hydrogen leakage across the entire supply chain, making them a more attractive and less-polluting option to customers around the world than those companies that lag behind on leak detection, prevention, and mitigation. These policy tools will not only give the US access to a bigger share of the multi trillion-dollar hydrogen market but also become competitive against our European and Asian counterparts that are also developing low-carbon hydrogen technologies.

Policy Recommendations

The US should pursue an array of policies to ensure American companies can compete and win in the global market for clean hydrogen. Technology-wide policy recommendations are designed to impact multiple value chain segments, such as manufacturing, project development, and offtake. Additional policies specific to individual segments of the value chain will ensure the US can grow and maintain a competitive advantage in those priority segments with the greatest potential for US leadership.

Technology-Wide

Recognition of international clean hydrogen standards

The EU is likely to be one of the most lucrative markets to sell clean hydrogen; BCG estimates that the EU will grow to a market of around $480 billion, or about 12% of the total global serviceable addressable market (SAM). But the EU is clearly demonstrating that not just any clean hydrogen will do, pursuing policies such as REPowerEU that will only allow hydrogen produced from renewable resources to be imported. South Korea represents an even larger potential market for clean hydrogen, at $750 billion, due to its own aggressive hydrogen targets and limited production capacity. We must reflect the implications of the varying approaches to clean hydrogen standards in the design of our own policies, leveraging the opportunities they create for the US to become a world leader in the development and implementation of hydrogen production technologies.

The US should make use of RD&D, expanded incentives, and lifecycle emissions standards to encourage our domestic industries to continually drive down emissions from hydrogen production, transport, and storage. Beyond the obvious climate benefits, this would put the US in a stronger position to compete for international markets – where there are much stricter carbon intensity limits on purchased and produced hydrogen.

These three recommendations for US regulation would promote domestic competitiveness with international standards.

1. Increase the cost of emitting Methane

Carbon dioxide is a known byproduct of hydrogen production, particularly when produced using Steam-Methane-Reformation (SMR) technologies. One way to resolve this is to integrate carbon capture technology into fossil fuel derived hydrogen production. Notably, the recently passed hydrogen Production Tax Credit (PTC) within the Inflation Reduction Act (IRA) requires a lifecycle analysis (LCA) and is therefore designed to favor the least carbon-intensive production pathways. Furthermore, the IRA encourages hydrogen producers to address "upstream" emissions including methane, which ultimately raise the carbon intensity of hydrogen produced from fossil fuels. Addressing these upstream emissions will increase the value of the tax credit these hydrogen producers can receive.

There is also an additional provision in the bill that targets methane leakage more widely from fossil fuel operations with a methane fee, though this does not necessarily target SMR facilities. The methane fee does however impact shipments of Liquefied Natural Gas (LNG), and the US Government is actively engaged in dialogue with international partners to set a global standard on the carbon intensity of LNG exports. Similarly, methane emissions associated with fossil-derived hydrogen production will be a problem for the US in the context of competitiveness and potential exports to international markets. For example, the European Commission’s Carbon Border Adjustment Mechanism (CBAM) which considers the carbon emitted during the production of carbon intensive goods that are entering the EU. This import tax will go into effect by October 1st, 2023, and some of the initial goods impacted by CBAM include not only hydrogen but other products such as cement, aluminum, and steel, which can potentially be produced using hydrogen. Therefore, the penalty for methane emissions should be increased, e.g., by augmenting the recently passed fee provision in the IRA to explicitly include all SMR facilities (existing and future) for hydrogen production.

2. Support hydrogen leak mitigation

One piece of the puzzle that isn't yet being addressed by policy is "downstream" emissions, specifically for direct hydrogen leakage between point of production and use. For example, the Hydrogen PTC discussed above only covers emissions from ‘well-to-gate’, meaning up until the point of production, but not after it leaves the production facility. That’s fine if all hydrogen produced is burned or used in a fuel cell, which emits no greenhouse gases. However, if hydrogen were to leak at any point in the value chain, e.g. during transport or storage, then its reactions with the ambient air could lead to indirect warming via ozone, methane, and water vapor formation.

It is important to tackle direct hydrogen leakage because of its short-term global warming potential. It also makes sense from a competitiveness standpoint. Environmental and safety concerns associated with hydrogen leakage could limit global uptake of low-carbon hydrogen. By developing solutions to minimize leakage, the US could ensure it gets greater access to a larger market across the clean hydrogen value chain.

Though there are existing hydrogen leak detection methods, more research is needed to produce technologies that can detect lower concentrations of hydrogen with shorter response time in a variety of applications and from a variety of assets (electrolyzers, storage facilities, pipelines, etc.). This is an underdeveloped area that the US can lead on and gain a competitive advantage. The U.S. Department of Energy (DOE) and National Science Foundation (NSF) should fund researchers of hydrogen leak detection and rapid mitigation responses. Additionally, as leak detection and mitigation strategies come to market readiness, they should be demonstrated as part of the DOE’s hydrogen hubs programs to validate their usefulness in hydrogen networks and ecosystems.

Furthermore, like the IRA's methane fee discussed previously, Congress should also explore creating a similar provision on emissions resulting from direct hydrogen leaks at facilities. Specifically, it should target the indirect greenhouse gas emissions (e.g. ozone) produced from hydrogen leakage throughout the entire value chain of hydrogen technology. The fees collected could be used to fund the further development of specialized and accurate leakage detection equipment, which will also have huge export value to international markets that are also currently building out their hydrogen technology systems (e.g., EU, UK, and Asia).

As a final policy lever to spur innovation in hydrogen leak detection and mitigation, the US Environmental Protection Agency should co-ordinate with other agencies such as the DOE and the US Department of Transport’s Pipeline and Hazardous Material Safety Administration to establish a hydrogen leakage threshold on all hydrogen infrastructure. Failing to meet this threshold should trigger corrective actions or fines, thereby inducing hydrogen suppliers to mitigate leakages.

3. Introduce a low- or zero-carbon fuel standard

Incentivizing hydrogen and its derivatives will not only increase offtake but also will signal a clear demand for low or zero-carbon hydrogen.

The IRA established five years of tax credits to support the production of sustainable aviation fuels (SAF), a low-carbon alternative to conventional jet fuel. This will provide a market for these cleaner liquid fuels, including e-fuels which can be made by combining clean hydrogen with captured carbon.

The US could take advantage of even more direct ways of driving market demand for clean hydrogen. A low-carbon fuel standard (LCFS) that sets clear and aggressive targets for reducing the carbon intensity (CI) of transportation fuels would create firm demand and thus drive investment in the production of the very cleanest fuels. Demand-side policy like an LCFS can help further scale up the clean hydrogen industry in the US, enabling producers to achieve economies of scale and lower costs so their products can become more competitive on the global market. California’s LCFS has been successful in accelerating the production of clean fuels like biodiesel and renewable diesel in the state, though jet fuel producers are not required to comply due to federal preemption over state laws on aviation. Congress should explore these types of policy tools at the federal level to drive investment in clean fuels, including those made with clean hydrogen.

OEM

Low-cost electrolyzers are essential for gaining hydrogen manufacturing competitiveness. China currently holds the leadership position for cheap electrolyzers, and the US missed this early opportunity. According to the BCG analysis, Chinese dominance is due to a very large portion of electrolyzer material being located within China, which also has 50% of the present global market.

However, not all is lost. The electrolysis process for hydrogen production is still very inefficient and expensive, especially when compared to fossil derived hydrogen, which is substantially cheaper when produced with steam methane reformation. There is much more room to improve and leapfrog the current generation of electrolyzers, and with additional, targeted R&D funding in this area of improved electrolysis, US players will be able to compete with existing technologies to produce electrolytic hydrogen more efficiently across the value chain. Several policy actions are needed to secure these growth opportunities as well as reduced risk exposure to China’s dominance in this technology arena.

Company Highlight: Air Products

Air Products, a US company founded in 1940 in Detroit, Michigan, is the world’s leading hydrogen supplier. It owns and operates over 100 hydrogen plants producing more than seven million kilograms (three billion standard cubic feet) per day of hydrogen and it maintains the world’s largest hydrogen distribution network.

Seifi Ghasemi speaks on how the IRA positions the US to be competitive in hydrogen production

1. Continuous investment in R&D

The US can achieve a competitive advantage in developing and patenting more efficient electrolyzers and hydrogen production technologies. We want the next generation of these technologies to be invented in America, built in America, and sold everywhere. These emerging technologies include anion exchange membranes, which contain no platinum group metals, and thermochemical water splitting which can source heat from nuclear or renewable energy. This is important because platinum is a recognized critical mineral internationally, and removing the need for this mineral will reduce a potential chokepoint on the overall supply chain. Additionally, research efforts at the US DOE and NSF should focus on developing and commercializing technologies in these categories to catalyze domestic ownership of intellectual property and manufacturing for new hydrogen production infrastructure. This should also include open topics and technology-neutral solicitations to keep the research program nimble and responsive to innovative ideas.

2. Maintain support for manufacturing incentives

Manufacturing incentives are key to rapid deployment of electrolyzer technologies. The IRA provided $10 billion in 48C manufacturing tax credits, which provides a 30% ITC to clean energy manufacturing facilities. This credit can help stimulate businesses to build novel electrolyzers and components here. This helps to grow our scientific and manufacturing expertise, retaining intellectual property rights over technologies and manufacturing processes, and providing opportunities for thousands of American workers. Ensuring continued availability of the 48C tax credit would deliver these positive results.

Project Development

Between 2020 and 2050, the US has a chance to tap into a nearly $130 billion market for clean hydrogen project development. The US can secure a greater share of this prize by fine-tuning and maintaining existing policy levers and expanding the scope of its demonstration and deployment efforts to include international partnerships.

1. Continue to support hydrogen hubs

The IIJA created an $8 billion program to demonstrate hydrogen hubs – connected ecosystems to study and validate large-scale, low-carbon hydrogen production, transportation, storage, and use. The unique opportunity for U.S. competitive advantage in project development revolves around learning how to establish and operate these networks in a way that creates economic benefit for nearby communities, avoids environmental hazards, and results in use or offtake of low-carbon intensity hydrogen.

In managing this program, the DOE should consider only applications that connect public works, clean energy manufacturing, and technological expertise and have a well-formed business plan for the actual use or sale of produced hydrogen. Doing so ensures that domestic companies and governments can grow project management, business, and financial expertise for large-scale demonstrations and export that knowledge and talent as needed.

The US DOE should further encourage hub applications to incorporate recycling, critical material recovery, and leak mitigation strategies into their business plans. For hubs that utilize electrolysis, recovery of platinum group metals will be critical to producing new electrolyzers in the future and can demonstrate the value of having a nearly closed-loop hydrogen network. Incorporating leak detection and mitigation can help validate those technologies and strategies across hydrogen production methods.

The UK, EU and the Middle East are actively developing their own hydrogen technological systems, or ‘clusters’, which are essentially the equivalent to hubs. There is an opportunity here for the US to lead on this particular type of project development, where the knowledge and know-how will be of great value in the context of any potential technology transfer to international markets.

Presently, the US is on track to develop and build out its hydrogen hubs first, thanks to federal policy support via IIJA and IRA. The funding notice for regional clean hydrogen hubs was released in September 2022, and it is anticipated that awards for projects will be finalized by the end of this year.

2. Create and engage international innovation networks

One way to scale up domestic innovation efforts, increase the production of clean energy technologies, and harmonize global standards is through International Innovation Networks (IIN). The most well known IINs for energy include Mission Innovation and the Clean Energy Ministerial. In the hydrogen context, the DOE and State Department plus other relevant federal agencies should engage with their counterparts in mature and emerging economies across the globe, with the intention of demonstrating first- or second-of-a-kind hydrogen network systems using American equipment and labor.

These early demonstrations with global partners serve multiple purposes: they provide the necessary validation for large-scale projects, they create economic value for partner nations and their workers, and both nations can use the knowledge gained from the venture to further iterate and innovate on the technology.

Transport and Storage

Notwithstanding the production pathway, the infrastructure and technological innovation required for the transport and storage of hydrogen is a critical part of the value chain. However, given the inherent chemistry of the element, the technical know-how in containing and managing hydrogen is complex, primarily due to its small molecule size which can leak easily. Furthermore, the farther hydrogen has to travel between production and end-use, the greater the potential for leakage into the atmosphere. This is still a nascent industry; therefore, the US can seize this opportunity to demonstrate and lead in the development of safe and effective hydrogen transport and storage.

The BCG study

found that the US has a strong competitive advantage in this segment of the value chain, especially since 75% of globally operating hydrogen salt cavern storge sites as well as more than 90% of the global hydrogen pipelines are located in the US and EU.

The technology-wide policy recommendations discussed above aim to increase hydrogen offtake, especially to decarbonize hard-to-abate sectors with high-heat requirements, e.g., steel, chemicals. This will increase demand for hydrogen-specific transport and storage infrastructure – irrespective of the color of the hydrogen produced (e.g., blue v green) – which will be needed globally. Even if Europe decides to place an import duty (via CBAM) on some US produced hydrogen due to its carbon intensity, transmission pipelines, adequate storage and offloading equipment will still be needed and are all key parts of the hydrogen technology system. Therefore, the quality of innovation and R&D in this area can give the US a competitive edge in becoming a key supplier of these critical transport and storage components for international markets building out their low-carbon hydrogen production systems.

1. Continue investment support for hydrogen-specific transport technologies

Building upon the provisions in IIJA and IRA, there needs to be a continuation of government investment to support the development of novel and high-quality hydrogen transport technologies, which is primarily carried out by DOE’s Hydrogen and Fuel Cell Technologies Office (HFTO). This should include things such as ammonia cracking and novel liquid organic hydrogen carriers (LOHCs). Hydrogen can be physically stored and transported as a liquid or gas; however, it is very unstable in its pure form. Therefore, chemicals such as LOHCs allow us to store and transport hydrogen over long distances in another chemical state that is more stable, instead of free hydrogen molecules. LOHCs are also considered to be an effective and efficient means for transporting and storing renewable energy because they can be stored for long periods of time. This way hydrogen can also provide resiliency to the grid, and which is why HFTO’s pioneering work in this area will also help US leadership in expanding deployment of renewable energy systems.

Support should also be continued for complementary technologies, such as storage networks and associated port infrastructure for hydrogen hubs. Not all hydrogen hubs will be coastal, but some of the first will be and high-quality specialized port infrastructure for hydrogen storage and transport will have huge export potential to markets in Europe and Asia, which are looking into developing their own hydrogen economies.

2. Incentivize repurposing of natural gas infrastructure and conduct necessary safety research

Thanks to new authorities, the DOE can now offer loan guarantees for an even wider set of critical energy infrastructure. This includes provisions within the Inflation Reduction Act to support repurposing existing natural gas infrastructure for hydrogen. However, increased investment in R&D and demonstration of this type of repurposing is still needed. Recent analysis shows that that there is a very high risk associated with transporting hydrogen through distribution pipeline systems, especially to confined spaces such as homes. Notably, none of DOE’s current roadmaps consider hydrogen as a viable option for heating homes, but still crucial for transport and other hard to abate industrial sectors. Nevertheless, leading on the innovations that improve hydrogen transmission pipeline safety would increase the export potential of this technology to those international markets that are contemplating switching from natural gas to hydrogen, e.g., Europe, the Middle East, and Southeast Asia. In the US, it is anticipated that a considerable portion of the hydrogen will be transported via pipelines, including a large network carrying not only hydrogen but also hydrogen blended with natural gas. Therefore, the repurposing of natural gas infrastructure to accommodate hydrogen blends will be crucial for supporting a hydrogen economy. Furthermore, the build out of such pipeline technology will have the potential to be transferred to those international markets that are actively considering fossil-derived hydrogen with carbon capture.

Impacts from Policy Recommendations

As one of the nascent technologies of those BCG assessed, clean hydrogen presents a large market opportunity for US players in global markets. While nascent, the industry starts from a position of strength: the US is endowed with sizable geological storage and pipeline access.

Both the Bipartisan Infrastructure Law and the Inflation Reduction Act boosted the competitiveness of American hydrogen manufacturers, project developers, innovators, and those looking to expand and modernize hydrogen transport and storage. With appropriate standards for emissions leakages, as well as additional “guardrail” regulations, US companies can supply a growing global market for low-carbon and carbon-free hydrogen.

Ensuring US companies can compete and win in the global market for clean hydrogen relies on the federal government putting the right policies in place to stimulate manufacturing and upgrade investments in innovative electrolyzers. As the BCG report indicated, there is a significant market opportunity in several of the hydrogen value chain segments. Stimulating the market with investment and incentives, as well as proper regulations, will take time and money. But this cost will be outweighed by the benefits: emissions reductions, expanding global markets for US businesses, and the job growth that comes from this market expansion.