Report Published October 14, 2021 · 13 minute read

Unforced Errors: How One Simple Fix Could Improve Student Loan Repayment

The Upshot

If you’re worried that lifting the student loan repayment freeze will lead to a massive round of defaults, or that borrowers simply can’t make student loan payments regardless, there is cause for optimism: The government has a plan, and a good one. The current student loan system offers repayment options that vary with earnings—called income-driven repayment plans (IDRs). They operate like federally backed insurance. When borrowers can’t make a payment due to low earnings, they don’t have to. Their balance carries forward, and they resume payments when their earnings allow for it. If they haven’t paid off their loan after 25 years, their balance is forgiven. This is a well-designed system that makes borrowing for college less risky—high earners pay their loans off quickly, and low earners get a break.

So, what’s the problem? The problem is people aren’t using it. Why? Because the current system makes it as hard as possible to enroll and to stay enrolled. At present, borrowers are automatically defaulted into the “fixed” repayment plan, which offers none of these protections and leads to the highest loan default rates. This is an unforced error and is bad for everyone—taxpayers and borrowers alike.

But there’s a clear fix: Make the best plan (for everyone) the automatic and only option. Get rid of the other options. Automatically deduct payments when earnings are high and leave borrowers alone when they are low. Don’t put the onus on borrowers to navigate a complicated system. Here’s what it will take:

(1) Make IDR the only plan, with an option for borrowers to pre-pay; and

(2) Make repayment automatic through withholding by linking loan information from the US Department of Education to the US Department of the Treasury.

And here’s the best part: All the evidence we have suggests that if we do this, student loan defaults will go down, and repayments to the government will go up. The rare policy win-win.

Narrative

The biggest problem contributing to the student loan dilemma also has the easiest fix: simply change the way in which loans are repaid. “Free” college is a worthwhile discussion, as are the rising cost of college and a reconsideration of need-based grant aid. But, holding those costly issues aside, small changes in how and when borrowers repay hold enormous potential to ease debt burden and increase repayments.

Like any investment, the decision to go to college is not without risk. Most of the time, that decision pays off—yet even when it does, the reward is not immediate. Earnings are, unsurprisingly, the lowest and most volatile right after leaving school. When graduates enter the labor force, it takes time to find the right fit. This is a good thing. We want workers to have the freedom to experiment to find the right path. But earnings volatility has big repercussions for repaying student loans, which come due quickly.

The vast majority of borrowers are enrolled in what is known as the “Standard” student loan repayment plan, which is the one they are defaulted into if they take no active steps to switch. Under the “Standard” plan, the sum of your loan balance plus interest is divided into 120 monthly repayments starting six months after leaving school. That means borrowers’ first payment is the same as their last payment, 10 years later. Are earnings six months after college the same as 10 years later? No, not even close. IDR presents a more logical course of action by letting repayment levels vary with earnings, which makes monthly payments more manageable to borrowers of any income level. Yet a surprisingly low percentage of borrowers are currently using this option—and many don’t even know it’s available.

The Congressional Budget Office (CBO) took stock of the student loan portfolio in 2017 and found that only 24% of undergraduate borrowers were enrolled in one of several IDR plans already available under current legislation.1 Consider the newest version, the Revised Pay As You Earn (REPAYE) plan. Under this plan, borrowers owe a monthly payment of 10% of their discretionary income after subtracting 1.5x the poverty line. That means if they earn less than 1.5x the poverty line, after some deductions, they owe nothing, though interest continues to accrue. If they earn a lot, they owe no more than they would under the Standard plan. Moreover, student loans are rarely dischargeable under bankruptcy, yet unlike under the Standard plan, IDR borrowers are eligible for forgiveness after 20 or 25 years. These protections work like insurance, and they suggest that just about everyone should be in IDR, as everyone is at risk of missing a payment, and many might benefit from forgiveness after years of making payments on their student loans. There’s an obvious reason why so few borrowers are enrolling in what is the best choice, and it’s called “choice architecture.”

Choice architecture refers to the way choices are presented. In this case, students are offered a bevy of loan repayment options: Standard, Graduated, Extended, Income-Based Repayment (IBR), Income-Contingent Repayment (ICR), Pay As You Earn (PAYE), and REPAYE. To change out of the Standard plan, borrowers have to affirmatively contact their servicer, and to enroll in an IDR plan, borrowers have to show proof of earnings, which then need to be recertified every single year. These hurdles simply deter borrowers from enrolling in a plan that benefits both them and taxpayers. Behavioral economics has taught us that when people are faced with complex choices they want to avoid, they often do nothing. In this case, that means they get the default option: the Standard plan. For nearly all borrowers, that’s the worst possible choice. We ran a lab experiment to make this point, and to further demonstrate how the federal government can set borrowers (and itself) up for success. Here’s what we found.

The Experiment

We recruited 542 undergraduates from Georgia State University, by all accounts a very representative institution, to take part in a lab experiment. We copied the Department of Education’s “Student Loan Exit Counseling” website, which students are required to take upon leaving school.2 Exit Counseling tells students about loans and repayment options and tells them what they will owe under each plan. For the 154 students in the main portion of the experiment, we made two changes.3 First, we told some students what recent grads like them earn. Second, for others, we changed the default option from Standard to REPAYE (the most current IDR plan).

To make sure they didn’t just hit buttons, we incentivized the experiment to mimic the real world. We told students they would receive annual “earnings” every “year” for 20 “years.” Their annual “earnings” would be a random draw from what recent college grads typically earn. We then told them that they had to make repayments on their loan of $23,000 at the end of each “year.”4 Then they read through the site and chose a repayment plan, just as borrowers do in real life. At the end of each “year” we subtracted their loan payment from their “earnings.” If they had anything left over, we translated that into cash for them when they left the experiment. But, if their earnings in any “year” were too low to make their payment, which depends on which plan they chose, they defaulted. If they defaulted, they lost all future payments and had a penalty of $5 taken from their real dollar take-home pay.5

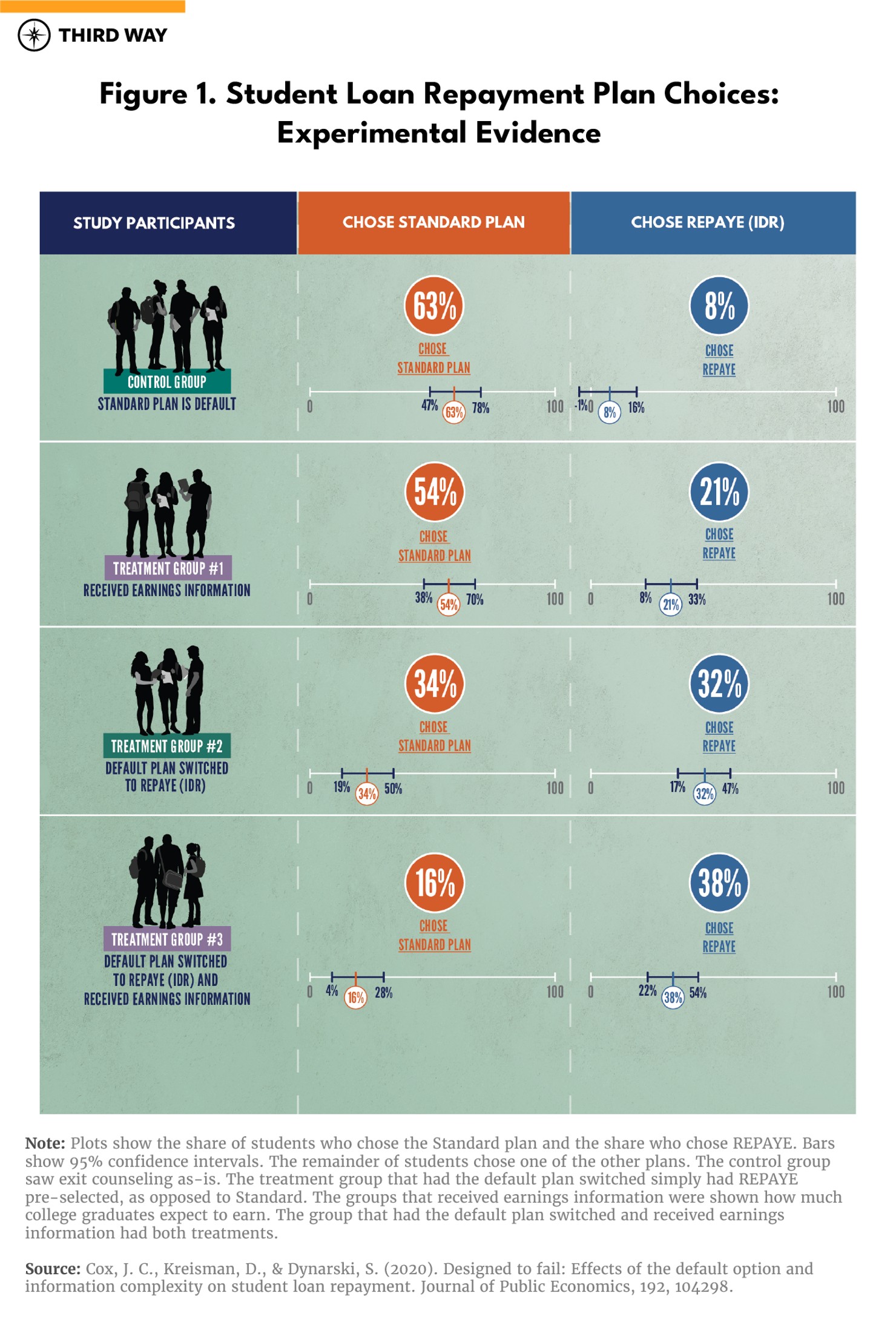

So, the students faced the same tradeoff actual borrowers face. They could choose an IDR plan, like REPAYE, in which they might take longer to repay and accrue additional interest but also get insurance protecting them from a costly default, or they could choose a fixed repayment plan, like the Standard plan, in which they repay quicker if they “earn” a lot, but they also face the risk of default with no protections. Figure 1 shows what they chose.

The control group, which got the exit counseling as it is for actual borrowers, chose the Standard plan in about the same proportion as students do in the real world: 63%. But for the group that had nothing changed other than which plan was pre-selected for them, only 34% chose Standard. Simply switching the default to an IDR plan nearly halved the share of people choosing the Standard plan (a 46% reduction). More, only 7% chose REPAYE when Standard was the pre-selected option, while 32% chose it when we simply switched the default to REPAYE for them.

It turns out that students were also overconfident in what typical undergraduates earn right out of college, which might have led them to discount the need for an IDR plan. But we found that giving them realistic earnings information didn’t have a big effect on their plan choice. The more meaningful mechanism to impact their payment plan choice was switching the default option. Combining earnings information and switching the default plan had the largest effect. But the takeaway is that changing the default changes behavior, for the better.

Fixing Policy Designed to Fail

We aren’t the only ones to notice the importance of simplification to getting better outcomes. A years-long effort to simplify FAFSA applications was based on studies showing that making that application easier increased college enrollment.6 The same is true for default options in general. A host of studies have made clear that the default option plays an outsized role in what we choose. Whether it is enrolling in a 401k plan or signing up to be an organ donor, the default option drives our behavior.7 The simple takeaway is that changing the default option can be a low-cost, high-reward lever for the government—and for students.

Importantly, another recent study shows that borrowers who received calls encouraging IDR enrollment were 21 percentage points less likely to become delinquent on their loans (they also had higher credit scores and were more likely to hold a mortgage).8 Two results are even more salient. First, those who switched to IDR paid down more of their debt despite lower required average payments. Second, many still failed to recertify despite the benefits they already saw. This tells us both that we shouldn’t worry that the government will recoup less under IDR than the Standard plan (in fact, the opposite can be true, though potential forgiveness must be taken into account), and that the system is currently so burdensome that merely enrolling borrowers isn’t enough—we need to actively keep them enrolled.

There’s one more key data point to note: Defaults are highest among those with low debt. This is because many who default didn’t finish a degree, often have low earnings, and are lost in an overly complex system. Yet their credit scores are damaged, their names are sent to collection agencies, and eventually their wages are garnished, proving that the government can take payments directly from paychecks.

The long and short of it is this: Right now, the burden is on borrowers to navigate an overly complex repayment system. All evidence points to this as a policy failure that is costing both students and taxpayers.

Recommendations

1. Make IDR the only repayment option.

This change is not controversial. In fact, the US is behind many other nations in this approach. Australia and New Zealand have fully implemented income contingent repayment plans, and the UK, Canada, Germany, and South Africa feature them prominently, as do Vietnam and Thailand. One common pushback is that some students may want to pay faster than an IDR plan allows. That makes sense, and policymakers can easily provide an option to pre-pay at any time. Another common pushback is that with everyone in IDR, the government won’t recoup payments fast enough. In fact, the CBO has already considered this, noting that the increase in effective subsidy rate to the taxpayer increases not due to lower repayments, but to forgiveness.9 In other words, the current system relies on collecting payments from those who can’t afford to make them. The benefit of IDR over other proposals, like “free” college, is that those who can afford to pay do, and those who can’t don’t. As such, it offers a more sensible approach than the current plan, which makes everyone pay regardless of means or the alternative of “free” college, which would make higher education no-cost even for those who could afford it.

2. Automatically deduct payments from paychecks through withholding.

The main barrier to streamlining IDR enrollment and repayment is not that this policy is unpopular. It is that we cannot agree on the details of implementation, in large part due to a lack of cross-agency cooperation. But that argument doesn’t hold water if you take this into account: Currently, if a borrower defaults on their loan, the entire balance becomes immediately due (this is called “acceleration”). If the borrower still can’t make repayments and comply with the repayment terms, the loan gets sent to a collection agency—which adds additional fees to the balance to cover the collection cost. On top of that, the collection agency can garnish the borrower’s wages. If they are unable to do that (for example, because the borrower is self-employed or unemployed), they can recommend that the Department of Education refer the case to the Department of Justice, which can then sue to collect the loan.10 In fact, federal law requires the Department of Education to request that Treasury withhold money from federal income tax refunds, Social Security payments, disability benefits, and other federal payments to be applied toward repayment of the loan in these circumstances. If all these agencies can work together once a borrower has defaulted, why can’t they do so on the front end to prevent that scenario?

The current system relies on collecting payments from those who can’t afford to make them. The benefit of IDR over other proposals, like “free” college, is that those who can afford to pay do, and those who can’t don’t.

In short, the government already withholds tax refunds and Social Security payments. But it currently only does so after a default. A better alternative would be for the Department of Education to provide Treasury with student loan balances. Based on earnings, Treasury could then calculate payment amounts and deduct through standard withholding. At tax time, any differences between estimated loan payments withheld against actual payments owed could be reconciled, just as they are for taxes. Further, borrowers could then be offered an opportunity to pre-pay at the same time. Treasury could even use the current thresholds that already exist under REPAYE to calculate payments due. Automatic withholding, if done in conjunction with making IDR the only plan option, could result in no defaults, no collection agencies, and no annual income recertification to stay enrolled in IDR. Withholding works for Social Security, Medicare, and income taxes, and in fact, Treasury is already working with the Department of Education to pre-populate FAFSA for future borrowers. Student loans should be next.

3. Handle contingencies and non-standard cases separately.

Just like income tax withholding, there will be many exceptions. For example, poverty lines might be location specific, and some earners have non-standard income reporting, or deductions that may work against required payments. While important, these are exceptions, not the rule, and they can be solved as well. With 45 million borrowers navigating this labyrinthine system, a failure to act with the tools at hand is a failure of government—one that continues to actively harm both students and taxpayers.