Report Published November 6, 2015 · Updated October 3, 2017 · 14 minute read

Understanding SIFIs: What Makes an Institution Systemically Important?

Emily Liner

What is systemic risk, why do we care about it, and what makes a firm systemically important?

For a long time, federal financial regulation focused on protecting the consumer. FDIC insurance keeps customers’ savings safe if their bank goes under, which prevents bank runs. The SEC protects investors from fraud in financial markets. On the state level, commissions monitor insurance companies to ensure that customers receive competitive rates and claims.

Post-financial crisis, the focus of financial regulation has shifted to protecting the financial sector from itself. Systemic risk mitigation is meant to ensure that if one institution drowns in a liquidity crisis, it does not pull other interconnected financial institutions under the water.

Thus, the term “SIFI” was invented: Systemically Important Financial Institutions. These institutions have been deemed so important to the functioning of the economy that special rules and buffers were put in place to (1) reduce the probability of failure and (2) ensure that if they do go down, they go down alone.

No financial institution wants to be a SIFI because it means more regulations and requirements. Moreover, the SIFI designation process invites contention: SIFI designation for banks is under a set of largely objective criteria that banks argue misses important nuances. SIFI designation for non-banks is under a set of mostly subjective criteria that non-banks argue is overly unpredictable and nuanced.

This paper describes who SIFIs are and discusses three contentious issues surrounding them: (1) how rigorous new rules should be, (2) how big is too big, and (3) how non-banks become SIFIs.

Who Are the SIFIs?

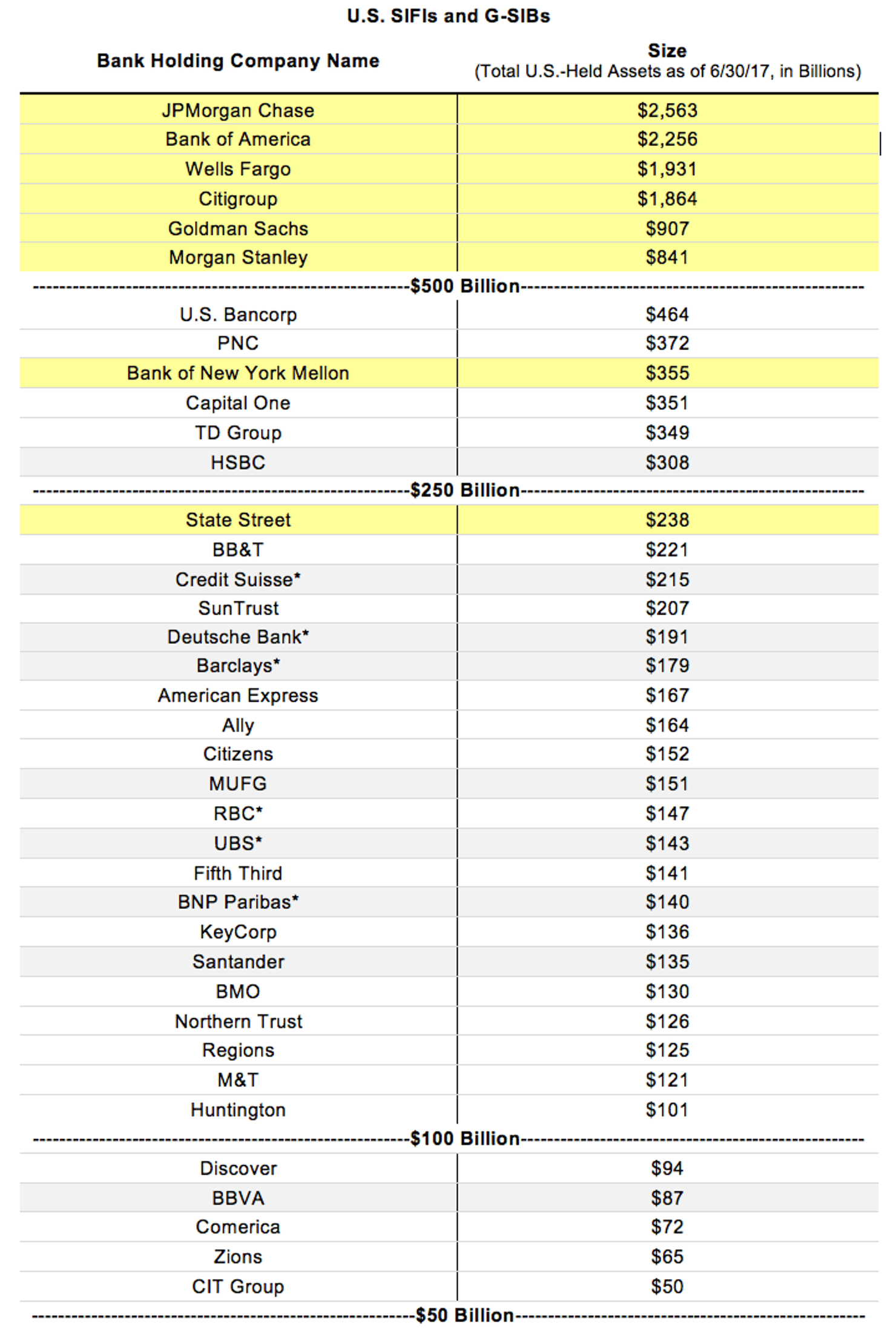

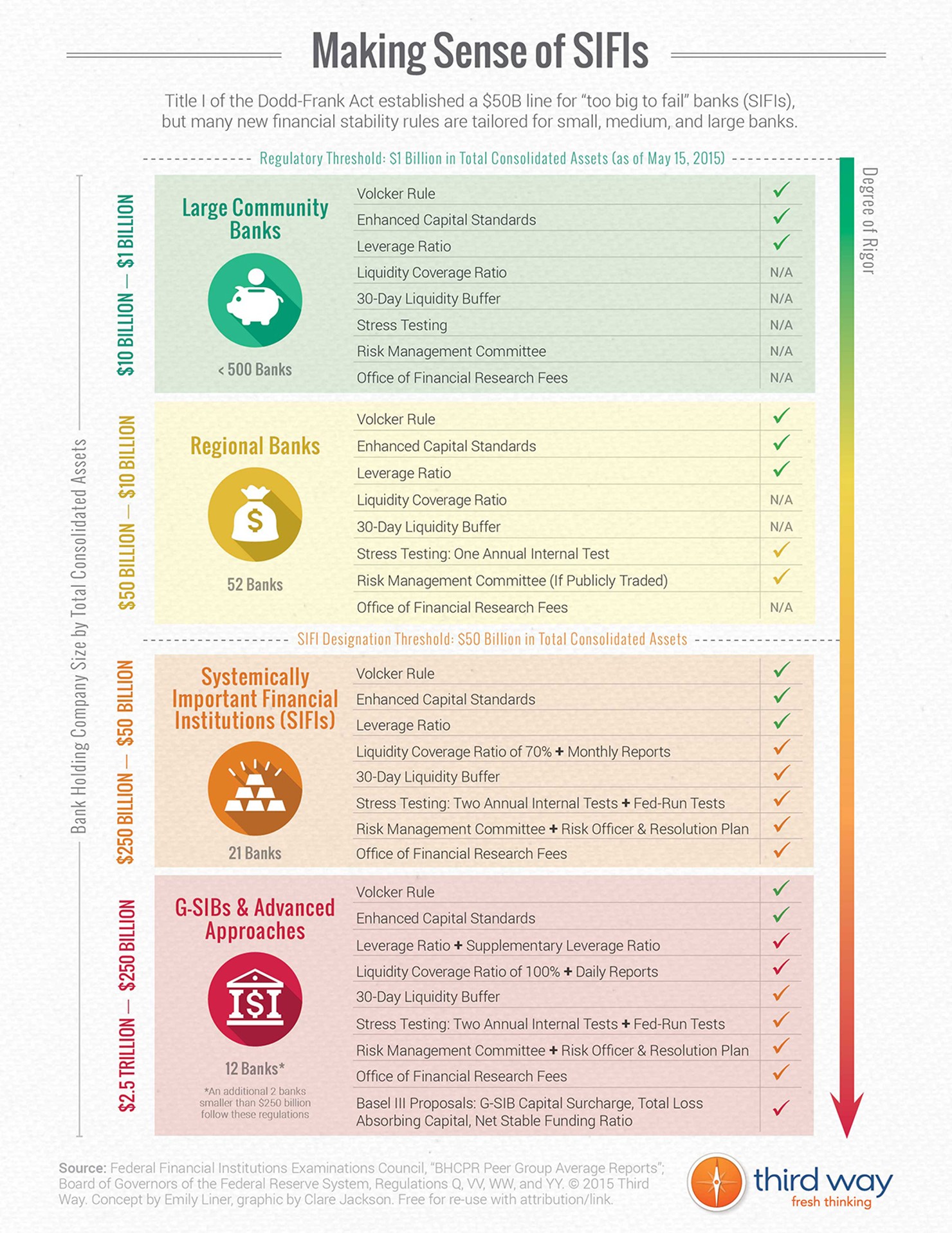

SIFIs are a creation of Dodd-Frank, and any bank with assets above $50 billion is deemed systemically important (savings and loans are not included). These 38 banks must adhere to stricter requirements on capital and liquidity than other banks. They must also go through yearly stress tests and have a plan for orderly liquidation. Pretty simple so far.

Note: The banks in yellow are G-SIBs based in the United States; the banks in gray are G-SIBs headquartered overseas with significant U.S. operations. Banks with an asterisk will be subject to Dodd-Frank stress testing beginning January 1, 2018.

Source: Federal Financial Institutions Examination Council.1

Because the biggest SIFI is about 50 times larger than the smallest SIFI, international regulators have created a special class of SIFIs called Global Systemically Important Banks, or G-SIBs. Compared to regular SIFIs, these banks must maintain even higher risk mitigation requirements.

Whereas the SIFI designation is based completely on the objective measure of asset size and is determined by the United States, the G-SIB determination takes a more holistic approach and is made by an international body. This body, the Basel Committee on Banking Supervision, is an international organization for central banks and financial regulators, and its G-SIB designation supersedes U.S. SIFI designation.

In addition to size, the Basel Committee’s framework looks at four other factors to select the G-SIBs.2 The investment banks Goldman Sachs and Morgan Stanley, for example, are on the list because they do so much business with other financial services companies (interconnectedness), in other countries (cross-jurisdictional activity), and in huge volumes of intricate instruments like over-the-counter derivatives (complexity). The Bank of New York Mellon and State Street made the list due to non-substitutability. They perform unique services that would be difficult for other firms to quickly replace if something happened to them. In this case, these banks specialize in holding customer funds for asset managers, insurers, and other firms, a service known as asset custody.

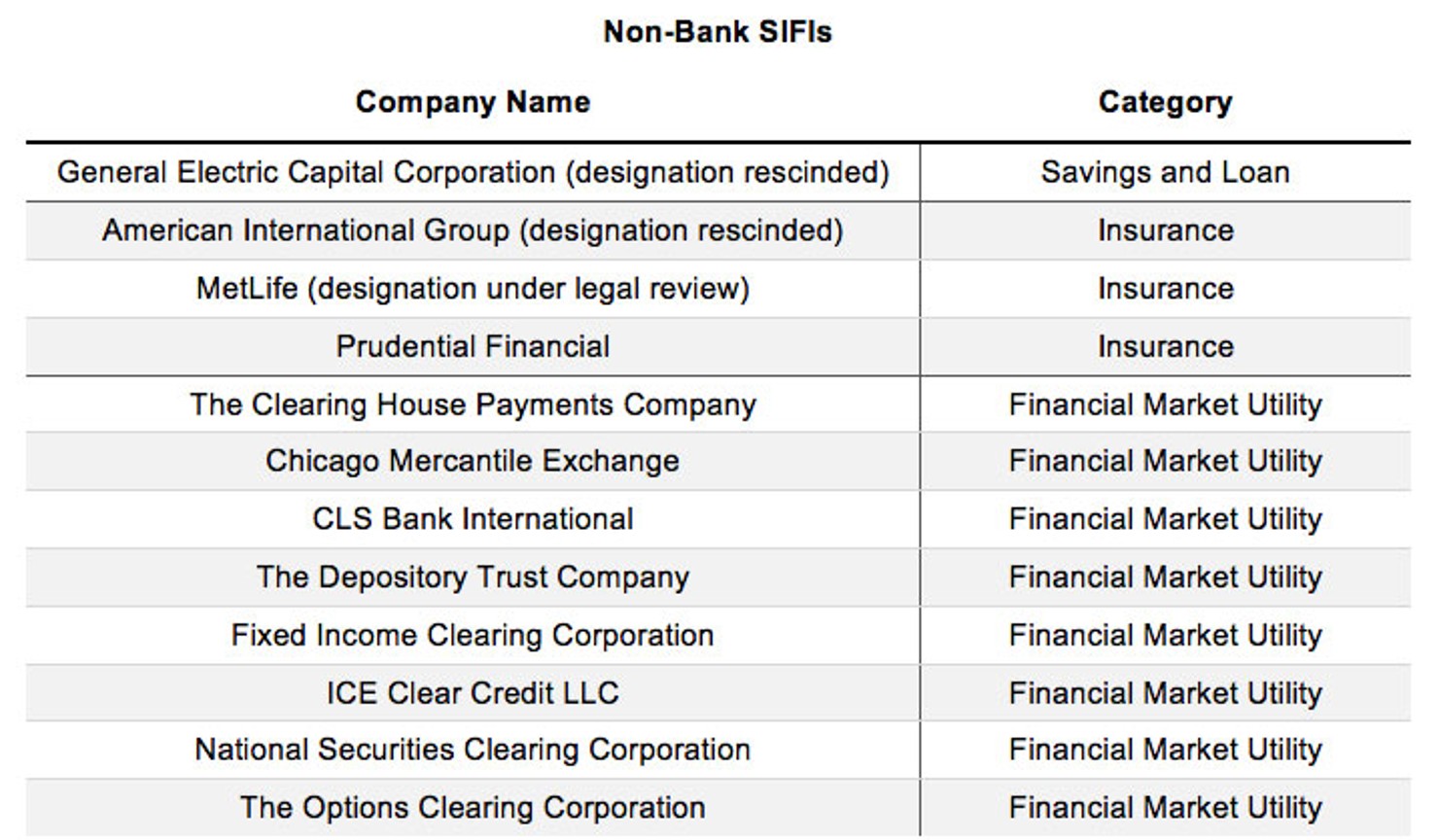

Finally, beyond the 38 banks there are currently nine non-bank SIFIs. Dodd-Frank’s Financial Stability Oversight Council (FSOC) has the responsibility of naming non-bank SIFIs, which it accomplishes with a three-stage review discussed later in this paper.

Source: Financial Stability Oversight Council3

With a very objective threshold for banks, a multifaceted framework for G-SIBs, and a case-by-case approach for non-banks, SIFIs start to get complicated. Thus, the task of naming both bank and non-bank SIFIs has become subject to debate and contention.

Issue #1: How Tough Should the Rules Be?

In general, SIFI firms must hold more expensive assets, amass a deeper equity cushion, undergo resource-intensive stress tests, and prepare complicated contingency plans to prepare for failure. Much of the current debate revolves around where to draw the line for new minimum capital and liquidity standards and if some smaller SIFIs should be exempt from stress tests and living wills.

All banks over $1 billion in size, SIFI or not, have to follow new enhanced capital standards under Dodd-Frank. Enhanced capital standards set a minimum ratio of equity to assets. Equity provides a cushion that grows and shrinks as asset values fluctuate. Regulators have historically used the ratio of total equity to total assets to determine a bank’s amount of leverage. After the crisis, a new ratio was created using risk-weighted assets, to take into account the quality of liquidity of different types of assets on a bank’s balance sheet. For example, a high quality liquid asset like cash or a Treasury bond fluctuates less than assets with more risk and return, like stocks and loans. SIFIs have more stringent requirements for these two capital standards than other financial institutions.

For the eight global systemically important banks there is a third standard called the G-SIB surcharge. This is a requirement for the eight globally important banks to hold even more capital than the other SIFIs. The idea behind the G-SIB surcharge is that “too big to fail” banks must either build up more capital (to reduce the likelihood of failure) or shed assets (to get smaller). When the Fed finalized the G-SIB surcharge rule earlier this year, it decided to make the U.S. requirements stronger than the global standard.4 The Fed also recently finalized another rule just for the G-SIBs that will require them to hold a certain amount of debt to serve as the second line of defense after the equity cushion. This rule, called Total Loss Absorbing Capacity (TLAC), is also a part of the global Basel Committee protocol.5

Liquidity requirements refer to the ratio of assets to liabilities at a bank. With the Liquidity Coverage Ratio, regulators want to make sure that SIFIs can fund their cash flow needs with internal assets for at least 30 days. That way, the firm will not suddenly find itself unable to meet upcoming expenses, as happened in several bank failures during the crisis. Global regulators are also working on an additional rule, the Net Stable Funding Ratio, that measures liquidity over a 12-month period. The goal of the NSFR is to nudge banks toward long-term, rather than short-term, funding sources.

Stress tests ensure that SIFIs have enough capital and liquidity to withstand potential worst-case scenarios. The hope is that these precautions will prevent SIFIs from taking on excessive risk, so that they are not in a position to fail and take down the system. In September, the Fed announced that banks with less than $250 billion in assets would be relieved of the qualitative portion of the annual Comprehensive Capital Analysis and Review (CCAR) stress test.6

If failure is imminent, then Dodd-Frank gives regulators the ability to contain and close down large, complex financial institutions. The Fed and FDIC keep resolution plans, also known as “living wills,” on file to understand how a SIFI would resolve itself if it failed. And the government uses Orderly Liquidation Authority to carefully dismantle the firm so its losses don’t affect others.

Non-SIFIs can avoid many, but not all, of these burdens. Dodd-Frank imposes new, graduated requirements on all banks bigger than $1 billion, and the rules become more stringent as bank size increases. The graphic “Making Sense of SIFIs” demonstrates the additional regulations that kick in at the non-SIFI $10 billion level and how they accelerate at the $50 billion and $250 billion SIFI levels.

Issue #2: How Big Is Too Big?

Given that no bank wants the burden of being a SIFI, the heart of the debate over SIFI designation is defining what “big” is. Some feel that the $50 billion threshold set by Dodd-Frank is too low, since it captures some regional banks who steer clear of investment banking and trading. Indeed, during normal times, the failure of a large regional bank can generally be contained because these banks are less complex.

Others argue that in bad economic times, the collapse of a large, regional bank could have a systemic impact—particularly if that bank is heavily exposed to derivatives and securities that all move in the same negative direction in a bad market, which could impede the firm’s ability to meet its obligations to other financial institutions.

Given the current debate over asset size, a variety of different numbers for the threshold have been suggested:

- $50 billion: A powerful group of supporters stand by the original threshold in Dodd-Frank, though former Representative Barney Frank has suggested indexing it to inflation or GDP growth.7

- $100 billion: Daniel Tarullo, the lead Fed Governor on regulatory issues, suggested in a 2014 speech that stress tests may be unnecessary for banks between $50 and $100 billion in size.8 That would relieve nine banks, leaving 24 in the ranks of the SIFIs.

- $168 billion: One idea from progressive economist Simon Johnson is to peg the threshold to one percent of GDP (currently $16.8 trillion), which would capture 15 banks. Since it is not based on a fixed number, this metric can move as the economy changes.9

- $250 billion: The Fed currently uses $250 billion as the starting point for tougher leverage and liquidity requirements, which affects 13 banks.

- $500 billion: Recent Republican Senate legislation would increase the asset threshold tenfold, slashing the number of automatic SIFIs from 33 to six. Banks under $500 billion could still be designated on a case-by-case basis.10 This dramatically raises the threshold but then adds some subjectivity to the designation that could potentially capture smaller banks.

Another possibility, as proposed by H.R. 3312, the Systemic Risk Designation Improvement Act and a new companion bill in the Senate, S.1893, is to change the hard asset line to an activity-based assessment. Proponents believe that this would be more consistent with the Basel framework while maintaining the spirit of Dodd-Frank. Others, however, are concerned that this would make the process of SIFI designation more burdensome and curtail regulators’ ability to exercise enhanced oversight over large national banks.11

Issue #3: What Makes a Non-Bank a SIFI?

Since Dodd-Frank went into effect, the number of non-bank SIFIs has gone from 12 to nine. Right now, one is an insurer and eight are financial market utilities.

It is this designation for non-banks that has invited much of the scrutiny on Capitol Hill. Unlike banks which have a clear demarcation, non-banks go through a three-stage process on the way to SIFI designation. Along the way, the criteria for SIFI designation become more and more of a judgment call.

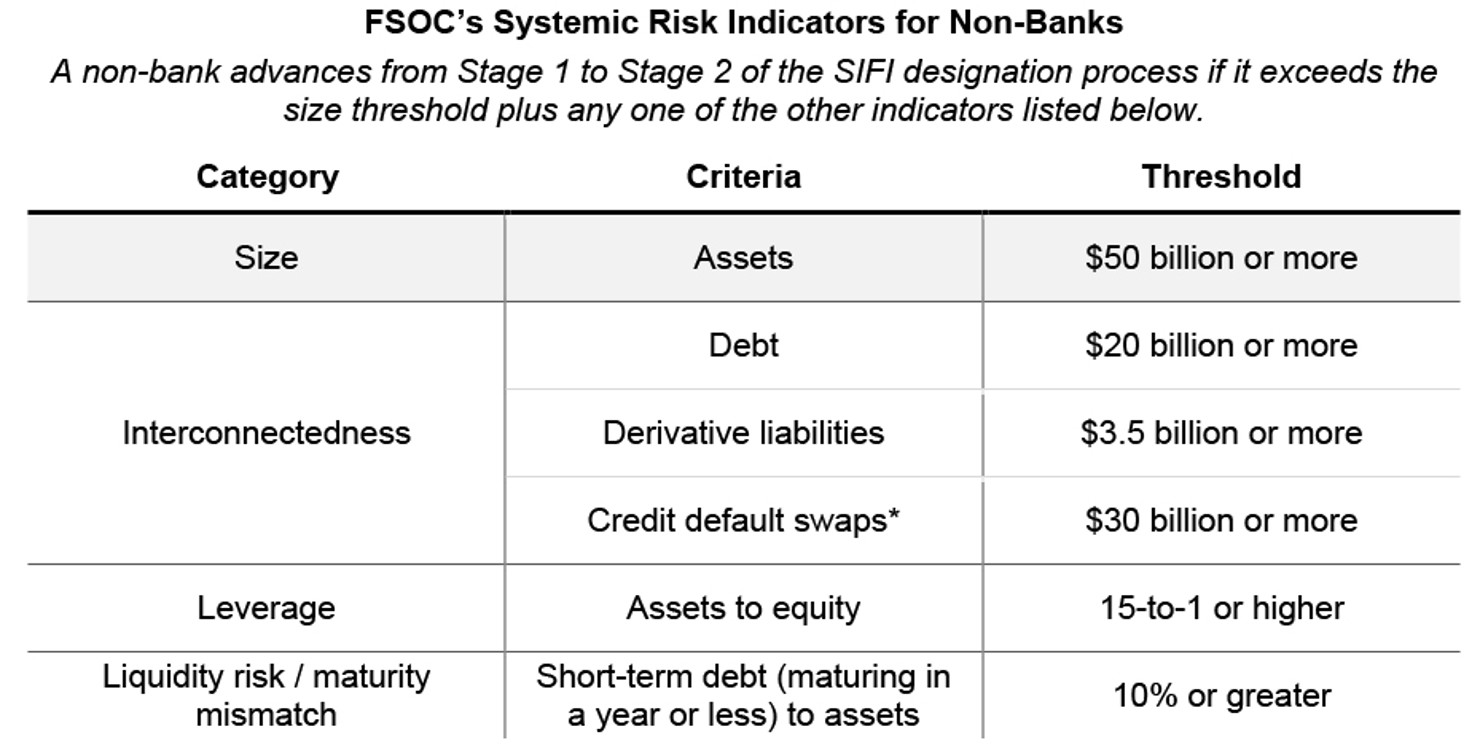

In Stage 1, FSOC analyzes whether a firm should be put under consideration based on size plus at least one other indicator of interconnectedness, leverage, or liquidity risk from the chart below. So, for example, a non-bank with more than $50 billion in assets and derivative liabilities greater than $3.5 billion would advance from Stage 1 to Stage 2.

*Note: FSOC considers the volume of credit default swaps in which the non-bank is listed as the “reference entity” (the firm that is the subject of the swaps rather than one of the counterparties).

Source: 12 CFR Part 1310.12

The annual and quarterly reports that firms submit to the SEC contain almost all of the information needed to deduce whether FSOC would pass a non-bank from Stage 1 to Stage 2. FSOC, however, has the authority to conduct a Stage 2 analysis of a firm that does not pass the Stage 1 thresholds if there are other firm-specific thresholds that it deems could pose a threat to financial stability.13

In Stage 3, FSOC may look at two standards to make a final SIFI designation. First, could the firm’s material financial distress pose a threat to the financial stability of the United States?14 AIG, GE Capital, MetLife, and Prudential were evaluated under this standard. FSOC could also use a second standard, which asks, is the firm’s nature, scope, size, scale, concentration, interconnectedness with the financial system, and mix of activities so important that, regardless of its size, failure would cascade throughout the world of finance?15 FSOC has not used the second standard in any of its determinations so far. To industry, the second standard is less vague, and therefore more predictable, than the first standard.

The non-bank SIFIs fall into the following three types of institutions:

Savings and Loan SIFIs: The $50 billion SIFI bank threshold does not apply to savings and loans, even though they resemble banks in many ways. This means that large savings and loans are not subject to the higher liquidity requirements, Fed-run stress tests, and risk management rules that banks over $50 billion must follow. The only way to make a large savings and loan comply with the same rules as an equally large bank is to designate it as a non-bank SIFI, so FSOC made the $508 billion GE Capital a SIFI in 2013. After GE Capital was broken up, FSOC agreed to rescind its SIFI designation in June 2016.16

Insurance Company SIFIs: In general, the “plain vanilla” insurance business model is not very risky. A no-frills life insurance company goes to the capital markets to invest in securities like long-term Treasury bonds so that it has a source of cash matched to a policy that expires in 20 to 30 years. Then came AIG and its Financial Products division, which got into trouble by acting like a trading firm instead of an insurance company. So far, AIG, MetLife, and Prudential have been named SIFIs. Although their portfolios are nowhere near as risky as pre-crisis AIG, it is difficult for the industry to escape the hangover effect of AIG’s bailout. But because AIG has reduced its size to half of what it was before the crisis, the FSOC decided to rescind its SIFI designation in September 2017.17 MetLife is currently contesting its designation in the court system. A U.S. District Court judge ruled in MetLife’s favor in March 2016; that decision was appealed by the Obama Administration and is now under consideration by the U.S. Court of Appeals.18

Financial Market Utility SIFIs: Also known as central counterparties or clearinghouses, there are eight Financial Market Utility (FMU) SIFIs. FMUs mitigate counterparty risk—the risk that one side or the other cannot hold up its end of a trade. Instead of the seller and buyer directly swapping with each other, the FMU provides payments from special accounts in the counterparties’ names, and it provides securities from a central repository. FMUs stand in the middle of trillions of dollars of counterparty exposures, so it is critical that they have enough liquidity to clear all of the transactions they handle. Therefore, they are now eligible to receive emergency loans from the Federal Reserve System. To minimize the chance they would need to ask for a loan, they are now required to hold enough internal funds to cover the potential default of their two biggest customers.

Conclusion

If SIFI designation is so burdensome, then why does it exist? The reason is to end “too big to fail.” No one wants to be in another situation in which some firms are saved (AIG), some are hitched to a new parent (Bear Stearns and Merrill Lynch), and only exceptional firms are allowed to fail (Lehman Brothers). The SIFI system may not be perfect, but going forward, firms should be less likely to fail—and if they indeed deserve to fail, they can do so without taking down the rest of the system.