Report Published October 7, 2020 · 12 minute read

Make Medicare Coverage Choices Easy

Takeaways

Americans often have choices when it comes to their health care coverage, but the process is confusing and frustrating. Medicare beneficiaries, in particular, face a more complicated set of choices and have more factors working against them when it comes to making a good choice for themselves.

Choosing a health plan doesn’t have to be a bad experience. Policymakers can help consumers with three key steps that involve the public and private sectors:

1. Enable broader use of personal Medicare data to customize decision support.

2. Boost federal support for programs that provide one-on-one support for beneficiaries.

3. Invest in research to improve health insurance literacy and inclusiveness with decision support.

Does my health insurance plan cover COVID-19 care? What will it cost me if I have diabetes? Are my doctors in-network? Every day, Americans have questions like these and more about their health insurance coverage, but getting answers is often hard. Some information is couched in jargon, some is hidden, and other information is just not available at all.

Health care is far too personal and important for consumers to fly blind. For example, what if an app on an individual’s phone alerted them during an open enrollment period that they could save money and get better care for a newly diagnosed health condition with a different plan? Ideally, it would prompt them to check out options and get better coverage for their needs.

Getting help choosing a health plan should be that easy. With open enrollment season starting on October 15 for Medicare and November 1 for the Affordable Care Act exchanges, it’s a good time to consider how to improve people’s experiences with choosing coverage. This report explains the challenges consumers face when choosing a plan, presents a framework for the public and private sector in helping consumers, and proposes three key steps for improvement with a focus on Medicare beneficiaries.

Why is choosing a health plan so hard?

Getting the right health plan that fits your budget and meets your health care needs is great when everything goes right. But so much can go wrong.

Take Monique, 66, who supplements her Social Security check with a part-time job while she stretches every dollar. When Monique turned 65 and joined Medicare, she was overwhelmed with the choices for coverage. With 28 Medicare Advantage plans, original Medicare, and 28 choices for prescription drug coverage, she selected a Medicare Advantage plan with the lowest premium.1 Monique did not consider that her medications would be cheaper if she spent a little more in premiums to get a lower copayment. Not wanting to get overwhelmed again, she stuck with her plan again at age 66 because it was familiar—even though it meant stretching her dollars a little further to pay for the medicine and skipping doses.

That story of someone like Monique choosing a health plan is not unusual. In fact, this scenario typically happens based on behavioral science. Several factors can throw individuals off choosing the right plan for themselves:

- Choice overload is a principle that explains how too many choices can be overwhelming. It can lead individuals like Monique to either make a uneducated choice—or no choice at all. Research has shown additional choices that are complex, uncertain, and rushed do no good.2 Instead, a person facing choice overload often makes random and uninformed choices—what’s worse, people are typically unaware that they made a poor choice.3 One study of Swiss health care consumers who have health plan choices similar to Americans in Medicare and the ACA exchanges showed that they became less likely to switch plans as their options increased.4 As the health care economist Austin Frakt recently wrote, “too much choice without enough guidance can be overwhelming.”5

- Health insurance literacy measures the understanding of concepts involved in health coverage. One study found that only 9% of consumers understood the four most basic components of health insurance: premiums, deductibles, maximum out-of-pocket costs, and co-insurance.6 For consumers who have low health literacy, it’s a challenge to figure out how, for example, higher premiums might come with lower copays. With lower levels of health literacy, people are less likely to make the choice they intend; this problem gets worse as one ages.7 Health literacy is an even bigger problem for people of color. For example, Latinx people are half as likely, on average, familiar with health insurance terms.8 As a result, they are less likely to take advantage of the savings from Medicare Advantage plans.9 Literacy challenges are compounded for older, disabled, and low-income Americans who lack computer skills or access to the internet, which is a common way to overcome them.

- Status quo bias is the principle that explains the tendency for people to accept current choices and avoid making new decisions.10 For example, Monique became more settled with her initial health plan despite her first choice not being the best one for her.11 This problem is common and affects all kinds of people. A study of the retirement accounts of university faculty found that they nearly always stayed with their initial choice of investments regardless of better investment opportunities.12

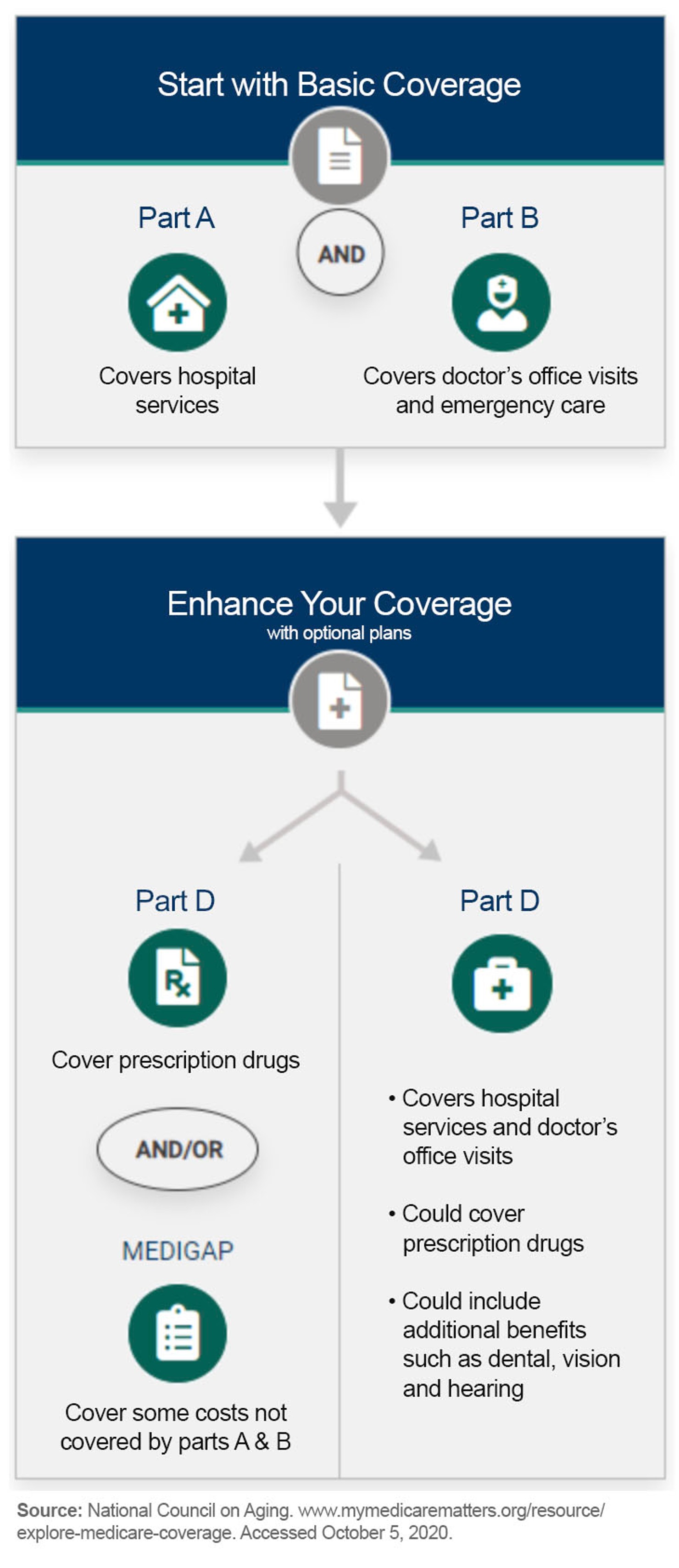

These are just a few of the many problems associated with making good choices about health care.13 They are especially pervasive in Medicare given its extra complexity with Parts A, B, C, and, D and supplemental plans called Medigap, each with their own set of features and coverage options (see chart below).14 In addition, some Medicare beneficiaries also qualify for Medicaid benefits, which can vary by state. Because of this, competition in health care insurance markets is not optimal. Consumers regularly leave money on the table because of the complexity.15 They may not be aware of new supplemental benefits for people with chronic diseases that can include in-home personal care, meal assistance, and pest control that vary greatly between plans.16

For people like Monique and all other Medicare beneficiaries, the consequences of a poor choice can be far-reaching. It can impact the cost and quality of their health care—potentially for the rest of their lives. For this reason, it is even more important to provide Medicare beneficiaries with support in making their choice.

Who is Trying to Make Choosing Easier?

Making it easier for consumers to choose the right health plan requires both high-tech and high-touch services. High-tech services include sophisticated technology that can analyze a person’s specific health data as well as make complicated health care terms easy for a consumer to understand. High-touch services include actual people who work with consumers, helping them sort information and decide.

The public and private sectors both have distinct, but symbiotic roles in facilitating consumer choice. The public sector role focuses on making information available and reliable for everyone. Alongside that, the private sector deploys the information to be most helpful to people. These actions break down as follows:

Public Sector Roles

- Collect and disseminate reliable information. In Medicare and the ACA exchanges it runs, the federal government collects and distributes information of all plans available in a region. This information is broadcast through its websites, Medicare.gov and Healthcare.gov, and includes information such as premiums, out-of-pocket costs, and provider networks. Yet, even such basic information has its challenges.17 For example, accurate lists of provider networks are often not up-to-date due to a variety of technical challenges.18 Public and private initiatives to improve this information are well underway.19

- Ensure transparency. Medicare regulates the information that health plans and insurance agents can use to sell private Medicare coverage. The guidelines help ensure accurate and non-discriminatory information about a plan’s costs and benefits as well as about Medicare in general.20

- Technology- and human-based support. Medicare provides support through a variety of means including an introductory pamphlet, “Medicare and Me,” a toll-free helpline, and information about each private plan option online. Federally funded state health insurance assistance programs (SHIPs) have a specific responsibility to counsel Medicare beneficiaries about health plan choices but cannot recommend specific plans. And the website MyMedicare.gov allows beneficiaries to see their health care history online based on payment claims from doctors and hospitals.

Private Sector Roles

- Customize information. Private health insurance brokers and online shopping services and apps sort public information based on the individual needs of consumers. For example, they can estimate the projected health care costs for a consumer based on different enrollment options. In contrast, the public sector Medicare.gov has that feature only for the prescription drugs taken by a given patient.

- Educate and raise awareness. Although advertising by health plans and insurance brokers is designed to benefit them, it also serves to raise public awareness about the availability of options. These efforts also educate Medicare beneficiaries on the way Medicare works. For example, to sell a Medicare Advantage plan, an insurance broker may need to educate beneficiaries about the limits on benefits in traditional Medicare in contrast to the expanded benefits under Medicare Advantage.

- Invest in innovative technology. Online shopping services and apps for health plans like eHealth, HealthSherpa, and GoHealth as well as decision support tools like Picwell are investing in advanced technology like artificial intelligence to provide consumers with highly customized recommendations and savings.21 These new tools can radically reduce the complexity of choosing a health plan by modeling an individual’s health costs based on their specific health care needs and financial preferences. For example, eHealth has found that its drug cost comparison tool potentially saved $782 on average for users who entered their drug list while shopping for a Medicare Advantage plan.22 The idea of maximizing customer benefits is driving additional private investment by online brokers in decision support technology. So too is the demand for online services as a result of coronavirus pandemic. Most older Americans are now using online resources for health information and communication.23 As computer literacy grows among this age group, private sector investment will be critical in meeting their needs.

What more needs to be done?

Policymakers can improve people’s experiences with choosing coverage—starting with those eligible for Medicare—with measures built on the strengths of the public and private sectors by taking three key steps:

- Enable broader use of personal data from MyMedicare.gov. Medicare maintains health care records for each beneficiary, including data on beneficiaries’ health conditions, tests, procedures, and medication lists. This information is extremely helpful to know and understand when selecting a health plan. Today, however, Medicare has a cumbersome process for individuals who want to gain access and transfer that information to entities like SHIPs and online insurance brokers.24 Instead, beneficiaries should be able to authorize a trusted, regulated organization to access the data on their behalf.25 This process would be similar to the way HHS allows organizations to assemble a patient’s complete electronic health record among pieces held by multiple providers.26 Federal law should require organizations that access the data to keep the data secure through technology like encryption. No one would be able to see the data unless the beneficiary makes an explicit, informed decision to share their data. Any organization receiving the data would have to abide by those same terms. Furthermore, any SHIP or insurance broker receiving the information would have to get an explicit, informed agreement from the beneficiary about the data use. The agreement would spell out, in plain language, the limitations of the organization’s services including whether it makes recommendations about health plans and the kind of financial relationships it has with health plans. That way, beneficiaries would know the potential biases of any organization that uses their data to help them decide on a health plan.

- Boost support for SHIPs. Federal SHIP funding has not kept up with the increasing demand for SHIP services, even though they are a critical and objective source of advice for beneficiaries. SHIPs also solve problems for beneficiaries as they try to navigate the complexity of Medicare. Congress should increase the program’s funding to $75 million (from the current level of $52 million) over the next two years.27 That would bring funding levels to where they were ten years ago, adjusting for increased demand and inflation.28 It would also enable expanded outreach to communities of color where health disparities are magnified by the lack of effective decision-support. Congress should also provide a technology budget for SHIPs so they can have access to innovative decision support tools.

- Invest in research to improve equity and effectiveness of decision support. Congress should set aside funding in the HHS budget for behavioral economics research to evaluate interventions that can improve health insurance literacy for everyone—with a special emphasis on reducing racial and ethnic disparities in health insurance literacy. While the problems with health insurance literacy are well established, evaluations of solutions have not received the same attention.29 Such research can reveal where innovative techniques are customizing information to individuals and where new approaches are needed.

Conclusion

Choosing a health plan should not be a frustrating experience. Policymakers have a big opportunity to help consumers if they take a series of steps now. The evolution of high-tech and high-touch decision support requires a long-term, consistent interplay between the public and private sector. Private sector innovation can raise the level of service for all if policymakers collaborate with the private sectors and enable the use of data. By setting policy with explicit roles for the public and private sectors, innovative decision support can finally make choosing Medicare coverage easy.