Report Published October 30, 2015 · Updated October 30, 2015 · 11 minute read

Everything in Moderation: Why the Economy Needs a Little Inflation

Emily Liner

Quick—can you guess the U.S. inflation rate?

Business Insider asked its readers to try this two years ago, when inflation was about 1.5%. The results were stunning: the average respondent guessed that inflation was 9%, and 1 in 5 thought it was in the double digits.1 A Pew poll around the same time found that 8 in 10 Americans claimed that inflation is a “very big” or “moderately big” problem.2

Inflation is a problem in today’s economy—but for the opposite reason that many think. Lackluster demand and falling oil prices have pulled inflation all the way down to 0%, according to the latest Consumer Price Index (CPI) estimate.3 Zero inflation may sound like a good thing to anyone who lived through the ’70s and ’80s, but economists think that is too low. They would rather inflation be closer to 2%, which is the official medium-term inflation target of the Federal Reserve.4

Why would the Fed want 2% inflation when rising prices are so unpopular? This memo explains what inflation is and why a little bit of inflation is a good thing.

What Is Inflation?

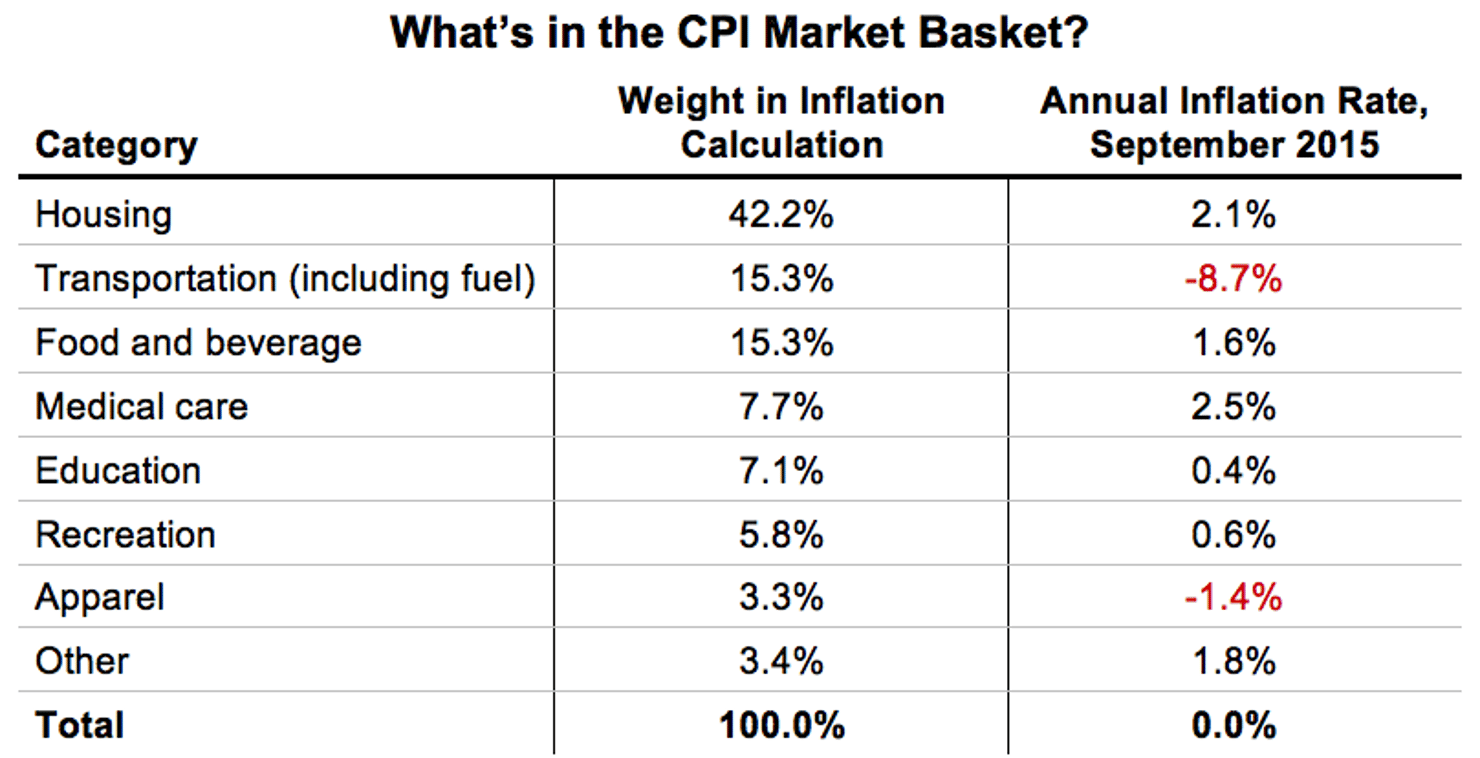

The inflation rate tells us whether prices are rising, and by how much. Economists measure inflation by tracking the prices of a specific basket of goods and services from month to month. (See the glossary at the end of this document for the different types of inflation indexes.) The market basket used to calculate CPI contains more than 200 categories of products and is comprised not only of items in the grocery store, like milk and eggs, but also expenses like rent, health care, and tuition. These items are weighted to reflect their share of the consumer economy. Sometimes certain categories are taken out completely, such as energy and food, because their prices are so volatile. Inflation occurs when the aggregate prices of the market basket rises over time.

Source: U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers (CPI-U)5

Americans fear inflation because of the havoc that it wreaked during the ’70s and ’80s. A furious cycle of rising prices and wages sent waves of uncertainty and unease throughout the economy, dragging down growth and employment. This was particularly troublesome for people on fixed incomes, like a pension, annuity, or interest payments. And for workers whose wages didn’t rise as fast or, worse, lost their jobs, their purchasing power quickly evaporated.

Inflation was high and volatile until Paul Volcker became Fed chairman and raised interest rates to bring inflation under control. This led to short-term pain in the form of a recession, but in the long-term, it launched a new era of low, stable, and predictable inflation known as the Great Moderation.

Source: U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers (CPI-U, frequency: annual, units: percent change from year ago), retrieved from Federal Reserve Bank of St. Louis Economic Research (FRED)6

Why Is Some Inflation Good?

Think of the national economy as a massive boulder. If you have to push it from a standstill, it’s going to take a lot of force. Modest inflation helps move the economy forward by giving it a little momentum. When we expect inflation, it gives us an incentive to increase spending and investment, giving the economy a little bit of wind at its back. As rising prices of consumer products gently increase revenue, firms are apt to either hire more people or give them raises. A company with millions in the bank may spend big on a new plant that it might have otherwise delayed. In moderation, inflation creates a virtuous economic cycle in which consumers have an incentive to purchase, businesses to invest, wages to rise, and employment to expand. Just as modest inflation helps growth, so can growth push upward on inflation. Often, the existence of inflation is a sign that businesses are hiring and consumers are spending.

Conversely, when the economy is struggling, inflation gives the Fed ammunition to fight recessions. When the economy slows down, the Fed responds by lowering nominal, or stated, interest rates. This also has the effect of lowering real interest rates—the actual cost to borrow after adjusting for inflation. With a little inflation, it’s possible for real rates to go slightly negative, which gives the economy a little extra stimulus. How? With a negative real interest rate, depositors incur a small loss for keeping money in the bank, so there is an incentive to spend or invest instead. But we don’t want nominal rates to go negative, because then banks would have to charge depositors interest on their savings, which would lead people to start cashing out their deposits. A little inflation allows nominal rates and real rates to straddle zero, giving us a little benefit for changing our behavior without completely reversing the incentives.

Additionally, the existence of inflation during a downturn can help employers avoid layoffs. Think about it this way: If you own a business and sales start to dip, you’re faced with a dilemma: Do you cut wages or lay off workers? Employers know how tough it is to present workers with an actual cut in their paychecks. It’s just bad for worker morale. Instead, though, employers can freeze wages or raise them at a rate slower than price increases. In nominal terms—plain, unadjusted dollars—workers don’t get a pay cut. But in real terms—adjusting for purchasing power—workers are getting a small pay cut, allowing businesses to recover. If inflation were zero, that small, real wage cut just wouldn’t be an option. Employers would lay off more people, unemployment would rise higher, and climbing out of the downturn would be even more difficult.

Just as inflation should ideally be moderate, it should also be stable and predictable. Here’s why. Whenever you take out a loan or open a savings account, the interest rate you’re given factors in the expected rate of inflation. If inflation exceeds the rate factored into the loan, borrowers win and lenders lose. That’s because the previously agreed-upon interest payment becomes cheaper over time, in real terms. On the other hand, inflation that is lower than expected punishes borrowers and rewards lenders, as interest payments grow more expensive than anticipated. This dynamic between lenders and borrowers is why stable, predictable inflation is so important. When borrowers or lenders can win or lose big—because of unpredictable inflation—defaults are more likely and uncertainty looms large over the economy.

What Makes Deflation Worse Than Inflation?

There’s a high school physics term that explains why it’s so hard to get something that’s not moving—like a great, big boulder—to start moving: inertia. In the economy, that’s deflation, and it’s actually a bigger problem than inflation. Deflation occurs when prices are falling. When people notice that prices are going down, they start to hold off on buying things because the price could keep going down in the future. When that happens economy-wide, it can create a slowdown that is very difficult to correct.

Deflation in America is rare but not unheard of. During the Great Depression, the stock market bottomed out and Americans were faced with tremendous outstanding personal debt. People began holding onto their money rather than spending it, which brought down consumer demand. Since companies were unable to sell their products, they slashed prices and laid off employees en masse. As more people lost their jobs, demand fell even more, setting a deflationary spiral into motion.

Short-term deflation, however, is a very different animal from long-term, Great Depression-like deflation. When we have temporarily low oil and food prices, it feels like a bonus because our income stretches further. Since we need to replenish gas in our cars and food in our kitchens on a regular basis, we’re not going to stop buying those things. And as long as we can trust that we’ll remain fully employed, we’ll maintain our regular spending and saving habits. So, temporary deflation isn’t going to set off an economic catastrophe when it’s a short-lived event.

Should We Be Worried About Deflation?

We know that inflation is slowing down, since the CPI reports show that inflation has fallen from 2.1% in May 2014 to 0% in September 2015. How close we are to outright deflation depends on which data you use. Core CPI, which removes volatile energy and food prices, shows inflation at a more robust 1.9%, compared to 0% overall.7 Economist Daniel Alpert, on the other hand, notes that when housing is taken out of the market basket, the U.S. has been experiencing deflation since November 2014.8 Going forward, the IMF projects less than a 2% chance of deflation in the U.S. next year.9

A bigger issue is the threat of deflation elsewhere—namely, Europe, where annual inflation has fallen to -0.1% as of September.10 Because the global economy is so interconnected, deflation in a major trading partner can hurt U.S. exports. If prices for local goods in Europe decline but prices on imports don’t change, consumers will be less likely to buy products imported from the U.S. If American firms drop their prices to compete, they’ll be less profitable. Big-ticket items like industrial goods will be even harder to move because European companies will be inclined to sit on their cash rather than spend it. That is why the European Central Bank is trying to coax some inflation out of the Eurozone.

Deflation in Japan: A Tough Habit to Kick

Earlier this year, Prime Minister Shinzo Abe made an unusual plea to the private sector in Japan, asking firms to give workers a pay raise of at least 2% this year.11 His hunch is that an increase in wages should cause prices to go up—and that should stimulate the spending and investment that could kickstart the economy. Given that Japan’s annual GDP growth has been just 1.1% over the last 25 years, a little inflation could serve as the shot in the arm that it needs.12

Even if employers follow through with Abe’s request, Japan faces another hurdle to growth: Its citizens save too much. This is a problem that might sound unfathomable to Americans, but it is the result of two and a half decades of very low inflation (0.5% annually) in Japan.13 Companies are clinging to $2.1 trillion in cash, a sum equal to 44% of the country’s GDP.14 Since low inflation depresses interest on bank deposits, individuals keep cash at home, to the tune of a collective $300 billion.15

Even children have inherited the hoarding mentality. KidZania is an international chain of theme parks, where kids get play money to spend on games and rides inside. In most countries, kids blow through their play money, but Japanese children are remarkably reluctant to spend their cash.16 This penchant to save, ingrained from years of deflation, will make Abe’s plea for spending all the more difficult.

Conclusion

What we need to fear is not inflation itself, but more fundamental problems in the economy that show up in runaway inflation or uncontrollable deflation. Unexpected swings of prices—either up or down—can cause big and problematic shifts in the economy. In a world of slowing growth, maintaining a slight and steady level of inflation can actually keep the economy above water.

Glossary: Variations of Inflation Measurements

CPI-U, Rate: 0%: The Consumer Price Index for All Urban Consumers (CPI-U) is the “headline” number that is regularly reported by the media as the general inflation rate.

Used by: Many employers and property managers to calculate cost-of-living adjustments in wages, salaries, and rents.

CPI-W, Rate: -0.6%: The Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W, only captures about 28% of the U.S. population, but it has been in use since 1913, compared to 1978 for CPI-U.17

Used by: The Social Security Administration to calculate annual cost-of-living adjustments.

Core CPI, Rate: 1.9%: Core CPI, which is reported as the index for all items except food and energy, is viewed as a more stable measure of inflation than the overall index because it is less sensitive to temporary price changes.

Used by: Economists making evaluations or projections of inflation over a period of one year or longer.

Chained CPI, Rate: -0.5%: Unlike other CPI measures, Chained CPI more fully accounts for substitutions that consumer make when prices change. It is considered the most technically advanced of the BLS’s major cost-of-living indexes.18

Used by: Chained CPI is currently not used by the government, but some have proposed using it for tax code parameters and federal benefit programs.

PCE, Rate: 0.2% / Core PCE, Rate: 1.3%: Economists generally prefer the Personal Consumption Expenditures index—which is based on surveys of businesses rather than surveys of consumers—because it captures a wider consumer base than the CPI-U and fully accounts for substitution effects like Chained CPI does.19

Used by: The Federal Reserve to evaluate whether it is achieving the inflation objective of the dual mandate.

Note: Inflation rates reflect the most recently reported 12-month period.

Sources: U.S. Bureau of Labor Statistics (CPI)20, U.S. Bureau of Economic Analysis (PCE)21