Report Published October 16, 2012 · Updated October 16, 2012 · 10 minute read

A Better Way to Handle the Debt Ceiling

To break the ongoing stalemate over the debt ceiling, Third Way is proposing a commonsense solution that would automatically raise the debt limit as long as fiscally responsible debt targets are achieved. If we fail to meet those targets, then we would fall back to our current system. This change would enable fiscal certainty and responsibility, all while avoiding the threat of default.

The Problem

Politics Threatens a Default

The United States has an outstanding record of paying its debts on time.1 That record nearly came to an end in August 2011, though, when Congress got one day away from a default after several months of playing a game of chicken over the debt ceiling. The Budget Control Act of 2011, signed by President Obama on August 2, 2011, averted the crisis by lifting the ceiling on the Department of Treasury’s borrowing authority. But the crisis left a black mark on our credit history.

Now, history is repeating itself as the next debt ceiling target deadline grows near. House Speaker John Boehner has again threatened to oppose a debt ceiling increase without offsetting spending cuts.2 He calls the debt ceiling “an action forcing event.”3

Yet, that stance is the same one that led to the game of brinkmanship over the debt ceiling in 2011. And, it will lead to the same result this time because it places the GOP’s budget goals over the need to protect the nation’s credit rating. It is a negotiating stance that does damage to the nation and the economy in three ways: 1) the threat of default puts the U.S. credit rating at risk; 2) wrangling over the debt ceiling destroys business certainty; and 3) default causes certain bills to be paid—and others to stack up untouched.

1) The threat of default puts the U.S. credit rating at risk.

As we discussed in our memo, “The Dominoes of Default,” the United States has the luxury of borrowing money more cheaply than any other country because Treasury bills are the safest investment on earth.4 Our low risk means that we have to pay investors very low interest rates.

But, the 2011 debt crisis gave investors worldwide a reason to doubt that the U.S. will always be as responsible with its debt as it had in the past. Four days after the crisis ended, Standard & Poor’s, one of the three large credit rating firms, downgraded the AAA U.S. credit rating to AA+ in part due to unstable and unpredictable policymaking in Congress.

More recently, Moody’s has warned that political dysfunction over budget issues next year, which includes the debt ceiling vote, would lead to a downgrade.5 So far, neither Moody’s nor Fitch have followed S&P by issuing a downgrade, but all three credit rating agencies have warned that further political dysfunction on debt payments and reducing the debt will necessitate a downgrade.6

And what would this downgrade mean? For one, we would have to pay investors more to take on our debt as the days of being a risk-free investment would inevitably pass—a situation we cannot afford.

2) Wrangling over the debt ceiling destroys business certainty.

When the U.S. borrows money, there should be no doubt that the nation will pay its debt. Yet, when the nation gets close to broaching our debt limit—and doubt starts to creep in—foreign investors are not the only ones who start to worry. The debate over the debt ceiling during the summer of 2011 vividly showed how uncertainty over federal fiscal policy can have a direct impact on American businesses.

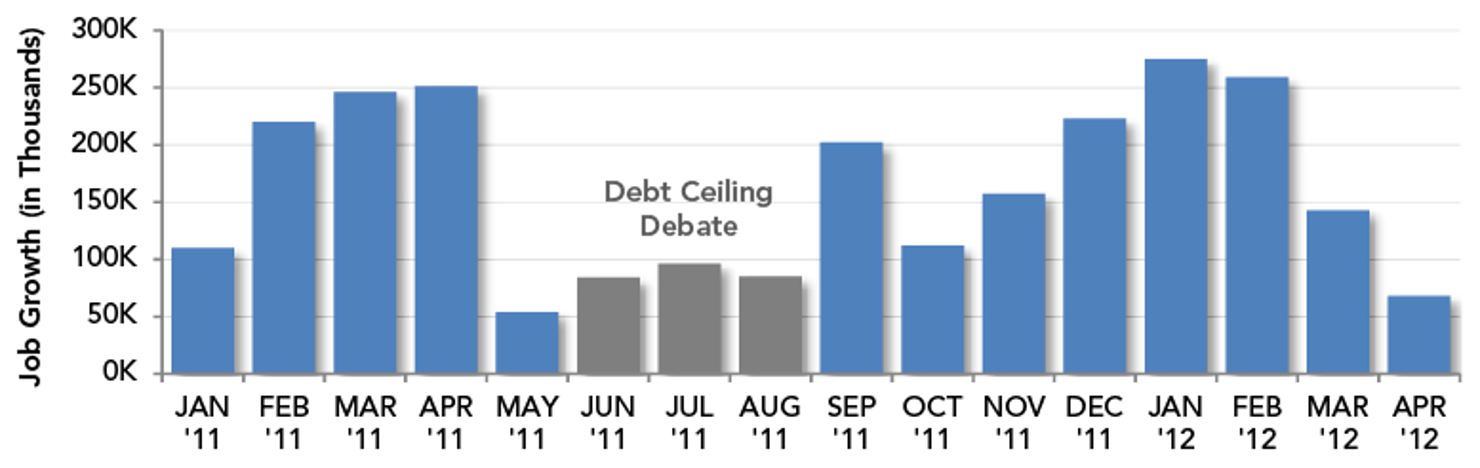

Economists Justin Wolfers and Betsey Stevenson at the University of Michigan studied the impact of the debt ceiling debate on the economy.7 During the three months that preceded the August deal on the debt limit, job growth fell by over half.

Monthly Growth in Non-Farm Payroll8

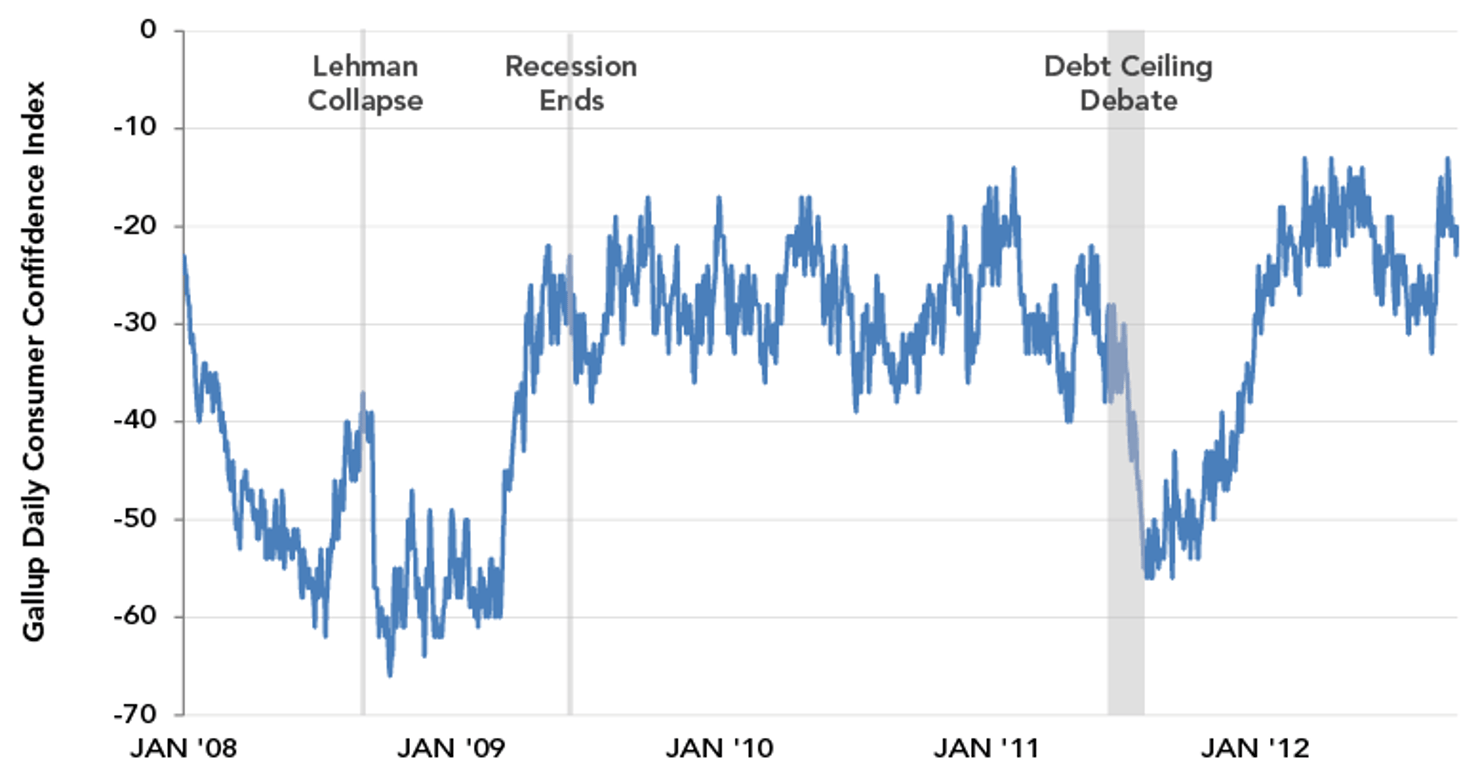

That loss in job-growth is not surprising, though, given the effect that the debate had on consumers. Consumer confidence in the economy dropped precipitously, which in turn, dried up demand for new services and new jobs.

Consumer Confidence9

As the economy continues to recover from the Great Recession over the next few years, American businesses are going to need economic certainty—not increased political brinkmanship over the debt ceiling.

3) Default causes certain bills to be paid—and others to stack up untouched.

During the 2011 debt crisis, some members of Congress argued that the Treasury Department could find ways to juggle federal payments to pay Treasury notes and avoid default if the debt ceiling weren’t increased. This terrible precedent would be like a family paying its mortgage but not its auto loan or credit card debt. The consequences would be the same for the nation’s credit worthiness.

Such cavalier thinking threatens everyone who depends on the federal government to pay its obligations. Businesses providing products and services to the federal government—from computers to weapons systems to microscopes—need to meet their payroll and pay their bills. Seniors and veterans rely on checks from the government for basic living and health care. Soldiers and federal employees—from FBI agents to meat inspectors—need to be paid for vital government services to continue. Regardless of the politics of those who depend financially on the federal government, they certainty did not sign up to be treated as pawns in political power struggle.

In the simplest terms, how can the United States be a world leader if it can’t fulfill its most basic obligations?

The Solution

Link Automatic Debt Ceiling Increases to Healthy Debt Targets

Debt ceiling increases understandably cause concern among Members of Congress. Not only are they unpopular votes, they also serve to remind the nation of the mounting levels of debt that have been building up for decades. But the way to control the debt is through a balanced budget deal—not by putting the nation at risk for default.

The origins of the debt ceiling go back to World War I.10 In 1917, Congress gave Treasury the flexibility to offer bonds of varying maturities under an aggregate limit on those bonds. Previously, the Administration had to ask Congress for permission to borrow money for specific projects with specific types of bonds. Today, that flexibility has turned into a straight jacket for Treasury as it juggles bonds to avert a debt crisis.

When Congress comes together after the election to deal with the various provisions of the fiscal cliff, Democrats and Republicans should leverage this moment to also fix our broken debt ceiling process to promote fiscal certainty and responsibility.

From 1980 to 2007, Congress avoided the risk of default by making frequent use of the Gephardt Rule. Named for former Democratic Majority Leader Richard Gephardt, this rule allows for automatic debt ceiling increases under certain circumstances. The process begins in the House where a debt ceiling increase is deemed to have been passed once a budget resolution has passed the House and the Senate.11 The Clerk of the House automatically sends the legislation to the Senate, which then follows the normal legislative process. The Gephardt Rule remains on the books, but Congressional leaders have not been able to utilize it because the divided Congress has not agreed upon a budget resolution.

Congress can build upon the certainty that the Gephardt Rule ushered in and make adjustments to it to ensure fiscal responsibility in two possible ways:

- Change the debt ceiling law so that it adjusts automatically as long as debt targets are achieved; or

- Amend the Gephardt Rule so that House leaders can deem a debt limit adjustment without waiting for the Senate to act as long as the House has passed the budget resolution AND a fiscally responsible debt target has been met for that year.

Option #1 would allow for truly automatic increases in the debt ceiling as long as federal budgets were on a sustainable path. Option #2 would allow for automatic votes to increase the debt ceiling.

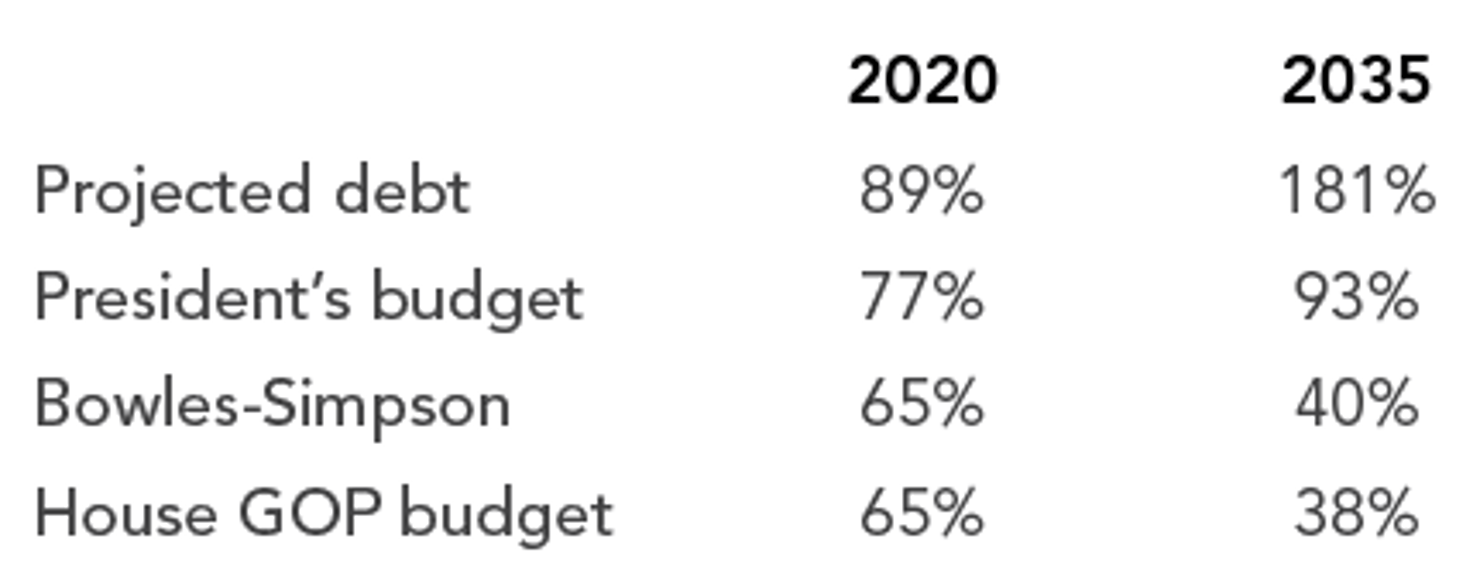

Here’s how Congress could set the debt targets: Most of the major budget proposals across the political spectrum aim for a debt-to-GDP limit of 60% to 80% by the end of the decade.12 Without changes in current policy, the Congressional Budget Office (CBO) projects that our debt will rise to 89% of GDP in 2020 and 181% in 2035.13

As part of negotiations on the fiscal cliff, a debt target could be set for each year based on CBO estimates. Congressional leaders would need to compromise on what those targets would be as part of the broader negotiation over the fiscal cliff, but these targets could be similar to various targets from leading budget proposals (as shown below):

Projected Debt and Targets (% of GDP)14

Under such an agreement, if the fiscally responsible debt targets were met and certified by CBO, then the modified Gephardt rule would apply and the debt limit could be automatically raised (Option #1) or automatically sent to the Senate for vote following passage of a House budget (Option #2). However, if our debt-to-GDP exceeded the debt targets, Congress would have to use the normal legislative process for the debt ceiling vote. The threat of a separate vote would help encourage future Congresses to stand by a responsible budget deal and put our nation on a sound fiscal trajectory.

Critiques and Responses

Won’t the threat of a default continue even with debt targets?

True, Congress could always change the process for automatic increases in the debt ceiling. But as long as there is progress toward stabilizing the debt, it will be much harder for one party in Congress to coalesce around a strategy that threatens default as a necessary step for fiscal discipline.

Couldn’t Congressional leaders ignore the option to use the automated debt ceiling procedures under the Gephardt rule?

Yes, nothing would force House leaders to adopt a debt ceiling increase automatically as part of a House budget resolution. But House leaders could no longer claim that their hands were tied over the debt ceiling due to opposition to a debt ceiling increase within their caucus. If House leaders had the power to make a debt ceiling increase happen automatically, then it would be their responsibility to use that power to avoid default.

What if CBO’s projections for the debt turn out to be wrong?

Mistaken targets would not endanger the nation’s credit rating and could be corrected. CBO’s debt projections from a budget deal, which would set the targets for the debt, would be subject to many technical uncertainties such as projections of economic growth and interest rates. Congress would need to periodically review the debt targets and make sure they continued to be accurate and make adjustments accordingly.

Why is a debt target necessary?

If a nation’s debt exceeds its capacity to make payments, then fiscal collapse is not far behind. In order to avoid a debt crisis similar to what Europe is experiencing, the U.S. must reduce its long-term structural deficit. A debt target would give lawmakers a highly visible measure of their success and a process to avoid unnecessary default.