Memo Published June 28, 2013 · Updated June 28, 2013 · 17 minute read

The Four Fiscal Fantasies

Democrats are at a crossroads. There is growing pressure on the party from many liberal advocates to curtail further efforts at long-term U.S. fiscal reform. They argue that any real entitlement changes should be shelved for at least the remainder of Obama’s presidency, thus relegating a grand bargain to the J.C. Penney sales bin.

They note correctly that our short-term fiscal situation has improved, that there has been a welcome pause in health care cost inflation, and that our economy still has far too many un- or under-employed. Thus, their alternative: a return to the agenda of Obama’s early first term when the economy was in free-fall—another round of massive spending on job-creating investments, new and expanded entitlements, continued high deficits, and a substantial tax increase.

A portion of this argument is now moot: a large-scale grand bargain died with the fiscal cliff deal, which eliminated the main forcing mechanism—we won’t soon again see trillions of dollars of tax breaks expire and automatic spending cuts to discretionary defense and domestic programs occur on the same day. Without these hammers, a grand bargain has about as much life as the Monty Python parrot.

But just because we aren’t likely to see one large fiscal deal does not mean that Democrats should stop pursuing fixes to our safety net programs. In fact, the liberal case is built on four fiscal fantasies that we describe below. If Democrats heed this policy advice and walk away from fixing entitlements, it will be a catastrophic policy and political mistake—for the party, the middle class, and the country’s future.

Fantasy #1: Taxing the rich solves our problems.

Virtually every progressive economic plan proposes significant tax increases on the wealthy and large new government spending, holds the middle class harmless, and manages to achieve reasonable budget deficits. Lo if this were possible.

Raising additional taxes on the wealthy is necessary, but it is not sufficient. Suppose we pass a new tax plan that completely soaks the rich. We raise the top rate ten points to 49.6%. We impose the Buffet Rule, requiring all millionaires to pay at least 30% in taxes. And we dramatically raise the estate tax to create a $3.5 million exemption with a 45% rate. Most of these rates are all well above anything under serious consideration, but let’s play this policy out for a moment.

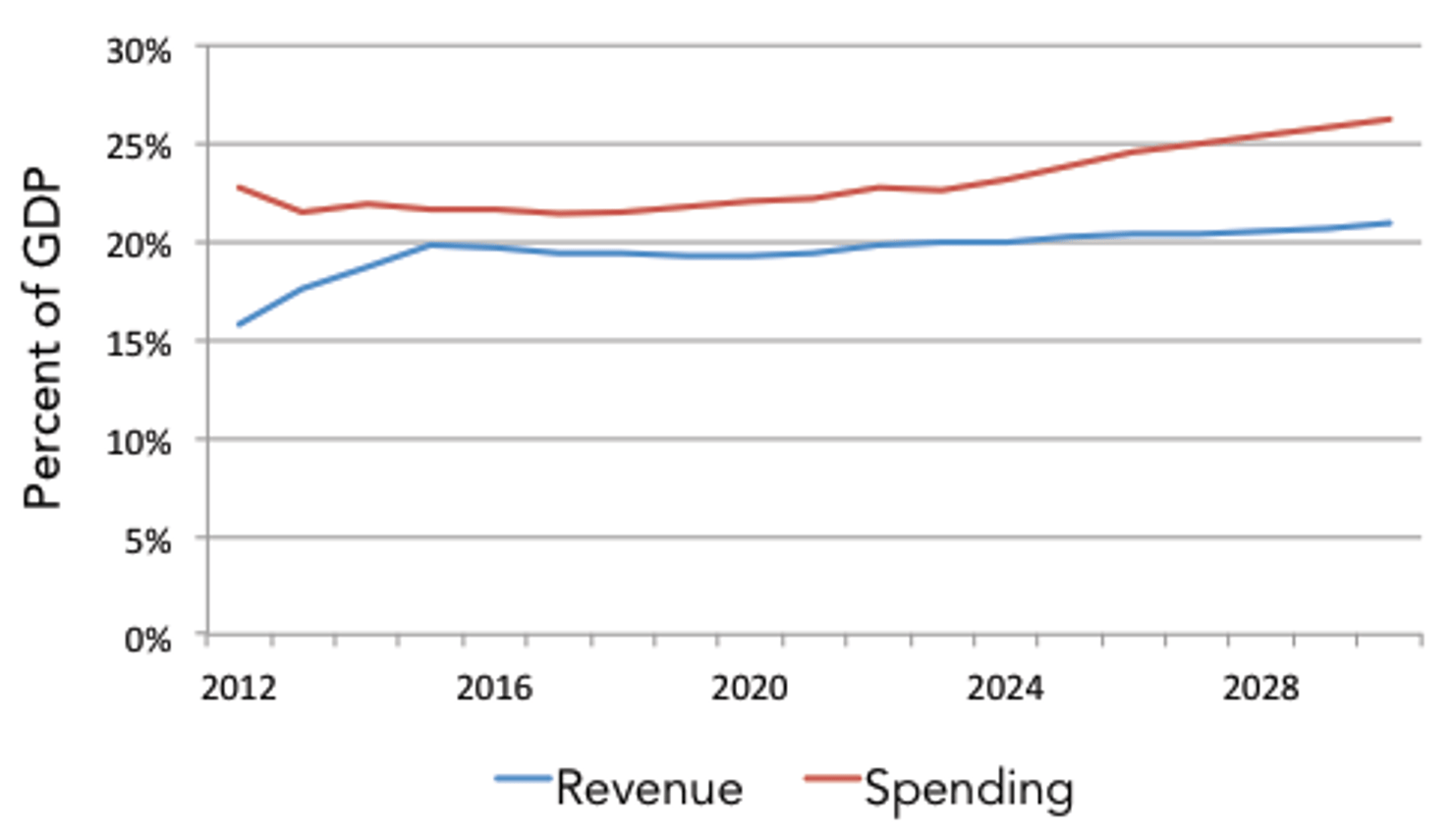

If we leave entitlements on auto-pilot in this scenario, our deficit in 2030 will be close to a stunning $1.3 trillion, in 2013 inflation-adjusted dollars.1 Thus, the belief that we can solve our long-range deficit problem by taxing the wealthy alone is a fantasy. We can solve some of the problem this way, but that’s about it.

Soak the Rich Scenario: Spending and Revenue Projections2

Let’s give credit to prominent liberal economist Simon Johnson and co-author James Qwak, who together penned a book arguing that entitlements should not be trimmed and proposed a plan on how to do it while keeping the country’s finances roughly in check. They called for significantly higher taxes on the wealthy. But they candidly admitted that, to afford entitlements, the middle class would have to pay more taxes as well. This is part of their list and how it would affect a working family earning $65,000 in wages:3

- 1-point point bump in FICA for Social Security ($650 per year);

- 1-point bump in FICA for Medicare ($650);

- 50-cent increase in the federal gas tax ($100 with rebate);

- 5% VAT ($750), halve the mortgage interest tax deduction ($600); and

- Other tax hikes ranging from the elimination of the state and local tax deduction to a new carbon tax.

Some of these ideas may eventually be necessary, but we need to realize that it comes out to several thousand dollars a year in new taxes for middle income families.

Of course we need to raise taxes on the wealthy, but Democrats cannot pretend it’s an economic panacea; it will only accomplish so much.

Fantasy #2: We can have it all.

There is a belief that America can afford (and Americans will accept) ever-growing entitlements and robust public investments. This is a fantasy on both policy and political levels. Let’s start with the policy.

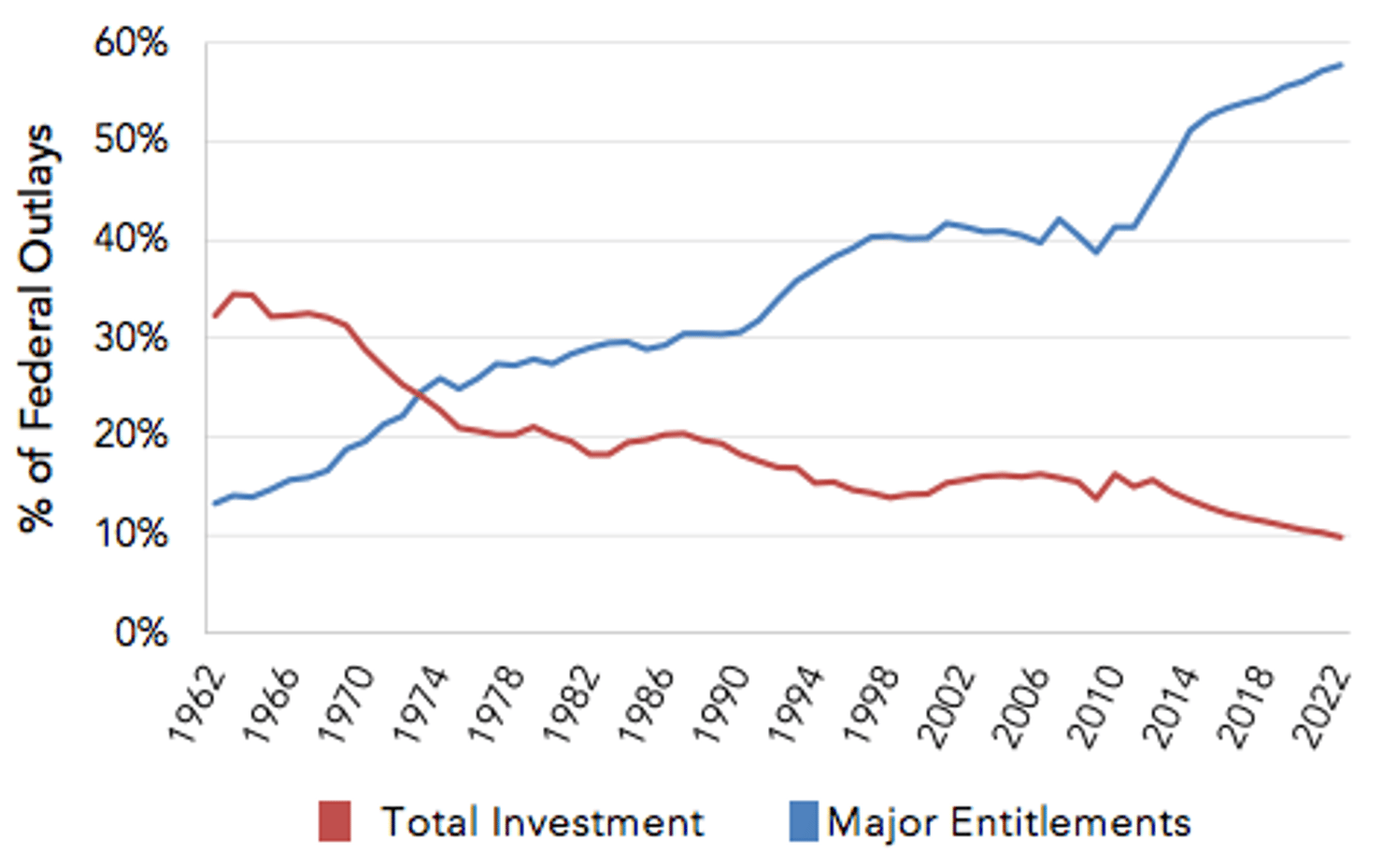

In the mid-1960s, the federal government spent three dollars on public investments for every one dollar it spent on the major entitlement programs. By 2012, the ratio was reversed; we spent three dollars on Social Security, Medicare, Medicaid, and CHIP for every one dollar we spent on investments. And the ratio will be five to one in 2022. This does not include other major entitlements like veteran’s health and disability, Supplemental Security Income (SSI), and food stamps.

It will only get worse as the realities of demographics come into play. Over the coming two decades, the number of elderly people in America will jump 81% while the working age population inches up by 8%.4 We like to paint a portrait of the elderly as uniformly economically vulnerable—and many undoubtedly are. But today there are 3 million senior citizen families—one of every nine senior households—who earn more than $100,000.5 There is a multitude of prim, gated elderly communities where legions of senior citizens receive massive government subsidies far beyond their contributions to the programs. Meanwhile, we cannot scrape the nickels together for universal pre-K, Pell Grants don’t come close to paying for college for deserving poor kids, we have lousy roads that could employ tens of thousands of people to fix, and our space program is a faint echo of the past.

Democrats have two broad economic legacies: the New Deal/Great Society safety net programs of FDR and LBJ and the New Frontier investment programs of JFK. These are both our children. There was a point—during the decades that our economy grew at an average annual rate of 3.3%—when we could send each child to summer camp, piano lessons, and ballet, stay roughly within a budget, and keep tax rates relatively low. To believe we can do so in the future is pure fantasy.

Investments and Entitlements as a Percentage of Federal Spending6

So what have we done? We’ve spent lavishly on one child, and we’ve starved the other. The proof? Just look at the past several years. The major entitlement programs have bludgeoned investment programs into submission. In every budget deal, domestic discretionary spending was the sacrificial lamb. We thought sequestration would be too difficult for the political system to bear. No one blinked; no one cared. This isn’t a new story—Gramm-Rudman-Hollings choked discretionary spending in the 1990s and left entitlements alone.

We continue to test the thought that we can have it all despite overwhelming evidence that in the real debates that occur in the halls of Congress, investment programs always take the hit. When will we learn?

The political case is even more stark.

At the start of the Great Recession, we rescued the banks, passed a stimulus package that approached one trillion dollars, and saved the auto industry. Then we made a choice. We decided to pass universal health care.

Third Way actively supported health reform; we are not playing Monday morning quarterback. But we could have made a different choice—more stimulus, a huge infrastructure bank, massive energy reforms, and increases to investments. Instead we chose a new health care entitlement to complete the safety net, and it was a choice that, predictably, precluded any other significant spending that could boost the economy. Why? Because there is a limit on how much voters will allow for government spending, especially when our national, publicly held debt is $11.9 trillion and has jumped from 37% to 75% of GDP in the space of five years.*

* Gross federal U.S. debt is now $16.7 trillion.

The evidence is clear:

- Democrats were slaughtered in the 2010 mid-terms;

- The House flipped;

- There are now 30 Republican governors in state houses;

- Democrats lost governorships in the states that directly benefitted from saving the auto industry; and

- The Tea Party was born.

There is a belief by many on the left that if a spending program is worthy, then voters will support it without trade-offs. That too is a fantasy. Economics is about the allocation of scarce resources, and Democrats too often pretend that taxpayer resources are not scarce—particularly if they deem those taxes as coming from the wealthy.

Yet, time after time, as Democrats have sought to increase spending in the modern era beyond a breaking point, they’ve been brought back to earth by voters. In all cases, the spending programs were poll-tested and popular. And, in the abstract, spending on health care, education, roads, bridges, science, space, research, and college is popular. But voters intuitively see the avoidance of choices and cannot help but see a $11.9 trillion national debt as profligate which spurs a popular anti-spending movement (remember Ross Perot?). Ultimately, when debt levels balloon under their watch, Democrats pay for it at election time. Is it worth losing an election over important spending programs that can create economic opportunity? Yes, but realize you lose the opportunity to spend again because the opposing party will have the power to thwart it.

It would be foolish and dangerous for Democrats to pretend we can have it all. Neither the policy nor the politics will support that, and the time has come to rebalance our nation’s and party’s priority back to investments in our future.

Fantasy #3: Waiting is benign.

In May, the actuaries released the Social Security and Medicare Trust Fund reports. The Medicare outlook, thankfully, was improved—albeit from dire to dismal. The Social Security outlook was decidedly awful. Over the past ten years, the insolvency date had crawled forward from 2042 to 2033. The hope was that an improving economy would push the date further out. It did not, and every indicator of Social Security health worsened between 2012 and 2013.Many prominent liberal voices say we should ignore calls to fix Social Security and Medicare. On Social Security, they say 20 years is “as far as the eye can see."7 But it’s the blink of an eye in an actuarial table. It means that someone who is 45 today is being promised (and is planning on) full benefits and no tax increases, but in reality will not come close to full benefits at retirement or stable taxes.

Entering Work and Entering Retirement: Number Reaching 25th and 65th Birthday Each Day8

| Year | 25th Birthdays | 65th Birthdays | Ratio of 25 to 65 year olds |

| 1990 | 11,691/day | 5,823/day | 5 : 2.5 |

| 2000 | 10,620 | 5,921 | 5 : 2.8 |

| 2010 | 11,712 | 6,670 | 5 : 2.8 |

| 2020 | 12,253 | 9,654 | 5 : 3.9 |

| 2030 | 12,499 | 10,948 | 5 : 4.4 |

On Medicare, we had a welcome pause in health care’s growing costs, but we’ve had pauses before. In the 1990s, health care inflation took a three year hiatus. Many crowed that the problem of exploding health care costs was over. So, is this current pause permanent? There is no consensus whatsoever that it is. In fact, unlike the rest of the economy, there has been zero productivity growth in Medicare in two decades.9 We also know there is massive overutilization of health care services—tests that shouldn’t be administered, procedures that won’t improve people’s lives, drugs that needn’t be prescribed, and medical errors that shouldn’t occur all tied into a health care system that still mostly rewards the quantity of services offered, not the quality. There is an enormous economic cost of this for middle class wages, business job creation, and taxpayer funding of Medicare and Medicaid. Why shouldn’t we aggressively solve these problems?

Still, there is a growing belief on the left that it is benign to wait on fixing the major entitlement programs. But it is a fantasy. Every year that we wait, the fixes get appreciably harder. The proof?

Several years ago, liberal proponents of an all-tax solution for Social Security called for eliminating the payroll tax cap to solve the problem. Now they say it solves “most of the problem.” Why? Because we waited too long. Today, eliminating the FICA cap entirely (which we do not advocate) solves 79% of the problem.10 Supporters of a tax-only solution now also call for adding a point to the payroll tax for all workers. To be clear, 1-point for a typical working age family would add $650 to that family’s payroll tax burden in a single year—not counting the employer contribution to FICA. Over the course of their peak earning years, it would mean an additional tax burden of nearly $20,000. Paying more to get the same benefit is a form of benefit cut—a big one. This does not include the cost to employers who would be paying hundreds of billion dollars more in new FICA taxes that could instead employ American workers or raise wages.

Should we fix the roof when the sun is shining or wait for the next downpour? Waiting is anything but benign.

Fantasy #4: The politics get better.

There’s no debate that our safety net programs need to be fixed so that they are there for current and future generations. There is unanimous agreement among liberals, conservatives, and moderates. The only questions are when and how.

There is a belief on the left that the politics improves as we get closer to the insolvency date and that we could enact a better solution with Democrats holding the White House and both houses of Congress. But this, too, is a fantasy.

First, the only way entitlements ever get fixed is through divided government. Solutions inevitably include some measure of tax increases and benefit cuts, and no party wants to do that alone. So if there is another magical moment like 2009 and 1993 when Democrats win it all, the odds that they will sacrifice their majority on the altar of a Social Security or Medicare fix are remote.

Let’s face facts. The political roster we have now is as good as it will ever be. We have a Democratic president committed to the safety net, a solid Democratic majority in the Senate with a leader committed to the safety net, and a strong minority leader in the House also committed to the safety net. In 2017 and beyond, who knows what the leadership of Washington will look like. It may be as good as today’s, but it won’t be better and it could be worse for fixing safety net programs.

Elderly Share of the Electorate: 2012 to 2024 | |||

| 2012 | 2016 | 2020 | 2024 |

| 16% | 19% | 21% | 23% |

Second, 16% of the electorate in 2012 was over the age of 65. In 2016, it will be 19%, 21% in 2020, and 23% in 2024 based on Census Bureau projections of the population.11 When the near-elderly are included (those between the ages of 55 and 64), 39% of the electorate will be above or near retirement age in 2024. How will we possibly fix safety net programs then?

For those who advocate for delay, there is a method to the madness. Among some elderly advocates, the strategy is to delay entitlement fixes for as long as possible, because the view is that the closer we get to insolvency, the more likely a solution will tilt more toward tax increases rather than benefit cuts. With the elderly and near-elderly voting populations representing two of five voters in just over a decade, they are probably right. So, as we are in a pitched international battle for economic livelihood, we can count on future withering tax increases on the middle class to fix these programs.

What to do?

Opponents of entitlement reform have labeled any attempt to trim these costs as “austerity economics.” But that label is a misleading attempt to dodge the serious choices Democrats must make if we are going to reset our priorities for future generations and renew long-term U.S. economic strength.

First, we haven’t had an austerity budget. Between 2004 and 2008, federal outlays averaged $3.022 trillion in 2013 dollars. Between 2009 and 2013, federal outlays averaged $3.698 trillion in 2013 dollars—an average annual budget that is 22.3% higher in the most recent five-year period than over the previous five-year period.12 This doesn’t include short-term tax expenditures like the payroll tax break for workers.

Second, the course that we are now on, in fact, sets us on an austerity budget path for kids, science, roads, research, energy, and investments. Fourteen cents of every federal dollar not going to interest was spent on entitlements in 1962, but in 2012 that amount was 47 cents. By 2030, 61 cents of every non-interest dollar will go toward funding these programs.13 The other 39-cents will go to everything else—net interest, defense, intelligence, veterans, foreign aid, children, infrastructure, energy, and research. In this battle for the remaining scarce resources, investments will lose.

We can fix Social Security so that it is there for future generations while paying a more generous benefit for those at lower incomes. We can trim some of the fat from Medicare so that it doesn’t swallow the budget, go bankrupt, and erode wages. We can find needed savings in other mandatory programs to finance new investments for decades to come. Along the way, we would be raising taxes on the wealthy and narrowing long-range deficits.

None of these will be easy, but ending the fiscal discussion is a severe mistake—for the country and for Democrats. Here are the broad brush strokes of what we ought to do on the entitlement and investment portions of the budget:

- Pass a Social Security commission with a guaranteed up or down vote on a 75-year solvency plan. After the demise of Bowles-Simpson and the Super Committee, Washington is justifiably commission-averse. But a commission is the only way to fix Social Security, because neither party wants to go it alone. Furthermore, if it is designed to succeed (like the 1983 Greenspan Commission or the Defense Base Closure and Realignment Commissions) rather than fail with too broad a scope or unrealistic vote thresholds, the outcome will be very different.

A Social Security fix offers something for both parties. For Democrats, an Obama-led bipartisan commission plan is certain to raise taxes on the wealthy (we estimate about $500 billion over the first ten years mostly through a partial lifting of the cap) and some minimal benefits cuts (likely through chain-weighting of CPI). The plan is also certain to protect the most vulnerable. For Republicans, the plan is guaranteed to narrow short- and long-range deficits. A FICA tax increase dedicated to solvency is the only revenue increase Republicans will willingly support. It will also put an end to the Democratic drumbeat that Republicans are seeking to end Social Security. - Enact a series of Medicare fixes to reduce excess spending on unnecessary care and dedicate all savings to Medicare solvency. For Democrats, smart fixes will obviate the need for benefit cuts and make the pause in health care cost inflation permanent. There are enough areas where costs can be trimmed without having any impact on seniors’ benefits—bundled payments, medical homes, end-of-life, etc. For Republicans, fixes will be sizable enough to pass the reform test and would also reduce long-range deficits. We recommend starting with a permanent fix to the Sustainable Growth Rate (doc fix) that is paid for by score-able policies that reduce duplicative care and increase provider coordination.

- Increase investments through off-setting savings in other mandatory spending programs. For Democrats, additional savings from federal pensions, farm subsidies, and all other mandatory spending should boost spending for investment priorities in kids, science, research, curing disease, infrastructure, energy, and college—and not for deficit reduction. For Republicans, defense sequestration would end and all new domestic investments would be deficit neutral.

Conclusion

The grand bargain is over, but there is a tremendous opportunity to promote particular policy fixes individually. They would help grow the economy, provide room for additional spending in places that create future growth, foster opportunity for middle class families, reduce our long-range deficits, and make the safety net secure. But these opportunities will not occur if our fiscal conversation is ended prematurely.