Report Published February 15, 2019 · 14 minute read

The Opportunity Bank: A Trillion Dollars in New Small Business Lending

Ryan Bhandari

Takeaways

Last year, one out of three small businesses did not apply for financing simply because they thought they would be denied, or because the cost of credit was too high, or because the application process was too complicated.1 When one-third of small business owners are scared to even pursue capital, we have a massive opportunity crisis on our hands. In this paper, we dissect the degree and the reasons for the lack of opportunity capital for much of the country and propose a broad new “Opportunity Bank” to provide up to $1 trillion in new small business and start-up lending over the coming decade.

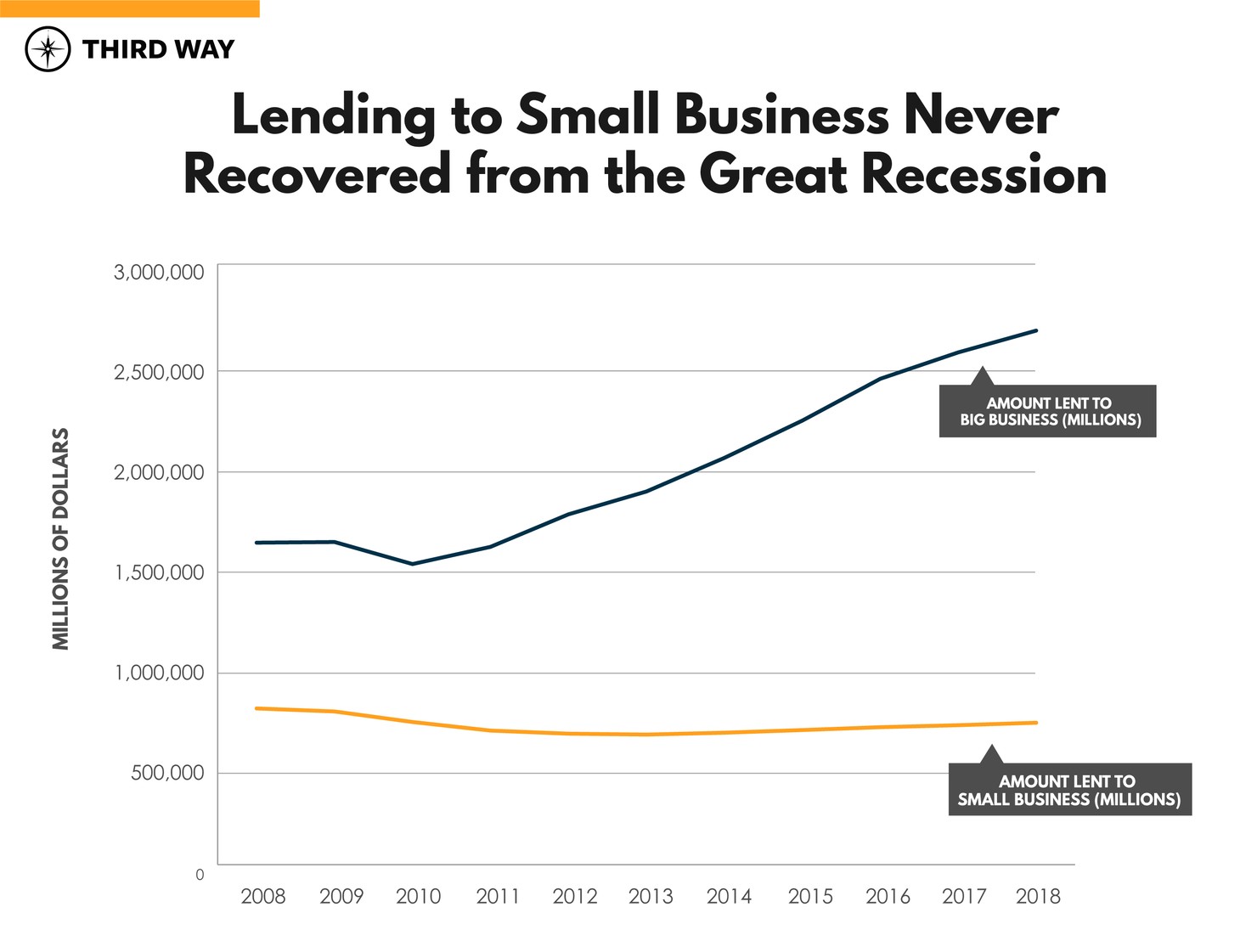

- Access to traditional forms of credit has declined for both small and rural businesses. Since the recession ended, big businesses have posted a 35% increase in loans, as small businesses have seen a 9% decrease. Rural lending to businesses is below 1996 levels when adjusted for inflation.

- Banking sector consolidation has led to higher small business loan rejection rates, with large banks rejecting nearly half of all small business loans while community banks deny only one-sixth.

- Partly as a result of less credit, more than 2,100 counties in America suffered a net loss of businesses between 2005 and 2015, shedding a net total of 200,000 private sector businesses and 1.2 million private sector jobs over that decade.

- To provide millions more small business owners with the opportunity to start and grow a business and create jobs, we propose to unleash $1 trillion in new lending over the next decade through a new Opportunity Bank.

- The trillion dollar Opportunity Bank would partner with local banks and credit unions to quadruple the number of loans being offered and remove the barriers that stop individuals from seeking and receiving government-backed loans in the first place.

America faces an opportunity crisis. Unless you live in a certain place, have a certain background, or have a certain credential, opportunity in the digital age feels like it is slipping away. Third Way has proposed a series of big ideas so that everyone, everywhere has more opportunity to earn a good life in our modern economy. The idea below addresses the concentration of access to credit that is essential to starting and growing a business.

The Problem

According to the Federal Reserve’s Small Business Credit Survey, one-third of the small business owners in this country were too scared to pursue capital in 2017. They did not pursue lending because they thought they would get denied for the loan, because the cost of credit was too high, or because they felt the application process was too difficult to navigate.2 It’s no wonder they are nervous—despite the booming economy, access to credit for small businesses is far too restricted.

Since the recession ended, big businesses have seen a 35% increase in their loan volume compared to a 9% decrease for small businesses, as the chart below illustrates.

Moreover, rural lending to businesses is below 1996 levels when adjusted for inflation.3 And many of the largest financial institutions have stopped making loans to businesses with less than $2 million in revenue and stopped making loans less than $100,000. Instead, large financial institutions direct loans of less than $100,000 to their small business credit card products that earn higher yields. This is a serious problem though as many small businesses, especially those in their most nascent stages, are seeking loans under $100,000.4

One of the primary reasons for lower access to credit is the fact that there are fewer community banks than there were two decades ago. A wave of mergers in the finance industry that started in the early ‘90s, but was dramatically accelerated by the Great Recession, has resulted in a disappearance of roughly 10,000 banks over the last 30 years. Some have also argued the Dodd-Frank Act, which helped shore up the stability of the financial sector, also came with higher compliance costs that tended to hurt community banks more than larger, established banks.5

As the number of community banks has declined, so has lending to small business. Small community banks make loans to budding entrepreneurs and business owners partly based on non-quantifiable metrics of trust and interpersonal connections (i.e. I know this person and trust her to repay this loan). Large banks usually do not.

Since small businesses ask for less money than big businesses, there is also a smaller financial return for a big bank that lends to a small business. Thus, banks are more inclined to lend to larger companies. This is likely the reason why small business loans at community banks garnered an approval rate of 83% compared to just 50% from large banks.6

It also helps that these larger companies seeking loans have a longer history of quantifiable measures such as book value and free cash flow. Unfortunately, many small business owners often do not have a credit history that larger financial institutions find satisfactory. According to the Federal Reserve’s survey, the leading cause of being denied for a loan was an insufficient credit history.

When small businesses are starved for capital, it has massive repercussions on communities across the country. New, small businesses account for almost all of net job growth each year.7 They also inject competition into the marketplace. Competition brought on by small businesses push incumbent businesses towards innovation, raises worker’s wages by offering alternatives, and drives down high profit margins that accrue disproportionately to the already rich and powerful.

It’s very concerning then that new businesses continue to account for a decreasing share of the economy. In 1980, startups were 13% of all firms, but in 2014, they were only 8% of all firms.8 Even more alarming is the fact that, due to technology, new businesses are not hiring at the clip they used to. In 2017, the average new business hired 4.2 workers compared to 7.3 new workers in 1994.9 So we need more new businesses than in the past to create the same number of jobs.

And while new business growth continues to slow everywhere, certain areas, in particular, have been hit harder than others. In two-thirds of counties, there were fewer businesses up and running in 2015 than there were in 2005. These 2,100 counties had a net loss of 200,000 businesses and 1.2 million jobs. The other one-third of counties have seen increases in the number of businesses (350,000) and jobs (6.7 million) over the same time period.10

What do small businesses do in the face of restricted access to credit from traditional financial institutions? They turn to more expensive means such as credit cards and online lenders. In fact, 62% of small business owners who applied for online lending did so because they thought they had a better chance of being funded that way. This is in spite of the fact that net satisfaction with online lenders is significantly lower than net satisfaction with bank loans. It needs to be easier and cheaper for new, small businesses to get loans.

The Solution: The trillion dollar Opportunity Bank

To provide millions more small business owners with the opportunity they need to earn their own way and create jobs, we propose $1 trillion in new lending over ten years. This sweeping change would radically alter urban, suburban, and rural communities. The Opportunity Bank will do four key things:

- Quadruple the number of government-backed loans available for small businesses

- Reduce the risk of small business lending for banks

- Cut billions in fees for small business owners

- Remove barriers that restrict millions from getting government-backed loans

Quadruple the number of government-backed loans available for small businesses

Sixty-five years ago, Congress established the Small Business Administration (SBA) and its flagship 7(a) loan guarantee program to help facilitate loans that private financial institutions were hesitant to make to small business owners. But just as the startup landscape has changed drastically since the mid-20th century, so too must the government’s role in supporting small businesses.

The Opportunity Bank will redesign and supercharge the SBA’s 7(a) loan program. The Opportunity Bank would be authorized to increase the volume of small business loans guaranteed by the SBA to $1 trillion over the next decade—from $25 billion per year to $100 billion per year. In FY 2016, $25 billion in loan guarantees supported 57,000 small businesses.11 With $100 billion, there should be at least 200,000 small businesses getting SBA loan guarantees each year.

With 200,000 small businesses getting government-backed loans, communities that have been shedding businesses over the past decade can get injected with a shot of opportunity. Small business lending can once again flow into places like Cuyahoga County, Ohio, which lost almost 4,000 businesses between 2005 and 2015, and back into Wayne County, Michigan, which lost almost 3,000 businesses over the same time period.

Reduce the risk of small business lending for banks

Under the current system, banks can apply for loan guarantees from the SBA if they find a loan to be particularly risky. If they are approved for a loan guarantee, the SBA will guarantee that, in the event of default, a certain percentage of the loan (between 75% and 90%) will be repaid to the bank. The Opportunity Bank would change the structure of the guarantee amounts per loan to make it less risky for banks to lend money to startups—especially those looking for smaller lines of credit.

|

Current Guarantee Amount |

New Guarantee Amount |

|

|

Loans up to $150,000 |

85% |

90% |

|

Loans between $150,000 and $700,000 |

75% |

85% |

|

Loans over $700,000 |

75% |

80% |

By increasing the loan guarantee amount, possible default on a loan will be less painful for a bank, thus encouraging them to take more risks with the money they lend out.

Cut billions in fees for small business owners

For the service of providing the guarantee, the SBA charges a fee on the guaranteed portion of the loan, which almost always gets passed onto the borrower.12 But the current fee structure unnecessarily adds extra costs for small business owners—dampening their ability to get credit.

To reduce the cost of lending to small businesses, the Opportunity Bank would restructure the fees charged to the guaranteed portion of the loan in the following way:

|

Current Fee Assessed on the Guaranteed Portion of the Loan |

New Fee Assessed on the Guaranteed Portion of the Loan |

|

|

Loans under $125,00013 |

0% |

0% |

|

Loans $125,000 to $150,000 |

2% |

0% |

|

Loans between $150,000 and $700,000 |

3% |

1.0% |

|

Loans over $700,000 |

3.5% |

1.5% |

Reducing the loan fees will ensure that small business owners looking for an SBA loan get more favorable interest rates. Right now, if a small business owner takes out a $200,000 SBA guaranteed loan, she has to pay a 3% fee on $150,000 (the guaranteed portion). That’s an extra $4,500 in cost to the small business owner. Under the new system, that same small business owner would only to pay a 1% fee on $170,000 (the new guaranteed portion) which is only $1,700. The Opportunity Bank will save thousands of dollars for small business owners all over the country.

Remove barriers that restrict millions from getting government-backed loans

Right now, when a bank denies a loan, the bank can apply for a 7(a) loan guarantee with the SBA. The SBA has its own set of requirements that a prospective borrower must meet before it will approve the loan. They aren’t as stringent as the bank’s, but they’re stricter than they need to be. For example, anyone with payments left on student loans is ineligible for an SBA loan.14 Given the ubiquity of student loans in our society, this is an unnecessary barrier that prohibits millions from accessing government-backed credit. SBA also looks for credit scores that are above 680, which, to be fair, is right around the national average. Digging a little deeper though, 67% of those 30 and younger and 60% of those between 30 and 39 do not have a credit score of 680.15 Credit scores tend to build up over time and this arbitrary threshold disadvantages younger people. There’s also a racial component to this. For example, the average credit score for African Americans tends to be lower than that of other groups: 677 compared to 701 for non-Hispanic whites.

The Opportunity Bank will revamp the process by which small businesses are approved or denied for 7(a) loans, with the emphasis being placed on expanding the reach of the loan program to borrowers who may not have the necessary collateral or credit score. This will be especially critical to ensure equitable access to loans across communities of color, the disabled, and other disadvantaged groups.

How to pay for the trillion dollar Opportunity Fund

We estimate that this proposal would carry a federal cost of $36 billion in its first decade. Currently, SBA covers the entire cost of the loan guarantee program through the fees charged to banks. Because this proposal lowers the fees and increases the amount of guaranteed money, the 7(a) program would require additional federal investment. We estimate that it would require another $3.6 billion per year to fund the changes in the 7(a) program. Here’s how we calculate that number:

Based on estimates from the SBA’s FY 2016 Annual Performance Report, we assume, on average, that a 3% fee is being charged on 80% (the guaranteed portion) of the $25 billion in loans supported. This comes out to $600 million (3% of 80% of $25 billion) in fees that can support $25 billion in lending to small business. Quadrupling the number of loans supported to $100 billion while holding the fees and guarantee amount constant would mean 3% fees on 80% of $100 billion, which is $2.4 billion. Of course, we lower the fees (to roughly 1% on average) and up the loan guarantee amount (to about 90% on average) so we can expect about $900 million (1% of 90% of $100 billion) in fees going forward.

This gives the revenue estimate, but we still need to know how much it will cost to service $100 billion in loans. It’s natural to think that we can just quadruple the current number (i.e. since $600 million services $25 billion in loan guarantees, then $2.4 billion should cover $100 billion in loan guarantees). But there are two factors that will increase the cost of servicing loan guarantees. First, we are increasing the amount of money guaranteed on each loan so about $90 billion out of the $100 billion in loans made will be guaranteed by 7(a) now. Second, we are also increasing the likely default rate of the loans being issued because we are making it less risky for banks to use the 7(a) program and lowering the standards for who is eligible for a loan guarantee. About 16% of SBA loans ($4 billion out of $25 billion) on average do not get fully repaid each year, yet the SBA can cover the cost of servicing $3.2 billion on those loans (80% of $4 billion) with $600 million in fees. Servicing $3.2 billion in debt doesn’t actually cost $3.2 billion because assets are liquefied to pay back the debtors before SBA has to come in with the rest of the money. We’re going to assume that our modifications roughly double the default rate to 30%. Now, we have a 30% default rate on $90 billion of guaranteed loans meaning SBA will have to service $27 billion worth of default each year. We’re now servicing about 9 times the number of loans ($27 billion compared to $3.2 billion), so we’ll need at least 9 times the current amount of fees to do it.

This would put the cost of servicing the new 7(a) program at $4.5 billion per year (9 x $600 million). We are only taking in $900 million in fees though, creating a shortfall of $3.6 billion that would be needed in funding.

There are a number of ways to pay for this proposal including, but not limited to, eliminating the step-up in basis tax provision, ending preferred treatment for capital gains, raising the highest marginal tax rate, or eliminating the carried interest loophole.

Conclusion

With access to credit diminishing in so many communities, it’s time for the federal government to become a partner in helping small businesses grow and flourish. A trillion dollar Opportunity Bank would radically reshape the way credit reaches small business all over the country. These changes to the 7(a) loan guarantee program will inject up to $1 trillion in loan guarantees over a decade so small business owners can get the credit they need to create the business they want. No longer will size be a critical factor in the determination of whether or not you get credit. The Opportunity Bank will ensure that credit flows to small business in the future the way it flows to big business right now. And the Opportunity Bank will become a partner to small business offering guidance and support to all budding entrepreneurs who want the opportunity to earn a good life where they live.