Report Published December 6, 2012 · Updated December 6, 2012 · 14 minute read

Rate Reality

Jim Kessler, Lauren Oppenheimer, & David Hollingsworth

Interest rates on U.S. government debt are likely to rise in the future unless we change our current budget path. Although one cannot predict a precise time when capital markets would eventually punish the U.S., many agree on this: by the time markets signal that the U.S. has too much debt, it will be far too grave to readily correct.

If deficits are so bad, why are interest rates on U.S. Treasury bonds so low? This is a familiar refrain heard in Washington and among some respected voices on the left who believe that a focus on the deficit is an overblown reaction to a manageable problem. They argue that if our debt was really a big deal, investors wouldn’t be supplying us with capital so cheaply.

Yes, Treasury rates are low, though not because of—but in spite of—our massive debt. Today, temporary factors leave many investors paralyzed and uncertain about where to put their money. With once safe economies now in the gutter, U.S. Treasuries have become, in essence, the cleanest port-o-potty at the state fair.

U.S. Treasuries will likely remain the safest debt investment for at least several years whether or not we achieve a broad and balanced budget deal. But absent a deal, for rates to stay low beyond the near term the world has to remain in a very scary and static economic place.

Five Reasons Why Interest Rates Will Eventually Go Up

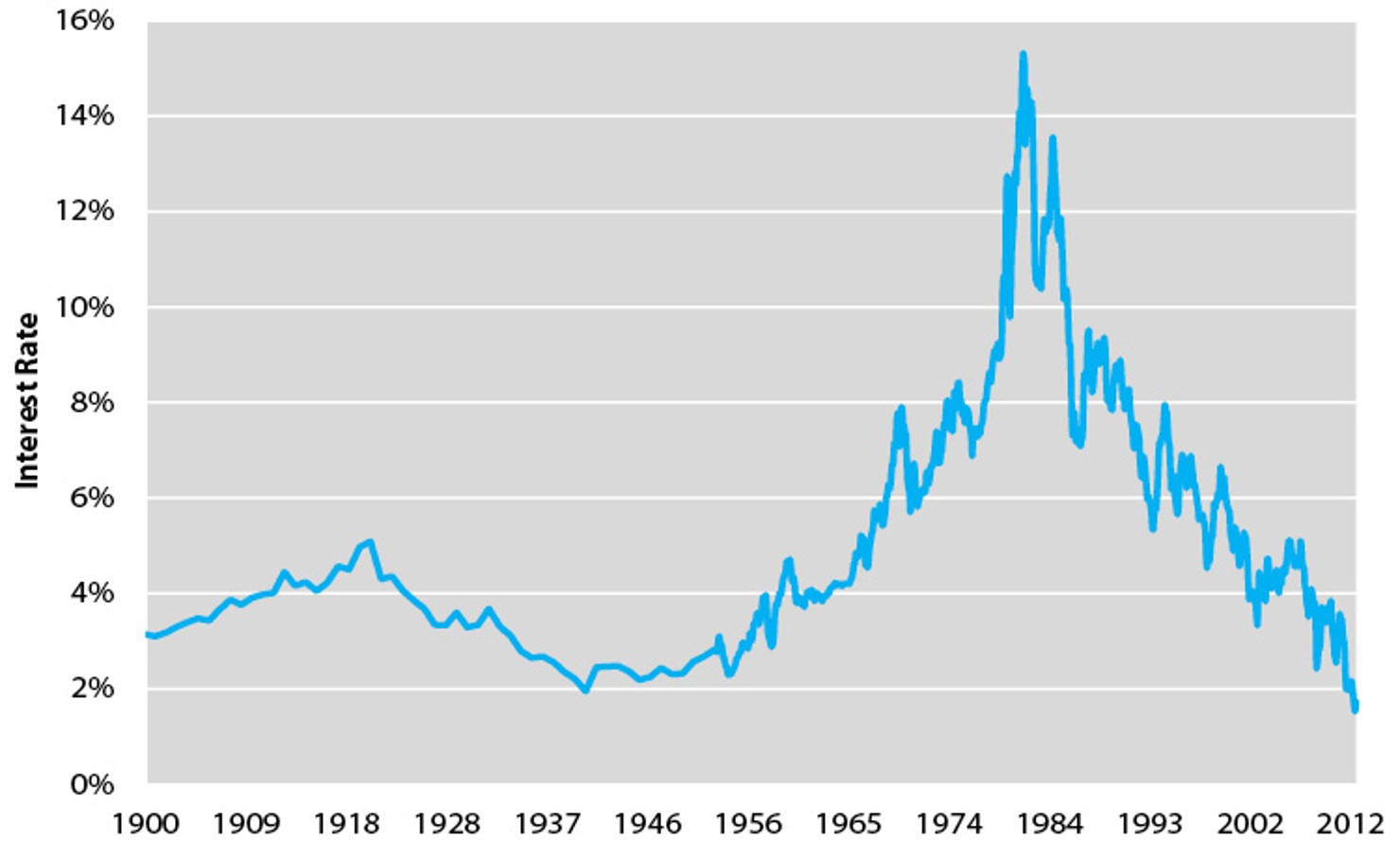

Seventy-one years ago, interest rates on U.S. Treasury bonds hovered around 2%. The Federal Reserve kept government borrowing costs low so the U.S. could sell enough bonds to prosecute the war.1 For the first time since World War II, Treasury bond interest rates have again dipped below 2%. The world is not at war, but it is as uncertain and volatile as any time in recent memory. Will these low rates last?

U.S. Treasury Bond Interest Rate History (1900 – 2012)2

Without a change in our fiscal trajectory, we believe the answer is no. Our interest rates are low for a variety of temporary reasons. These include: a struggling domestic economy, the deep European recession, an economic slowdown in China and developing markets, and low inflation—coupled with Federal Reserve intervention through quantitative easing. These conditions won’t last forever.

It is true that the U.S. has structural advantages that help keep interest rates low, such as the dollar’s status as the world reserve currency and our large and dynamic economy. But we’ve had these same structural advantages for decades, with interest rates varying widely—for example, in the early 1980s rates were consistently above 10%. So our advantages just mean we won’t be Greece, not that we will continue to have historically low rates indefinitely.

Below are 5 reasons why U.S. interest rates are likely to rise, particularly if Congress fails to come to a deal that reduces our deficits in the medium and long term.

1) Europe gets its act together.

Is a European recovery realistic enough to be a reason our interest rates could go higher? Not immediately, but in the future—yes, absolutely.

Realize this: if you put the entire European Union together, the size of their economy and collective debt obligations are not too much different from ours. Europe’s problems are as much political as economic. Investors don’t believe that the Eurozone—the 17 European countries that share the euro—have in place strong enough institutional mechanisms or a cohesive enough political structure, to solve its problems.

Yet over the past several years, Eurozone members have been inching closer to a political solution by more fully integrating the continent—including the development of a single banking supervisor for all Eurozone countries which would help stabilize the financial sector. Serious obstacles clearly remain, but it is certainly plausible that over the next several years Europe will move to a level of integration that satisfies investors, making the bonds of European countries an attractive alternative to U.S. Treasury bonds. In fact, some investors are starting to have greater faith in Europe getting its act together before the United States. In short, a much stronger Europe cannot be discounted down the road.

U.S. vs. EU (2011)

U.S. | EU | |

Annual GDP Growth3 | 1.7% | 1.5% |

GDP ($ trillions)4 | $15 | $17.6 |

Market Capitalization ($ trillions)5 | $15.6 | $7.6 |

Debt to GDP6 | 73% | 83% |

Fortune 500 Companies7 | 132 | 161 |

2) China cuts back on buying Treasury Bonds.

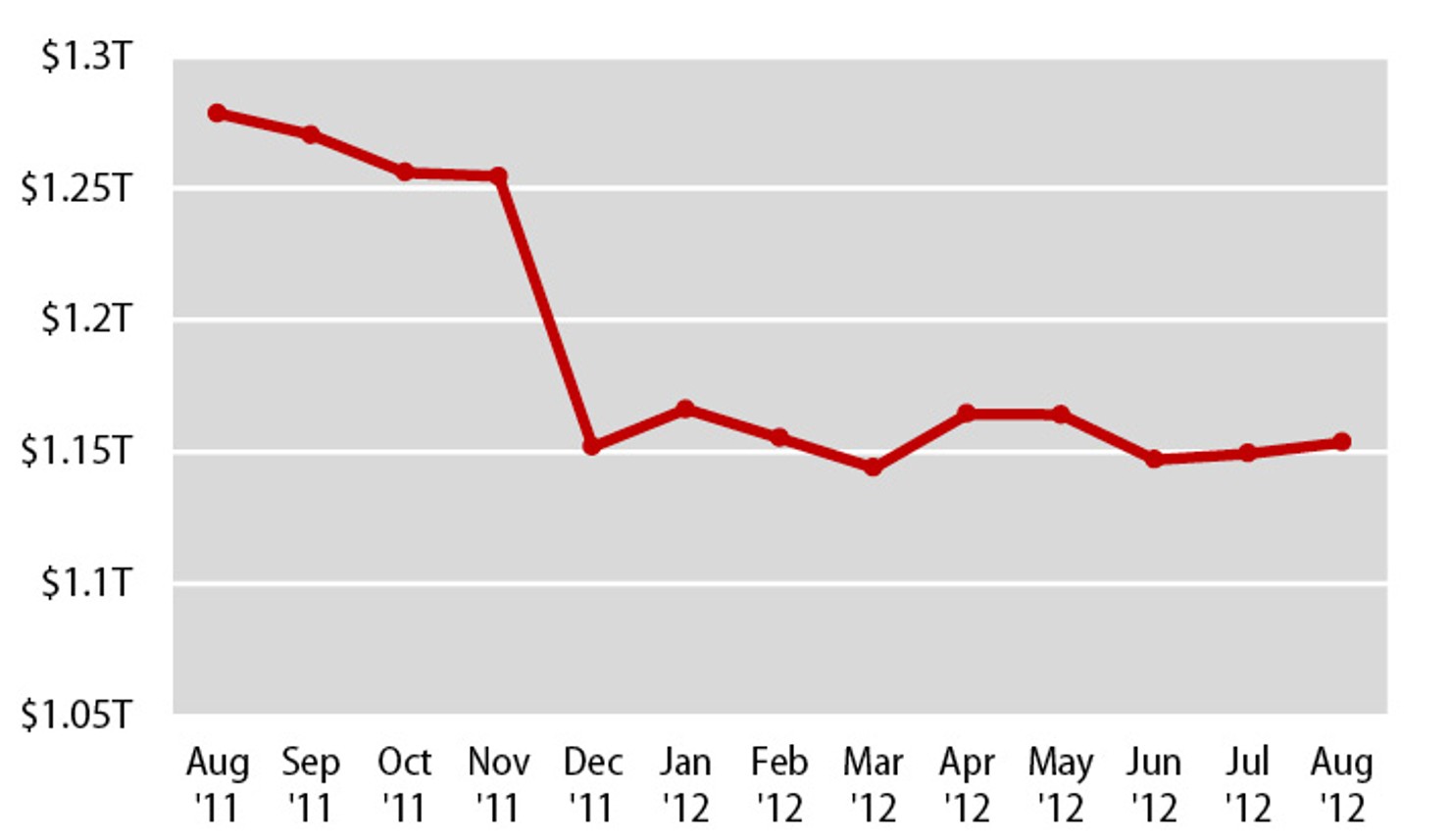

Our ace-in-the-hole has been China. Currently, China is the largest foreign holder of U.S. government debt, with nearly $1.2 trillion in holdings. With the accumulated U.S. dollars from their trade surplus, China buys Treasury bonds—in part to devalue their currency, making their exports cheaper. However, there is evidence that China is seeking to diversify its portfolio and buy fewer Treasury bonds.8 If China continues to invest in Treasury bonds on the same scale it has been for the past few decades, some investors believe that economic historians will look back at these purchases as the worst investment of the 21st century.

Why? Look at it this way. China has stowed away a trillion dollars in wealth that it accumulated through trade and economic growth in investments that pay a real interest rate—the nominal interest rate minus the rate of inflation—of less than 1%. Suppose everything you put in your 401K earned 0.5% in real growth; would you be satisfied with that kind of return? That’s the return China is getting for a safe investment and a cheaper currency. And that is why the Chinese government has approached investors to explore options for investing in European debt instruments and equities as an alternative to Treasury bonds.

The question is whether China is “hedged to wedge?” In other words, is China stuck with U.S. Treasuries because selling them would both devalue their remaining assets and appreciate their currency? Perhaps the answer can be found in this statistic: over the last year, China’s holdings of U.S. Treasuries have declined by $125 billion, or 9.8%.9 This could indicate that China is exploring options for a way out of its marriage with U.S. government debt.

Less reliance by China on U.S. Treasury bonds will have mixed results for the U.S. economy. But it will certainly put upward pressure on interest rates in the future.

Chinese Holdings of U.S. Treasury Bonds ($ trillions)10

3) Interest rates regress toward historical averages.

There are no crystal balls, but one of the most powerful forces in the market is regression toward the mean. In other words, what goes up must come down, and vice versa.

U.S. Treasury bond yields currently reside in the 99th percentile of rates over the past 112 years—from high to low.11 Over the past fifty years, the average interest rate for 10-year U.S. Treasury bonds is 6.7%; over the last 30 years it’s 6.5%.12 On November 27, 2012, the interest rate on a10-year U.S. Treasury bond was 1.64%.13 Our interest rates are likely to regress towards the mean at some point.

One factor that could push interest rates toward their historic average is the full recovery of the U.S. economy. With so much slack in the economy, interest rates can remain low without fear of overheating or inflation rearing up. However, when the economy picks up and achieves its full potential, interest rates are likely to rise. There will be increased demand for capital—businesses will expand and hire more workers and households will be less risk-averse and buy more goods and services. The Federal Reserve has pledged to keep interest rates low until the economic recovery is in full swing, but it has not pledged to keep interest rates low once the economy is nearing its full potential. We are all rooting for a robust economic recovery, but this also means servicing U.S. debt will become more expensive.

There are some who feel differently; that low rates are permanent. This may be so, but we should be wary when we convince ourselves that we have reached a new economic era—that “this time is different.” The housing crisis came about because of a belief that prices would never retreat. The tech bubble was fed by the belief that technology had permanently changed the productivity of the economy such that price-to-earnings ratios were meaningless. The “great moderation” led us to believe that major ups and downs to the economy were a thing of the past. Now the belief is that rising interest rates are relics of a different age. We’ve been down this road before.

4) QE Infinity will be finite.

Unlike Eurozone countries that do not have their own central bank, the Federal Reserve can always keep government borrowing costs low because it can print money to purchase Treasury bonds. The latest round of quantitative easing—known as QE III or QE Infinity—has the Federal Reserve pledging to buy up U.S. mortgage-backed securities to ensure low interest rates for at least the next several years. If investors sour on U.S. Treasury bonds, the Federal Reserve could step in to purchase Treasury bonds to keep government borrowing costs low. They can do this, theoretically, forever.

But this leads to two problems. One, with continued Treasury bond purchases by the Federal Reserve, inflationary expectations would eventually enter the economy. When the economy is operating below full capacity—as the United States clearly is—Federal Reserve purchases do not pose serious short-term inflationary concerns. However, if the Federal Reserve was compelled to print money to buy Treasuries as the economy returns to full capacity, inflationary expectations would likely rise.

Inflation will not take off in the next few years; tales of hyperinflation around the corner are highly exaggerated. But once inflationary expectations are introduced into the economy, they are very difficult to reverse, which means the U.S. could eventually find itself back in 1970s-style stagflation—an economic environment with both low growth and high inflation.

In short, if investors won’t provide capital to the U.S. government cheaply, the Federal Reserve would be forced to purchase Treasuries to maintain low rates, making significant inflation at some point in the future more likely.

The second problem is that the Federal Reserve controls short-term rates but only influences long-term rates. Other factors—including future expectations of monetary policy and the performance of the economy—also play a role in determining long-term rates. While the Federal Reserve is usually successful at controlling long-term rates in normal economic times, it becomes more difficult in extreme financial conditions. A study by Canada’s central bank, the Bank of Canada, found that cuts in short-term interest rates during a recession do not automatically lead to a corresponding fall in long-term rates.14

If America doesn’t solve its fiscal problems, and our economy continues to limp along while other economies revive, the Federal Reserve may not be able to keep interest rates down throughout the economy. Many businesses and households could struggle to borrow at affordable rates despite low short-term interest rates and government borrowing costs. Low rates can’t force lenders and investors to part with their cash.

This is why QE Infinity can’t last forever. At some point, monetary policy will cease to be effective, and inflationary pressures will be difficult to contain. Investors would seek more promising investments off our shores, and economic growth would be increasingly difficult.

5) Markets won’t give an early warning of problems

When the markets say you’ve got a problem; you’ve got a crisis. There is a misconception in Washington that markets are like smoke detectors, giving warnings at the first hint of trouble. There is a belief that if America’s debt truly starts to get out of control, markets will begin to gently bump up interest rates, giving us plenty of time to change our fiscal trajectory.

Don’t count on it. Capital markets are not great at pricing long-term risk. Some market participants don’t think capital markets see beyond a time horizon of a few years. But investor sentiment can turn quickly. Market reactions are often non-linear—meaning that the price for stocks and bonds can experience large fluctuations in response to incremental changes in circumstances.

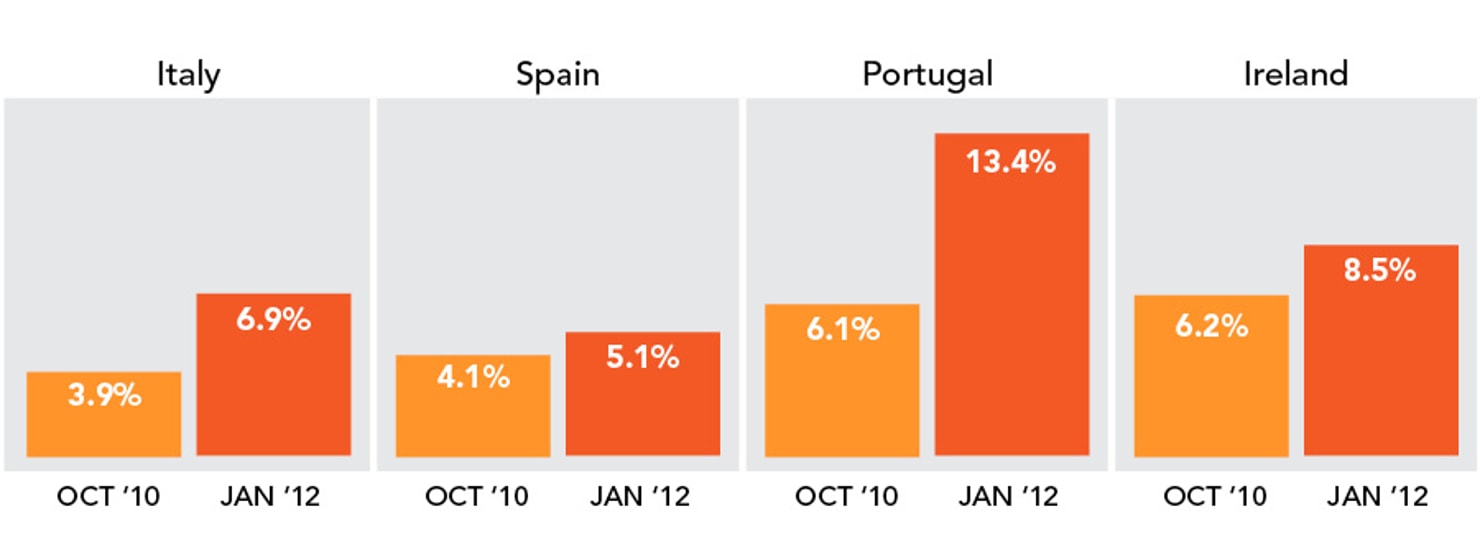

As late as January 2010, Greece was able to borrow at a 5.5% interest rate—2% higher than the rate on German bonds, considered the safest in Europe.15 Just a year later, Greece could only borrow at 12.5%, nine-points higher than German interest rates.16 And of course, we’ve seen the deterioration in their creditworthiness—and economy—since then.17 By the time the markets woke up to Greece’s problems, and raised interest rates on their debt, the cake was already baked. It was far too late for Greece to make policy adjustments to prevent a crippling recession.

If we fail to correct our current fiscal trajectory, the markets will eventually lose faith in our ability to service our debts. Investors will require more compensation to account for the increased riskiness of U.S. Treasury bonds. And the transition could be sudden, leaving America with little room to maneuver. When investors judge that the pain it takes to solve a country’s problems is too great for political leaders to bear, they quickly head for the exits.

Chinese Holdings of U.S. Treasury Bonds ($ trillions)18

Conclusion

Some Washington policymakers have been lulled into complacency by our historically low interest rates, thinking there is plenty of time to fix our deficits. But low interest rates do not mean that the markets are content with the U.S. fiscal situation. We are merely the cleanest dirty shirt in the closet.

At some point, the temporary measures that keep our interest rates low will hit an expiration date. We cannot predict that date, but when it comes it is likely to be sudden and painful.

This December, Washington has the greatest opportunity in decades to deal with our fiscal crisis. Many market participants believe a balanced deal would lead to growth in both the short and long term. As the Australian Foreign Affairs Minister put it, “America is just one budget deal away...from ending all talk of America being in decline.”19

But the key is a balanced deal. Markets realize that haphazard spending cuts and tax increases do not improve the growth prospects of countries. An all revenue plan would be frowned upon by capital markets; an all spending cuts plan would be looked down upon as well. Investors don’t believe that all government debt is bad, but are concerned that very little of U.S. government debt is productive.

A balanced deal would kick-start a virtuous cycle that our recovery has been missing. Capital markets would move from a “risk off to a risk on” economic environment. In a “risk off” state of mind investors believe it is wiser to hold on to money than to spend it on a new hire, invest it in a new plant, put extra products on the shelf, or conduct new research. They are in a wait and see mode.

When the stage is set for economic growth, investors move to a “risk on” mode. They believe it is riskier to hold onto money than to spend it. The danger, as they see it, is not having enough products on shelves, not enough research to develop new products, and not enough people and capacity to produce. A balanced deal would flip the switch from risk off to risk on.

We don’t need to solve everything at once, reducing our deficits too fast and too steeply. Europe has shown the folly of closing deficits too quickly. We must maintain investments in infrastructure, education and basic science; we must continue to help those still struggling under the weight of our underperforming economy. But we must change the trajectory of our deficit over the medium and the long term, setting the stage for fiscal health and vigorous economic growth.

In other words, we don’t need to panic. We just need a balanced deal.