Report Published October 10, 2018 · 44 minute read

Industry Matters: Smarter Energy Use is Key for US Competitiveness, Jobs, and Climate Efforts

Jason Walsh, Ryan Fitzpatrick, & Mykael Goodsell-SooTho

Introduction

In recent years, the conversation on energy in the United States has shifted from a theme of scarcity to one of abundance. The surge in domestic production of oil and gas alone, which provides a significant advantage to the US economy, may also have drained some of the urgency and enthusiasm from efforts to improve energy efficiency while achieving economic growth targets, particularly in the industrial sector. Yet even in this age of abundance, smarter, cleaner, and more efficient energy use could still provide enormous benefits to American industry, workers, and the country as a whole. Greater national focus on improving industrial energy use could help to:

Increase Economic Competitiveness and Job Growth - US manufacturers are the cornerstone of our nation’s industrial sector and a vital source of good-paying jobs. By improving energy performance, we can help businesses reduce waste, create and sustain jobs, save money, and invest in long-term growth.

Achieve Climate Goals - The industrial sector is America’s biggest end-use emitter of greenhouse gases (GHGs). Unless we have a strategy to reduce these emissions, we have little chance of hitting our climate targets.

Keep Up with Market Trends – Businesses, cities, states, and entire countries are enacting policies to promote cleaner and more efficient energy use, including standards and incentives that will impact major industries. By helping our manufacturers stay on the forefront of changing energy demand, the US can ensure their ongoing access and competitiveness in evolving global markets.

This report examines each of these reasons for making industrial efficiency and emissions reduction a national priority. It also lays out a number of clear, achievable pathways to saving energy, increasing competitiveness and cutting carbon in US industry, including wider use of industry best practices, increased deployment of existing technologies, and accelerated innovation of new technology solutions. These pathways offer a useful guide for future policy discussions between government, industry, labor, and other stakeholder groups.

1. Strengthening the Bottom Line for US Businesses and Workers

An energy and emissions strategy for American industry must center on manufacturing, the most economically important and energy reliant part of the U.S industrial sector.1

The Value of US Manufacturing

Manufacturing is a critical component of the US economy. With a total output valued at $2.17 trillion, American manufacturers are responsible for 11.8% of the nation's GDP.2 Manufacturing is also critical to US workers. In 2016, manufacturers directly employed nearly 12.5 million people with an average hourly wage of $26.50.In addition, each full-time job in manufacturing creates 3.4 full-time equivalent jobs in nonmanufacturing industries—the highest multiplier in the US economy. 3

In 2017, the total US economy consumed an estimated 97.8 quadrillion Btu of energy, or 97.8 quads. The industrial sector consumed nearly one third of that amount (31.5 quads).4 EIA expects total national energy consumption to increase 4% by 2025, with nearly all of that growth coming from industry.5

This massive and growing energy consumption within the industrial sector is heavily concentrated in a few key areas. Manufacturing is by far the most energy-intensive component of the sector, accounting for 75% of industrial energy use.6

That share is even further concentrated within a handful of sub-sectors known as energy-intensive manufacturers (EIMs), which dominate energy consumption in manufacturing. These manufacturers convert natural resources into basic materials through processes that require high energy inputs, including high-temperature heat. These processes convert, for example, iron ore, bauxite, petroleum, lime stone, silicon dioxide and biomass into iron and steel, aluminum, chemicals, cement, glass and paper—all of which are essential material building blocks on which our economy and society relies. If the top five energy consuming manufacturing sectors in the US were their own country, they would rank 9th in the world in terms of total energy used.7

If the top five energy consuming manufacturing sectors in the US were their own country, they would rank 9th in the world in terms of total energy used.

Major opportunity for savings

Despite advances in industrial energy efficiency, and recognizing the inherent thermodynamic losses that are part of industrial processes, a large amount of the energy used by US manufacturers is still wasted. An astounding 64% of the primary energy consumed by US manufacturing is “lost” during transmission, power and steam generation, process heating, HVAC and lighting use, and other activities.8

We can do better. A significant percentage of manufacturing energy that’s wasted can be saved, which in turn saves money that manufacturers can otherwise use for capital and workforce investments that make them more productive and competitive.

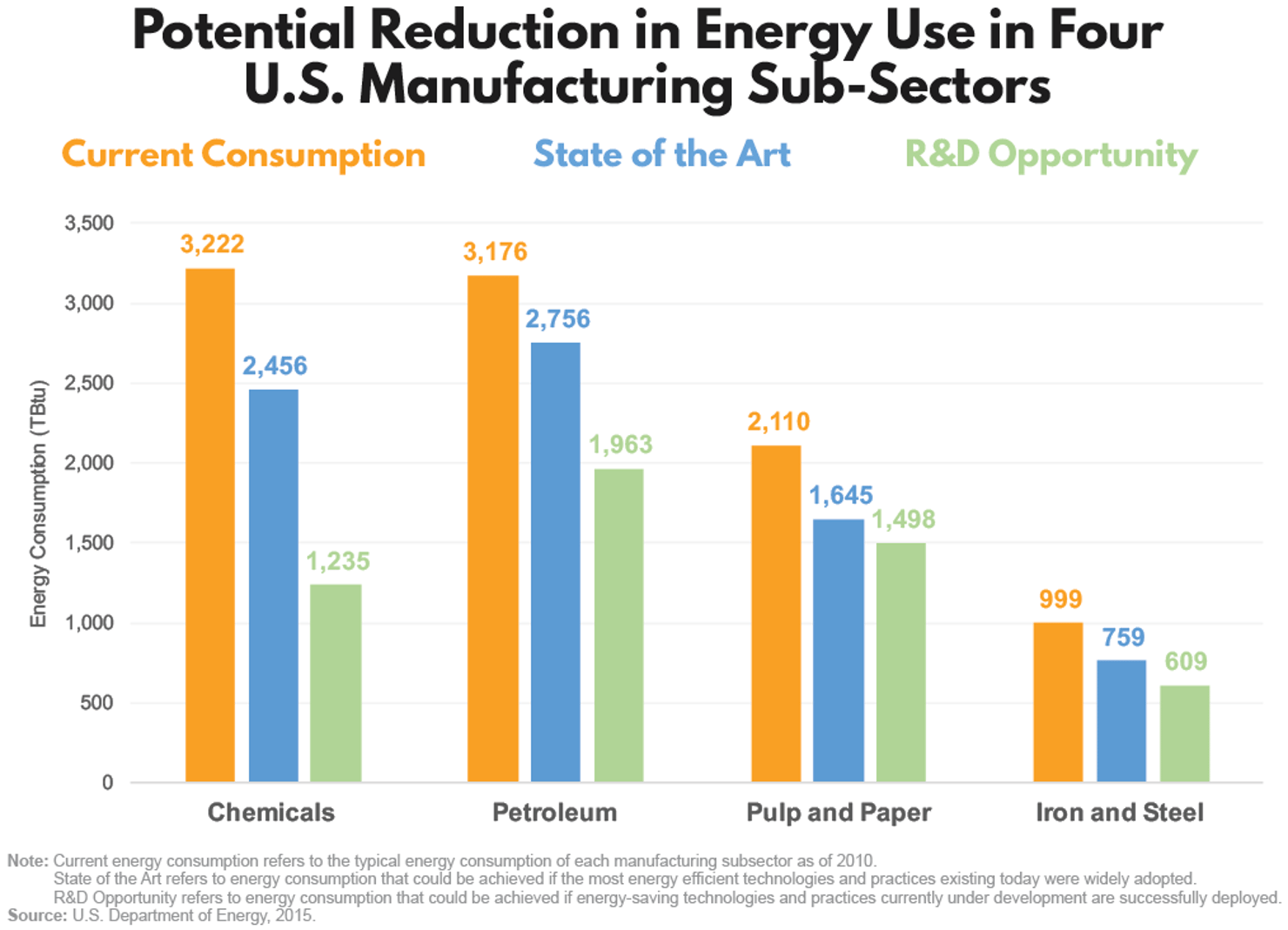

The Department of Energy (DOE) produced a series of studies that provide technology-based estimates of potential energy savings opportunities in four EIM sub-sectors.9

The studies analyzed two energy savings opportunity ‘bandwidths’: (1) the “current opportunity” bandwidth represents energy savings, compared to current typical energy consumption, if the best technologies and practices available are used to upgrade production; and (2) the “R&D opportunity” bandwidth represents additional energy savings available, after realizing the current opportunity, if applied R&D technologies under development are deployed.10 As the table below makes abundantly clear, the opportunity to save energy and reduce emissions among EIMs is enormous.

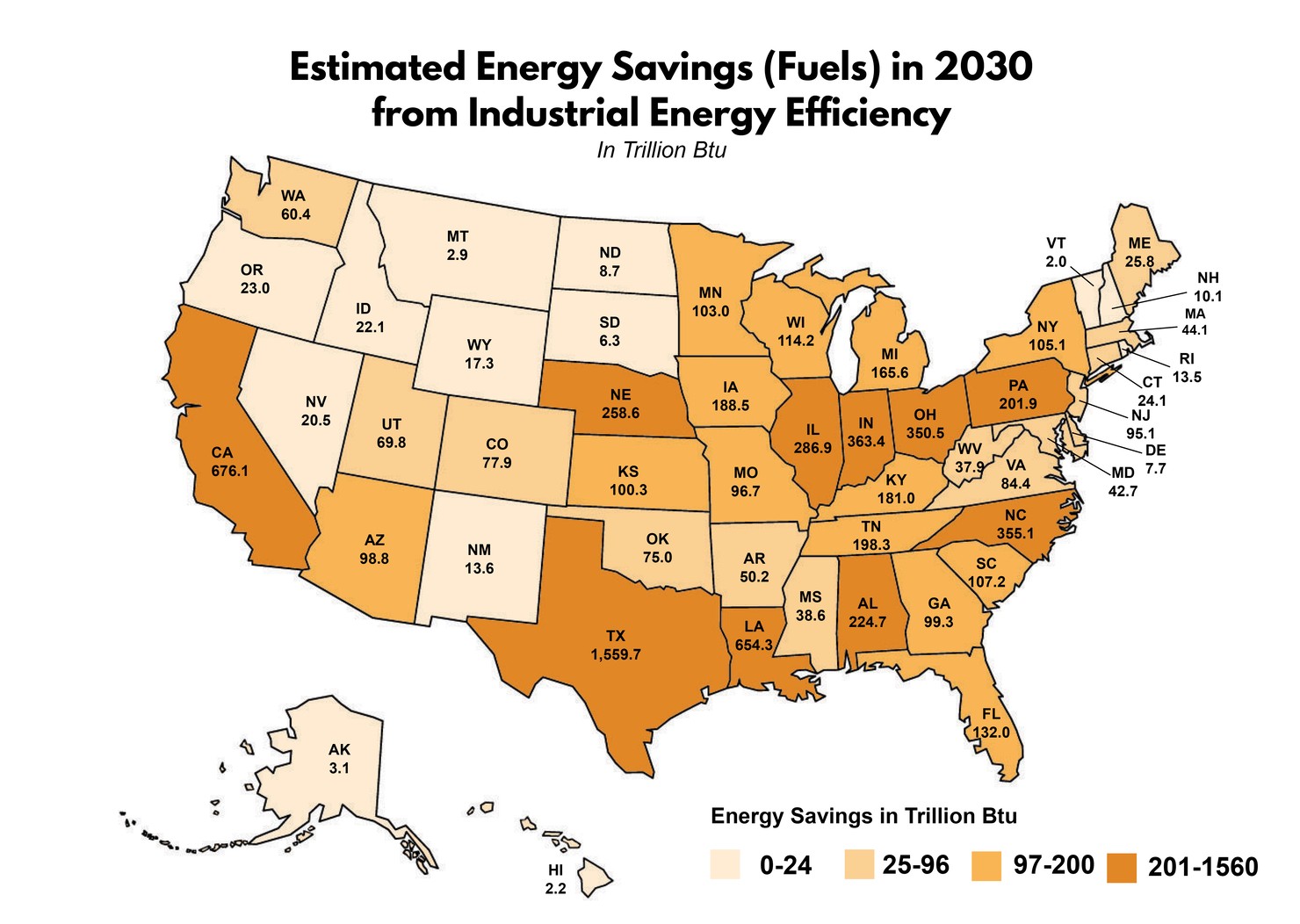

Another way to analyze industrial energy savings opportunities is on a state-by-state basis. In 2016, DOE used economic and energy intensity projections to estimate the potential industrial energy savings in all states by 2030 if the industrial sector doubled its rate of energy efficiency improvement. Opportunities were found in every state, with a regionally, economically, and politically diverse group of states topping the list of unrealized savings (Texas, California, Louisiana, Indiana, North Carolina, and Ohio).11 If industries in just these six states were to meet DOE’s projections, the energy they saved would be equal to 4% of all primary energy used by the entire country.12

If industries in just these six states were to meet DOE’s projections, the energy they saved would be equal to 4% of all primary energy used by the entire country.

It’s clear that energy savings opportunities are abundant. If US manufacturers can cost-effectively realize these savings by making capital investments in more energy efficient technologies and practices they will increase their profits, their ability to reinvest, and their economic viability. And because U.S manufacturing is such a critical supplier and catalyst for the overall economy, these benefits will also accrue to workers and businesses across all economic sectors. It will also position US manufacturers, and the nation as a whole, to be winners in perhaps the most important global economic race of the 21st century.

Jobs and Opportunities for American Workers in a Changing Economy

America’s changing energy economy is already reflected in the US workforce. According to the 2018 U.S. Energy and Employment Report (USEER),13

substantial numbers of American manufacturing workers are employed in the production of energy efficiency, clean energy, and low carbon emission technologies. For example, the USEER found that 315,578 workers were employed in manufacturing ENERGY STAR-rated appliances and other energy efficiency-certified building and lighting products. Another 476,338 workers were employed in automotive manufacturing subsectors for component parts that increase vehicle fuel economy.

The USEER also found that almost one of every five US construction workers (1.27 million out of 7.1 million) support the construction or installation of energy efficient technologies.14 This is a strikingly large proportion of the construction workforce, particularly given the uneven mix of state and federal policies that incentivize energy efficiency. Indeed, one analysis found that if all states adopted a few proven energy efficiency policies, they could create over 600,000 new jobs.15 These figures illustrate the job-creating potency of a business model in which the savings from reducing energy waste can be reinvested to undertake even more ambitious energy efficiency efforts—a virtuous cycle that also supports steady employment for boilermakers, pipefitters, glaziers, insulators, and other skilled craftsmen and women.

It’s worth emphasizing that the men and women employed in the manufacturing and construction sectors are disproportionately workers without a four-year college degree, often considered a proxy measure for membership in America’s working class. This group has been on the losing end of structural trends in the overall labor market over the past few decades, but manufacturing and construction jobs provide a chance for working class Americans to climb the economic ladder.

A proven means to climb that ladder are joint labor-management apprenticeship programs prevalent in both manufacturing and construction fields. This “earn while you learn” system provides high-quality skills training, well-defined points of job access, and long-term career pathways. Apprenticeship programs are also central to Project Labor Agreements, or Community Workforce Agreements, that are often used for publicly funded infrastructure projects, and which enable the training and hiring of workers from local and underserved communities.

The bottom line: policies and investments that help create and sustain good-paying manufacturing and construction jobs in turn enable greater equity and mobility in a US economy that badly needs more of both.

2. Industrial Sector is Key to Meeting Climate Goals

To minimize the risk of severe damages from a changing climate, the US and other nations need to drastically reduce the amount of carbon dioxide and other GHGs they release into the atmosphere.16 This will require significant emission cuts in all major segments of the economy. The US has been fairly successful in cutting carbon from the power sector in recent years, thanks to strong consumer demand for renewable energy and the switch from coal to natural gas. National standards for vehicles have had a significant impact on fuel efficiency and emissions in the transportation sector.17 Unfortunately, the US has not taken such substantive steps to help its industries move in the same direction—a shortcoming that could put even long-term climate goals out of reach.

Industry’s share of emissions is larger than you think

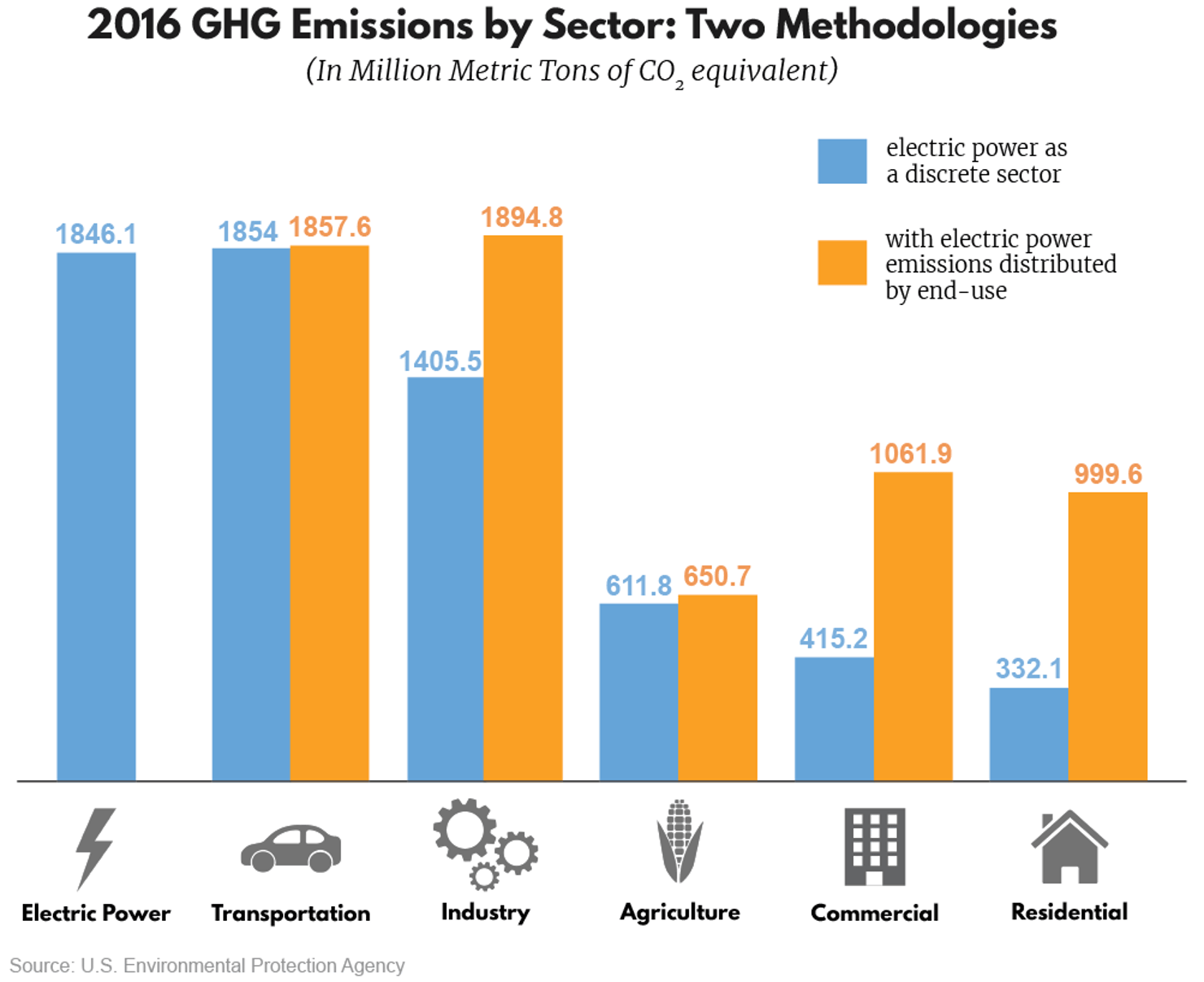

The electric power sector has historically been the largest source of greenhouse emissions in the US, though the transportation sector now surpasses it by a narrow margin. According to the Environmental Protection Agency’s “U.S. Greenhouse Gas Inventory,” transportation and power each accounted for 29% of emissions in 2016, with the industrial sector assuming its usual position as distant third, with 22%.18 Its smaller share of emissions could help explain why there’s been somewhat less focus and urgency around cutting carbon in industry, compared to power and transportation.

EPA’s Inventory has another method of accounting for emissions, though; and it paints this situation in a much different light. Instead of treating power generators as their own discrete sector, this less-referenced methodology distributes emissions from power generation to the end-use sectors that actually consume this electricity. By this metric, the industrial sector is actually the nation’s largest source of greenhouse gas emissions. In 2016 industry was responsible for 1,894.8 million metric tons (MMT) of carbon dioxide equivalent (CO2e), or 29% of the U.S total.19

The industrial sector is actually the nation’s largest source of greenhouse gas emissions. In 2016 industry was responsible for 1,894.8 million metric tons (MMT) of carbon dioxide equivalent (CO2e), or 29% of the U.S total.

This methodology clearly suggests a need for increased attention and urgency around industrial emissions. Emissions from a range of economic activities like construction and mining are included in the “Industry” designation. But similar to industry’s energy consumption, GHG emissions from industry are also concentrated within manufacturing. One analysis of the most energy intensive manufacturing plants in the US, representing less than 0.5% of all US manufacturing facilities, estimated that they were responsible for roughly 25% of US industrial sector emissions, the equivalent of 5% of all U.S GHG emissions.20 This provides yet another reason to make manufacturers a priority focus of any effort to promote smarter energy use and emissions reduction in American industry.

Electricity use is only part of industry’s challenge

Including emissions from the electricity used for things like motors, ovens, space heating and cooling, lighting, etc. is enough to push the industrial sector above other end users. But these offsite or “indirect” emissions from electricity are still a relatively small portion of industry’s overall emissions footprint. Of the total of CO2e that industry emitted in 2016, only one quarter were indirect emissions.21

The remaining industrial emissions are “direct” emissions, which typically occur on-site at manufacturing facilities. The main sources of direct emissions from industry are:

- Combustion of fossil fuels like natural gas and petroleum for process energy (e.g., heating for furnaces, kilns, and dryers);22

-

Chemical reactions that occur when raw materials are transformed into products (e.g., cement and ammonia);23 and

-

The production and use of hydrofluorocarbons (HFC’s), highly potent GHGs used in refrigeration, air-conditioning, aerosols, and foams.24

The lesson here is that transitioning the grid to renewables and other low-carbon power sources is helpful in addressing industrial emissions, but it can only do so much. Successfully cutting carbon in this sector will require significant onsite action at these facilities.

Industrial emissions could surge if steps aren’t taken

Though the industrial sector has not been a primary focus of energy and climate policy, industrial GHG emissions have decreased in the US since 1990, with some sub-sectors dropping dramatically over that period of time. For example, emissions from iron and steel production dropped by almost 60% between 1990 and 2016 (from 99.1 MMT CO2e to 41.0 MMT).25 This was the result of improvements in energy efficiency, but even more importantly a shift from ore-based production to increased recycling of scrap steel.

Arguably, however, the most significant driver of industrial sector GHG reduction has been the structural shift in the US economy toward services and away from production of manufactured goods. This is by no means a positive trend from a global GHG emission standpoint. Much of the manufacturing that the US loses is simply offshored to some other country, and the emissions (in addition to the jobs) go along with it—something technically referred to as “carbon leakage”. Manufacturers in these countries tend to use less energy efficient technologies and are subject to less stringent pollution standards, so global emissions end up higher than they would have been if manufacturing had stayed in the US.26

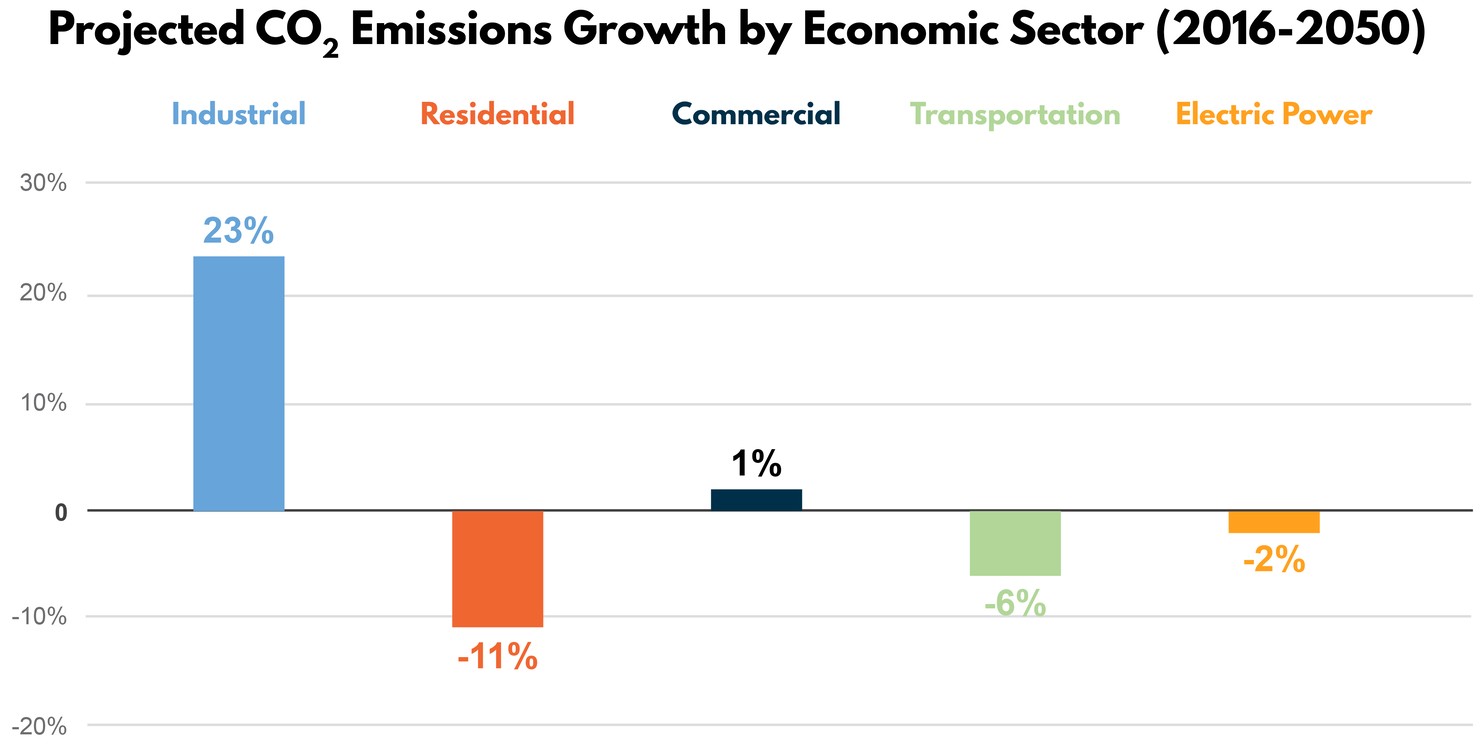

Regardless of what has been driving it, the decades-long trend of decreasing industrial emissions in the US may be reaching its end. The US Energy Information Administration’s (EIA) reference case projects that energy-related CO2 emissions from industry will rise 23% between 2017 and 2050, while other economic sectors see flat or declining emissions.27 Much of this growth is attributed to expanded output driven by sustained low prices for natural gas, especially among manufacturers like chemicals producers that use gas as a fuel and feedstock.

3. Domestic and International Drivers of a Carbon-Constrained Economy

As the impacts of energy consumption and climate change become harder to ignore, public policy and consumer demand worldwide are curving inexorably toward efficient, low-emissions processes and products. Washington should acknowledge this trend in global markets and pursue policies and investments that will help US manufacturers stay ahead of it. If we fail to heed the international and domestic warning signs discussed below, American industry could find itself racing to catch up to the world economy instead of leading it.

Signs of a global trend

Even though the US has announced its withdrawal, the Paris Climate Agreement will still put significant downward pressure on GHG emissions—including emissions from industry. Every other nation on the planet remains in the Agreement (or, in the case of Nicaragua and Syria, plans to join). And a number of our biggest international economic competitors have laid out emission reduction strategies specifically for the industrial sector, including China (see Appendix A), Japan, and the EU.28

National policies that put a price on carbon are already impacting many U.S manufacturers. Over 40 countries use some form of carbon-pricing mechanism, either an emission-trading system or a carbon tax.29 US-based multinational companies that use energy in any of these countries must already account for GHG emissions, which can lead to voluntary reduction programs as well as the development of national reduction policies.30

Whether they’re required to or not, many multinational companies are choosing to adopt an internal carbon price because they—or their shareholders—view carbon risk management as a business imperative. As of 2017, almost 1,400 companies worldwide were disclosing their current or planned use of carbon pricing, an 11% increase over 2016.31

Technology investment is another good indicator of where the sector is headed. Clean energy is expected to be one of largest markets of the 21st century. According to Bloomberg New Energy Finance (BNEF), global clean energy investment in 2017 was $333.5 billion, 3 percent above 2016’s total and the second highest investment year on record. With countries around the world racing to develop, deploy, and export these technologies, US manufacturers face serious competition for these lucrative markets. China was home to the largest sum of clean energy investment in 2017 at $132.6 billion, while the US came in a distant second with $56.9 billion.32 When it comes to catalyzing innovation, the US fell behind eleven countries in Europe and Asia in terms of government investment in energy RD&D (as a percentage of GDP) in 2015.33

When it comes to catalyzing innovation, the US fell behind eleven countries in Europe and Asia in terms of government investment in energy RD&D (as a percentage of GDP) in 2015.

In particular, the US is falling behind in some of the most cutting-edge and important clean energy technologies for industry. For instance, a copper mine in Chile has pioneered the use of solar thermal technology for refining, generating more than 80% of the heat it needs with zero emissions.34 Another example is Dubai, where the world’s first steel plant equipped with carbon capture commenced operation in 2016. The government of the United Arab Emirates strongly backed this particular project, noting that it now gives domestic industries and workers a leg-up on what could be a growing export market for industrial carbon capture and low-carbon steel.35

Domestic forces also pushing industry toward cleaner, more efficient energy use

Regardless of current inaction at the national level, American states, cities, and businesses are adopting explicit emission reduction targets, clean energy goals, and other policies that will shape their investment and procurement decisions. Many of these activities could create opportunities for some domestic manufacturers, as well as challenges for those who fail to keep up.

Ten states have adopted legally binding carbon pricing regulations, including California, which is implementing the country’s first economy-wide cap and trade program. The other nine are northeastern states participating in the Regional Greenhouse Gas Initiative (RGGI), essentially a CO2 cap and trade system in the electricity sector. Since January of 2018, New Jersey Governor Phil Murphy signed an executive order directing the state to rejoin RGGI, and Virginia Governor Ralph Northam proposed legislation that would enable his state to join for the first time. Meanwhile, 29 of the largest US cities have codified GHG emissions reduction targets, and 43 cities have committed to 100% clean energy goals.36

In what may have the most direct and immediate impact on major manufacturing sectors, California recently adopted a first-of-a kind procurement requirement called Buy Clean California. The law requires state-funded infrastructure projects, such as highways and bridges, to use building materials (including steel, insulation, and glass) that meet low carbon intensity standards.37 Though it’s only one state, California is the world’s fifth largest economy and spends $10 billion annually on infrastructure—a market large enough to potentially influence suppliers well outside its borders.38

Numerous US manufacturers have made commitments to purchase clean energy and reduce GHG emissions, which will have significant impacts on their operations and domestic supply chains. 132 of America’s largest manufacturers have established GHG reduction targets, 40 of them have set renewable energy goals, and 190 companies are participating in a partnership with the federal government to reduce energy intensity across their US operations.39

Numerous US manufacturers have made commitments to purchase clean energy and reduce GHG emissions, which will have significant impacts on their operations and domestic supply chains.

International and domestic actions to reduce emissions and energy consumption show a clear and escalating pattern, and one that will certainly have an impact on markets for manufactured goods. By taking steps now to maximize efficiency and clean energy use, US manufacturers can increase their ability to remain competitive as global business priorities evolve. With a clear and focused national strategy, the federal government could support this shift among American manufacturers and the workers they employ.

4. Pathways to Reducing Industrial Sector GHG Emissions and Energy Waste

Any strategy to reduce GHG emissions and capture energy savings from industry must recognize several factors that are unique to the sector:

- The diversity and complexity of the US industrial sector is staggering. It consists of hundreds of sub-sectors, many of which rely on processes and technologies that are unique to that particular sub-sector. As such, reducing energy waste and emissions in the industrial sector will require a wider array of solutions than any other economic sector.

- As the data from the Inventory reveal, nearly three times as much industrial emissions result from off-grid processes as from grid-sourced electricity. This explains why the transformation of the power sector to lower carbon sources to date has had a limited impact on industrial emissions, and why it’s so important to look for on-site solutions.

- There are limits to what portion of industrial GHGs can be avoided, based on the laws of thermodynamics and chemical reactions for which there simply are no emissions-free alternatives.40 For the foreseeable future, the only way to deal with a significant portion of industrial emissions will be to capture, potentially utilize, and permanently sequester them.

- With its extensive supply chains, the manufacturing sector is uniquely positioned to enable more efficient energy use and lower GHG emissions in other end-use economic sectors, such as transportation and buildings.

What follows is a summary of what we view as the most important pathways to do so, which are grounded in a recognition of the unique industrial sectoral factors delineated above.

Pathway #1: Deploying Commercialized Co-Generation and Industrial Efficiency Technologies

Co-generation systems, commonly referred to as combined heat and power (CHP), are among several industrial efficiency technologies and energy management measures that are fully commercialized and deployed across the country but significantly under-utilized.41

CHP systems generate electric power and useful thermal energy from a single fuel source— predominantly natural gas, though biomass and other fuels are also used.42 These systems consume up to 40% less fuel while generating the same amount of power and thermal energy as separate heat and power systems. CHP systems are installed at nearly 4,400 sites in the US with a total capacity of 82.6 GW. These systems avoid 241 MMT of CO2 emissions and save 1.8 quads of fuel and annually—that’s more than twice the equivalent energy of all the natural gas produced in the Bakken region each year.43 The vast majority of CHP capacity (86%) is concentrated in the industrial sector and, in particular, in EIM subsectors.44

These are impressive numbers, but we’re nowhere near our full potential. While CHP represents roughly 8% of electric generating capacity in the U.S, it exceeds 30% in countries such as Denmark, Finland and the Netherlands.45 DOE estimates that there is another 154 GW of technical potential for CHP at industrial facilities for on-site use and the export of excess electricity back to the grid, which would nearly triple our current capacity.46 A high percentage of that potential is, unsurprisingly, in EIM sub-sectors, including petroleum refining (44.7 GW), chemicals (40.3 GW), and paper (25.2 GW). 47

DOE estimates that there is another 154 GW of technical potential for CHP at industrial facilities for on-site use and the export of excess electricity back to the grid, which would nearly triple our current capacity.

Beyond CHP, there are a range of commercially available technologies and measures that manufacturers can deploy to reduce energy cost and GHG emissions. These include advanced electric motor systems, high efficiency boilers, mechanical insulation, energy-efficient lamps and lighting controls, and sensors and controls that improve process performance.48

We have evidence that implementing these industrial efficiency end use approaches yields significant results. DOE’s Better Plants Program partners with manufacturers to identify and capture cost-effective energy efficiency opportunities. Through the end of 2016, Better Plants partners reported cumulative energy savings of 830 TBtu and $4.2 billion in energy costs, with an average annual energy intensity improvement rate of 3.1%.49

Despite their sizeable economic and environmental benefits, a number of barriers keep CHP and other industrial efficiency measures from reaching their deployment potential. Common challenges include: the dominant utility business model, which often positions CHP and end-use efficiency as a source of revenue erosion; internal competition for capital investment within companies, where the scale and payback of investment in CHP and end-use efficiency often competes unfavorably with investments that are smaller and yield payback more quickly; and a lack of awareness and knowledge about the technical and economic potential of CHP and end-use efficiency. If these and other barriers can be overcome, the energy savings, GHG emission, and economic impacts of deploying these technologies are demonstrable.

Pathway #2: Innovating Advanced Manufacturing Technologies

As noted above there exists a multiplicity of sub-sectors within U.S manufacturing. This fact, in turn, requires innovation in a diverse range of advanced manufacturing technologies that can be applied across the entire sector to achieve emission reductions. Importantly, advanced manufacturing innovation must also encompass material as well as energy efficiency in product design and production, which includes the light-weighting of materials, the reduction of material waste, and re-use of materials, all of which can achieve substantial reductions in energy use and GHG emissions.

We briefly summarize four advanced manufacturing technologies below, which are illustrative of the energy saving (and by extension GHG emission reduction) opportunities and challenges in U.S manufacturing.50

Process Heating

Process heating operations supply thermal energy that transform materials into myriad commodities and end- use consumer products, using energy obtained from steam, electricity and fuels. Process heating systems include furnaces, heat exchanges, kilns, and evaporators. These systems are used extensively by EIMs, but also in a range of other manufacturing sub-sectors. Process heating accounts for over 7 quads of US manufacturing energy use annually with approximately 36% of that energy lost as waste heat.51

Key RDD&D opportunities and challenges for this technology include high efficiency “super-boilers”; waste heat recovery systems; advanced non-thermal water removal technologies; and low-energy, high-temperature materials processing using selective heating techniques, such as microwave heating.

Additive Manufacturing

Additive manufacturing (AM), often referred to colloquially as “3-D printing,” builds up objects by ‘adding’ layer upon layer, from computer models, rather than the current manufacturing practice of cutting away materials from a starting work piece. These are nascent techniques, but they could have a transformational impact, reducing materials use (dramatically, in some applications), reducing the weight of end products, and enabling the fabrication of complex structures that can’t be mass-produced using existing technologies. AM techniques can be applied across the manufacturing sector, but show particularly strong energy savings for sub-sectors that rely on the complex use of materials and components parts – and where the weight of the end product has enormous cost, competitiveness and life cycle energy implication -- such as automotive and aviation manufacturing.

Key RDD&D challenges and opportunities for this technology include process controls that improve precision and increase throughput while maintaining the quality of the end product; scalability capabilities that enable larger volume production, both in size and number of parts produced; and more diverse material compatibility for new metal and polymer materials formulated for AM, providing application-specific properties such as flexibility, conductivity and low embodied energy.

Smart Manufacturing: Advanced Sensors, Controls, Platforms and Modeling for Manufacturing (ASCCPMM)

ASCCPMM, branded as ‘Smart Manufacturing,” involves technologies and practices that can capture, share, and process in real time the increasing amounts of information available at manufacturing facilities by using advanced sensors, data analytics, and control systems. The technologies and practices involved in Smart Manufacturing can interact at every level of the manufacturing sector, from equipment to plants to supply chains. They are valuable tools for energy management, and as such provide particular value for EIMs, where their application can model, predict, and optimize processes, with resulting energy savings ranging from 5% to 30%.

Key RDD&D challenges and opportunities for Smart Manufacturing include developing lower power and more resilient wireless sensors; improving real-time measurement of equipment energy consumption and waste streams; open standards and interoperability for manufacturing systems and devices; and better cybersecurity in an era of proliferating cyberattacks.

Wide Band Gap (WBG) Semiconductors for Power Electronics

WBG technologies allow semiconductor applications at higher frequencies, temperatures and voltages, which in turn enable the production of smaller, lighter and higher efficiency power electronics. These technologies can realize very large energy savings for motor-driven systems across the manufacturing sector, and could also accelerate the motorization of specific equipment such as large compressors; in addition, WBG semiconductors can provide energy savings in a variety of applications in the building, transportation and power industry sectors.

Key RDD&D challenges and opportunities for WBG semiconductors include reducing the cost of the substrate materials, most importantly silicon carbide and gallium nitride, compared to conventional silicon substrates currently in use; and improving their operating voltages and device reliability relative to silicon-based technologies.

These summaries of a handful of AM technologies underline the importance of continued innovation. But the best innovation doesn’t happen in isolation at the lab bench. Rather, it’s generated by applied research and development, and by selective demonstration and deployment of these technologies, which in turn creates a technology learning feedback loop that advances the R&D.

But the best innovation doesn’t happen in isolation at the lab bench. Rather, it’s generated by applied research and development, and by selective demonstration and deployment of these technologies.

The most ambitious example of this approach for AM is Manufacturing USA, a public-private collaboration consisting of linked Manufacturing Innovation Institutes, each of which has a unique technology concentration while contributing to the advancement of the US manufacturing sector as a whole.

There are currently fifteen Institutes established or planned, with the shared goals of increasing US manufacturing competitiveness through new technologies and innovation; reducing GHG emissions and improving energy productivity; stimulating regional economic growth; and developing a skilled workforce in each of the technologies of focus. Industry demand for Manufacturing USA can be gauged by clear metrics: nearly 60 percent of the Fortune 50 manufacturers are partners, and the Institutes have attracted $1.3 billion in private sector investment.52

Pathway #3: Moving the Industrial Sector to Clean Energy Fuels and Electrification

Almost all industrial processes have been designed around the availability, low cost, and energy density of carbon-heavy fossil fuels. Decarbonizing the industrial sector will require strategically replacing fossil fuels for certain processes through increasing the use of clean fuel sources and electrification.

The most important part of the value chain to focus such efforts on is industrial process heat, the largest source of fossil fuel use in the industrial sector. To transition to clean process heat, three considerations are worth emphasizing: (1) current conversion processes that transform raw materials into thermal energy in EIM subsectors require very high temperatures; (2) thermal heat cannot effectively be delivered over long distances; and (3) many process operations must be run continuously. Therefore, substitutes for fossil energy used for industrial heat processes must be dispatchable, able to achieve minimum temperature thresholds (depending on the operation), and located at or very close to the point of consumption.

Substitutes for fossil energy used for industrial heat processes must be dispatchable, able to achieve minimum temperature thresholds (depending on the operation), and located at or very close to the point of consumption.

There are select clean energy sources, albeit at different levels of commercialization, that could meet these criteria. Given their size and operational flexibility, small modular nuclear reactors (SMRs), show particularly strong promise as a supplier of industrial process heat. Light water SMR technologies currently being developed can produce thermal heat at temperatures up to 300 degrees centigrade (°C), which is hot enough to conduct some industrial activities like processing certain chemicals.53 Other heat sources would be needed to supplement these light water SMRs in order to achieve higher temperatures needed for additional industrial processes. However, other SMR technologies under development that use different types of coolants (e.g., high temperature gas) could provide outlet temperatures up to 850°C, which would make them applicable for a range of EIM sub-sectors, such as oil refining and chemical manufacturing.54 These would not be adequate solutions for sub-sectors that require direct heat at the highest temperatures, like the 1,700°C needed for iron and steel manufacturing or 1,500°C for cement.

It has been estimated that one-third of projected US industrial energy demand in 2025 could be met by about 235 SMRs with a capacity rating of 150 MWt.55 Of course, this estimate is entirely theoretical as very few SMR projects in the US have a realistic chance of commencing operation by 2025.56 Nonetheless, the technical capacity exists for SMRs to decarbonize a substantial portion of industrial energy use by 2050.

Solar thermal and (to a far lesser extent) geothermal energy sources could also play a role in meeting industrial energy demand. Concentrating Solar Power (CSP) plants may be able to produce heat at temperatures as high as 1000°C, which could make them applicable to roughly the same set of manufacturing subsectors as non-light water SMRs. Geothermal plants using current technology operate at much lower temperatures for thermal applications – up to 150°C -- which would allow them to provide thermal energy to a limited number of manufacturers with lower heat requirements, such as food processing.

Both solar thermal and geothermal hold an important advantage over SMRs as potential clean heat sources: they are commercialized and deployed. But they are also at a disadvantage: the geographical mismatch between the best resources for the technologies and location of US manufacturing. For example, currently operating CSP plants are concentrated in the Southwest, where the best solar resources exist, whereas U.S manufacturing is concentrated in Midwestern, Eastern and Gulf Coast states.

Another pathway for decarbonizing industrial energy use is through greater electrification of industrial process and power generation operations, linked with continuing efforts to shift the power sector to clean energy sources. Only 1% of conventional boilers and 10% of process heat applications in the industrial sector are electrified,57 and it’s technically feasible to scale up the deployment of electric boilers and electric heating technologies, including resistive, induction and infrared heating.

But there are barriers to electrification as well, none greater than the high cost of using electricity compared to direct fossil fuel use to generate process heat. Therefore, a critical R&D challenge will be to focus on industrial applications where electrification, relative to fossil fuels, can make more efficient use of thermal energy. More fundamentally, however, we need new technological and economic analysis to develop a better understanding of which industrial sector technologies would be the most promising and cost-effective to electrify.58

Pathway #4 Innovating Industrial Carbon Capture, Utilization and Sequestration (CCUS) Technologies and Building Out CCUS Infrastructure

The 2014 Intergovernmental Panel on Climate Change (IPCC) synthesis report estimates that climate mitigation costs will be 138% greater if CCUS technologies are not widely deployed.59 Therefore, the status of CCUS deployment is of paramount importance in evaluating the progress of climate mitigation strategies. The International Energy Agency (IEA) tracks the progress of a variety of clean energy technologies towards their Sustainable Development Scenario (SDS), which includes the Paris agreement climate goal of keeping global temperature increases well below 2°C.60 They schematically label technologies as (1) On track, e.g., Solar PV; (2) More efforts needed, e.g., a number of EIM sub-sectors; and (3) Not on track.

IEA judges the status of CCUS technologies, in both power and industrial sector applications, to be not on track. The total proven annual capture rate of existing industrial CCUS projects globally is 28 MMT of CO2, far short of the 400 MMT of storage required per year to be on track to meet the SDS target in 2030. IEA does note some positive developments, such as the opening in 2016 of the world’s first large-scale carbon capture and storage project in the iron and steel industry in Abu Dhabi, which is capturing up to 800,000 tons of CO2 annually, and the deployment of the first bioenergy with carbon capture and storage (BECCS) project (in the US – more on that below). But IEA emphasizes that the overall status of CCUS deployment should make policy support and investment in this technology an urgent priority.61

Given the findings of the IPCC analysis and IEA’s SDS target tracking, we don’t think it’s an exaggeration to assert that the success of the international effort to keep global warming below dangerous levels hinges in no small part on our success over the next seven years in bridging the gulf between where we are in the deployment of CCUS technologies now and where we need to be in 2025.

The US has the capacity to be the global leader in this effort, but domestic CCUS faces optical and economic barriers. In April of 2017, the world’s first BECCS project commenced full commercial deployment at an Archer Daniels Midland (ADM) ethanol plant in Illinois, which will inject 1 MMT of CO2 in a saline aquifer. Just three months earlier, the Petra Nova project in Texas started operations, the world’s largest CCUS deployment on an existing power plant; it will capture up to 1.4 MMT of CO2 annually, transporting it by pipeline to a nearby oil field, where it’s used for Enhanced Oil Recovery (EOR) and then sequestered.

Despite the global significance of these projects coming online, the media reception to their deployment was vastly eclipsed by the announcement in 2017 by Southern Company and Mississippi Power that they were discontinuing the CCUS portion of their Kemper Power Plant, after years of development and billions of dollars of investment, and would instead operate it as a natural gas plant.

The failure of Kemper, and other high-profile CCUS projects that preceded it, such as FutureGen in Illinois, are in part simply recent examples of the challenges of being first movers in the energy sector. It is always difficult to move new energy technologies to market, and the failure rate is high. But in addition to the typically high costs associated with first-of-a-kind projects, their demise was also a reflection of an economic perfect storm that emerged over roughly the same period they were developed.

Arguably the most significant component of this perfect storm was the unprecedented drop in natural gas prices, which made it increasingly difficult for the retrofitting of existing coal fired power plants, let alone the construction of new plants, to be cost competitive with new natural gas plants. This cost crunch in turn made it all the more important for CCUS projects to find markets for their captured CO2, the most robust of which is EOR. But the precipitous drop in oil prices has limited the demand for EOR as well as the price that oil producers are willing to pay for the CO2 that enables it.

The challenges of deploying CCUS in the US power sector show no signs of abating. However, current opportunities to deploy CCUS in the industrial sector are numerous and more economical. And unlike in the power sector, where various cheaper low and zero carbon alternatives to CCUS exist, in the industrial sector there are fewer and in many cases no emission reduction alternatives to CCUS.

As detailed above, there are numerous ways in which we can and need to reduce industrial sector emissions. But there are thermodynamic, technological and economic limits to what proportion of GHG emissions from fossil fuel combustion can be mitigated by realizing greater energy and material efficiencies, and implementing electrification and fuel switching strategies.

The challenges of deploying CCUS in the US power sector show no signs of abating. However, current opportunities to deploy CCUS in the industrial sector are numerous and more economical.

And that still leaves us with the necessity of capturing emissions from industrial operations that don’t involve energy conversion, but rather result from chemically transforming raw materials into commodities. In fact, it’s these emissions that can be captured most economically with currently available technology because they can yield high-purity sources of CO2 (e.g., from ethanol, natural gas and ammonia processing).62 The ‘breakeven’ cost of capturing CO2 from these pre-concentrated sources is $18-$30 per ton,63 whereas the price range of the post-combustion capture of CO2 is $55-$83 per ton. In addition, there is geographical proximity of large amounts of these high purity sources to sites where they can be used and/or sequestered. According to one analysis, 43 MMT of high purity industrially sourced CO2 are emitted annually within 100 miles of saline formations; of these, 32 MMT of high purity CO2 are emitted annually within 100 miles of oil fields that could potentially use EOR.64

However, taking advantage of this opportunity requires building out the nation’s CO2 pipeline infrastructure. At present, there are 50 individual CO2 pipelines in the US, with a combined length of roughly 4,500 miles, almost all of which are dedicated to EOR operations—more than half of the pipelines, by mile, are concentrated in the Permian Basin oil fields.65 The construction of long-distance, large-volume CO2 pipelines linking industrial sites emitting high-purity CO2 sources to oil field customers is the necessary next step in making industrial CCUS logistically and economically feasible. Importantly, this infrastructure would not only dramatically lower the cost and risk for potential storage projects, it would likely stimulate economic growth in those regions by anchoring and attracting current and future industrial development.66

Importantly, the Bipartisan Budget Act of 2018 included an extension of the 45Q tax credit for storing CO2 that also increases the value for each ton of CO2 captured and sequestered, directly and through EOR, from industrial facilities and power plants. IEA analysis projects that the passage of this tax incentive could catalyze capital investment in CCUS deployment of approximately $1 billion over the next 6 years, most of which will go to developing industrial CCUS projects in the subsectors noted above where high-purity CO2 is emitted.67

In tandem with deployment, further innovation of CCUS technologies that focuses on their use in diverse industrial applications will be necessary to improve the performance and drive down the cost of deploying these technologies. Mission Innovation, the global initiative to accelerate clean energy innovation, involving 22 countries and the European Union, has developed seven “Innovation Challenges.” The Carbon Capture Challenge, for which the US and Saudi Arabia are global leads, summarizes priority areas for R&D:

Further efforts must be focused on research and development to enable new and novel carbon capture technologies, aimed at driving down costs and facilitating broader deployment. Fundamental research should be directed in areas that could result in revolutionary, not just incremental, advances in gas separation and geologic storage of CO2. Parallel efforts to utilize CO2 must also be pursued, exploring the use of captured CO2 to create plastics or algal biofuels, carbonate materials, or other uses yet-to-be-discovered.68

Pathway #5: Scale up industrial production of low-emission gases and high efficiency refrigeration and air conditioning equipment

The US GHG Inventory categorizes Industrial Processes and Product Use (IPPU) as emissions from industrial processes and the use of GHGs in products. Examples of IPPU emissions are those that result from the chemical transformation of raw materials and those that result from manufacturing processes and use by consumers.

IPPU accounted for 362.1 MMT of CO2e in 2016, of which nearly half (159.1 MMT) resulted from the Substitution of Ozone Depleting Substances (ODS).69 This clunky term refers to the use of HFCs to replace other gases (chlorofluorocarbons and hydrochlorofluorocarbons) that cause damage to the stratospheric ozone layer. This substitution has occurred under the auspices of the Montreal Protocol and the Clean Air Act Amendments of 1990 and it’s working -- the ozone layer is recovering. But while HFCs don’t deplete the ozone layer they are extremely powerful GHGs. In 1990 there were virtually no US emissions from these gases. In 2016 they represented more than two times the emissions from the next two biggest IPPU sources combined, iron and steel production (41.0 MMT) and cement production (39.4 MMT).70 Globally, HFCs are the fastest growing GHG, increasing at a rate of 10-15% annually. There’s at least one estimate that a fast phasedown of HFCs could prevent 100 to 200 billion tons of CO2e by 2050 and up to 0.5C of global warming by 2100.71

There's at least one estimate that a fast phasedown of HFCs could prevent 100 to 200 billion tons of CO2e by 2050 and up to 0.5C of global warming by 2100.

Emissions from HFCs are distributed across the industrial, residential, commercial and transportation sectors. In fact, very few of these emissions come from the manufacturing process itself in the US, as manufacturers use reliable emission control equipment. Most result from the fugitive emissions of coolants and refrigerants in air conditioning and refrigeration systems in homes, businesses, and vehicles.72 We include this pathway in an industrial sector-focused report because it’s an example of how manufactured products, via supply chains, in effect move GHG emissions across the economy and because, given the dispersed nature of the end-products, the most impactful way to reduce them is at the source: by manufacturing alternative gases that emit low or no emissions.

This substitution is already happening. US manufacturers are producing alternative gases for a variety of products in response to market demand from downstream manufacturers and end-use consumers. Indeed, a number of US companies are very well positioned to capture market share for these alternative gases as the market expands for them globally, with attendant economic gains for not only those companies but also American workers and the US economy more broadly.

But while the shift from HFCs to alternative gases has started, it must occur more rapidly and in all countries in order to bend the curve on GHG emissions. This will be particularly important in emerging economies such as India, Brazil and China, where markets for refrigeration and air conditioning are expanding exponentially.

In 2016 an agreement was reached in Kigali, Rwanda by nearly 200 countries to adopt a global phasedown in the production and consumption of HFCs. Fittingly, this agreement was reached at a Meeting of the Parties to the Montreal Protocol. Under the agreement, most developed countries will begin a phasedown in 2019 and most developing counties will begin in 2029.

As occurred after the Montreal Protocol was adopted in 1987, a phasedown and replacement of one set of gases for another in appliances and equipment also presents an enormous corollary opportunity to achieve significant improvements in the energy efficiency of air conditioners, refrigerators and others products. In effect, the Kigali agreement, and the national policy responses of the parties to it, could catalyze the production of a new generation of high-efficiency, low-GWP appliances and equipment that could rapidly penetrate markets across the global economy over a period when demand for many of these products will be skyrocketing. According to one analysis, the adoption of more energy efficient room air conditioners alone could avoid roughly 100 gigatons (Gt) of CO2e emissions by 2050.73

However, the path forward for US implementation is not immediately clear. In 2017 a federal court ruled against an EPA rule that banned the use of certain HFCs in specified applications, though that ruling is being appealed to the Supreme Court. Furthermore, the US Senate will almost certainly have to ratify the Kigali agreement as an amendment to the Montreal Protocol.

Conclusion

Whether it’s workforce opportunity, U.S. competitiveness, or climate change, there are more than enough reasons to promote smarter, cleaner, more efficient energy use in the industrial sector. Many individual companies and manufacturing subsectors are already taking steps in the right direction. However, federal policy support will be needed to maximize the benefits that enhanced industrial energy performance can deliver for the country. In this report, we have identified the types of technologies and practices that will produce the most impactful improvements in this sector, and would suggest that policymakers focus their efforts on these particular pathways to success.

Getting any meaningful policy objective over the finish line in Washington today is a challenge. But this issue has some powerful assets working in its favor—enormous potential for economic and environmental gains, a message that resonates with manufacturing communities across the country, and a potent combination of business, labor, climate, and other interests who are eager to help get the job done. This makes for a unique opportunity to advance a number of important national priorities while guaranteeing a stronger future for American industries and workers. Now is the time to seize it.

Appendix A

China’s Policies on Industrial Emissions

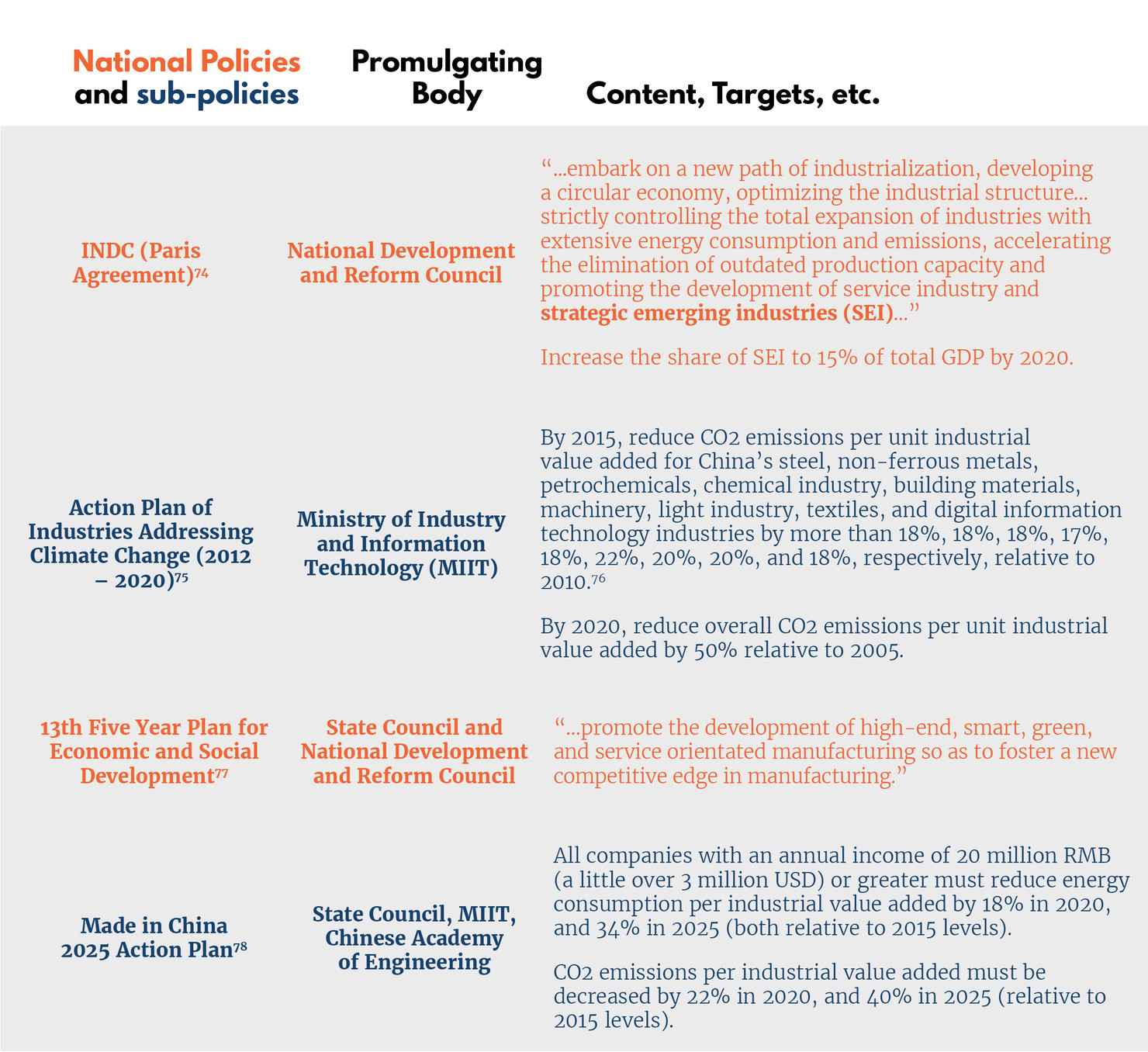

The US has sporadically used voluntary goal setting, R&D efforts, best practices initiatives, and other discrete policy mechanisms to promote smarter energy use in specific industrial sectors, with some degree of success. China, on the other hand, is committing to ambitious long-term goals for energy efficiency and productivity across a wide swath of industries and is developing expertise in critical fields of low-carbon manufacturing. These policies are being implemented for the express purpose of combating air pollution and climate change, but China is also using them to position its manufacturers for competitive advantage in emerging markets for cleaner and more energy-efficient technologies, products, and materials.

The Chinese government directs its national economy under the guidance of various action plans and policies that overlap and intersect. In Table A-1 we highlight the most important existing national policies that impact China’s industrial sector and industrial GHG emissions, along with sub-policies setting industry-specific requirements.

Table A-1

China’s focus on Strategic Emerging Industries (or SEI, which includes advanced materials, control equipment and robotics and smart manufacturing) reflects its intent to become a leader in high value, low carbon manufacturing.79 China’s INDC target boosts SEI to 15% of national GDP by 2020, as laid out in the Intended Nationally Determined Contribution submitted as part of the Paris agreement, is enormously ambitious; in 2010 SEI made up not quite 4% of China’s GDP.80 By the end of 2017, however, SEI’s share of national GDP had reached roughly 10%.81 The “Made in China 2025 Action Plan” underlines the importance of SEI, but also outlines a low carbon roadmap for the development of Chinese industry as a whole.82

China’s Actions on CCUS, Nuclear Energy, and Emissions Trading

China is implementing, or planning to implement, technology-specific and carbon pricing efforts that will contribute to the decarbonization of its industrial sector, helping to achieve the goals outlined in the policies above.

- Carbon Capture, Utilization, and Storage: 14 Chinese CCUS projects have begun full commercial operation with capture and/or storage capacities ranging between 2,100 and 280,000 tons of CO2 per year. Several projects in the planning phase are designed to capture well over 1 million tons of CO2 per year.83 Importantly, these CCUS projects are not confined to the power sector—the technology is already deployed in several manufacturing sub-sectors, including chemicals production and oil refining.84 Moreover, The Financial Times reports that “…state-owned enterprises in China’s heavy industry sectors, including cement and steel, have begun considering adding equipment to existing plants that would allow them to capture about 90 to 95 per cent of their carbon emissions.”85

-

Nuclear Energy: China is rapidly expanding its nuclear power program, investing in advanced high-temperature gas-cooled reactors which can provide flexible ratios of heat and electricity. Its HTR-PM is currently the worlds most advanced high temperature reactor project—a demonstration unit links two 250 MWt units with 750°C outlet temperature to a 210 MWe steam turbine.86 Reportedly, China plans to innovate on its HTR-PM reactor to allow for the direct replacement of coal power for hydrogen production, seawater desalination, and a wide range of other industrial processes.87 Though no nuclear industrial heating projects have been deployed yet, a feasibility study for nuclear powered district heating is currently being conducted by China General Nuclear.

-

Emissions Trading System (ETS): In December 2017, China officially announced the rollout of a national ETS that links up the nine pilot cap-and-trade systems which the country has been operating at the city, provincial, and regional levels for the past several years.88 According to the announcement, the ETS will initially cover approximately 1,700 electric generating companies, which currently account for roughly one-third of China’s total emissions. By 2020, coverage will be extended to carbon-intensive industries such as steel, chemical manufacturing, building materials, textiles, and non-ferrous metals.89 China worked closely with the European Union (EU) in designing and deploying its ETS, and a three-year EU-China cooperation project on emissions trading which just began indicates China’s intent to link its ETS with other international carbon trading systems in the future.