Report Published December 15, 2015 · Updated December 15, 2015 · 11 minute read

Home Equity Vouchers

Paul Lapointe

Fourteen percent of all homes in the United States have a negative equity balance—meaning that the homeowner owes more on the mortgage than their home is worth. This number is even worse in certain regions of the country. In Las Vegas, 25% of homes have negative equity; in Rockford, IL, 29% of homes have negative equity. In Jacksonville, NC, an astounding 43% of homes have negative equity.1 For these homeowners, this is more than just a balance sheet mismatch. A lack of home equity makes families more vulnerable to price shocks, makes selling their home more difficult, and puts them at risk of losing the most important asset they own.

In our foundational report, Ready for the New Economy, we laid out a series of challenges that are profoundly shaping the evolving economy in the 21st century. One key area: increasing wealth for low- and middle-income families and giving them a better shot at financial security. In this brief, we lay out a problem that millions of American families face, a lack of adequate equity in their home. We then propose a unique solution, Home Equity Vouchers, which would help low- and middle-income families to more quickly pay down their mortgages, build up equity, and relieve the burden of debt.

The Problem

A home is one of most important assets that many middle-class families have. In the Federal Reserve’s 2013 Survey of Consumer Finances, 65% of all families owned their primary residence.2 For these homeowners, the overwhelming majority of their net worth is in their homes. The same survey showed that the median value of all primary residences was $170,000 vs. a median of $52,700 in financial assets among those same homeowners.3 For non-homeowners, their median total net worth was just $5,400—a figure that mostly reflects lower incomes, but is also likely effected by the fact that rent does not build wealth in the same way that mortgage payments do.4

For older households, homeownership is even more important and more prevalent. Approximately 86% of households headed by someone aged 65 to 74 own a home and 80% headed by someone aged 75 or above own a home.5 These families will often rely on the equity built into their homes upon retirement. To supplement Social Security and private retirement savings, households may take several actions to extract equity from their homes:

- Sell their home and relocate to a less-expensive place;

- Enter into a reverse mortgage, allowing them to spend their equity while still living in the home, or;

- Take out a home equity line-of-credit (HELOC), where they receive a lump sum loan using their house as collateral.

Even if a family does not take equity out of their home, owning a residence outright can substantially lower living costs (compared with renting or still making mortgage payments) and reduce the retirement savings required to maintain their pre-retirement standard of living.

But too many households are not building this important equity cushion. Many families are carrying mortgages on their homes well into retirement age—39% of households with a head between the ages of 65 and 74 have a mortgage, and 19% of households with a head over 74 years old still have a mortgage.6 This limits the ability for these families to tap into home equity and potentially forces them to delay retirement.

Further, the bursting of the housing bubble during the recent recession showed that low levels of home equity are not just a problem for older Americans. In 2012, according to Zillow’s Negative Equity report, 31% of all homes were underwater7—meaning the market value of the home was less than what was owed on the mortgage. This problem was greatly fueled by low down payments made at the time of purchasing homes. Even though housing markets have largely recovered, 14% of all homes are still underwater. This problem is even greater for low-value homes—24% of homes in the bottom third of value are currently underwater. This puts these homeowners at a greater risk of losing their home and results in them being unable to sell their home to cover their debts.8

But, while home equity is critical, current federal policy is subsidizing the absolute opposite—more debt. The mortgage interest deduction allows homeowners to take a tax deduction on interest paid for mortgages up to $1.1 million. This makes a mortgage a cheap source of debt—the interest rate you pay is subsidized by the tax deduction, resulting in a below market interest rate. And this subsidy costs the government $77 billion per year.9 Consequently, people are often told that they’d be fools to pay off their mortgage early and that, instead, they should use that money elsewhere. This advice ignores, however, the security and stability that home equity provides. Additionally, it assumes that the money that would be used to pay off the mortgage earlier is instead put into an investment that earns a higher rate of return, an assumption that may not hold for many households.

The Solution

To allow low- and middle-income families to get out of debt quicker and into ownership faster, we propose the creation of a Home Equity Voucher program. This program would match up to $500 a year—or $5,000 per family over a decade—dollar-for-dollar, on additional principal payments above a family’s current monthly mortgage requirements. For 30-year fixed mortgages, grants would be limited to families making under $125,000 and for the first 10 years of a home loan—the timeframe where paying down equity has the most long-run financial benefit.

These grants would be targeted at homeowners that truly need help in building equity by restricting eligibility on the following criteria:

- Total household income must be under $125,000;

- It must be an owner-occupied, primary residence;

- The mortgage must be a traditional 30-year (no short-term or interest only loans);

- The home cannot have any HELOCs on it, preventing someone from taking out a loan on a house and then using that money to claim these grants, and;

- Mortgage contracts cannot include requirements to make these payments, ensuring that these payments truly contribute to building equity, rather than increasing loan amounts.

With these conditions, we estimate that about 14 million households would be eligible for these grants each year.10

Homeowners would see a number of benefits. First, they would pay less over the course of their mortgage. The government would chip in up to $5,000 over ten years, and the extra principle paid down early on would result in lower interest payments throughout the life of the loan. Second, they would pay off their mortgages quicker. With the additional money being put towards the loan early on, the homeowner would be able to pay off the loan in substantially less time. And, third, throughout the course of the mortgage, the homeowner would own more of their house than they otherwise would, resulting in a larger buffer against price shocks and adverse events.

Case Study

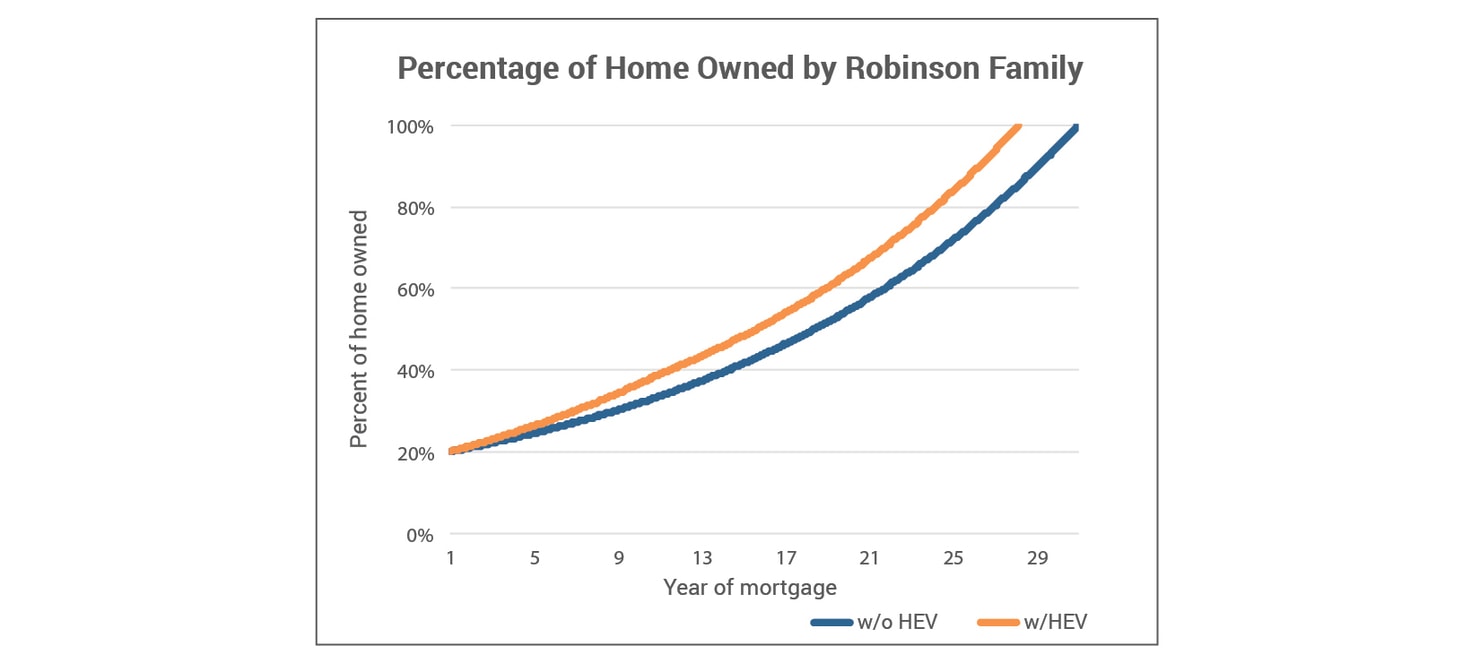

Take the case of the Robinson family, a middle-class family that decides to purchase a single-family home for the first time. They pick out a $250,000 home, make a 20% down-payment ($50,000), and take out a 30-year mortgage for the remaining $200,000. Let’s also assume that interest rates normalize and they get a rate of 5.72%.11

Without the home equity voucher program, they would pay roughly $418,000 (in principal and interest) over the course of their 360 month loan. If, however, they fully utilized the home equity voucher for the first ten years of their mortgage, they would end up paying about $385,000 and have paid off the loan in just 327 months. This means that the Robinsons would save $33,000 ($5,000 from the grant and $28,000 from reduced interest payments) and own their home outright over two and half years earlier (see Appendix for explanation of calculations). More importantly, they would own more of their home throughout the life of the mortgage (see below chart). Five years into their mortgage, they would own 2.3% more of their home than otherwise; ten years in, it would be 5.4%; twenty years in, 9.6%. This additional equity would help stave off price shocks that otherwise could put their home underwater.

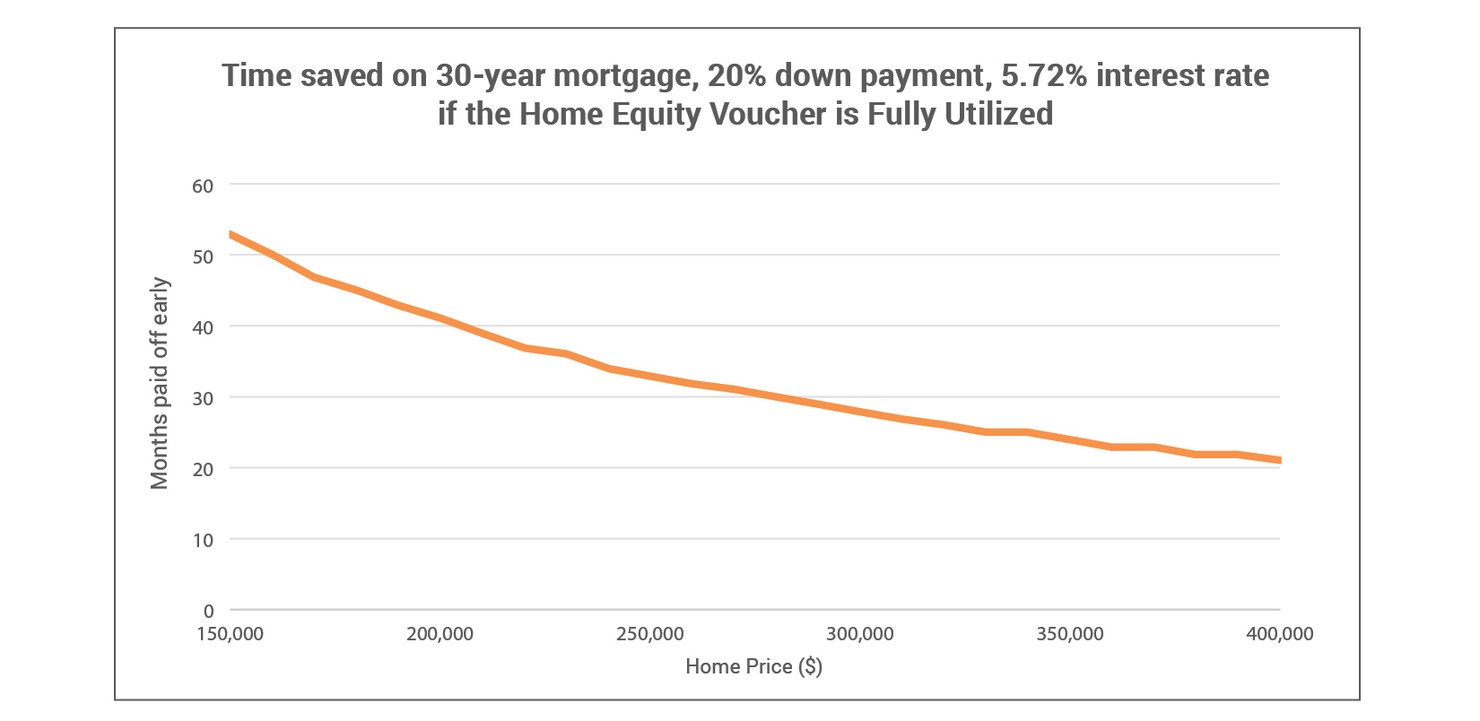

The grant would be even more meaningful for lower-priced homes. The chart below shows how early someone fully utilizing the vouchers would pay off a 30 year mortgage (with a 20% down payment and 5.72% interest rate) at different home values. For example, a mortgage on a $152,000 home (which happens to be the median home price in Lexington, KY12) would be paid off 52 months early.

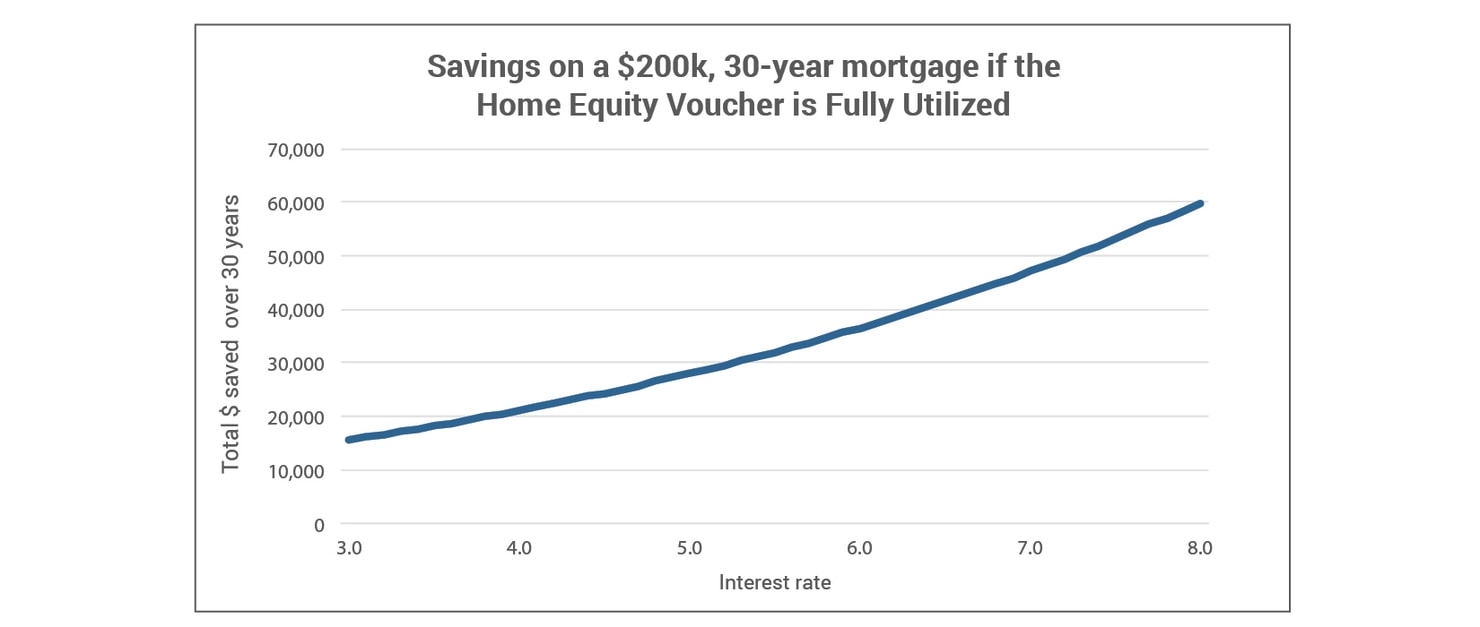

Additionally, the grant would be more valuable when homeowners face higher interest rates. The below chart shows how much is saved at different interest rates in the case of a homebuyer that takes out a $200,000, 30-year mortgage and fully utilizes the Home Equity Voucher. As depicted, the homebuyer would save about $21,000 by using the program if they received a 4% interest rate. If, however, their interest rate was 6%, they would save more than $36,000 by fully utilizing the program.

How would it work?

Below are two potential processes for administering the Home Equity Voucher program.

- Option 1. When a homeowner makes their monthly mortgage payment and includes an extra amount, this would trigger a downstream process at their mortgage servicer. The servicer would be required to transfer information on all overpayments to the Department of the Treasury (or another designated agency, such as the IRS) each month. The Treasury would verify eligibility and make a matching contribution to the mortgage. This option would maximize the take-up rate due to the ease for homeowners, but verifying income eligibility may be challenging and it would rely on participation from mortgage servicers.

- Option 2. Homeowners make additional payments throughout the year which would be reflected on a modified 1098 form. Currently Form 1098 tracks mortgage interest paid throughout a tax year, but this could be amended to also include additional principal. When the IRS processes the individual’s tax return, they would transfer any qualifying match to the mortgage servicer. This option would slightly lower the value of the grant (because the matching grants would be paid out later) and would probably also lower the take-up rate, but would make it easier for income verification and would not require participation from potentially reluctant mortgage servicers.

In order to offset the costs of this program, we propose adjusting the mortgage interest deduction so that homeowners can only deduct interest paid on up to $500,000 in mortgages, instead of the current $1.1 million limit. As scored by the Congressional Budget Office, this would save about $60 billion over ten years.13 $6 billion a year would account for 12 million of the 14 million eligible households fully taking advantage of this grant—a take-up rate that would be much higher than in other programs that incentivize savings.14

Using savings from reducing the tax deduction to provide low- and middle-income households with these vouchers would redirect the resources that the government is putting into subsidizing homeownership to help those that truly need it. Currently, 51% of the benefits of the mortgage interest deduction go to those with incomes over $100,000.15 There are three primary factors behind this: higher earners generally have more expensive homes, making their interest payments higher; higher earners are in higher tax brackets, making a tax deduction more valuable to them, and; lower earners often do not itemize deductions, making a tax deduction meaningless to them.

Further, reducing the mortgage interest deduction would have the added effect of reducing the inflationary aspect of the program. While it is often cited as increasing homeownership, research has shown that the deduction does little to increase ownership and, instead, causes homebuyers to purchase larger and more expensive homes.16 A lower cap on the value of mortgages that the deduction can be taken on would dilute this effect.

Conclusion

Middle-class Americans are not generating the kind of wealth that leads to stability, security, and certainty in the 21st century economy. Too many families lack sufficient assets and are faced with seemingly insurmountable debt.

The Home Equity Voucher program would help counter this by realigning incentives in the mortgage industry to promote equity instead of debt. This would help millions of low- and middle-income Americans generate assets faster and lock in more financial security. In doing so, these families would have more protection against adverse events and price shocks and would be put into a better financial position for later in life.

Appendix

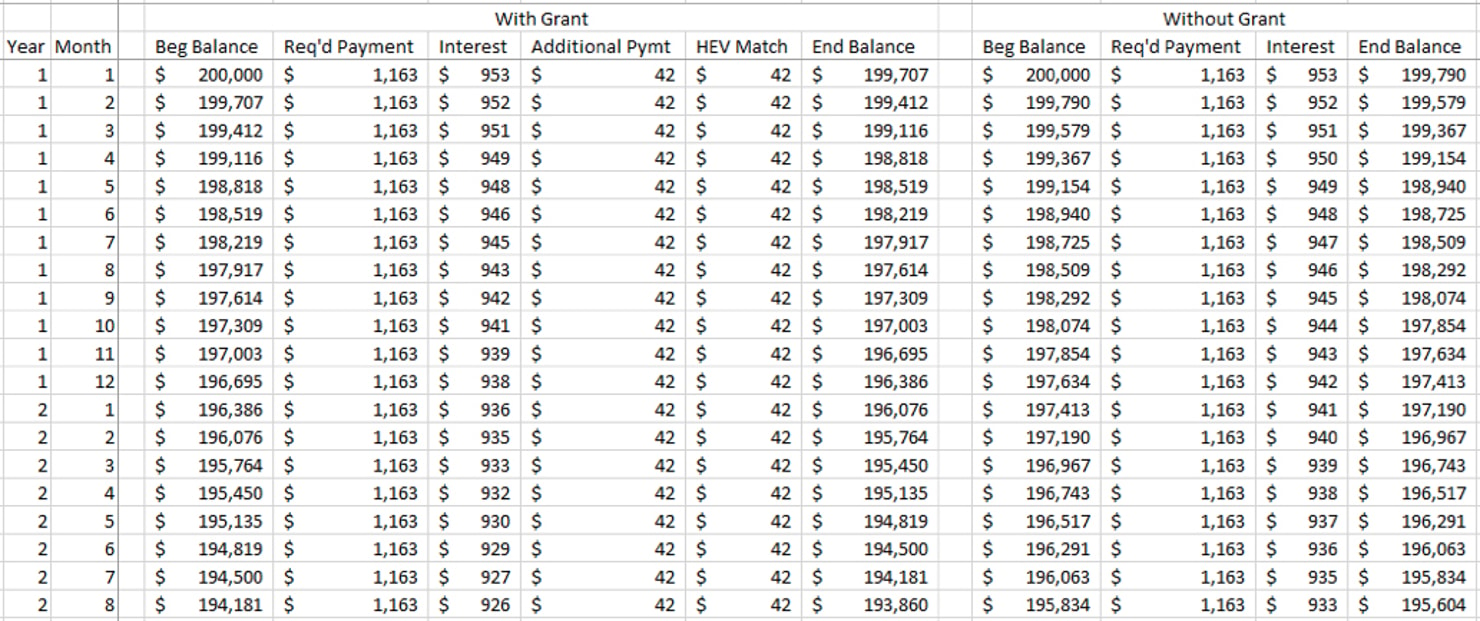

To calculate the impact of the home equity voucher, we simulated monthly mortgage payments with and without the grant program. Excel’s pmt function was used to estimate monthly required payments. Additional principal payments were assumed to be evenly distributed throughout the year and the government match was assumed to be made at the same time as the additional payment. Taxes and insurance are not factored in and do not affect the savings, as they remain constant in either scenario.

The below table shows a snapshot of the model. The fields include beginning and ending monthly mortgage balance, required and additional payments, and interest amount (for both with and without the grant program):