Report Published August 28, 2013 · Updated August 28, 2013 · 14 minute read

Dark Pools: Fear of the Dark

Lauren Oppenheimer & John Vahey

There’s a buzz on Wall Street and in Washington about a stock trading venue known as a Dark Pool. When you hear, “Dark Pool” the immediate reaction is, “Uh, that can’t be good.”

This paper sheds some light on what dark pools actually are, explains that dark stock trading is not new, notes some key differences between trading in a dark pool and trading on an exchange, highlights who uses dark pools, and poses the question: should you be afraid of the dark?

What’s a Dark Pool?

Dark pools are private, electronic stock trading venues that allow buyers and sellers of a stock to be matched anonymously. In a dark pool, prices are not displayed to investors—stock prices are dark. Dark trading is an alternative to trading on a “lit” exchange, like the New York Stock Exchange (NYSE), where traders benefit from visible prices.

Dark pools cater to large institutional investors like pension funds, mutual funds, and hedge funds—institutions that regularly trade massive quantities of stock. These funds are continuously in the process of trading—adding and subtracting stocks from their portfolios. Their trades can move the market—driving the price of a stock way up or down.

For example, when retirees want cash they may redeem (or sell) their mutual fund shares. If a mutual fund has a large amount of redemptions they will need to sell a large quantity of shares to provide investors with cash.

When executing the large order, the mutual fund will try to not tip their hand and reveal—to opposing traders—that they are in the process of selling a large amount of stock. If other traders know that a fund is selling a big block of shares they will lower their bids—ultimately forcing the fund to sell for lower prices, reducing investment returns.

But orders in a dark pool are not visible to other traders. Therefore, less information is revealed about an institution’s in-process trade. And this helps the mutual fund investor redeem their shares for the best possible price. This is why investment managers choose to execute portions of their big trades in the dark.

From 2007 through 2012, the total share of dark trading rose from 30% to 33.2% of the total equity market volume.1 Dark pools account for about 15% of total equity market volume, or roughly half of all dark trading.2

Overall dark trading volume includes dark pools in addition to what is known as broker-dealer internalization. A broker-dealer is a firm that can execute trades on behalf of clients (broker) or trade and hold securities for their own account (dealer). Internalization—a type of dark trading—occurs when a retail customer submits an order to sell stock and the broker-dealer buys the shares—without publicly displaying the order.

Traders have always sought to trade stealthily. So, while dark pools are a relatively new addition to the markets, dark liquidity has been around for a long time.

In the past, big institutional funds relied on exchange floor brokers to discreetly fill large orders. As the Securities and Exchange Commission’s (SEC) 2010 Concept Release on Equity Market Structure notes, “A primary source of dark liquidity for many years was found on the manual trading floors of exchanges. The floor brokers ‘worked’ the large orders of their customers by executing such orders in a number of smaller transactions without revealing to potential counterparties the total size of the order."3

A seasoned broker “works” a 1 million share “parent” order with lots of smaller “child” orders. They try to be stealthy by making smaller purchases of 1,000, 5,000, or 10,000 shares over an extended period of time. The broker protects the order by not revealing its full size. This gets the customer the best possible price.

In the past decade, the role of brokers on the floor of the New York Stock Exchange has become diminished. Manual trading floors have largely been replaced by fast and efficient electronic trading. In today’s automated, electronic markets traders use dark pools to work stock orders. Dark pools protect the value of the fund’s order and minimize the cost of executing a big trade.

As a 2013 New York Law Journal article notes, “There are a number of benefits to trading in a dark pool, the most critical being privacy of the transaction. For example, because the dark pool does not reveal price quotations or other information to the public, investors are free to execute trades without risk of moving the market."4

Dark pools are a modern, computerized version of the hidden order ticket smartly tucked away—in the darkness—of a broker’s pocket.

What Makes a Dark Pool Dark?

In a dark pool, traders are blindfolded. They can’t see the prices that other traders are willing to buy and sell for, say, Disney stock. This lack of “pre-trade transparency”—or the ability to view prices before trading—is the defining feature of a dark pool.

Lit exchanges, like NASDAQ or NYSE, run “central limit order books”—electronic trading platforms that visibly list stock prices and how many shares are for sale at each listing price.*

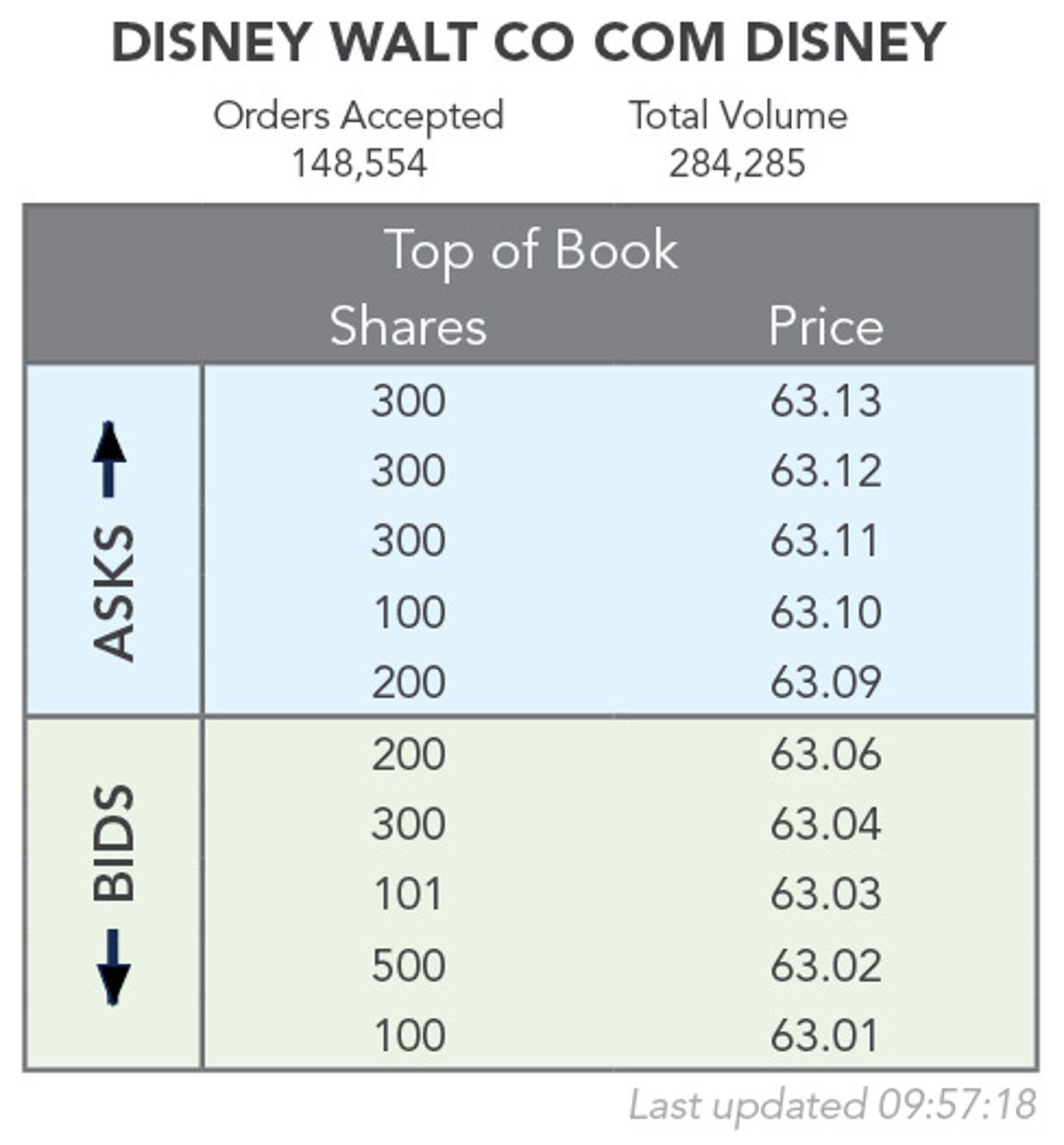

The website for the BATS Exchange (www.batstrading.com) displays their streaming central-limit order book. They refer to it as “Book Viewer.”

This is what an order book looks like. Anyone can see it. It clearly lists all the bids (in the green section) and offers (in the blue section).

One of the best aspects of the lit markets is that if you need to get your hands on shares right away you know how many are for sale and how much you will have to pay to buy the shares.

The order book also displays the “depth” of the order book—or how many shares are available at each price. You can see that there are a total of 1,200 shares of Disney for sale between $63.09 and $63.13. An exchange’s limit book provides a ton of information, not to mention visual stimulation.

In the order book above, the market for Disney stock is $63.06 bid and $63.09 offered. If you are a buyer, there are 200 shares for sale at $63.09; if you are a seller, you can sell 200 shares at $63.06.

If a new order to buy 500 shares of Disney stock for $63.07—a new best bid—is entered the order book updates instantly. Any trader following the market closely will see the new best bid lit up in the order book.

When prices fluctuate in a dark pool you see nothing—the movements of prices and quantities are hidden. If you would like to buy a stock you reveal your bid only to the operator of the dark pool—who keeps it hidden from other traders.

When a seller of the same stock enters an order to sell at your bid price you are anonymously matched. If no match exists you walk away empty-handed—unable to buy any shares.

Do Dark Pools Get Lit?

Dark pools are only dark up to a point. If a trade is consummated, they are required to provide “post-trade transparency”—similar to an exchange. A dark pool is required to report the trade to the Financial Industry Regulatory Authority* (Finra)—the primary regulator for dark pools—within 30 seconds.5 Eventually the transaction details appear on the stock ticker running on the bottom of Bloomberg TV or CNBC.

Dark pools are registered broker-dealers so they are regulated by Finra, the self-regulatory agency for broker-dealers.

The most significant disclosure difference between a completed trade on a lit exchange and a dark pool is that a lit trade report will specify the exchange where the deal was made. Currently, a dark pool trade report does not identify the exact dark pool where the trade occurred.

There are always market players trying to determine where large blocks of shares are trading. Sometimes these traders will try to buy or sell a small amount of shares in a dark pool to test the dark waters. If their order gets gobbled up that could point to the existence of a large order. Uncovering evidence that a big order exists in a dark pool is meaningful information to traders.

Regulators may soon make it easier for traders to identify which stocks are being most actively traded in specific dark pools.

On July 12th, 2013, The Wall Street Journal reported that Finra was going to propose rules to increase dark pool transparency.6 The proposed rules, which would have to be approved by the SEC before going into effect, would include a requirement for each dark pool to report their trading volumes, on a stock-by-stock basis, each week or two. This would help give investors and regulators a more accurate picture of total dark pool trading volumes.

How Did Dark Pools Come to Be?

In 1975, Congress wanted to better connect the scattered regional exchanges that made up the U.S. equity markets. Congress directed the SEC to foster the development of the national equity market. Congress could have decided to centralize all U.S. stock trading on one exchange.

Instead market forces and technological innovation have shaped the markets. Dark pools are a type of trading venue that has sprung up due to investor preferences, the electronic trading revolution, and subsequent regulatory changes.

The first official dark pool opened up in 1986 when Instinet began to offer clients the ability to electronically swap large blocks of shares anonymously away from an exchange’s trading floor.7 Up until to that point if a trader wanted to swap a large block of shares off the exchange floor they would call a broker who specialized in block trading. The broker would call around to other funds seeking a counterparty or fill the order with an opposing customer order if one existed.

But, calling around to see if traders were interested in buying a large block of shares would tip off traders that someone was trying to sell.

Instinet allowed traders to anonymously, and electronically enter an order to buy or sell a stock at a certain price without using a phone broker. If an opposing order existed in the Instinet system the orders were matched and a trade would occur. If a trader bid and no one was willing to sell no trade would occur. And, importantly, the trader’s bid was not revealed to the market. The bid remained dark.

These inconspicuous trading venues allow fund managers to preserve the value of their investment ideas. When an investment manager develops a unique, contrarian view about a company’s hidden value they don’t want other investors to profit from their analysis. If you continue to aggressively bid for, and buy, a stock in the lit markets other traders will be able to anticipate your next move.

Who Makes the Rules in a Dark Pool?

Dark pools are not required to disclose how trades are matched within the dark pool, so the rules are opaque. But here’s how it could play out with a typical trade and how it compares to a lit exchange.

A “mid-point” order is an example of a basic order type. A trader that enters a mid-point order is seeking to buy a stock at the point in between the best public market bid and the best public market offer. (Since dark pools are dark they reference the prices that are displayed in the lit markets).

On the exchange, if Disney stock is $63.06 bid and it’s offered at $63.10 the mid-point price is $63.08. Traders enter mid-point orders because they represent a savings—to both the buyer and the seller—in comparison to a purchase of stock at $63.10 or a sale of stock at $63.06. $63.08—the mid-point—splits the difference. Everyone saves 2 cents per share.

Now imagine that three traders have entered three anonymous mid-point orders into a dark pool. Buyer 1—whose order has been sitting in the pool for a few minutes—wants to buy 500 shares. Buyer 2—who just entered the pool seconds ago—is looking to buy 10,000 shares. And Seller 1—who also just entered the pool—has a total of 1,000 shares to sell.

Does Buyer 1—who was the first to enter an order—get all of their shares before Buyer 2 gets any? On a lit exchange that would be the outcome. Or does Buyer 2 get all the shares because their order was the biggest? Because dark pool rules are not disclosed, traders may have no clue how their order interacts with other orders in the dark pool.

Clients of dark pools can request that a dark pool share information about their order handling processes. But, currently, dark pools are not required to share such information.

Exchanges, like NYSE and NASDAQ, are required to file their trading rules with, and have them approved by the SEC. This allows traders to know the rules that govern the trading of stocks on the exchange.

But, importantly, dark pools do not have a monopoly on dark trading. Current public exchange rules also allow dark, and partially dark order types. Traders can use a fully dark order type, similar to a dark pool order. And traders can also enter what is known in the markets as an “iceberg order” (also known as a “reserve order”)—where only a small portion of a larger order is visible to other traders. The tip of the iceberg is visible but the bulk of the order remains below the surface—invisible to other traders. As trades occur against the visible portion of the order, hidden shares emerge and become the new tip of the iceberg.

Who Controls Access to Dark Pools?

Dark pools are exclusive clubs—up to a point. Broker-dealers, like Credit Suisse and Goldman Sachs, who own dark pools are allowed to restrict access to their pools. They can deny access to a competitor or someone who’s trading style they believe will be disruptive to their customers in the pool.

As the SEC stated in their 2010 Market Structure Concept Release, “dark pools are not required to provide fair access unless they reach a 5% trading volume threshold in a stock."8

Once the 5% level is breached, the dark pool is required to establish clear rules for granting access to the pool. This assures that all investors will be able to access the venues where a stock is most actively trading.

Conversely, lit exchanges are essentially open to the public. They must offer non-discriminatory access to qualified broker-dealers. Exchanges are prohibited from having “unfairly discriminatory terms that prevent or inhibit” investors from trading against the best bid or offer displayed in the national exchange market.9 This rule is in place to ensure that investors have access to the best price available in the public market.

Conclusion

Each morning when the equity market opens the search for liquidity begins anew. Investment fund managers must locate the trading venues—dark and lit—where they can execute their investment strategies in the most efficient way. Successful investors are always seeking ways to maximize investment returns and minimize the cost of trading.

Dark pools are one specialized venue where 15% of stock transactions take place—the modern day equivalent of a hidden order ticket. Yet, the term “dark pool” is awash in negative connotations. The reality is that dark pools are a modern invention created by traditional market demands.

Of course, too much of a good thing can be bad. Lit bids and offers support the process of price discovery—or the ability to establish a security’s fair market value. Ensuring that displayed prices in the lit markets are accurate indicators of fair market value is critical for the U.S. equity market. If, in the future, dark pool trading makes up a preponderance of the equity market’s volume—and investors become reluctant to post a lit bid or offer—that will be an issue for policy makers to address.

But, lit markets offer two crucial things—clear prices and instantly accessible bids and offers—that investors value highly. Dark pools do not offer investors these two essential benefits of lit trading. Therefore, it is likely that the lit markets will retain a significant percentage of the equity market’s volume.

As policymakers continue to debate reforms to strengthen the equity markets, they should seek to preserve innovations—like dark pools—that investors benefit from, while also seeking to ensure that overall market quality is protected.