Report Published April 2, 2015 · Updated April 2, 2015 · 20 minute read

Cellulosic Ethanol is Getting a Big Boost from Corn, for Now

Takeaways

- Cellulosic fuels offer economic, environmental, and national security benefits, but scaling-up the technology has proven difficult and costly.

- Companies with an extensive background in the corn ethanol industry are cracking the cellulosic code, with projects that account for more than 80% of commercial capacity in the U.S.

- Continued investment from these companies in facilities and innovation is critical to growing U.S. cellulosic capacity, especially in the near term.

- Certain proposals to reform the Renewable Fuel Standard would discourage engagement from the corn ethanol industry, delay the commercialization of cellulosic ethanol in the U.S., and steer this investment overseas.

The federal government has aggressively pursued cellulosic biofuels for well over a decade. Commercial production of cellulosic biofuels, made from fibrous, non-edible plant material, would give the U.S. a way to dramatically lower its greenhouse gas emissions, reduce its reliance on petroleum, and create new opportunities for growth in the agriculture and technology sectors.

Getting cellulosic technologies out of the lab and into large scale production has taken longer than expected and continues to be a challenge. A far-reaching biofuels mandate known as the Renewable Fuel Standard (RFS), along with billions of dollars in R&D and demonstration investment have brought cellulosic fuels to the cusp of success. Still, only a handful of companies have been able to squeak past technical and economic challenges to open commercial-scale plants. If these companies can replicate the success of their initial projects and drive down costs, the U.S. might have found a way to unlock the benefits of cellulosic fuels. That is, unless efforts to reform the RFS inadvertently stop this progress in its tracks.

Alluring but Elusive: The Quest for Cellulosic Biofuels

Ever since the Arab oil embargo in the 1970’s—and the gasoline shortages and price shocks that accompanied it—the U.S. government has pursued a number of ways to reduce its reliance on foreign petroleum, including the use of biofuels.1 The effort to expand domestic production of renewable fuels was accelerated in 2005 when the RFS went into law. The policy required the blending of at least 7.5 billion gallons of renewable fuels into the nation’s fuel supply by 2012.2 It was widely assumed at the time that virtually all of this mandate would be met with America’s rapidly increasing stocks of ethanol produced from corn starch.3 Still, few expected the RFS to be as effective in boosting corn ethanol production as it ended up being—with the industry meeting its 7.5 billion gallon goal in 2007, a full five years early.4

Seeing even greater opportunities for domestic biofuels, Congress and then-President George W. Bush expanded the RFS in 2007 and created an explicit new goal for the program—the development of a second generation of renewable fuels made from non-corn feedstocks. The updated RFS mandated the blending of 36 billion gallons of renewable fuels by 2022, but allowed standard corn starch ethanol to count for no more than 15 billion of those gallons. The rest would have to come from a combination of specifically designated fuel categories, with the vast majority of the requirement met by cellulosic fuels.5

Congress had several reasons to pursue this particular biofuel technology. Cellulosic fuels have a very small carbon footprint, emitting up to 115% less greenhouse gases than gasoline (compared to an average reduction of 34% from corn starch ethanol).6 They also can be produced from a wide variety of feedstocks, providing agricultural opportunities in regions across the country, on land that might not be suitable for other crops, and using biomass materials that are currently treated as waste.7 Finally, developing fuels from cellulosic plant materials would allow for increased levels of biofuel production while minimizing the diversion of grains like corn away from the livestock feed supply.8 Because of these superior characteristics, cellulosic fuels sidestep much of the criticism levied by opponents of biofuels in general and enjoy a broader base of political support.

Despite Congress’s best efforts, production of cellulosic biofuel has lagged far behind the levels outlined in the 2007 RFS legislation. The policy called for cellulosic fuels to start reaching U.S. gas tanks in 2010, but the path to large-scale production has proven longer and much more difficult than anticipated.9 Several projects have failed along the way, while other companies succeeded in completing small demonstration facilities but thus far have been unable to scale production up to larger plants.10 The industry was able to produce commercial volumes of cellulosic ethanol and generate credits under the RFS in 2014, but the total for the year was very small—less than 1 million gallons.11

Corn Ethanol Industry Leading the Charge for Cellulosic

Although attempts to harness the immense environmental, economic, and national security benefits of cellulosic ethanol have largely been thwarted, the U.S. might have found a partner that can help break the logjam—its corn ethanol industry.

Several small and upstart firms have successfully reached pilot phase and even completed small-scale demonstration projects, and they may still take their cellulosic technologies to the next level. But so far, getting to commercial-scale plants that can produce meaningful quantities of fuel has been less romantic than a Silicon Valley success story. For the most part, these larger plants have been spearheaded by established companies with a sizeable presence in the corn ethanol industry as producers, suppliers, or service providers. In fact, projects sponsored by three of these companies (Abengoa, POET/DSM, and Quad County Corn Processors) account for over 80% of total U.S. cellulosic ethanol capacity. That number will rise to 88% once a fourth company (DuPont) opens its cellulosic facility later this year.12

Third Way examined these four companies to determine what kinds of advantages their common background in first generation ethanol may have afforded them; how these types of companies could help the U.S. realize its cellulosic goals; and how their contribution to cellulosic development would be affected by certain RFS reform proposals.

The Advantages of Having a Corn Ethanol Connection

In analyzing the biofuels industry, Third Way found that there are two main obstacles to commercializing cellulosic ethanol: technology and economics. The four companies we examined found a number of ways to capitalize on their first generation backgrounds in order to overcome the technological and economic challenges that continue to stifle most other cellulosic projects.

Overcoming Technology Challenges

Making cellulosic ethanol requires enzymes that can break down cell walls and access sugars in the cellulose of plant material.13 Developing the enzymes and other technologies to do this cost-effectively and at a large scale has proven to be a complex and costly endeavor—one that has stifled many an attempt to reach commercialization. Today’s cellulosic ethanol producers have addressed this issue by taking advantage of in-house R&D capabilities that they developed through their corn ethanol businesses, and by coaxing top biotechnology firms into strategic partnerships.

Using In-House Expertise

Large and flexible R&D budgets and a deep pool of institutional knowledge have given some of these first generation companies an advantage in developing cellulosic biofuels. Abengoa, for instance, maintains a large permanent innovation operation, spending more than $200 million on bioenergy technology development in 2013 alone.14 The company has amassed expertise in enzyme technology through its corn ethanol business, aiding its development of a proprietary enzyme specifically for cellulosic ethanol production.15 Similarly, DuPont leveraged existing customer relationships and R&D operations in corn genetics, agribusiness, and chemicals to create its own cellulosic technology.16 Each company has used its decades-long background in multidisciplinary research to address unanticipated technical setbacks and fine-tune their commercial cellulosic facilities.17

Luring the Right Technology Partner

While in-house R&D operations can be helpful in developing cellulosic technologies and troubleshooting challenges, some first generation companies also have taken advantage of their existing facilities and reputation within the industry to attract partners who can supply the technology. For example, POET entered into a joint venture with Dutch technology giant, Royal DSM, to develop proprietary enzymes for their cellulosic facility. A major draw of this partnership for DSM was POET’s fleet of 27 corn ethanol plants, which could provide significant demand for the new cellulosic technology and the potential for long-term profitability.18 Technology partners have also been secured by some first generation companies to scale-up the cellulosic innovations developed in-house. For instance, Quad County Corn Processors entered into a licensing agreement with Syngenta, a large biotechnology company with expertise in engineering corn for ethanol, to expand production of its proprietary cellulosic fermentation technology.19

Overcoming Economic Challenges

Even if it finds the right technology, a company still has to prove that its cellulosic ethanol plant will make money consistently over the long-term and provide a competitive return on investment. Like any “first of a kind” project, cellulosic facilities are expensive to build—roughly 5 times the per-gallon cost of a standard corn ethanol plant.20 And because of the technology and regulatory risks associated with cellulosic projects, the few lenders who are willing to invest expect incredibly high returns.21 The first generation companies that have overcome this challenge used resources and expertise acquired from their corn ethanol businesses to secure financing and to cut their capital and production costs.

Securing Financing in a Tough Market

The financial crisis and instability in federal biofuels policy in recent years have dampened investor interest in U.S. biofuels generally.22 But the technology risks of cellulosic ethanol projects, publicized by several high-profile failures, have made venture capital and private equity financing for these plants even harder to come by.23 To overcome these financing challenges, established companies in the ethanol industry have taken advantage of opportunities that would be harder for the average cellulosic startup to access.

One alternative has been simply to self-finance. Abengoa’s bioenergy business has more than $2 billion in annual revenues and the company is committed to maintaining its position in the biofuels industry for the long-term.24 As such, it was both able and willing to invest an estimated $200 million of its own money to complete its cellulosic facility.25 DuPont, a Fortune 100 company with $35 billion in revenues in 2014,26 also self-financed its first cellulosic ethanol facility.27 In POET/DSM’s case, first generation assets helped secure financial support through a corporate partnership. POET used its large footprint in the corn ethanol industry to entice $150 million in financing from DSM for their joint venture.28

Since oil and gas companies have largely ceased this kind of major investment in advanced biofuels projects, the engagement of large, well-funded companies with existing interests in the biofuels industry is proving vital in helping to fill-in the investment gap.29

Cutting Capital and Operating Costs

Although the high capital and operating expenses of cellulosic ethanol facilities are expected to fall as the industry matures, getting to that point will require the first several iterations of plants to employ creative methods of reducing or offsetting cost in order to get up and running.

One method that first generation biofuel companies have used to lower cost is co-locating facilities. The cellulosic operations at both Quad County Corn Processors and POET/DSM are “bolt-on” expansions added to existing corn ethanol plants. This allows cellulosic production to piggyback off of existing access roads, rail spurs, water lines, and electric distribution infrastructure, avoiding major capital expenses and lowering the overall cost of the cellulosic project. The avoided cost of rail infrastructure alone can be millions of dollars, illustrating just how much of an impact can be had on a project’s bottom line by co-locating at a corn ethanol facility.30

These companies are also defraying some of their production costs by generating valuable co-products along with their cellulosic ethanol. POET/DSM is combusting leftover feedstock material from its cellulosic refining process to generate steam and biogas that can then be sold. This biogas, for example, will completely displace the natural gas currently used by the neighboring POET corn ethanol facility, which is twice the size.31 Quad County Corn Processor’s bolt-on cellulosic technology increases corn oil yield and creates a higher protein feed product for the livestock industry. Both of these co-products represent additional revenue streams that support the profitability of cellulosic production.32

Building a large-scale production facility that relies upon an uncommon feedstock requires the sponsor of a cellulosic project to create an extensive and affordable supply chain, from scratch, in a relatively short period of time. POET/DSM expedited this process at its cellulosic facility by taking advantage of POET’s relationships and reputation with more than 600 growers who had supplied POET’s existing first generation ethanol plant.33 Similarly, DuPont used its in-house expertise in enzymes for corn ethanol production and its relationships with researchers at Iowa State University, USDA’s Natural Resource Conservation Service, and harvest equipment manufacturers, to develop its plan for supplying 375,000 tons of agricultural residues to its cellulosic facility each year.34

Replicating Success: The Path to Broad Deployment of Cellulosic

Of course, the opening of a handful of commercial-scale plants does not constitute a “mission accomplished” moment for cellulosic ethanol—the combined 85 million gallons of capacity of all four plants we examined can produce a tiny fraction of the 16 billion gallons of cellulosic fuel ultimately envisioned in the RFS. But these initial successes are a critical step toward greater deployment of cellulosic technology by first generation companies. This will strengthen the companies’ ability to replicate their models and establish cellulosic ethanol as an economically viable commodity.

Companies that have achieved commercial cellulosic production continue to fine-tune their proprietary technologies and have identified improvements to increase the efficiency of their supply chain and plant operations.35 These improvements will increase the profitability of their existing cellulosic facilities but will be particularly impactful when incorporated in the early planning stages of subsequent plants. Internal estimates from some of these companies indicate that these insights could result in cost reductions of 25% in their next round of plants.36

All four of the first generation companies we examined have business plans to rapidly expand their cellulosic technology to additional facilities, in some cases adding 3.5 billion gallons of capacity.37 The experience gained from this increase in scale could put significant downward pressure on the cost curve for cellulosic ethanol technologies, paving the way for even greater market penetration.38 Unfortunately, new challenges have emerged that could deter first generation companies from sponsoring additional projects. Unusually low oil prices, for example, are eating into corn ethanol’s profit margin and could leave the entire industry less able or willing to pursue major investments like cellulosic projects.39 But an even larger and more permanent deterrent to first generation engagement in cellulosic ethanol would be created if certain proposals to alter the RFS are successful.

RFS Proposals Would Take the MVP Out of the Cellulosic Game

Disagreements surrounding climate benefits, land use change, and food displacement have polarized the RFS debate. But there is general consensus that, if these concerns have any validity at all, they are much less of an issue with cellulosic ethanol and other advanced biofuels than they are with corn ethanol.40 Some legislators, therefore, are targeting corn ethanol alone in their RFS reform efforts in the hope that they can address their concerns without disrupting the development of second-generation fuels.

While proposals to gut only the corn section of the RFS may not be intended to endanger the development of cellulosic ethanol, this is exactly what would occur. Given the nuances of current fuel markets and how they interact with the RFS, these proposals will discourage cellulosic ethanol investment by companies with a large stake in corn ethanol—the very companies that are helping to commercialize this long-sought fuel.

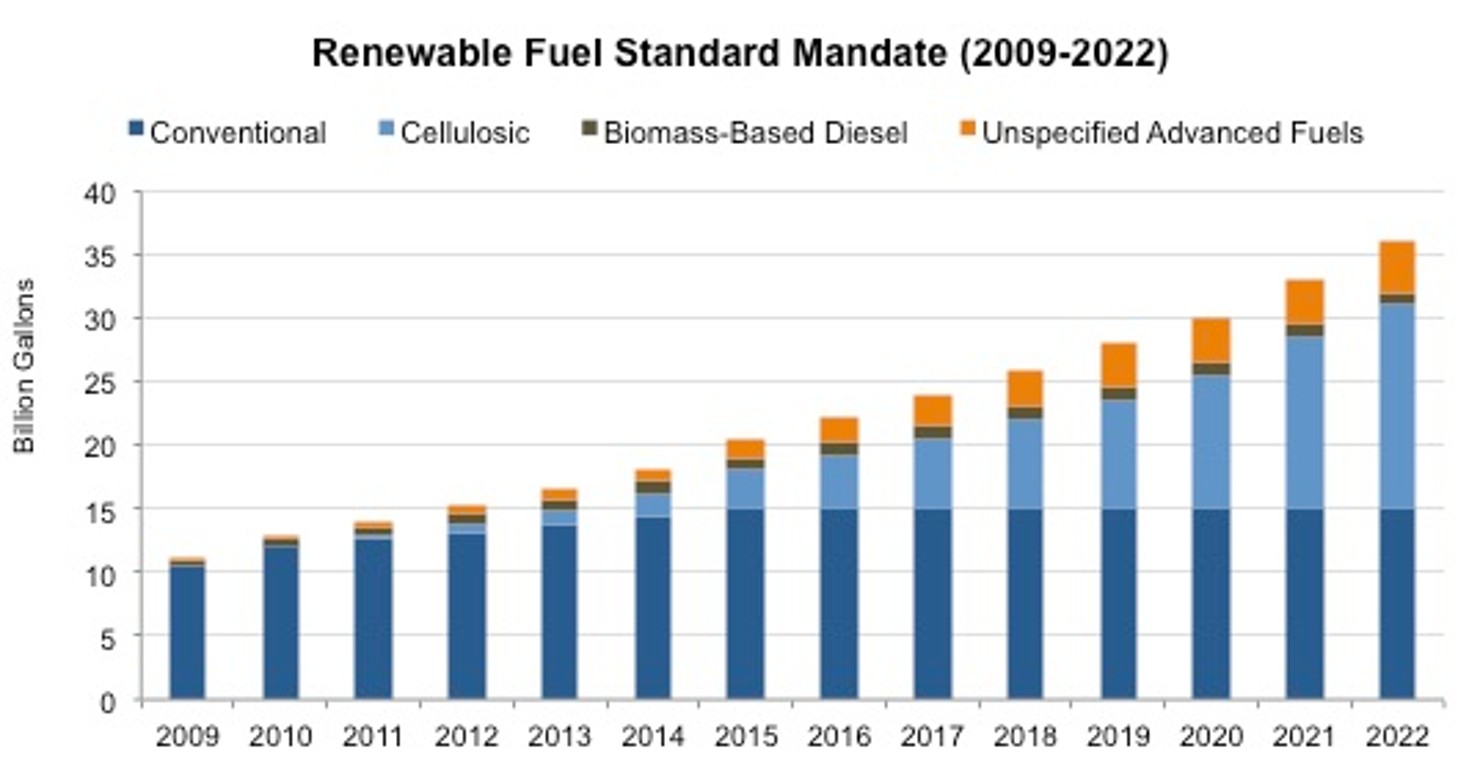

The details of these corn-gutting policy proposals vary somewhat, but the main thrust shared by all is the complete removal of corn-based biofuels as an eligible fuel for meeting the requirements of the RFS. They would also reduce the statutory requirement for total renewable fuels in any given year by the amount of corn-based fuels that is removed by the new policy.41 For example, the total required volume for all renewable fuels in 2022 would fall from 36 billion to 21 billion gallons, and would have to be met using a combination of only biodiesel and advanced and cellulosic fuels (no corn). Please refer to the Appendix section of this report for a chart showing RFS statutory requirements.

Corn Ethanol Already Has a Ceiling

If the goal of these proposals is to stop the growth of corn ethanol, they will have little impact. That is because no substantial growth in corn ethanol production is expected anyway. The RFS statute requires total blending volumes for all biofuels to grow steadily each year, reaching 36 billion gallons by the end of the program in 2022. Corn ethanol’s contribution to this total is explicitly limited, however, since the statute prohibits the use of more than 15 billion gallons of corn ethanol for RFS compliance. The industry already has 15 billion gallons of corn ethanol capacity42 and can actually produce beyond that level with its existing plants.43 This leaves little room for corn ethanol growth before hitting the RFS limit. Corn ethanol producers have little incentive to produce much beyond the 15 billion gallon cap, as these additional gallons would not be eligible for RFS credits (“RINs”), and therefore would be much less attractive in the marketplace and sufficiently more difficult to sell.44 And oil companies clearly are not interested in displacing any more of their product with biofuels than they absolutely must. This corn ethanol “ceiling” is a major reason why first generation companies seeking growth opportunities in the U.S. have begun investing in second generation technologies like cellulosic ethanol.

Corn Ethanol Also Has a Floor

In spite of its intense lobbying campaign against the RFS, the oil and gas industry actually wants ethanol—at least up to a certain point. This may seem counterintuitive, since biofuels compete with petroleum for space in the fuel tank. But because of its high octane content, ethanol is a desirable “oxygenate” and octane-boosting additive that improves the efficiency of gasoline combustion and reduces emissions of certain regulated pollutants.45

From the oil industry’s perspective, the optimal mix of ethanol for this purpose is roughly 10%.46 The U.S. consumed 137 billion gallons of gasoline in 2014.47 So theoretically, there would have been demand for about 13.7 billion gallons of ethanol as an octane booster and oxygenate that year—even without the RFS. Because of its low price and availability, that ethanol demand would be met almost entirely by the 15 billion gallons of capacity at existing corn ethanol plants.48 Export demand would occupy much of the remaining capacity not used for the octane/oxygenate market.49 In essence, eliminating the corn ethanol portion of the RFS requirement would not significantly reduce corn ethanol production—unless cellulosic ethanol were available to economically meet the oil and gas industry’s octane boosting and oxygenate needs.50 Producing this quantity of cellulosic ethanol in the near term would be a nearly impossible task. And, as explained in the next section, it would need to be accomplished without the help of companies engaged in corn ethanol production.

Proposals Create a “Gallon In, Gallon Out” Situation

Under a business as usual scenario, the total RFS requirement would continue to grow toward its 2022 peak of 36 billion gallons. Corn ethanol blending could continue (up to its 15 billion gallon cap), and any cellulosic fuel that was produced would be blended in addition to that volume. Under these conditions, companies with a stake in corn ethanol production would be willing to continue investing in cellulosic ethanol. The same willingness would not exist under a corn-gutting policy.

Without the demand previously created by the RFS, corn ethanol producers would rely on octane and oxygenate demand (13.7 billion gallons) to find a home for basically all of the fuel produced each year by its existing plants (with some of the remaining capacity used to produce fuel for export). But because the RFS would still cover cellulosic fuels, obligated parties would have to blend every gallon of cellulosic ethanol that became available, essentially giving cellulosic ethanol “dibs” on the limited oxygenate demand. Put simply, every gallon of cellulosic capacity that came online would cause the displacement of a gallon of capacity at an existing corn ethanol plant.

For context, if POET/DSM constructed another cellulosic facility like the one they opened in 2014, 25 million gallons of existing corn ethanol capacity would be displaced by cellulosic, resulting in the loss of $50 million worth of capital investment and $142 million in lost revenue to the corn ethanol industry.51 Under these circumstances, companies with an interest in corn ethanol would be shooting themselves in the foot by investing in new cellulosic projects.

The Bottom Line

Replacing corn ethanol with cellulosic may sound like the perfect outcome to some supporters of corn-gutting policies. In practice, however, this approach is highly unlikely to produce the desired results. By disengaging first generation industry from the effort, it greatly reduces the odds of achieving substantial cellulosic ethanol production, especially in the near term. And without large quantities of cellulosic ethanol to serve as a substitute, current levels of corn ethanol will still be produced in order to meet the oxygenate needs of the gasoline supply.

Conclusion

Commercially-available cellulosic ethanol would help the U.S. meet its climate goals, generate economic growth in the agriculture and technology sectors, and provide an additional hedge against volatile oil prices. Development of cellulosic ethanol technology has taken longer than policymakers hoped. But the pace of innovation has been impressive nonetheless, and the first commercial facilities are now up and running—thanks in large part to the engagement of the corn ethanol industry. By capitalizing on their existing resources, relationships, and industry knowledge, these first generation biofuels companies are able to overcome the economic and technological challenges that continue to stump others seeking to “crack the cellulosic code”. Continued investment from these companies in facilities and innovation would provide a needed jumpstart to cellulosic commercialization in the U.S. But a number of proposed changes to the RFS, however innocuous they may seem, would remove any incentive for the first generation industry to continue supporting cellulosic ethanol. At this critical stage in their development, cellulosic fuels can hardly afford to lose the closest friend they have.

Appendix

Source: Energy Independence and Security Act of 2007 (P.L. 110-140)

Conventional: This category refers to renewable fuels that achieve at least a 20% reduction in lifecycle greenhouse gas emissions compared to a petroleum-based equivalent like gasoline or diesel. Though cellulosic and other advanced fuels qualify for it, the conventional biofuels category currently is met almost entirely by corn starch ethanol. The annual values of this category indicate the maximum volume of corn starch ethanol that can be used to meet the total RFS volume requirement in a given year.

Cellulosic: Cellulosic fuels must be produced from cellulose, hemicellulose, or lignin and must achieve at least a 60% reduction in lifecycle greenhouse gas emissions compared to a petroleum-based equivalent. The values for this category indicate the minimum volume of cellulosic fuels that must be blended.

Biomass-Based Diesel: This category refers to any biomass-based diesel fuel that achieves at least a 50% reduction in lifecycle greenhouse gas emissions compared to a petroleum-based diesel. The values for this category indicate the minimum volume of biomass-based diesel that must be blended.

Unspecified Advanced Fuels: This category can be satisfied by biofuels that achieve at least a 50% reduction in lifecycle greenhouse gas emissions compared to a petroleum-based equivalent. This includes, but is not limited to, any fuel that qualifies as cellulosic fuel or biomass-based diesel.