Memo Published February 8, 2017 · Updated February 8, 2017 · 13 minute read

Why We Shouldn’t Re-Privatize the Federal Student Loan Program

Tamara Hiler

Should private lenders have a role in the federal student loan program?

Many believed this question was settled in 2010 when Congress eliminated the Federal Family Education Loan (FFEL) program, which had used private banks and some nonprofit agencies to serve as lenders for federal student loans, with government backing. Since that time, the Department of Education has served as the sole lender and administrator of all new non-Perkins federal student loans issued under Title IV of the Higher Education Act, leaving private institutions to lend to students only through the private market. But this year’s changing of the guard in Washington has re-opened new conversations about reversing this policy, especially as language in the 2016 Republican Party platform explicitly states that, “private sector participation in student financing should be restored.”1

But the FFEL program was eliminated in 2010 because the federal government was paying third-party entities billions in taxpayer subsidies to carry out the same lending functions the Department of Education is capable of handling on its own. As a result, many policy experts and economists on both sides of the aisle have raised concerns that any efforts to restore a FFEL-like program would mark an unnecessary reversal back to a system that is both overly-convoluted and costly, and would do nothing to address the most pressing problems facing our higher education system today—like reducing the cost of getting a degree or increasing completion rates across campuses. So while some may be eager to restore a FFEL-like system because of an ideological desire to get the private market back into federal student lending, this memo offers a brief explanation of why doing so would negatively impact both taxpayers and students alike, and would do nothing to lessen the role of the federal government in our student loan system.

FFEL vs. Direct Loans

For nearly 60 years, the federal government has been in the business of administering student loans. This involvement has historically been driven by a desire to help a greater share of students access postsecondary opportunities, including those who may have been traditionally deemed “too risky” to secure financing through the private markets. Over the years, the process of administering federal student loans has taken on many forms, including two very distinct models: guaranteed vs. direct lending.

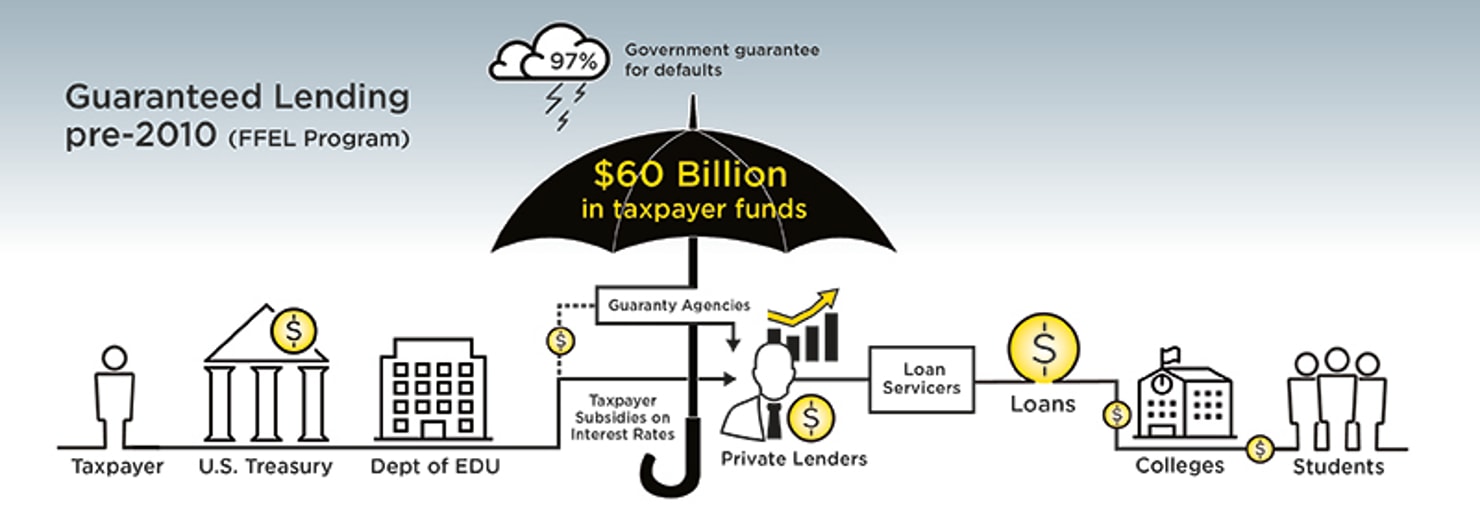

The Federal Family Education Program (FFEL): A Guaranteed Lending Model (1965-2010)

In 1965, Congress established its first guaranteed student loan program—now known as the Federal Family Education Loan (FFEL) program—as a way to help the federal government delay the upfront costs of administering student loans by guaranteeing (or insuring) loans being made through third-party private lenders rather than having them come directly from the federal government itself.2 This meant that the federal government, through its agreements with state and other private, non-profit guaranty agencies, contracted with lenders like Sallie Mae to disburse student loans using funds raised through the private markets. But because federal student loans weren’t very profitable given that their interest rates were set not by the market but by federal law, the government had to provide special incentives in the form of taxpayer subsidies as a way to encourage the private lenders to participate in the FFEL program.3 A second inducement was also needed to encourage lenders to provide loan access to all students (including low- and moderate-income students who may appear riskier on paper), so the federal government worked with third-party guaranty agencies to guarantee up to 97% of a loan’s outstanding principal and interest. This meant that even though the federal government wasn’t directly lending the money to students itself, it was still responsible for paying lenders for those loans in the case of default, an action that ultimately put taxpayers—not private lenders—on the hook for the cost of default.

A turning point for the FFEL program came on the heels of the 2008 financial crisis, when the federal government was forced to step in and provide much-needed capital to private FFEL program lenders as a lifeline to ensure these lenders did not simply stop issuing all new student loans.4 Through the Ensuring Continued Access to Student Loan Act (ECASLA) of 2008, Congress allowed the federal government to buy loans directly from FFEL lenders—a process that essentially rendered private banks and loans moot in the lending process, because the government was ultimately bankrolling the student loans.5 This situation accelerated an ongoing trend of private lenders making the choice to leave the federal student loan business, paving the way for Congress to eliminate FFEL altogether as part of 2010’s Student Aid and Fiscal Responsibility Act (SAFRA) law.

The William D. Ford Federal Direct Loan Program: A Direct Lending Model (1992-Present)

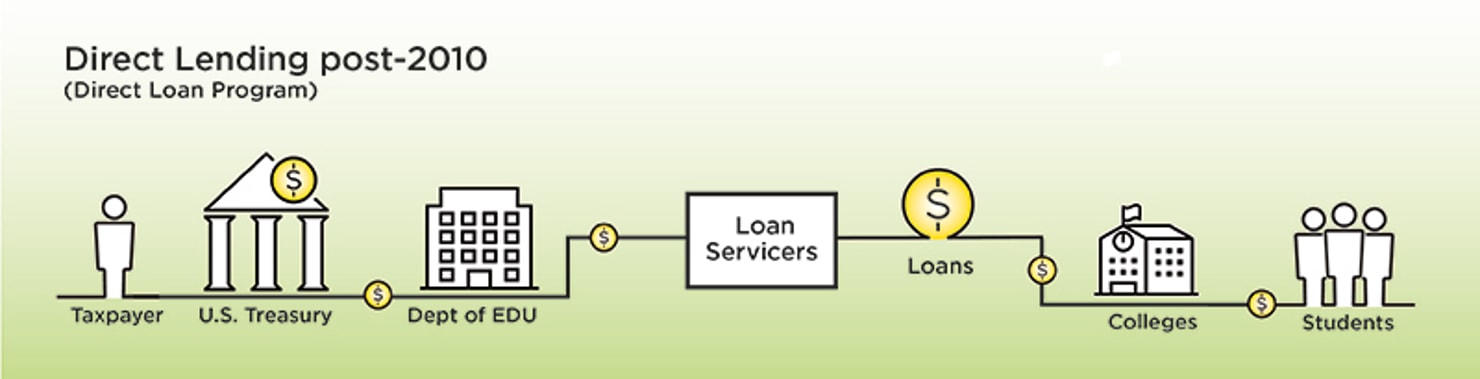

Congress created the William D. Ford Federal Direct Loan Program in 1992 as a pilot to test whether it would be cheaper and easier to have the federal government disburse student loans itself.6 Unlike its guaranteed lending counterpart, the Direct Loan program cut out the use of third-party private lenders and guaranty agencies altogether by instead having the Department of Education fund loans directly to students through the United States Treasury.7 This structure makes the federal government the creditor and collector of all accounts, contracting only with private entities and other non-profit organizations to help service the loans. Using this type of direct lending model creates a more streamlined process since it cuts out the third-party “middlemen” (i.e. private lenders and guaranty agencies) that exist in guaranteed lending programs like FFEL.8

It is the success of this simplified structure (whose benefits became even more apparent during the financial crisis of 2008) that ultimately solidified Congress’ decision to eliminate the FFEL program in 2010. Today, the federal student loan program operates under a 100% direct lending structure, making the Department of Education the sole provider of all federal student loans (private lenders can still issue student loans, they just aren’t backed by government funds).

Why We Should Stick with Direct Lending

With the ushering in of a new Administration, questions have already begun to surface about whether the structure of the federal student loan program will once again change. While no new proposals have been laid on the table to date, there are concerns that Congress may work with the Trump Administration to reinstate the role of private institutions—like banks and credit unions—in the process of originating, collecting, and overseeing the administration of federal student loans. Critics claim that today’s direct lending program is a government takeover of the student loan business, however there is no evidence to demonstrate that reestablishing a guaranteed lending model like FFEL would do anything to reduce the government’s role in the federal student loan system. Many believe that doing so would be little more than ideological exercise at the expense of having a more streamlined and efficient lending process in place. There are three reasons Congress would be wise to maintain the direct lending system that exists today.

Direct lending is more efficient and saves taxpayers billions of dollars.

According to a 2010 report by the Congressional Budget Office (CBO), the transition from the FFEL program to the fully-direct lending model will save the federal government more than $60 billion between 2010 and 2020.9 These savings are in large part due to the fact that direct lending ended the costly subsidies and administrative fees the government was paying to incentivize private lenders to participate in the FFEL program in the first place. The most expensive taxpayer subsidies came in the form of quarterly “special allowance payments” paid to private lenders when interest rate rates set into law for students by the Higher Education Act (HEA) were lower than market rates.10 Essentially, Congress agreed to cover the difference between what the borrower paid and what the lender could have gotten at the going rate for other types of consumer lending, because Congress limits how high an interest rate students can be charged for federal student loans. That meant that lenders were actually earning interest on FFEL loans from the federal government, and not the actual borrowers themselves.11 As a result of these subsidies, a New America report found that “the FFEL program had a 67% higher cost structure than the Direct Loan program,” ultimately transferring money from taxpayers into the pockets of banks and other private lenders.12

In addition, because third parties were integral to the FFEL system—including the guaranty agencies that insured the loans for these lenders—the federal government was also paying administrative costs to lenders and guaranty agencies to handle the loans and support the costs of their default loan collection.13 By switching to a direct lending model, the federal government has been able to cut out these unnecessary middlemen and ensure that taxpayer dollars are going towards programs that serve the public interest rather than profiting banks and other financial institutions. Notably, the savings generated by eliminating the wasteful subsidies and administrative costs affiliated with FFEL have gone in part towards a reinvestment in the Pell Grant program, which helps millions of low- and moderate income students attend college each year. In fact, FFEL’s discontinuation has allowed mandatory funding for the Pell Grant program to receive an annual cost-of-inflation increase every year through at least 2017—ensuring that Pell continues to cover a greater share of college costs for the students who need financial assistance the most.14

Guaranteed lending has no direct benefit to students.

There is an argument to be made that having third party lenders in the system could be justifiable (despite their cumbersome nature and high costs to taxpayers) if their presence in some way provided clear, additional benefits to the students they served. However, there has been no evidence to suggest that the reintroduction of private institutions in the loan origination and oversight process would do anything to reduce college costs or improve the borrowing experience for students in any way. If anything, there is reason to believe that a reversion back to a FFEL-like system could negatively impact students, either by exposing them to predatory practices by some banks and other private lenders, or by creating unnecessary confusion for students looking to navigate the loan process.

One of the key motivations for taking private institutions out of the federal loan system was to permanently eliminate the questionable practices some lenders used during the FFEL program, including doling out kickbacks to institutions in order to be included on “preferred lender lists” or using cash-based inducements to encourage students to take out more loans.15 Prior to SAFRA’s passage, FFEL lenders were sued by a group of state Attorneys General for questionable practices like offering students $50 to refer their peers or paying them bonuses of $1,000 for taking out new loans.16 And while federal law at the time prohibited this type of activity, lax enforcement allowed these practices to continue unabated.17 This means that even if safeguards are put into place, reintroducing private lenders back into the system could once again open the door for private lenders to put their business interests ahead of the best interest of students.

Upending the lending process again would also create unnecessary operational challenges for institutions, which could negatively impact the lending process for millions of students. Adding private lenders back into the system would require both time and money for institutions to update their systems—directing critical resources away from other programs geared towards providing student supports. According to a survey conducted by the National Association of Student Financial Aid Administrators, nearly two-thirds of aid administrators “found the administrative burden to be less severe in Direct Lending than in the FFEL program”—giving aid administrators more time to focus on best serving the needs of students trying to navigate the loan process.18 The introduction of a new guaranteed lending program could also create more confusion during the repayment process for students who take out various types of loans. For example, prior to FFEL’s elimination in 2010, students who had one FFEL loan and one Direct Loan were required to submit separate monthly payments, increasing their risk of default as they juggled multiple accounts.19 While many policymakers across the ideological spectrum have argued we need to further simplify the loan process for students today, establishing a new government-backed loan program would do exactly the opposite.

Returning to a FFEL-like program would not reduce the federal government’s involvement.

If the idea behind trying to change the lending system is to get the federal government out of the lending business, reviving a FFEL-like system would in no way accomplish that goal. The guaranteed lending model involves the use of “government-backed loans,” meaning that the federal government and taxpayers—and not the banks themselves—are the ones on the hook if a student defaults on his or her loan. And as we saw during the 2008 financial crisis, it was the federal government that had to bail out private lenders who feared they would be unable to raise sufficient capital in the private markets—a fate that would no doubt repeat itself if a FFEL-like program were reinstated and the market faced turmoil again.20 So while critics like to claim that today’s Direct Loan program is a “government takeover” of the student loan business, the truth is that the federal government has always played and will continue to play an integral role, even if private institutions begin to administer federal student loans again.

It should also be noted that even though Congress eliminated the involvement of banks and nonprofit organizations as lenders in the federal student loan program, entities like banks and credit unions are still able to provide loans to students in the private market. Their share of total student loans is quite low (only 6% of students took out private loans in 2011-12), given that private loans tend to be more expensive than their federal counterparts and do not come with important benefits like automatic fixed interest rates and the ability to participate in income-driven repayment programs.21 But the fact that they can’t compete with the Direct Loan system isn’t a reason to subsidize private lenders. The question then is not whether or not both the private market and the government have roles to play in the student loan market, but rather whether it makes sense to spend taxpayer money to have banks serve as subsidized middlemen, as was the case under the guaranteed-lending model used by FFEL.

Conclusion

Reintroducing a FFEL-like program is not in the best interest of students or taxpayers. Not only would the reintroduction of such a program represent a big step backwards in the effort to streamline the federal student loan system, it also makes little economic sense to send taxpayer dollars in the form of government subsidies back to private entities when there are no additional benefits to show for it. Spending time, energy, and money on reinstating a government-backed private lending program will do nothing to curb the rising costs at colleges or ensure that more students will graduate from postsecondary programs with the skills they need to secure well-paying jobs. Certainly there is room for improvement in the Direct Loan program, and we should make sure it operates as efficiently as possible, streamlining repayment and reducing defaults. But attempting to reintroduce costly middlemen does little more than distract from Congress’ ability to tackle these issues in a thoughtful and bipartisan way.