Memo Published July 23, 2020 · 17 minute read

Rescue, Rebuild, and Reinvest: How to Save Clean Energy Startups

Farah Benahmed & Doug Rand

Clean energy technology startups have long been given the short end of the stick from both the federal government and the investment community. To make matters worse, the economic impacts of the COVID-19 pandemic have exacerbated an already dire situation for clean energy startups by drying up funding that was already scarce. The current level of investment is negligible compared to what we need to kickstart the economy, create high-paying clean energy jobs, and address the climate crisis.1

The federal government must step in to rescue, rebuild, and reinvest in clean energy startups. In this report, we propose a suite of policies to accomplish just that. We lay out rescue-oriented policies focused on helping clean energy entrepreneurs keep the lights on, followed by policies that double down on successful startup programs to help us rebuild. Finally, we offer transformative ideas for reinvestment to ensure the United States remains a technological leader in the fight against climate change.

By implementing these policies in a future stimulus, clean energy startups will have the financial support and technical resources they need to keep innovating. These policies will help give our country a fighting chance of staving off the worst effects of climate change by fostering the next generation of clean energy scientists and entrepreneurs. Acting ambitiously today to save and accelerate startup growth tomorrow will send a clear signal to the investment community to follow suit.

Why We Need Clean Energy Technology Startups

Every nation on the planet faces a dual challenge of decarbonizing its economy by mid-century and competing to capitalize on the economic opportunities of this clean energy transition. As a longstanding world leader in innovation, the United States has the institutions, resources, and capabilities to reap the greatest benefits as an inventor and exporter of clean energy technologies. But the United States isn’t currently investing enough in groundbreaking technologies to compete against countries like China.2 While the U.S. is renowned for driving energy innovation during important times in history (e.g., nuclear power during the Cold War and the shale revolution after the 1970s oil embargoes), we have yet to go all in on clean energy.3

The status quo was insufficient before COVID-19, and it’s only getting worse. Leading the global energy transition requires thousands of U.S. startups working right now on complex technologies that may take years (or decades) to reach the market. Today’s clean energy entrepreneurs—and the thousands of workers they employ—must stay afloat during tough economic times and make it out on top. New companies will need to be launched without waiting for a pre-pandemic bull market to rise again. An army of clean energy scientists and entrepreneurs still needs to be trained and set up for success.

Without immediately ambitious measures to sustain and grow the number of startups tackling clean energy challenges, there will simply be insufficient investment to satisfy the increasing appetite of global investors and industrial firms for decarbonization technologies in the decades ahead.4

The COVID-19 Crisis

COVID-19 has had a massive impact on this country. Well over 3.5 million Americans have contracted the disease, and over 138,000 lives have been lost. The pandemic has also harmed our economy faster and deeper than the financial crisis of 2008. Over 50 million people have filed for unemployment. Thousands of businesses are shutting their doors, never to come back again.

COVID-19 has also created immense uncertainty in the market as the pandemic runs rampant across the United States. As market volatility plagues investors, the venture capital community may very well be holding onto their cash and refraining from making new investment decisions.5 In fact, VC investment activity has plummeted 25% since the pandemic hit.6 Entrepreneurs face challenges in raising capital as they struggle through production and project delays and determine how to keep staff on payroll.7 On a good day, supply chain disruptions can be debilitating for startups, especially if they have near-term deadlines to meet, and the pandemic has thrown a wrench into the steady supply of materials.8

In short, the pandemic could take many companies down—especially capital-intensive clean energy startups—without concerted federal action.

Public and Private (Under)investment in Clean Energy Innovation

The United States was already dramatically underinvesting in clean energy entrepreneurs before the COVID-19 crisis. The federal government currently provides about $8 billion for energy innovation, conducted primarily at universities and national laboratories.9 Capital markets provide some $66 billion in investments in mature clean energy technologies throughout the United States.10 But there is a gap in investments for projects that fall between academic research and late-stage deployment—a gap infamously called the “valley of death.”11 Clean energy entrepreneurs often get stuck here, with new technologies that are too advanced for academic grants but still too risky for capital markets.

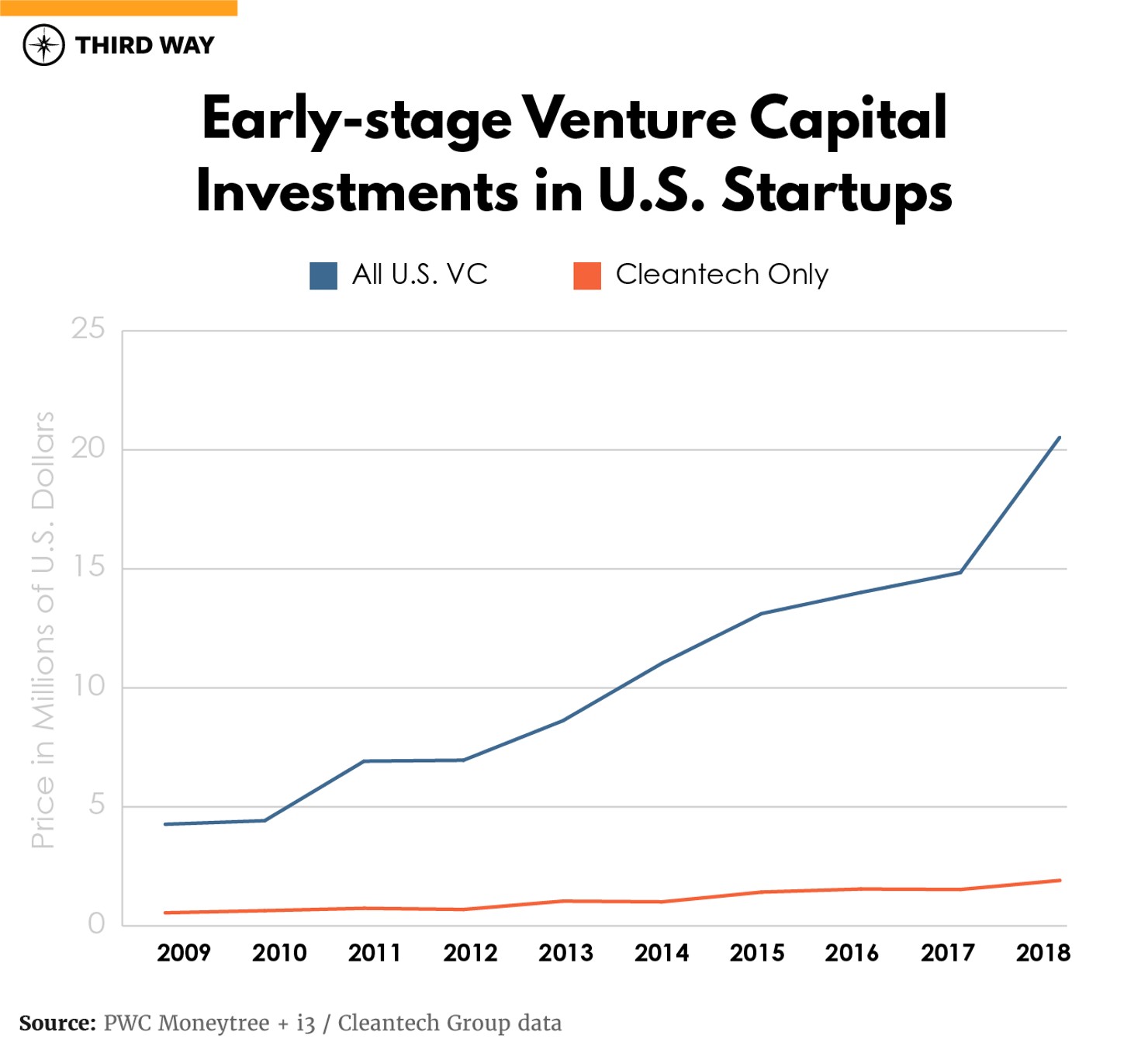

Venture capital can help bridge this gap, but clean energy startups currently receive only a small portion of VC investments (Figure 1). Between 2009–2018, VC funds made about 4,700 early-stage investments in U.S. clean technology startups, with the annual total growing from just over $500 million to just under $2 billion. During the same period, however, total early-stage investment in all U.S. startups skyrocketed to over $20 billion, with well over 3,000 transactions each year. This dramatic disparity does not bode well for the future of U.S. competitiveness in clean energy technologies or for a speedy path to decarbonization.

Figure 1: Early-stage venture capital investments in U.S. startups.12 (Source: PWC Moneytree + i3 / Cleantech Group data)

If VC is vital for the survival and success of a technologically innovative, capital-intensive company, it’s no surprise that relatively few clean energy entrepreneurs have been able to leave the starting gate—and that was before COVID-19 threw the entire startup ecosystem into crisis.13

Hard Tech Companies Have it Harder Than Others

It’s no secret that clean energy startups have a harder time attracting venture capital than other startups—but why?

Most clean energy startups are considered “hard tech,” meaning there is no guarantee that the technology will ultimately work out as planned.14 Based on this technology uncertainty alone, hard tech startups are a much riskier investment for venture capitalists, especially compared with pure software startups.15 Since the job of a venture capital fund is to invest someone else’s money into a profitable portfolio, it’s no wonder that hard tech startups are often left out of the picture.

Not all clean energy startups are categorically unattractive to venture capitalists. Some hard tech clean energy startups also have attributes of a software or biotech company, which have a long history of delivering significant returns on investment. Notable examples include Cruise Automation, which rapidly developed an autonomous vehicle software system and was acquired by GM for around $1 billion just three years after its founding; and Beyond Meat, which parlayed a large premium consumer market for plant-based meat alternatives into a successful initial public offering in 2019.

These blended cleantech/software and cleantech/biotech startups are largely responsible for the modest increase in total clean energy startup investments shown in Figure 1. We show this more clearly in Figure 2 by breaking down investments in clean energy technology startups by industry. There was an upswing in investments over the past decade in clean energy industries with a lot of software and biotech solutions—transportation and logistics, enabling technologies, and agriculture and food industries. In contrast, investments in clean energy startups in more exclusively hard tech industries—energy and power, materials and chemicals, and resources and environment—have seen scant, if any, growth in venture capital investments over the past decade.

Figure 2: Early-stage venture capital investment in U.S. clean technology startups, by industry.16 (Source: i3 / Cleantech Group data)

Figure 2: Early-stage venture capital investment in U.S. clean technology startups, by industry.16 (Source: i3 / Cleantech Group data)

The traditional venture capital model is designed to fund startups that resemble the big winners of the past several decades, i.e. software or biotech. That may be great for clean energy software or biotech startups, but it leaves an immense amount of essential clean energy innovation behind.

Given the long-run climate and economic benefits of clean energy startups, policymakers must be clear-eyed about the reality that many clean energy startups need more time and resources to prove out their technology and market readiness before professional investors will see a suitable risk/reward profile.

Policies to Rescue, Rebuild, and Reinvest in Clean Energy Startups

The U.S. government is well positioned to take on this challenge. The public sector can provide long-term financial support and technical expertise to innovative clean energy technologies until the private sector is ready to step in,17 saving and supporting clean energy startups that the United States and other countries desperately need to fight climate change.

The federal government must implement ambitious policies to support clean energy startups and entrepreneurs, leveraging private investment in order to overcome these looming challenges. These policies can be broken down into three categories: rescue, rebuild, and reinvest.

Rescue: Helping Clean Energy Entrepreneurs Keep the Lights On

The economic crisis caused by the COVID-19 pandemic has placed nearly all small businesses in a dire position, and clean technology startups are no exception. Congress must ensure that an entire generation of early-stage innovative companies—including clean energy startups—doesn’t die on the vine as part of its broader emergency measures to stabilize the economy and prevent further job loss. The following industry-agnostic actions would be relatively inexpensive and easy to implement compared with prior COVID-19 small business rescue measures.

- Temporarily waive cost-share requirements. Department of Energy research programs typically require awardees to achieve 20-50% cost-share from non-federal sources. This can be difficult for startups in the best of times and should be waived for the duration of the current national emergency.

- Eliminate government payment delays. Even when a small business successfully wins a federal agency contract or grant, they typically face a delay of 45–90 days before receiving the funds, awaiting final negotiations and payment processing. Congress should authorize the Treasury Department to make zero-interest advance loans to startups at the moment they receive a federal agency award notification.

- Fix PPP’s ability to reach startups. The Small Business Administration’s Payment Protection Program (PPP) should continue to process and accept loans, and receive increased funding in further rescue and recovery bills as needed. All small businesses that certify they need help in this crisis, including startups that are part of another firm’s investment portfolio, should qualify for relief through this program.18

- No-cost extensions and cash grants to keep existing government awardees afloat. Congress should provide no-cost extensions and supplemental funding to federal agencies, allowing them to send emergency payments to cover payroll and other expenses to any existing contractor or grantee that cannot meet its performance obligations due to disruptions caused by the COVID-19 pandemic (e.g. shelter-in-place orders, restricted access to lab facilities, etc.). These direct cash payments from federal agencies, including to existing Small Business Innovation Research (SBIR) awardees, would likely be more rapid and efficient than the Paycheck Protection Program (PPP), which relies on private-sector banks as intermediaries.

- Expand the SBIR Program to extend a lifeline to promising at-risk companies. Eleven federal agencies have longstanding SBIR programs that together provide over $3 billion per year to support innovative technology startups and small businesses. While many clean energy startups are struggling to make ends meet, Congress should provide supplemental funding of at least $300 million (allocated among these agencies) to immediately make awards of $100,000 to prior high-quality SBIR applicants that were not selected simply due to funding limitations at the time. Within the DOE alone, this would mean about $30 million spread across 300 additional small businesses.

Rebuild: Doubling Down on Successful Startup Programs

The U.S. Department of Energy (DOE) and other federal agencies have a wide range of programs with a proven track record of supporting talented energy technology entrepreneurs who create high-quality jobs.19 As the economy starts to reopen, Congress must ensure that these programs have the necessary authorizations and appropriations to rebuild an even larger and more dynamic clean technology startup ecosystem across the United States.

- Expand Manufacturing USA program to bolster U.S. manufacturing. Manufacturing USA funds federal, industry, and academic collaborations to strengthen and advance the U.S. manufacturing sector. Amid project delays and cancellations paired with job losses and furloughs, Congress should leverage this program to get this sector back on its feet. This includes extending the authorization for Manufacturing USA to at least 5 years; increasing funding to $250 million annually; and allocating 20-30% of funding to create and sustain workforce programs such as educational curriculum development, training, and apprenticeships. The ManufacturingUSA institutes should also be directed to develop greater capabilities in demonstration, scaling, and commercialization activities. Lastly, cost-share requirements should be temporarily waived. Both Senator Chris Coons and Representative Haley Stevens have introduced bills supporting this program (S.1427 and H.R.2397).

- Expand clean energy entrepreneurship training and resources: Congress should ensure that every DOE technology office has a portfolio of programs that accelerate the commercial success of clean energy startups. We recommend the revitalization or expansion of the following programs.

- The Sunshot Incubator initiative jump-started 100 companies that went on to raise 22x more funding from private-sector investors than they did from DOE. Critically, this program included a focus on reducing the “soft costs” of solar energy—regulation, installation, marketing, etc.—and not only hardware improvements. This Incubator model should be renewed at $100 million annually, enough to expand it to all of DOE’s program offices addressing the full suite of clean energy technologies, and focused on supporting the most promising companies to move from prototype to demonstration.

- American-Made Challenges is a prize-based platform that can rapidly move clean energy entrepreneurs from an initial idea to a commercial demonstration. The DOE should be authorized to make at least $50 million available through this platform, across all clean energy technologies.

- Lab-Embedded Entrepreneurship Programs, such as Berkeley Lab’s Cyclotron Road, allow first-time entrepreneurs with deep scientific expertise to access extraordinarily high-value equipment, expertise, and training over the course of two years in residence at the DOE Labs. Steady funding of $50 million per year would sustain a new national cohort of fellows, at an expanded number of federal laboratories and universities, administered through well-designed public/private partnerships.

- Energy I-Corps is an entrepreneurial boot camp for career researchers at the DOE National Laboratories. Program funding should increase to $30 million annually (comparable to the National Science Foundation’s I-Corps program) and expand to include DOE-funded teams at universities and small businesses.

- Small Business Vouchers incentivize both small startups and large national labs to collaborate on commercially promising research. Through this program, clean energy startups derive incomparable benefit from the Labs’ technical expertise. Program funding should increase to at least $30 million, and should be extended across all DOE National Laboratories, potentially including other federally-funded facilities as well.

- The National Incubator Initiative for Clean Energy (NIICE) effectively fostered coordination and information-sharing among clean energy incubators across the nation, currently through the Incubatenergy Network. Under this initiative, clean energy startups have leveraged over $1 billion in private investment, generated $330 million in revenue, and created about 3,000 clean energy jobs. NIICE funding should increase to expand the Incubatenergy Network and create new opportunities to help revive struggling startups.

- Incentivize investment in clean energy innovation through the Small Business Investment Company (SBIC) program. SBICs are privately managed investment funds backed by a loan guarantee from the Small Business Administration (SBA), at zero cost to U.S. taxpayers. Today there are about 300 SBIC funds investing some $30 billion in small businesses, which tend to be relatively mature companies with low technology risk. The Senate Small Business Committee, as part of the bipartisan SBA Reauthorization and Improvement Act, has proposed to restructure the program and catalyze a new generation of “Innovation SBICs” that would promote U.S. advanced manufacturing and the financing of innovative technology companies, including clean energy startups.20

- Optimize the DOE SBIR Program to give a wider array of startups access to its resources: Through the SBIR program, the DOE already awards over $300 million to about 400 startups annually, which would rise automatically with increased DOE R&D budgets. While successful by many measures, the program currently relies on program managers scattered throughout the DOE, for whom SBIR is often their lowest priority. DOE’s SBIR program is larger than many of the Department’s applied technology program offices. It should be managed under one roof to operate with similar urgency and independence, especially given the increased needs of small businesses during an economic recovery. It should also follow the successful model used by the National Science Foundation, which prioritizes support for a greater number of small businesses instead of grants to previous awardees.21

Reinvest: Strengthening America’s Leadership on Clean Energy Innovation

As Congress crafts new stimulus measures to respond to COVID-19, it must ensure that policies not only stimulate the economy in the near term, but also lay a firm foundation for long-term US leadership in clean energy innovation. The following programs should be considered in future stimulus measures.

- Fund a new generation of energy scientists and engineers through RE-ENERGYSE. The Regaining our Energy Science and Engineering Edge RE-ENERGYSE) plan, once proposed but never authorized, would educate thousands of clean energy scientists and engineers through programs at universities, community and technical colleges, and K-12 schools, including targeted support for Minority-Serving Institutions. To meet the needs of the current economic crisis, the program should be established and the initial proposal of $74 million should be increased to at least $100 million, divided between the Department of Energy and National Science Foundation.

- Create a DOE-allied independent Energy Technology Commercialization Foundation. A non-profit Energy Technology Commercialization Foundation, authorized by Congress to work closely with the DOE, would ease energy innovators’ access to DOE’s tremendous technical expertise and world-class facilities, helping them advance their technologies more quickly to a commercial product. The foundation would raise most of its funds from private-sector and philanthropic donors that see value in accelerating the commercialization of such solutions. Congress should authorize the IMPACT for Energy Act with a one-time appropriation of $100 million, which will leverage substantially larger contributions from non-governmental donors.22

- Provide entrepreneurs with access to capital in every state. Struggling startups need access to equity capital to survive and flourish. The State Small Business Credit Initiative (SSBCI), first authorized in 2010 with $1.5 billion in federal funds, established capital access programs in every state, including measures to assist both Main Street small businesses and venture-backed startups. The Small Business Access to Capital Act would permanently reestablish SSBCI at the Treasury Department on a larger scale, ensure long-term small business recovery in every part of the country, and encourage further experimentation in financing models for clean energy startups and other innovative companies.23 Similarly, Senator Amy Klobuchar and Rep. Dean Phillips’ New Business Preservation Act would focus on the venture capital model, allocating $2 billion in federal funds to states to finance public-private equity funds and expand opportunities to more regions of the United States and a wider range of entrepreneurs.

Act Now to Save Clean Energy Startups

Clean energy startups are essential for creating the technologies we need to fight climate change, create high-quality jobs, and generate entirely new industries in the decades ahead. Even before the COVID-19 pandemic created an economic crisis, clean energy entrepreneurs tackling the toughest technology challenges found the greatest difficulty attracting early-stage venture capital. There is no substitute for the federal government’s role to ensure that clean energy startups make it through the current economic crisis and have firmer footing to succeed in the long run. As Congress considers additional emergency relief and stimulus policies, there are a range of promising options, not only to rescue clean energy startups imperiled by the pandemic, but also to rebuild successful government programs and reinvest in a strong national clean energy entrepreneurship ecosystem.