Memo Published January 10, 2023 · 7 minute read

Long Duration Energy Storage: Policies to Help America Lead

Isabelle Chan & Nicholas Montoni, Ph.D.

Takeaways

- Electrochemical Long Duration Energy Storage (LDES) provides America with the opportunity to reestablish itself as a manufacturing powerhouse—revitalizing industry and jobs in the pursuit of net-zero emissions.

- Between 2020-2050, US-based LDES equipment manufacturing could create over 10,600 jobs per year, billions of dollars in exports, and substantially progress global emissions reductions.

- To fully capture this competitive advantage, the US will need to support the effective implementation of existing clean energy policies while simultaneously bolstering innovative funding for R&D, demos, and incentives for US companies to choose to stay and manufacture in America.

Why the US Should Compete in the LDES Market

The U.S. could tap into a global market for electrochemical long-duration energy storage (LDES) valued at over $3 trillion between now and 2050. That market size could be significantly larger if nations around the world follow through on commitments to reach net-zero emissions, which will almost certainly require more storage to complement a surge in renewable generation, like wind and solar. That’s according to a groundbreaking report that Third Way and Breakthrough Energy commissioned from Boston Consulting Group (BCG), which looked at America’s competitive advantage in LDES and other clean technologies.

As we explain in this memo, the US can compete for a larger share of the LDES market by investing in innovation, supporting American manufacturing, and driving rapid deployment domestically as a launchpad into export markets. By becoming a world leader in innovative storage technologies, the US will create hundreds of thousands of jobs and enable abatement of over 8 billion tons of carbon dioxide and carbon dioxide equivalent in 2050. With that level of reward, it’s worth taking strategic policy steps to compete in LDES—particularly when it comes to America’s original equipment manufacturers (OEMs), a segment of the LDES value chain where BCG identified an especially high potential for advantage.

Policy Recommendations for Key Value Chain Segments

Technology-wide

Technology-wide policy recommendations are designed to impact US competitiveness in LDES across multiple value chain segments. Each has been chosen to promote the deployment of more LDES domestically, thereby encouraging further innovation and competition in the manufacturing of LDES technologies. These recommendations not only unlock technological advancements, expertise, a robust American workforce, and LDES deployment domestically, but also result in products and services that can be exported to mature and emerging markets as countries work to deploy more storage and modernize their grids.

Adopt a Framework for Ownership and Research of Storage Assets: LDES provides value both as a source of energy and reliability in times of crisis or high demand. In some markets, LDES is considered a generation asset, meaning it can’t be owned by system operators and owners must often pay for the bi-directional flow of electricity from storage assets. A standard storage as transmission (SAT) framework for deploying LDES should be created and US Regional Transmission Organizations and Independent System Operators should be required to use this framework to update SAT transmission planning, recognizing the value LDES provides to critical grid services. To understand these grid services, the US should also increase funding for RD&D into software development for transmission modeling, smart grid applications, and demand response. These research efforts should include requirements for researchers to engage in public-private knowledge sharing to increase the diffusion of innovative grid modeling software. As a final tool to promote accurate valuations of LDES, the US Department of Energy (DOE) should clarify the eligibility of innovative software for its loan programs.

Additionally, the federal government should establish a technical assistance program to help create implementation plans and support state-level standards and Integrated Resource Plan (IRP) modeling updates. While electrochemical LDES is still a developing technology, encouraging action by 2030 will allow for additional research into regional needs for storage while ensuring the US is prepared to take advantage of the peak in LDES deployment BCG expects to take place in the 2040s.

Implement a Nationwide Clean Energy Standard (CES): LDES becomes the most valuable at 60% renewable energy penetration and higher. Fortunately, modeling from the Decarb America Research Initiative shows that renewable energy penetration is likely to reach or exceed 60% under certain decarbonization pathways and with particular innovations. These conditions make LDES far more profitable, attractive, and useful on the grid, incentivizing further deployment. While it would be politically challenging to enact, an ambitious federal clean energy standard (e.g., 100% carbon-free energy by 2050) would likely boost demand for LDES and help unlock America’s leadership potential in this technology.

California’s Energy Storage

In 2022, the California Public Utilities Commission approved a new IRP for the state. The IRP established a target of 15 GW of energy storage, including the use of LDES technologies for the first time.

OEM (Original Equipment Manufacturers)

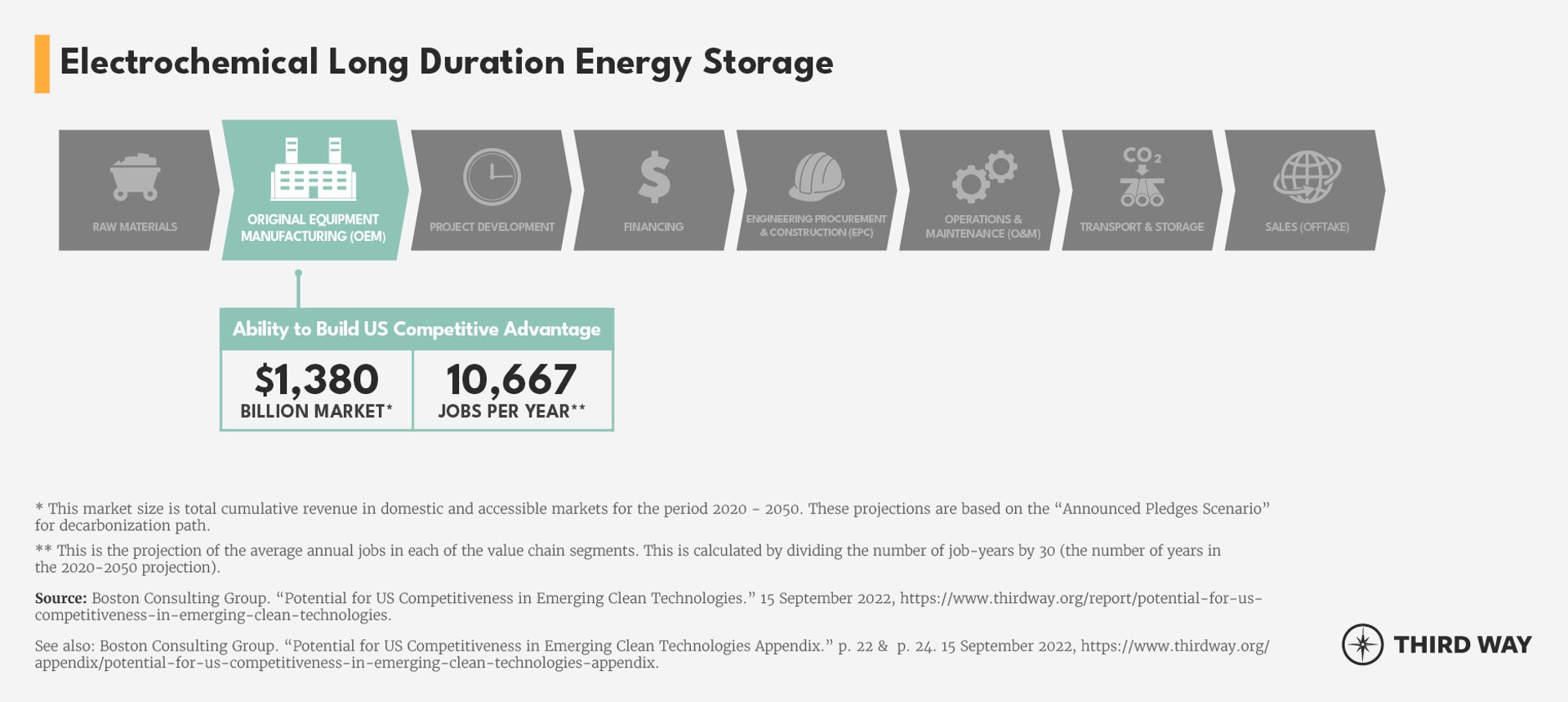

As highlighted in BCG's study, the US Serviceable Addressable Market for electrochemical LDES OEM between 2020-2050 is estimated to be over $1.3 trillion. The US has an advantage in both LDES demand- and supply-side policies, relative domestic market maturity, regulatory environment, and existing infrastructure. However, the US lags in intellectual property (IP), innovation, research, and technical leadership. If the US doubles down on innovation and establishes robust manufacturing hubs for LDES components and infrastructure, it can also lead in exports to the key potential markets in the EU, India, Japan, and Australia.

Company Spotlight

At the 11th International Conference on Advanced Lithium Batteries for Automobile Applications in 2018, China’s Regional Economic Development Agency pitched the economic benefits of doing business in China to the invited speakers and owners of US battery startups. While some US based battery startups remain committed to U.S. manufacturing, other companies accepted these compelling offers in China. Notably, many companies with U.S.-funded R&D ultimately set up manufacturing in China, underscoring the need to implement policies that invest in and incentivize domestic battery manufacturing.

Strengthening Direct Funding and Tax Incentives for American Manufacturing: As energy storage technologies mature, they run into the same barriers as any other innovation, especially in their ability to scale up production and achieve early market adoption. To grow this industry, the DOE should establish a grant program for small-scale pilots to demonstrate storage manufacturing capabilities. It should also clarify that innovative manufacturing techniques and facilities for batteries and components are eligible for DOE loan guarantees. Additionally, continued support for the 48C clean energy investment tax credit for manufacturing facilities will help stimulate domestic production of storage components. Building these technologies to be demonstrated and deployed domestically helps grow our scientific and manufacturing expertise and retain intellectual property rights.

Bolster the LDES Innovation enterprise: National Laboratories are the crown jewels of the US scientific enterprise, and this is no truer than in their wide-ranging work on energy storage. Despite our impressive scientific expertise, the US lags behind China, South Korea, and Japan in IP and research funding. Further investment in DOE-led R&D programs and the National Labs will help improve domestic ownership of intellectual property by accelerating the LDES research agenda. The DOE, along with other key federal science agencies, should continue to fund and manage R&D programs for innovative electrochemical storage technologies, with a focus on supporting high-risk innovations by providing larger grants over longer periods of time.

Furthermore, this research agenda should incorporate tangible metrics of success and progress. These could include, but are not limited to, technological, workforce, intellectual property, risk management, and impact benchmarks. Each eligible entity should be given funding up front to conduct this research program so they are able to adequately staff and prepare their research infrastructure, and industry stakeholders should compete to partner on these research efforts.

A final piece of the R&D puzzle is effective knowledge sharing. DOE and National Lab staff and researchers should be required to speak openly about their findings to help utilities, power companies, developers, and consumers understand the benefits of LDES technologies.

Lastly, as LDES technology advances, demonstrations will need to occur across the country to test LDES in multiple regions. The IIJA set the stage by funding two demo efforts within the Office of Clean Energy Demonstrations. However, we recommend allocating additional DOE funding since LDES demos will continue to require federal support to prove this technology is ready for deployment.