Blog Published February 23, 2022 · 10 minute read

Oil Prices Are Surging Again. What Does it Mean?

Key Takeaways

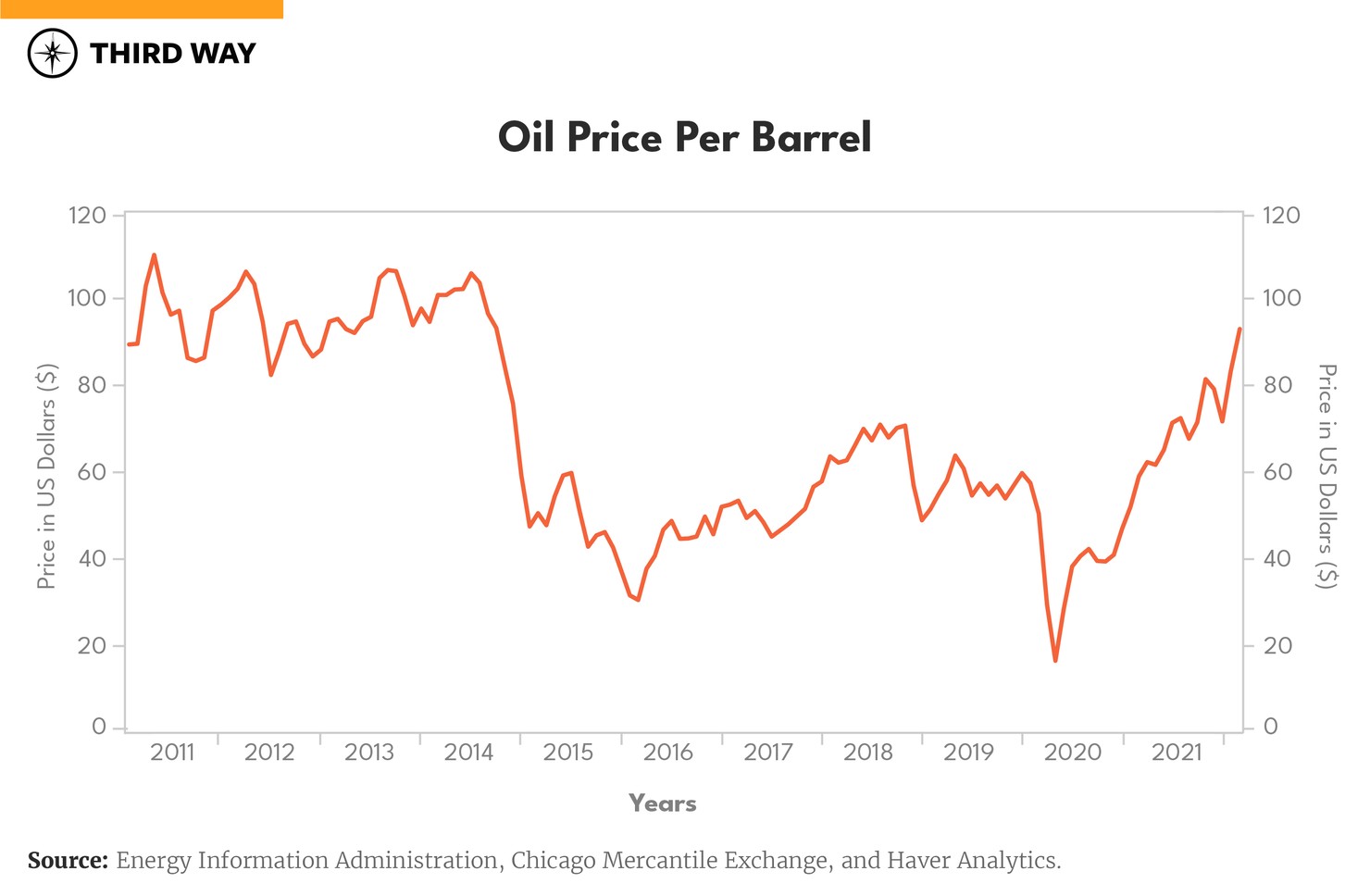

Geopolitics often drive oil price shocks and this time around, Russian military advances against Ukraine are pushing the world into a new round of oil price increases. Earlier this month, oil prices hit a 7 ½ year high and further risk and volatility are likely to persist in energy markets for some time.

It has been a while since prices have sniffed at $100 per barrel, and this time around, circumstances are more dire. Russia produces upwards of 11 million barrels a day of oil, or roughly 11% of global oil use. Given current constraints on maximum production capability in major exporting countries such as Saudi Arabia, the United Arab Emirates and Kuwait—not to mention, limits to rapid growth in output here in the United States—any disruption in oil supplies from Russia resulting from the crisis would have a large ripple effect. Unlike 1990, when a large glut of oil shielded consumers from the loss of supply when Iraq invaded Kuwait, there is not currently sufficient spare production capacity globally to immediately offset a large disruption in Russian exports.

Geopolitical events between 2011-2013 similarly drove oil prices into the $100 per barrel range several times amid the Arab Spring protests, Iranian threats to close the Strait of Hormuz, and the Libyan civil war that cut off the country’s oil exports. By 2014, rising US shale production, the end of oil sanctions against Iran amidst the signing of the Iran nuclear deal, and a Saudi-inspired price war sent prices tumbling in a boom-to-bust cycle so typical of oil’s history since the OPEC cartel was formed.

That price cycle has gone full circle since the COVID-19 pandemic began. Initial lockdowns in 2020 collapsed oil demand virtually overnight, leaving oil producers scrambling to throttle back output. Oil storage facilities were overfilled as energy demand collapsed. The ensuing economic crisis prompted governments to implement economic stimulus, which combined with the production and distribution of vaccines, brought about a quick turnaround in GDP growth and oil use by the second half of 2021. The sudden return of demand—almost as quickly as it had disappeared—has once again left producers deadlocked in trying to restore production to cover rising demand. That, combined with geopolitical tensions, has kept and could continue to keep oil markets on edge. Even the whispers of an Iranian nuclear deal in the last few days have done little to moderate oil prices.

Here are five common questions about $100 oil prices and answers to how they will affect American consumers, businesses, and the economy.

1. What does it mean for the US economy?

High oil prices have distributional impacts on the economy—hurting low- and moderate-income households disproportionately. At the same time, it benefits oil-dependent states – Texas, North Dakota, New Mexico, Alaska, Wyoming, Colorado, and parts of Pennsylvania and Ohio whose economies post job and revenue gains from increased drilling and rising production from oil and gas rigs. US oil and natural gas exports are now substantial, ameliorating the kinds of the balance of trade issues that once plagued the United States.

For American Households

High oil prices increase the pain at the gas pump for a large swath of consumers who are dependent on cars for work. It can hit workers with low and moderate incomes. Recent research at the Kansas City Federal Reserve Bank indicates that this link is evolving and may be weaker than in the past. In 2019, their research shows that low- and middle-income households spend about 3-4% of their incomes on gasoline. However, the pandemic has changed some of these dynamics. To the extent workers have the flexibility to work from home, they have been able to cushion the impact of higher gasoline prices. In contrast, low-wage workers who are not able to work from home are adversely impacted if they are dependent on cars for commuting.

For American Businesses

While direct oil sector employment and investment represent a relatively small share of the overall US economy at under 1% of total nonfarm payroll employment, investment in the oil patch still drives regional economic activity. However, investment in the oil patch has fallen from nearly $40 billion in 2014 to $23 billion last year. As it recovers in 2022, workers and businesses in oil states will feel the benefits.

2. The Biden administration released over 1.3 million barrels per day of oil from the Strategic Petroleum Reserve late last year. Why is gas still expensive?

Geopolitics

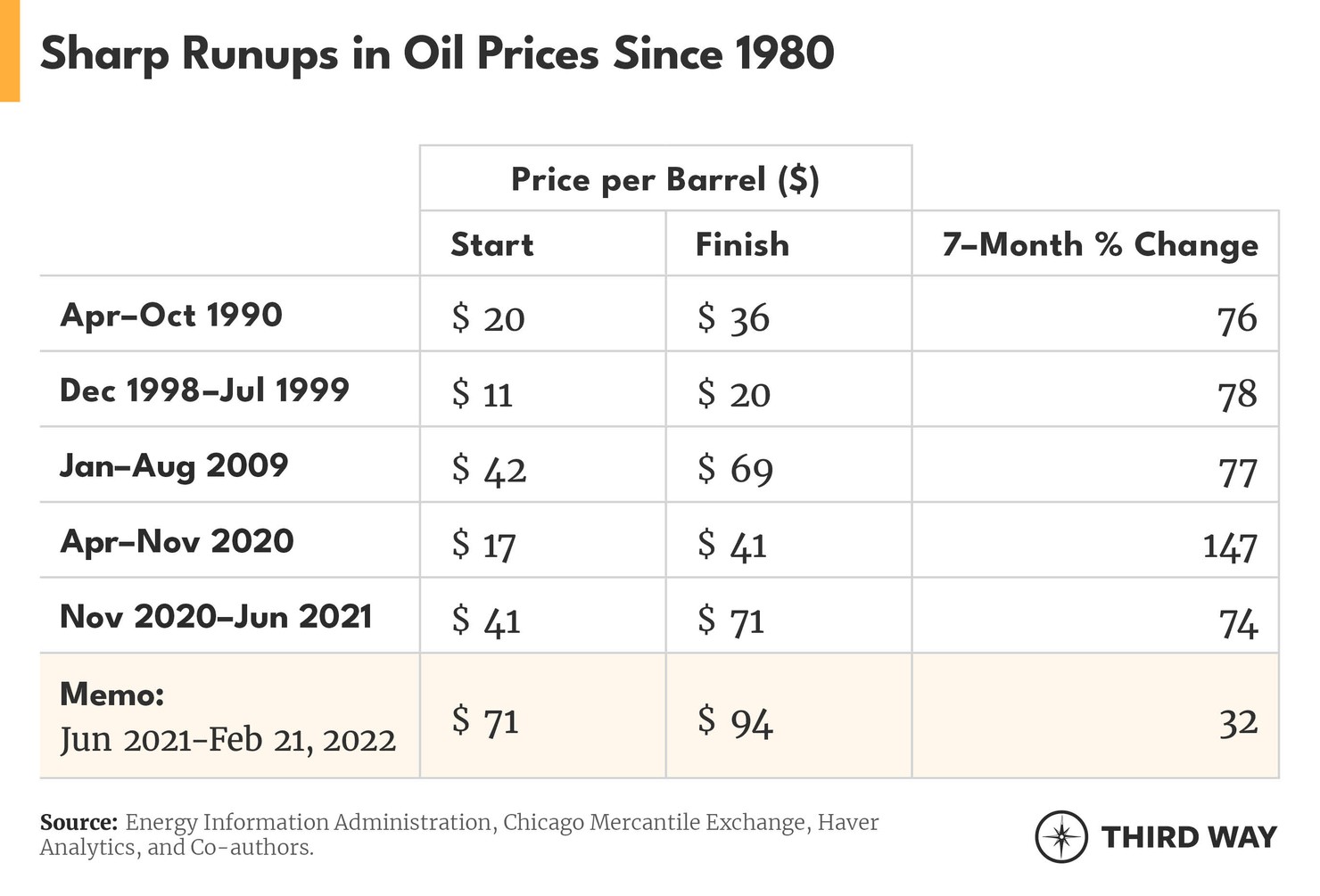

Geopolitical risks can outweigh any short-term measures available to policymakers. Last November, US, China, Japan, India, South Korea and the United Kingdom participated in a coordinated release of oil reserves. This likely tempered the rise in oil prices. Still, the headwinds from Russia’s military advances are too great to stop the rising prices of oil and natural gas. As the Russian border buildup commenced last spring, oil prices moved well above the $60 oil price that prevailed prior to the pandemic. European natural gas prices surged to levels which are now over five times higher than a year ago. As Russia has moved an additional five battalions into border regions, oil prices continued their ascent. Oil prices jumped from $40 to over $70 per barrel by June 2021. In a span of seven months, oil prices were up by 77%. For perspective, there have been only four other short 7-month runups in oil prices going back to 1980 (see table).

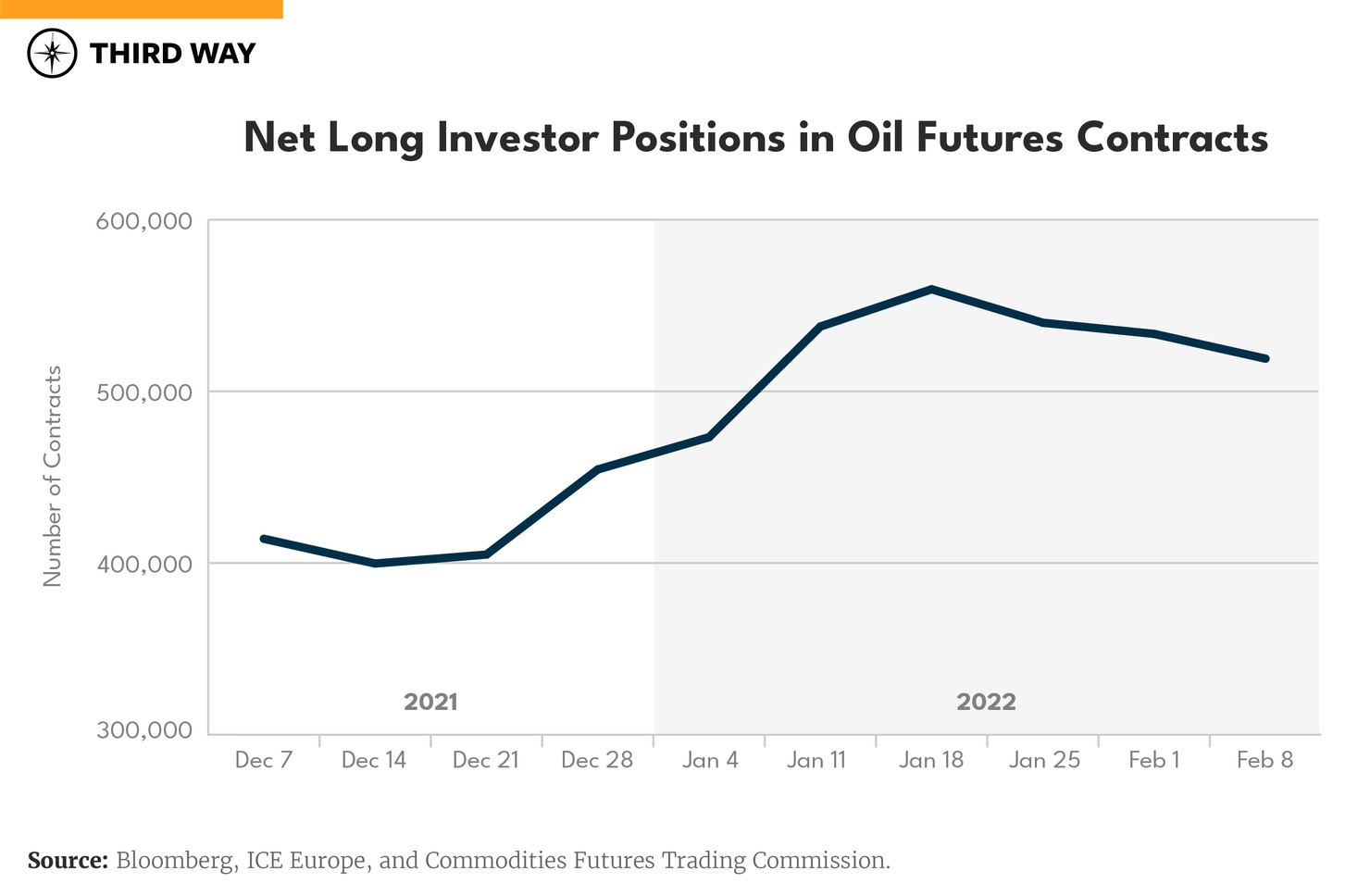

Financial Market Speculation

The chart below shows that the volume of speculative activity has increased by over 25% during the last several weeks. This means that traders were expecting oil prices to increase further, thereby paying them a handsome return for their speculation. Traders went “long” on oil, both here and abroad. This speculative activity compounded the run-up in oil prices created originally by the lag in restoring oil supply after COVID-19 related curtailments.

Global energy demand is recovering from pandemic lows…and supply is falling short.

As the global economic activity recovers from the omicron variant shutdowns, oil supply growth will have difficulty keeping pace with rising oil demand. The Organization of Petroleum Exporting Countries (OPEC) announced on February 2nd it would put more oil into markets, but many OPEC countries are maxed out of their current capacity to produce more, leaving the producer group unable to meet its own output targets. Any shortfall in Russian exports to the market will exacerbate the problem.

Global oil stocks at multi-year lows and dwindling OPEC+ spare capacity has left the market with only a small cushion. February 2022 IEA Report

3. How long could prices stay high?

Oil prices will stay high and be volatile for a while. Over time, high oil prices tend to cause consumers and businesses to adjust their spending patterns. More oil and gas rigs will come online, stimulated by high prices while consumers trim non-oil discretionary spending to compensate for the pain at the pump, leading to an economic contraction which in turn lowers the demand for oil. Consumers, businesses, and governments also adopt energy-efficient equipment and vehicles, creating a structural drop in the oil intensity of economic activity. That process eventually brings oil off its highs.

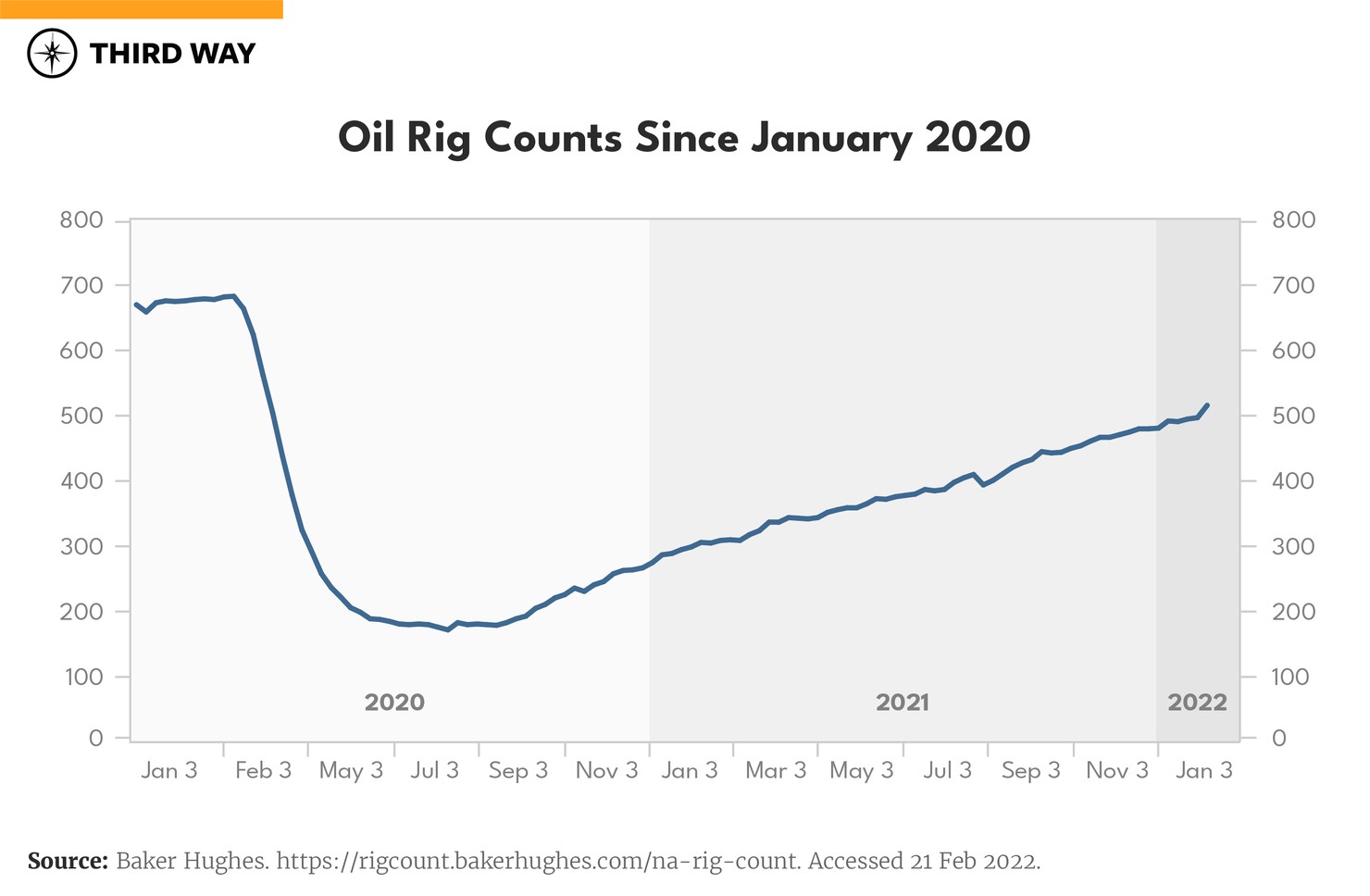

Higher prices have already ushered in recovery in US onshore rig counts, leading to rising supply. The longer oil prices remain in the $100+ range, the more the US onshore oil rig counts will expand. Domestic production growth of close to 800,000 barrels a day is already forecast for this year and will help to alleviate the supply shortfalls. If the geopolitical crisis worsens,US drilling and workovers of old wells may increase further. Oil rig counts crashed as the pandemic began in March 2020. Rigs producing oil in North Dakota and Texas, as well as a few other states, fell by 75% from March to August 2020. Even with the bullish Baker Hughes rig count report last week, the oil rig count remains about 25% below the pre-pandemic period.

4. Could the Biden Administration sell more oil from the Strategic Petroleum Reserve or suspend taxes to provide relief at the pump?

Yes and no. Last November, we wrote a blog laying out the set of options to address high oil prices. Given the disproportionate effects of higher oil prices, releasing more oil from the SPR is helpful, especially if it is done in conjunction with other allies in Europe and Asia. Likely this has kept some of the speculative activity at bay and tempered the rise in prices so far this year. The SPR has 590 million barrels of oil in storage and current sales are running at about 1.3 million barrels a day. The US consumes about 20 million barrels of oil per day.

Temporary cuts in gas taxes can provide some brief relief, but if left in place too long, will translate into higher demand that will prompt prices to rise back up. Federal gas taxes are 18.4 cents per gallon. State taxes at the pump average 30 cents per gallon.

But let’s be realistic about the savings any tax relief at the pump can actually offer. In 2020, the US consumed 124 billion gallons of gasoline, representing about 950 gallons of consumption per household. Eliminating the federal gasoline tax would only save about $3.50 per week for the average American household, assuming the gasoline prices averaged $3.50 per gallon. At the same time, loss of the gas tax would deplete funds for America’s transportation infrastructure. Federal gas tax revenue was over $30 billion in 2020 and provides 80% of the funding for the nation’s Highway Trust Fund (HTF). Maintenance and repair of bridges, highways, and roads are some of the important HTF-funded activities that could be jeopardized by a suspension of fuel taxes.

5. Is a recession inevitable from the $100 oil price spike?

That will depend on how extreme a geopolitical shock takes place. $100 oil by itself is not as disruptive as it used to be because the US economy is less oil intensive than it used to be. Since the 1970s, the US economy has become much more efficient in energy use per dollar of GDP. That means it takes less oil to produce our GDP than in the past. With the influence of the pandemic economy, the rise of fuel-saving e-commerce and telecommuting, and the evolving sources of energy—21% of US energy consumption in 2020 came from renewable sources—the impact is foggier. In the past, higher gasoline prices would cause a slowing in car sales. With a growing “work from home,” part of the economy and supply constraints, new and used vehicles are in demand. In other words, $100 oil has a much less negative impact on our economy than it used to. Still, together with other inflationary trends, it remains to be seen if consumers will pull back on spending.

Conclusion

The pace of the global economic recovery is very uncertain due to the Ukraine crisis and the pandemic. Many expect the pandemic risks receding, that a new variant will be milder and less damaging given ongoing improvements in vaccination rates and an accomplished “learning curve” on coping and minimizing outright shutdowns. But risks related to the pandemic could be replaced by new economic shocks imposed on global markets by Russia’s military actions.

Price spikes raise the possibility of forcing both consumers and businesses to cut back on their economic activity as rising oil and gasoline prices absorb badly needed income. Thankfully, Congress passed the American Rescue Plan and the Infrastructure Investment and Jobs Act, both of which provide important relief and stimulus for American households and businesses. This federal funding provides a critical cushion against the headwinds of energy price increases. Many households were able to build up savings as they benefited from tax relief and COVID-19 support. This will be helpful at least through the first half of this year. Persistent high oil prices beyond that will be a challenge and will take a toll on economic growth and on lower-income families in particular.