Newsletter Published May 1, 2026 · 10 minute read

Fission….Impossible?

Hi Friend!

Welcome back to On the Grid, Third Way’s bi-weekly newsletter, where we’ll recap how we’re working to deploy every clean energy technology as quickly and affordably as possible.

We’re excited to have you join us!

President Trump set a goal to quadruple American nuclear capacity from 100 GW to 400 GW by 2050. This goal is admirable–and quite ambitious. Over the past 25 years, the US has built only 3.3 GW of new nuclear. That means over the next 25 years, we’re going to have to build roughly 90 times that amount in the same timeframe. There’s certainly been no shortage of nuclear developers making moves to deploy, but that has created a noisy market, where it is genuinely difficult to discern which firms are approaching commercialization and which are destined for failure.

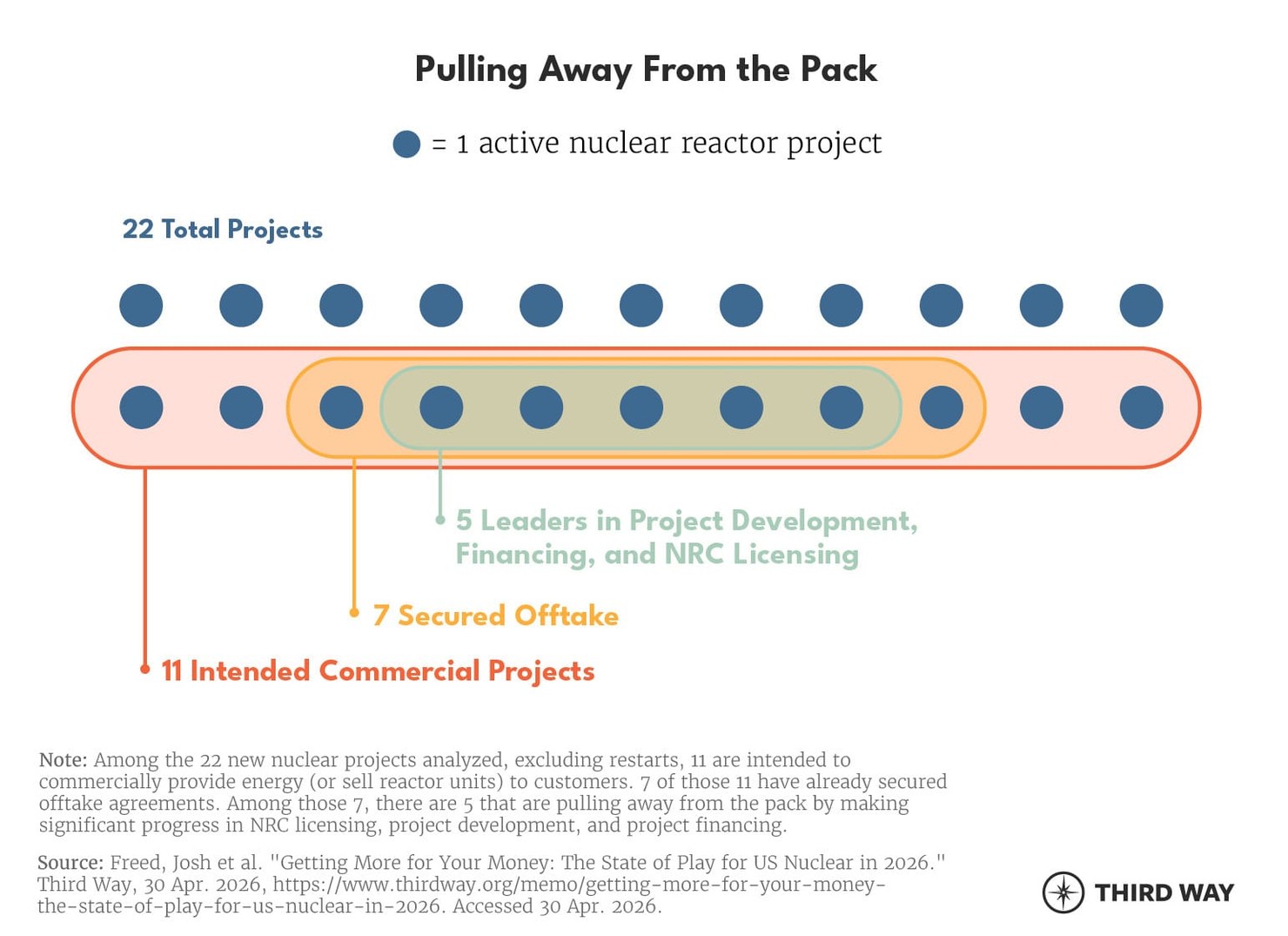

To understand where the nuclear sector actually stands, Third Way conducted a first-of-a-kind landscape assessment of every announced nuclear reactor project in the US, aggregating publicly available data on technology, site selection, financing, offtake agreements, and NRC licensing activity across 22 active projects. Some projects are making substantive commercial progress, but many are just treading water. You can read our full report here, but here’s a quick read-out.

The Good News: The nuclear industry is truly having a renaissance. Nuclear companies secured over $1 billion in private investment in the last quarter of 2025 alone. Bipartisan support has held strong, and we’re seeing public opinion increasingly favor nuclear energy. We’ve reached milestones like X-energy's partnership with Dow Chemical at Long Mott, Kairos Power's Hermes 2 with a power purchase agreement secured with Google, and Holtec's dual-unit project at Palisades. All of which have demonstrated that credible commercial pathways are in the works. Companies are securing offtake, signing engineering, procurement, and construction contracts, and engaging seriously with the NRC.

The Bad News: Of the 22 projects we surveyed, only 6 have directed public or private capital toward an explicitly commercial project rather than a test. Only 2 commercial projects have received NRC construction permits. And even if every project in our assessment deployed its maximum planned capacity, the US would still be 289 GW short of the 300 GW it needs to add to hit 400 GW by 2050. There’s a lot of work that remains to be done.

The Administration Tactics Don’t Match Its Goal: the Trump Administration has taken genuinely meaningful steps on nuclear unlocking long-overdue disbursements on fuel funding, and moving on permitting. But its approach continues to prioritize short-term announcements over longer-term, more durable progress. For example, the DOE Reactor Pilot Program, which the administration has invested significant time and energy in, focuses on achieving criticality for non-power reactors. That’s great in theory, but it does not move a reactor closer to putting electrons on the grid. Furthermore, the Energy Dominance Fund, the primary federal financing vehicle for domestic nuclear, has so far confined itself to restarts and uprates. Restarts matter–Palisades will bring 800 MW back to the grid–but there are a finite number of them, and they will not get the US to 400 GW. The fund was built to finance first-of-a-kind projects, as it did with Vogtle. It hasn't done that yet.

What Needs to Happen: Those familiar with Third Way know that we've spent over a decade working on advancing US nuclear policy. From our vantage point, the nuclear industry is at a genuine inflection point, and the difference between reaching 400 GW and falling short by hundreds of gigawatts comes down to decisions made today about where money and attention go. Right now, the US nuclear sector doesn't need a more crowded field. We're engaging directly with policymakers and investors to make the case that the public and private sectors need to concentrate resources on the projects actually closest to commercial deployment. The ones that have secured offtake, built project-specific financing structures, and engaged consistently with the NRC are the ones worth backing. We’re also continuing to track contradictions at the center of the administration's nuclear agenda and helping refocus this critical industry.

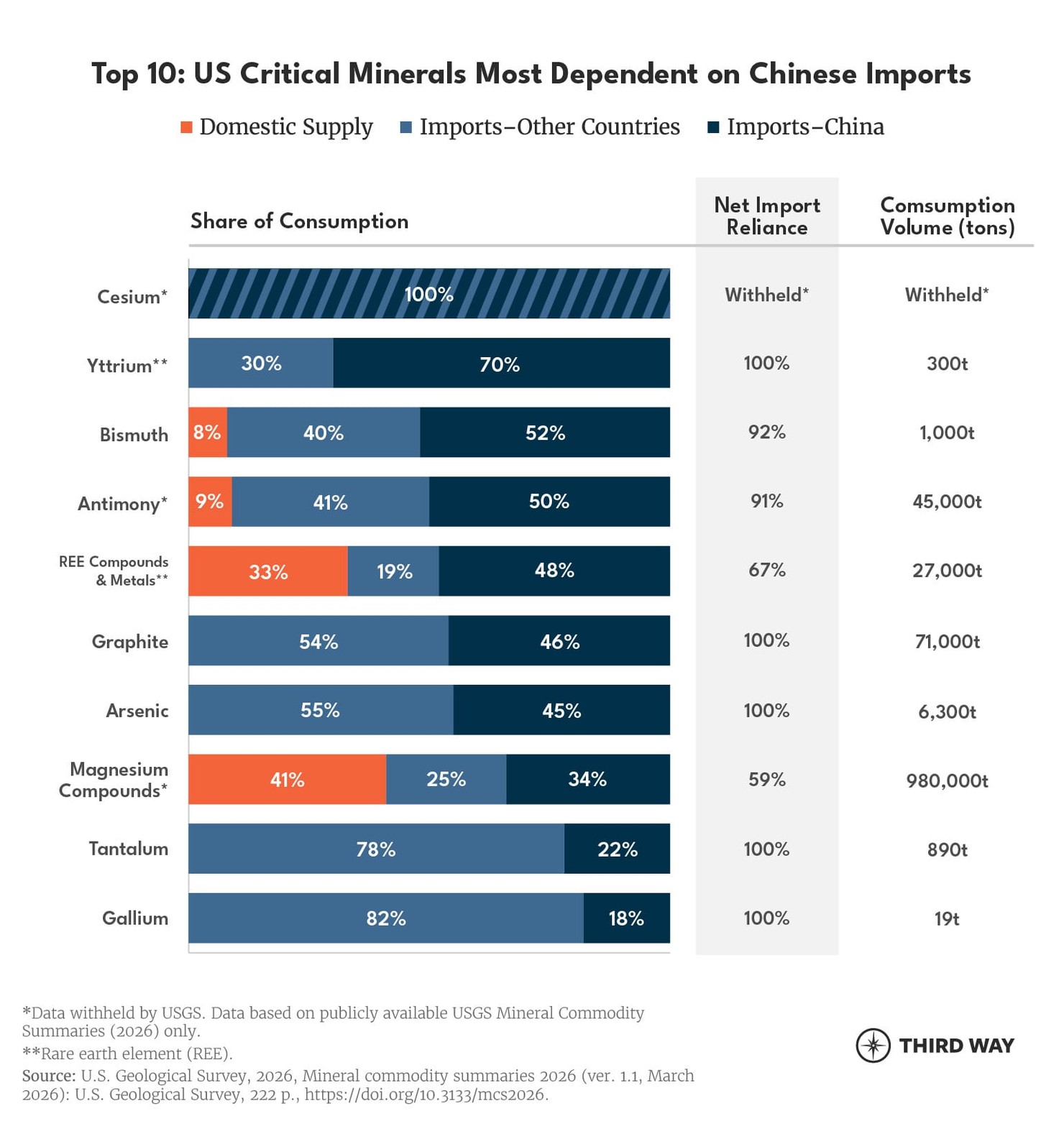

America’s clean energy buildout, defense systems, and AI infrastructure all run on 60 critical raw minerals (CRMs). But China controls vast supplies of the most strategically significant minerals and holds a near-monopoly on rare earth minerals, the subgroup of 17 minerals essential to modern electronics, weapons systems, and the energy sector. Even when the minerals are mined in the US or allied countries, they are overwhelmingly shipped to China for refining before re-entering global supply chains. A truly made-in-America clean energy surge requires taking back at least a portion of this essential supply chain.

China Controls the Middle: The US has made tangible progress on critical minerals in the last few years. MP Materials’ Mountain Pass mine in California has expanded rare earth outputs in the US, and Lithium America broke ground at Thacker Pass in Nevada. But despite this, the US still largely lacks the domestic capacity to refine, process, and chemically separate what it’s pulling out of the ground into usable inputs. That midstream gap is where US exposure is most acute, and where China’s grip is tightest.

Why That’s A Problem: China has a history of using its processing dominance as leverage. In 2010, it halted rare earth exports to Japan over a territorial dispute, cutting off the materials Japan needed for electronics manufacturing and defense systems. More recently, China imposed export controls on the US on gallium, germanium, graphite, tungsten, and antimony, which are essential to our semiconductors, energy, defense, and battery supply chains. While the US reached an agreement to pull back these restrictions, the underlying dynamic didn't change–Beijing can reach into American industry and restrict the flow of critical inputs whenever it chooses. At the most basic level, the inputs powering our grid, weapons systems, and economy should not be subject to a rival's decisions.

What Comes Next: Washington has never been more focused on critical minerals. Congress has several bills in play, the administration has issued multiple executive orders on domestic production and permitting, and even launched Project Vault to help build a strategic stockpile of critical minerals. But activity and strategy are very different things. The Trump Administration has acknowledged that processing remains a strategic vulnerability for the US while simultaneously proposing cuts to the Department of Energy and ARPA-E programs that would make US processing competitive.

The US cannot, and should not, try to replicate China’s state-directed model. What we can do, however, is compete the best way we know how: let innovation close gaps that brute-force capacity cannot. Our newest memo outlines how expanding resources for innovation in extraction, recycling, and substitution can help the US leapfrog China’s advantage in critical minerals processing. As the policy environment for critical minerals continues to develop, our team is engaging with relevant stakeholders and policymakers to ensure that the innovation agenda doesn’t get lost in the noise.

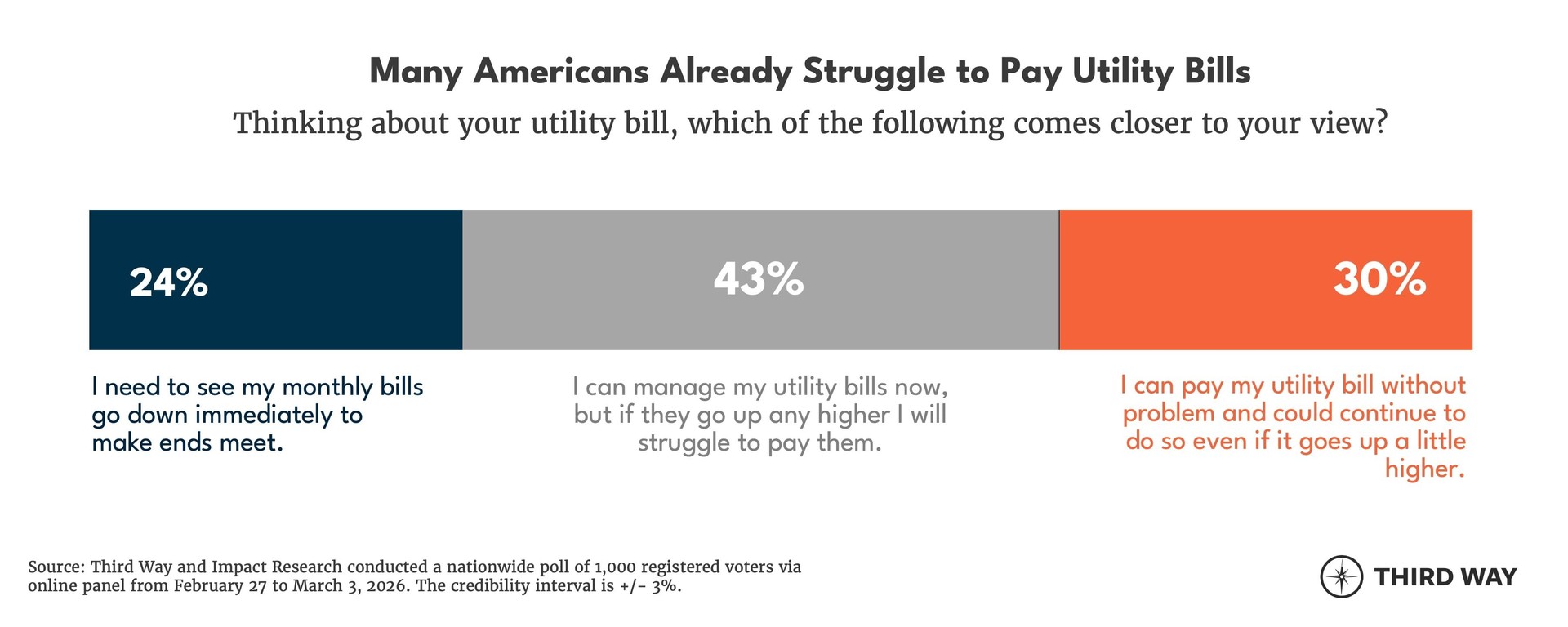

The power sector is changing rapidly, and Americans can feel it. Data centers are coming online, demand is rising, and electricity bills are going up in the process. In new polling from Third Way, 86% of registered voters said their energy costs have gone up in the last few years, and nearly a quarter of households already find current prices unmanageable. Our latest digs into how voters see the energy sector – and how they want to tackle rising energy prices.

What Are Americans Thinking? The public opinion research reveals a remarkably coherent perspective. Voters aren’t ideological about energy sources: they overwhelmingly want a mix of energy sources and don’t think either clean energy or fossil fuels are responsible for rising prices. Instead, they’re placing blame for rising prices on larger institutions beyond their control. They think utilities are price gouging, that data centers are consuming electricity without paying their share, and that the federal government isn't doing enough to stop either. In short, Americans think they’re getting screwed, and they want answers.

What Solutions Do They Want? Americans see a system that feels rigged against ordinary ratepayers and want real corporate accountability. They want the government to tackle price gouging, cap utility fees, and require tech companies to pay their fair share for the electricity they use. As we noted before, voters notably do not gravitate toward banning data centers outright. They want growth and a thriving private sector; they just want it to be fair.

What We’re Doing: Our team is focused on understanding how voters think about rising electricity costs, who they blame, and what solutions feel meaningful to them. We’re bringing these insights to policymakers and key decision-makers and helping develop effective policy solutions that put these messages into practice.

Chinese automakers account for 70% of all global electric vehicle (EV) production. In contrast, American EV production has fallen behind, with US giants like Tesla overtaken by less-expensive, well-made BYD and Geely models. Thanks to 100% tariffs on Chinese EVs and Department of Commerce restrictions on Chinese software and hardware, Chinese EVs are rare in the US so far.

But President Trump recently floated the idea of letting Chinese automakers into the US market. On paper, the idea sounds straightforward: allowing Chinese firms into US markets would let them compete directly with US automakers and deliver exactly what policymakers say they want: cheaper vehicles, more consumer choice, and faster EV adoption.

In practice, however, this is a much bigger gamble. Policymakers like Senator Elissa Slotkin (D-MI) are already pushing back hard, warning that opening the door to Chinese autos could put American auto jobs and the broader manufacturing base at risk. This week, Senator Slotkin introduced legislation to formally establish a national security review process for Chinese vehicles entering the country, potentially banning any that are deemed a threat.

Why This Matters: China is entering the EV market with over a decade of coordinated industrial policy under its belt, including tools like direct subsidies and preferential financing. That advantage shows up most clearly in costs. Chinese EV makers can build cars much more cheaply than US and European companies can. That means American automakers would either have to lower prices and take smaller profits to keep up or lose customers. And when profits shrink, so does their ability to invest in new factories, expand supply chains, and stay competitive over time.

Those kinds of pressures can start to affect where the auto industry physically lives. Capital and production tend to move to wherever it’s cheapest, with supply chains and jobs following. The US auto industry supports millions of American jobs and is one of our country’s core manufacturing sectors. If that base weakens, it’ll be hard to rebuild. And because EVs are becoming such a central part of the economy, relying more on Chinese imports would deepen our existing dependencies on Chinese batteries and critical minerals. What looks like cheaper cars today can end up reshaping the entire industry tomorrow.

What We’re Doing: The goal here is not to wall off the US auto market from competition, but rather, to ensure American automakers have the tools they need to scale, compete, and win. As our new memo lays out, that starts with maintaining a strong trade backstop. Tariffs and policies to grow domestic auto production should reflect the reality that Chinese EV firms are competing with heavy state backing, not on a level playing field. At the same time, policymakers need to close potential workarounds, like China routing production through countries like Canada or Mexico, that could allow Chinese EVs to enter the US market indirectly. Our team is tracking how this debate is evolving across trade policy, industrial strategy, and public opinion and working to connect the dots for decision-makers.

- Holly Buck, in the Jacobin, argues that data center moratoria are a strategic misstep and will likely offshore AI development and raise prices.

- Rob Meyer, in the New York Times, makes the case that the AI buildout is forcing America to confront a long-neglected grid modernization crisis.

- Shayle Kann, on the Catalyst podcast, talks with George Hershman, CEO of SOLV Energy, about how automation and AI are impacting energy project construction.