Memo Published April 27, 2026 · 10 minute read

Beyond the Valley of Death: Securing America’s Critical Minerals Future Through Innovation

Takeaways

- China’s dominance of midstream processing gives the country real power over global critical mineral supply chains. That leverage puts America’s defense, manufacturing, and energy systems at risk.

- The United States cannot simply mine its way out of this problem. Even with access to mineral resources, the US lacks competitive domestic capacity to process, refine, and separate them on a commercial scale.

- Closing this gap will require targeted investment to leapfrog China’s existing advantages in the mineral processing industry.

- Third Way has developed a realistic strategy to do so, built on three pillars: advancing extraction and processing technologies, scaling recycling and recovery systems, and accelerating substitution and materials innovation.

America’s economic future hinges on reliable access to an expanding catalog of 60 critical raw minerals (CRMs). They link every advanced system that the United States relies upon – from defense and energy to manufacturing, the tech sector, and artificial intelligence. The United States has significant geologic critical mineral resources, but has allowed this critical domestic industry to wither over the past 30 years. By contrast, China has consolidated considerable mineral reserves and captured essential elements of the CRM supply chain—processing, refining, and separation.

Today, China controls roughly 70% of global refining capacity for many of the most strategically significant critical minerals.

The country has a near-monopoly on the processing of rare earth elements (REEs), a subgroup of 17 CRMs essential to modern electronics, weapons, and defense systems, and the energy sector. Even when minerals are mined in the US or other allied countries, they are overwhelmingly refined by China for use in global markets.

This processing monopoly gives Beijing disproportionate leverage over global pricing and supply availability—leverage that China has periodically weaponized. More recently, China imposed temporary but strict export restrictions on CRMs essential for semiconductors, defense, and data centers.

The US later reached an agreement with China, but the message was clear: China can reach into the arteries of US industry and allied industry to restrict the flow at will.

This level of foreign influence over domestic industry is disturbing and damaging, doubly so because the technologies within the critical mineral supply chain were developed by the US and our allies.

US reliance on Chinese CRM supply chains is not a foregone conclusion. The US can still unwind its overreliance through coordinated policy, long-term investment, and sustained innovation, while also expanding supply, mitigating structural vulnerabilities, and building redundancy into key supply chains.

The US is Not Resource Poor—It’s Processing Poor

US policy has long concentrated on the tail ends of the CRM supply chain, growing US mining capacity, and, all the way downstream, boosting manufacturing capabilities. But those investments obscure the fact that the middle of the supply chain–including refining, processing, and separation–remains consolidated in China. The bulk of federal CRM policy has, therefore, focused on areas where the US is already performing relatively well, allowing core supply chain segments to languish.

Rare earths illustrate the processing gap. In 2025, the US mined roughly 51,000 tons of REEs and held approximately 1.9 million tons in reserves. Yet, the US produced only 8,900 tons of refined REE compounds and metals, meeting only 33% of our domestic demand.

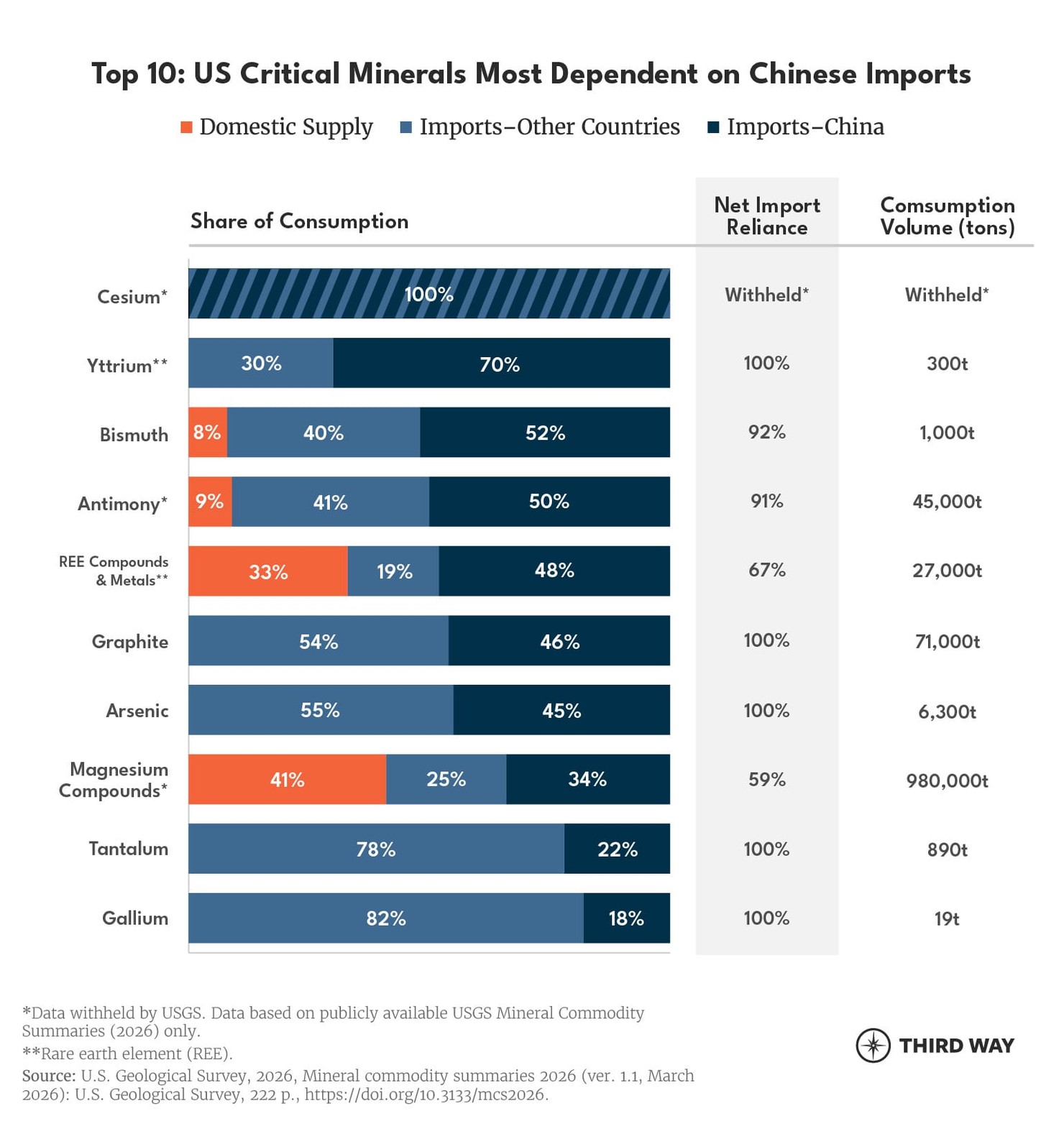

The remainder was largely sourced from China, reflecting not a mining failure but a processing failure. This, unsurprisingly, is true for many CRMs, since China has spent decades building a state-backed processing sector. The country has massive processing capacity, subsidized financing, lower production costs, and, for better and for worse, a tolerance for environmental tradeoffs that the US does not have. As a result, Chinese processors can compress margins and fend off competitors. For a full breakdown of CRM US import dependence, click here.

Building new processing capacity in the US is exceedingly difficult, both economically and politically. Processing facilities require substantial upfront capital and depend on long-term off-take agreements with manufacturers, who face additional uncertainties about how future supply chains will evolve, including geopolitical risks and trade disruptions. At the same time, building new processing facilities also means completing onerous federal permitting processes, whose timelines can delay project completion for years, with no clear end in sight. Local litigation–from surrounding communities and tribal nations who may oppose new construction–can further delay construction for years. For private investors considering expanding CRM processing in the US market, the cumulative risk profile can outweigh the expected return. Retaking some form of US leadership–or, at the very least, gaining ground against China–will require removing many of the barriers to building here at home, making it easier to actually build the infrastructure needed to process critical minerals here in the US.

We must couple that buildout with what America does best: innovation. Through our national laboratories, research institutions, advanced manufacturing ecosystems, and capital markets, this country must develop new tools and strategies to support mineral extraction, separation chemistry, material recovery, and industrial processing. Building extant technologies and processing facilities is critical, but it’s inadequate in the face of China’s decades-long headstart. The one-two punch of alleviating permitting restrictions and leveraging our country’s vast innovation ecosystem could put the US back on track for some semblance of competitiveness in CRM extraction and processing.

Leapfrogging China: A Three-Pillar Innovation Pathway

The sections below lay out a three-pillar agenda to grow US innovation in critical minerals. It calls for expanded and new programs to rebuild resilience across CRM extraction, processing, recycling, and substitution pathways. For a full downloadable table of our three-pillar innovation pathways, click here.

PILLAR I: Extraction & Processing Innovation

Policy Recommendation: Expand R&D support for critical mineral innovation programs, including the DOE’s RECOVER program and National Laboratory pilot-scale processing infrastructure, alongside university consortia and federally backed demonstration facilities. Establish a Critical Minerals First-of-a-Kind (FOAK) Validation Program to bridge the gap between laboratory breakthroughs and commercial deployment.

Domestic midstream competitiveness hinges on next-generation extraction and processing technologies that can materially improve yields and recovery rates while lowering costs and reducing environmental impacts.

The problem is that most of these innovations remain trapped between laboratory success and commercial viability–technically proven but unable to attract private capital without federal risk-sharing.

This includes advanced extraction techniques, enhanced byproduct and co-product recovery, and the exploration of unconventional feedstocks that expand the effective resource base. Programs like DOE’s RECOVER initiative already demonstrate how advanced technologies can unlock critical minerals from waste streams and non-traditional sources. Still, these efforts can be expanded to help accelerate broader commercial deployment.

Expanding US National Laboratory pilot-scale infrastructure–across facilities with existing critical minerals research programs–can serve as shared pilot environments for separation chemistry, continuous processing, and FOAK validation. Companies could validate technologies before raising large amounts of private capital, speeding up the innovation-to-commercialization pipeline.

To close the gap between research breakthroughs and commercial deployment, policymakers can establish a Critical Minerals FOAK Validation Program. Modeled on recent DOE funding opportunity announcements but specifically focused on mineral processing technologies, such a program would provide milestone-based support to validate cost, yield, and environmental performance before technologies scale to full industrial deployment.

PILLAR II: Recycling & Recovery Innovation

Policy Recommendation: Scale NETL recycling R&D programs and expand DOE’s RECOVER initiative to support urban mining and supply chain integration demonstrations that convert domestic waste streams into strategic mineral feedstocks. Establish federal recovered-material qualification standards to ensure that recycled inputs meet industrial specifications and can be integrated smoothly into downstream manufacturing for batteries, magnets, and semiconductors.

Even as mining scales, long-term demand growth is expected to outpace new mine production. Recycled feedstocks can help alleviate supply pressure and introduce greater resiliency to domestic supply chains. Technological innovation and recycling can reduce our import demand by 20-40% and alleviate supply chain pressures. The total value of domestically recycled critical mineral commodities reached $18 billion in 2025—economic weight that remains underleveraged.

Dedicated R&D, anchored in programs like NETL’s Critical Minerals Recycling and Recovery Initiatives, can improve recovery rates, purity, and process integration for lithium, nickel, cobalt, graphite, and REEs.

One promising pathway lies in urban mining—recovering critical minerals from discarded electronics and other goods. The RECOVER program, originally designed to pull minerals from industrial wastewater and water streams, is ready-made for expansion. Applied to e-waste and industrial scrap at scale, RECOVER-type programs could help recover lithium, cobalt, copper, and REEs from material that is currently wasted or exported to informal recyclers overseas.

This turns a waste problem into a supply chain asset.

Recycling, however, is not costless or automatic. Like Europe, the US will face high recycling costs, regulatory complexity, and technological barriers associated with separating increasingly complex products. Innovation is critical to meet industrial specifications required by battery, electronics, and advanced manufacturing industries.

PILLAR III: Substitution & Materials Innovation

Policy Recommendation: Refocus the DOE Critical Materials Innovation Hub on substitution priorities and establish Strategic Substitution Testbeds to accelerate the validation of alternative materials for real-world defense, energy storage, and semiconductor applications.

For some segments of the CRM supply chain, expanding domestic supply is not enough. Where processing remains highly concentrated among foreign entities of concern (FEOC), no realistic volume of new US mining resolves the vulnerability. In these cases, a more durable strategy may be to reshape demand itself.

Materials substitution—through alternative chemistries, novel alloys, and reduced-intensity designs—can reduce reliance on the most geopolitically constrained minerals.

Programs such as the DOE Critical Materials Innovation Hub have begun exploring substitution possibilities, but promising lab results are not the same as a national strategy. The US needs to expand its investment in substitution R&D and create clearer pathways to reach the energy, defense, and semiconductor manufacturers.

Japan offers a relevant precedent. After China weaponized rare-earth exports against Tokyo in 2010, Japan funded a Rare Metal Security Strategy and materials innovation programs to expand recycling and diversify supply. Japan invested in recycling, funded R&D into substitute materials, secured overseas supply, and built strategic stockpiles to reduce reliance on concentrated supply chains, specifically with China.

At home, creating Strategic Substitution Testbeds, for companies like Niron Magnetics, that are reducing Chinese-controlled REE dependence through innovative substitution processes, we can close the last mile between lab success and deployment. By providing applied validation environments where substitute materials are tested against the operational requirements of real defense systems, advanced manufacturing technologies, and energy infrastructure, before large-scale adoption.

Ambition Without Coherence

Washington has never been more focused on critical minerals, but progress has been uneven. Prior efforts, particularly under the Biden Administration, focused on expanding upstream supply incentives, but never seriously addressed the midstream processing gap where US exposure is most acute.

The current Trump Administration deserves some credit for recognizing that mineral processing is a major vulnerability for the US. But the administration’s strategy still has blind spots. They have emphasized domestic production and stockpiling through Project VAULT, but have not prioritized scaling recycling and recovery technologies that could supplement primary supply. This is especially risky as steep tariffs on imports are simultaneously reducing the flow of recyclable materials entering the US.

These efforts sit alongside proposals to cut research programs that make US processing competitive–including a 57% cut to ARPA-E and a 14% cut to the Department of Energy’s Office of Science. Weakening America’s innovation pipeline threatens to slow the development of the capabilities we are trying to strengthen.

The result is a policy posture that is serious about critical minerals in name, but incoherent in practice. Without a sustained, coordinated commitment to innovation–across processing, recycling, and substitution–these efforts will struggle to reach the scale the problem demands.

The US should not copy China. Replicating a state-backed industrial model built on subsidized overproduction, suppressed prices, and weakened environmental standards is neither possible nor reasonable. But we can compete, challenge extant ways of doing business, and reinvent the CRM supply chain. That is where America’s advantage lies, and it’s where we should invest.