Memo Published April 30, 2026 · 18 minute read

Getting More for Your Money: The State of Play for US Nuclear in 2026

Takeaways

- The Trump administration has set the right, ambitious goal for US nuclear; the United States should get to 400 GW by 2050.

- But the Administration’s tactics prioritize short-term headlines over durable success.

- Despite a noisy market, Third Way’s US nuclear sector landscape assessment found that a select set of reactor projects have emerged as the closest to commercial deployment.

- The American nuclear sector would be best served by a clear separation of the most commercially-ready technologies from those that will take much longer to get to commercialization. And investor dollars must follow suit. Resources must coalesce around the projects nearest to commercial viability.

- To rapidly accelerate commercialization at scale, the government must focus its leadership on identifying and supporting the technologies that can get to market in the timeline necessary to meet its 400 GW goal.

Following Through on 400 Gigawatts

In May 2025, President Trump set a goal to quadruple American nuclear capacity by 2050, going from 100 GW total to 400 GW in 25 years. That’s no small feat—in the past 25 years, the United States has only built about 3.3 GW of new nuclear.

Third Way firmly supports this aspiration. It is a pivotal time for the US nuclear sector, with many projects on the cusp of reaching significant milestones towards scaled commercial deployment. But it’s difficult to tell how much progress the US has actually made in growing domestic nuclear, given the sheer volume of noise coming out of the nuclear space.

The United States is on the brink of a historic achievement. This moment calls for a brutally clear assessment of which projects are primed for commercialization and which remain underbaked.

To get that clarity, Third Way has conducted a first-of-a-kind landscape assessment of announced nuclear reactor projects in the US. This project aggregates the latest publicly accessible information—including open-source press releases, reporting, and other announcements—to offer a snapshot of active projects that have announced a specific reactor technology, site, and discrete deployment opportunity.

The bottom line is that the United States—both the public and private sectors—can no longer afford to hand out participation trophies to every nuclear developer. To meet our nuclear goals, we need strong, future-oriented policymaking, effective investment, and a narrowing of the field of competing firms.

This assessment is intended as a call to action to help accelerate this process so American nuclear technologies are deployed at the pace we need to reach 400 GW by 2050.

For more details on each project, and additional restarts and projects revisiting prior, partially-completed construction, please see the full spreadsheet available for download here. See the methodology section at the end of this report for more on what defines an active project and its progress towards commercial deployment.

How to Read This Data

Getting to 400 GW means we need to build (a lot of) commercial nuclear plants quickly, and thoroughly evaluate which projects are on the path to commercial deployment.

Third Way’s assessment highlights metrics that most directly indicate how close a project is to commercialization. It begins with the fundamental criterion of whether a project has secured a commercial customer or offtaker, followed by whether they’ve secured project-specific financing, taken tangible steps towards project delivery, and formally progressed in commercial licensing:

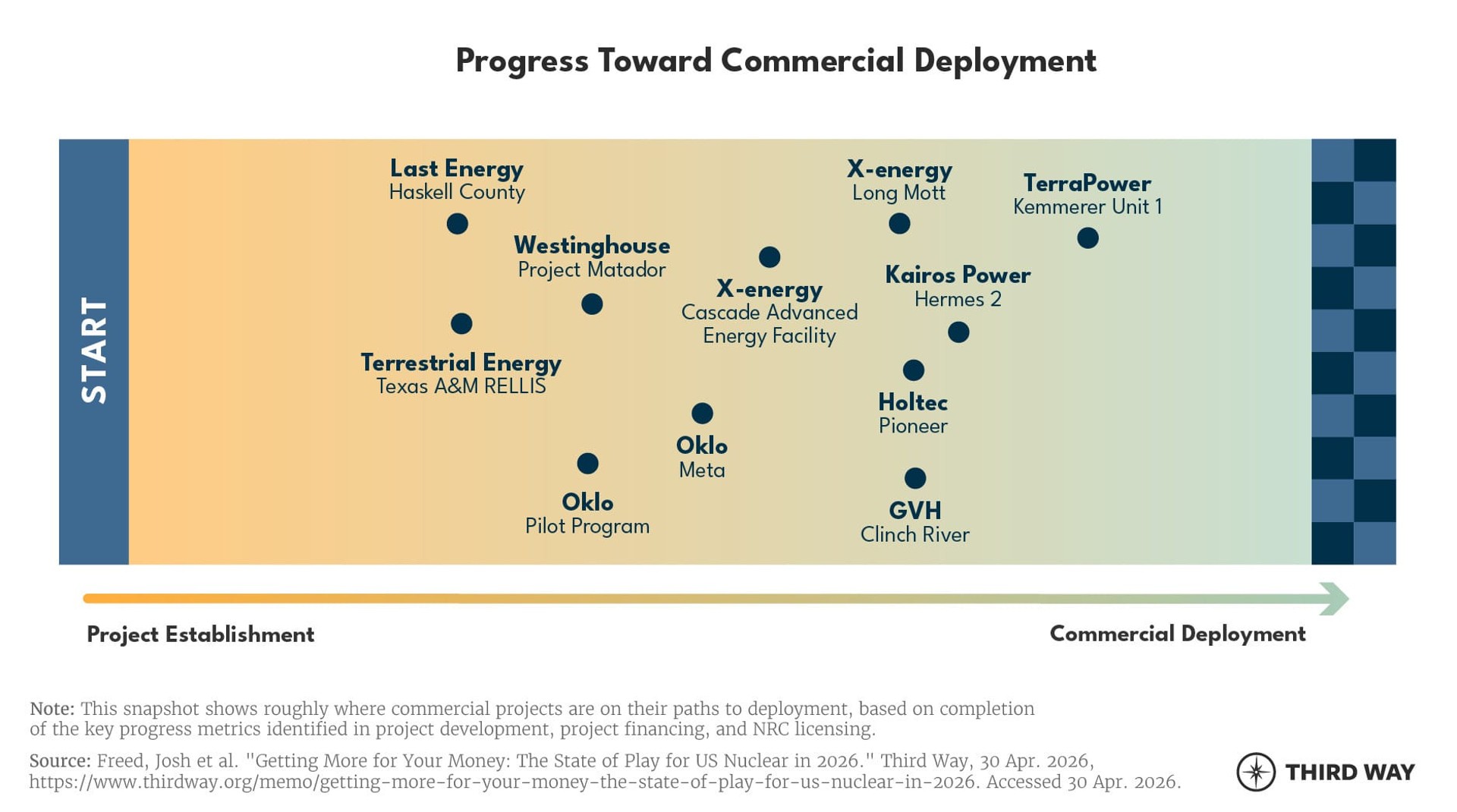

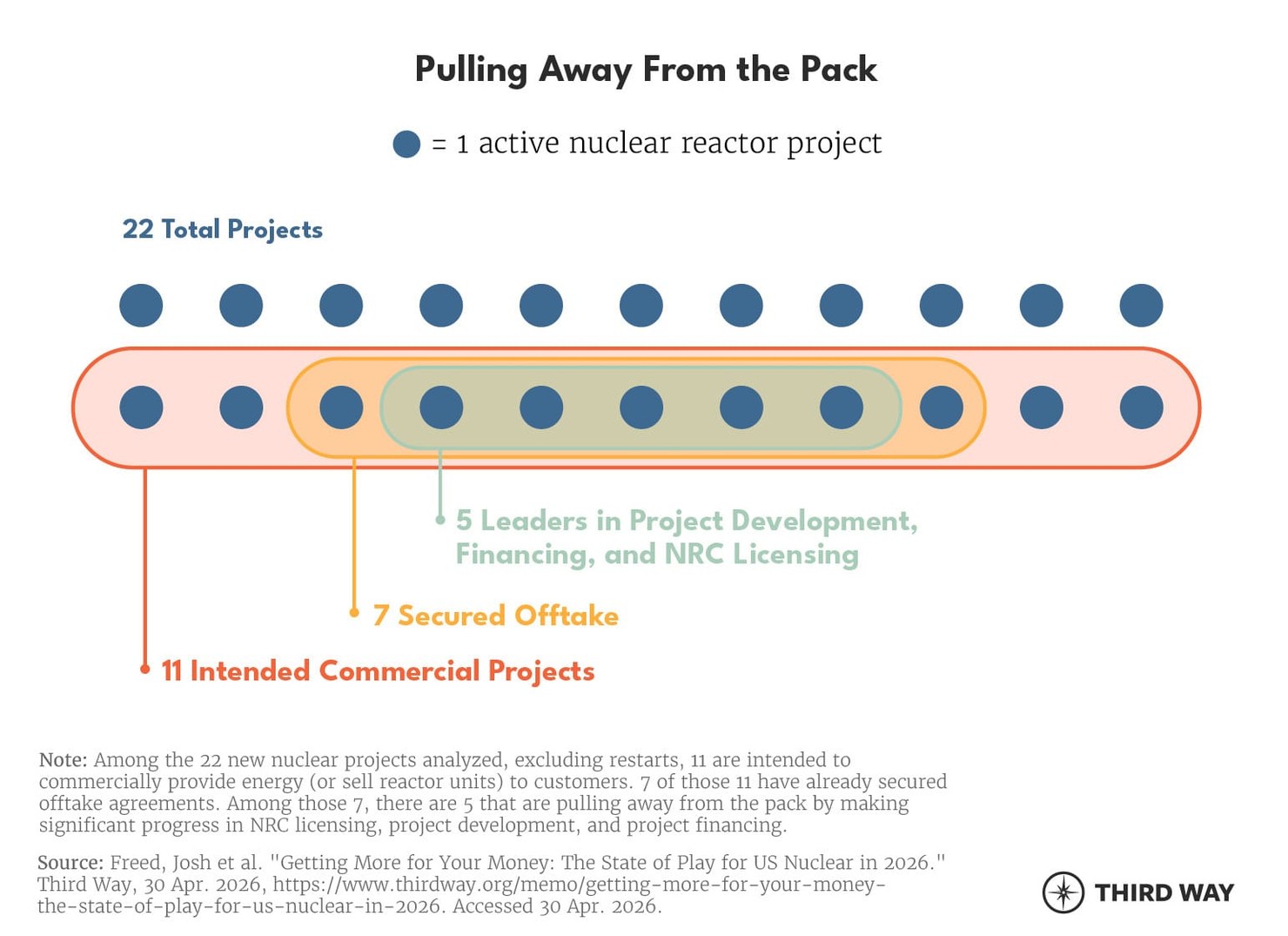

Out of the 22 active projects surveyed (and as shown in the table above), we found that:

- 11 are intended as commercial projects to provide energy to an offtaker (or provide the reactors themselves to a customer).

- Of those, 7 have secured offtake commitments to date.

- Most conspicuously, only 2 commercial projects have received Nuclear Regulatory Commission (NRC) construction permits. 2 non-commercial test/research projects have also received NRC construction permits.

The data shows a few commercial projects have differentiated themselves by meeting key benchmarks in project development, finance, and NRC licensing. While meeting these criteria does not guarantee a project’s ultimate success, it does increase project certainty and the likelihood of reaching final investment decisions, completion, and commercial operation.

The projects closest to commercial deployment have generally:

- Secured commercial offtake.

- Blended federal funding and private investment into project-specific financing pathways, allowing the signing of engineering, procurement, and construction (EPC) contracts.

- Engaged early, often, and collaboratively with the NRC.

Lessons Learned from Leading Commercial Projects

Some of America’s leading nuclear projects have illustrated unique and innovative pathways towards commercial progress:

Trailblazing new markets for nuclear energy: X-energy is a pioneer in securing customers for nuclear energy outside of the traditional power and utilities sectors, finding both a project developer and offtaker in its groundbreaking partnership with Dow Chemical at Long Mott Generating Station.

Unlocking creative project financing structures: Holtec, building upon site-neutral federal support for its SMR design, recently received an award through the Generation III+ SMR Pathway to Deployment Program for its dual-unit project at Palisades, with opportunities for additional public financing and crowding in private investment.

Iterative and sustained engagement with the NRC: Kairos Power’s Hermes 2 project built upon its prior engagement with the NRC on the development and licensing of the Hermes 1 non-power demonstration, culminating in a landmark power purchase agreement with Google in 2025.

Key Takeaways

There’s a lot more work to do if existing public-private partnerships are going to create a thriving new nuclear energy fleet. Third Way’s analysis of the data and current policies identifies three major weaknesses to the goal of scaling American nuclear energy.

1. New Administration Policies’ “Curb Appeal” Hides a Weak Foundation

The Trump Administration has taken some key steps in support of reaching 400 GW, such as unlocking long-overdue disbursements of fuel funding. However, not all of the administration’s policies and priorities have aligned with the scale of its aspirations. Reaching 400 GW of nuclear (or even something in that vicinity) in 25 years will require prioritizing commercially-ready designs and projects with existing commercial demand.

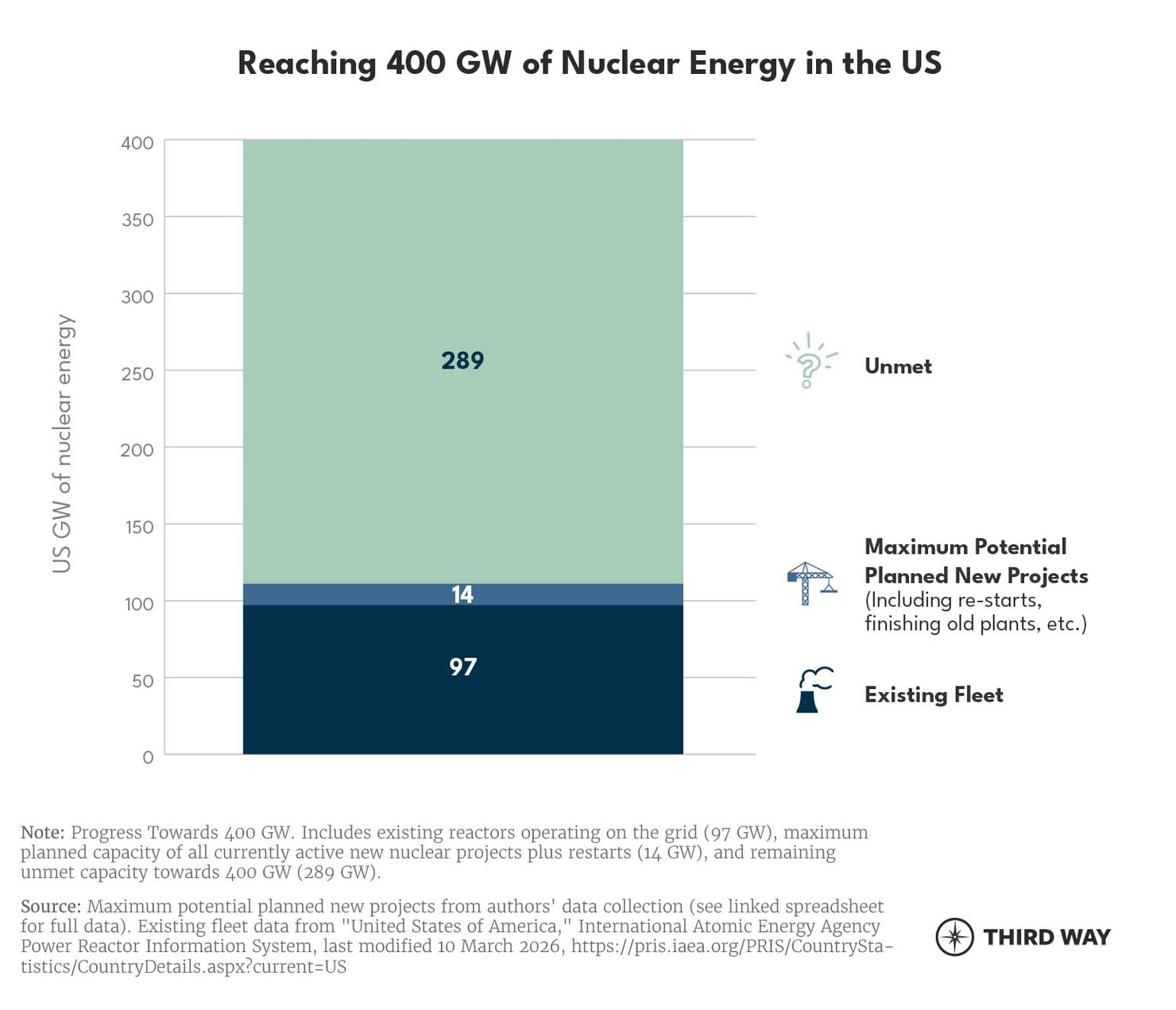

Even if every project included in this assessment, plus planned restarts of existing plants, were to successfully deploy their maximum planned number of reactors, we would still be 289 GW short of the additional 300 GW needed to meet the administration’s goals.

Getting to 400 GW requires sizable capacity additions, meaning gigawatt-scale large light-water reactors must play a role. Despite the completion of Vogtle 3 and 4, investors and private sector off-takers have shown less interest in new large reactors than small modular and advanced reactors. To them, building large reactor projects means bigger scale, higher costs, and longer timeframes.

While many headlines celebrate large reactor deals with countries like Japan, even basic details about the agreements—who will ultimately own and operate the plants, how they will be financed, and where they will be built—have not yet been released. Demand for new large reactors remains theoretical.

Customers, project developers, and investors need much more certainty to turn announcements into real projects.

Avoiding Distractions To The End Goal

Even more perplexing: in a period of constrained federal staffing and resources, significant time and effort have gone into developing (and hyping up) DOE’s Reactor Pilot Program (RPP) per last May’s Executive Order. The order called for at least three advanced reactors to “achieve criticality” by July 4, 2026.

With no clear commercial plant at the end of the tunnel, federal focus on the RPP is an unhelpful diversion from the 400 GW objective.

Criticality, which can be like idling a car engine, is necessary for a commercial reactor to produce electricity and provides useful data on newer fuel and reactor designs. But it’s not a commercial breakthrough, and few reactor companies would place “achieving criticality” in a non-power reactor as a key commercial milestone.

Above all, this program’s explicit goal is criticality and not deploying commercial plants. None of the program’s pilots presently meet the basic threshold of a commercial project: secured offtake of generated power and/or heat by a private consumer, or sale and deployment of reactors to a commercial operator.

Additionally, despite the RPP’s claims that it “fast-tracks commercial licensing,” DOE authorization is not a substitute for commercial licensing at the US Nuclear Regulatory Commission (NRC). The NRC has sole jurisdiction over the regulation of all civilian uses and commercial applications of nuclear energy.

The pilot program could provide the NRC with helpful data and regulatory familiarity for eventual commercial licensing. Otherwise, as it stands, it’s not at all clear that a DOE authorization will make it easier or faster for an RPP project to get an NRC license.

Some test projects have gotten shovels in the ground faster through RPP. But artificially accelerating project development timelines is a short-term solution, not a long-term fix. The government should prioritize helping companies engage with the NRC and develop robust supply chains. Both actions would help industry understand what to actually expect in the commercial project development process and lay the groundwork for future deployment.

The United States needs new commercial projects on the grid now (and ideally, in sizes larger than the microreactor scales typical of the RPP pilots), not gambles on test projects or more speculative designs for splashy social media.

2. Public and Private Investors Must Focus Their Money

Nuclear companies secured over $1B in private investment during the last quarter of 2025 alone – a huge boon to the industry. But both the private sector and the federal government could get more for their money, and by extension, closer to achieving 400 GW.

A significant portion of this private interest and investment in nuclear is directed towards developers with no commercial projects at present, limited market prospects for their technologies, and/or uncertain pathways to a commercial license. In and of itself, the volume of private capital doesn’t inherently measure progress towards commercial feasibility.

Without closer analysis, private investment announcements are just noise.

Federal investment has been critical to commercializing reactor designs and has facilitated the development of the most mature projects in the current pipeline. Current federal spending, however, does not match its previous efficacy or ambition.

The DOE Office of Energy Dominance Financing (EDF) is touted as the primary federal financing resource for domestic nuclear, with expansive loan authority and enthusiastic leadership. Its mandate is to take risks and “bridge the gap” where private banks and financial institutions are not yet willing to engage.

The program was designed to finance first-of-a-kind (FOAK) technologies, as it did with Vogtle 3 and Vogtle 4.

However, the administration’s ambitious goals are not being met by EDF’s shockingly conservative investment strategy, which is confined to low-hanging fruit, like restarts and uprates.

EDF’s director says, “We can’t lean in any harder on nuclear.” But while restarts are meaningful—the Palisades restart in Michigan is bringing 800 MW back onto the grid—there are finite restart opportunities in the US. Collectively, restarts and uprates will not get us substantially closer to 400 GW. To achieve our goals, EDF must make good on its promise and invest in FOAK projects.

Failure to invest in FOAK contributes to an environment in which many American firms plan FOAK deployment overseas, such as GE Vernova Hitachi’s BWRX-300 under construction in Canada and NuScale’s VOYGR-6 approved through Final Investment Decision in Romania. There is currently more concrete demand for large reactors like the AP1000 abroad than domestically, despite statements from EDF to the contrary. EDF has stated its support for new large reactor investments, but so far, it has failed to put its money where its mouth is.

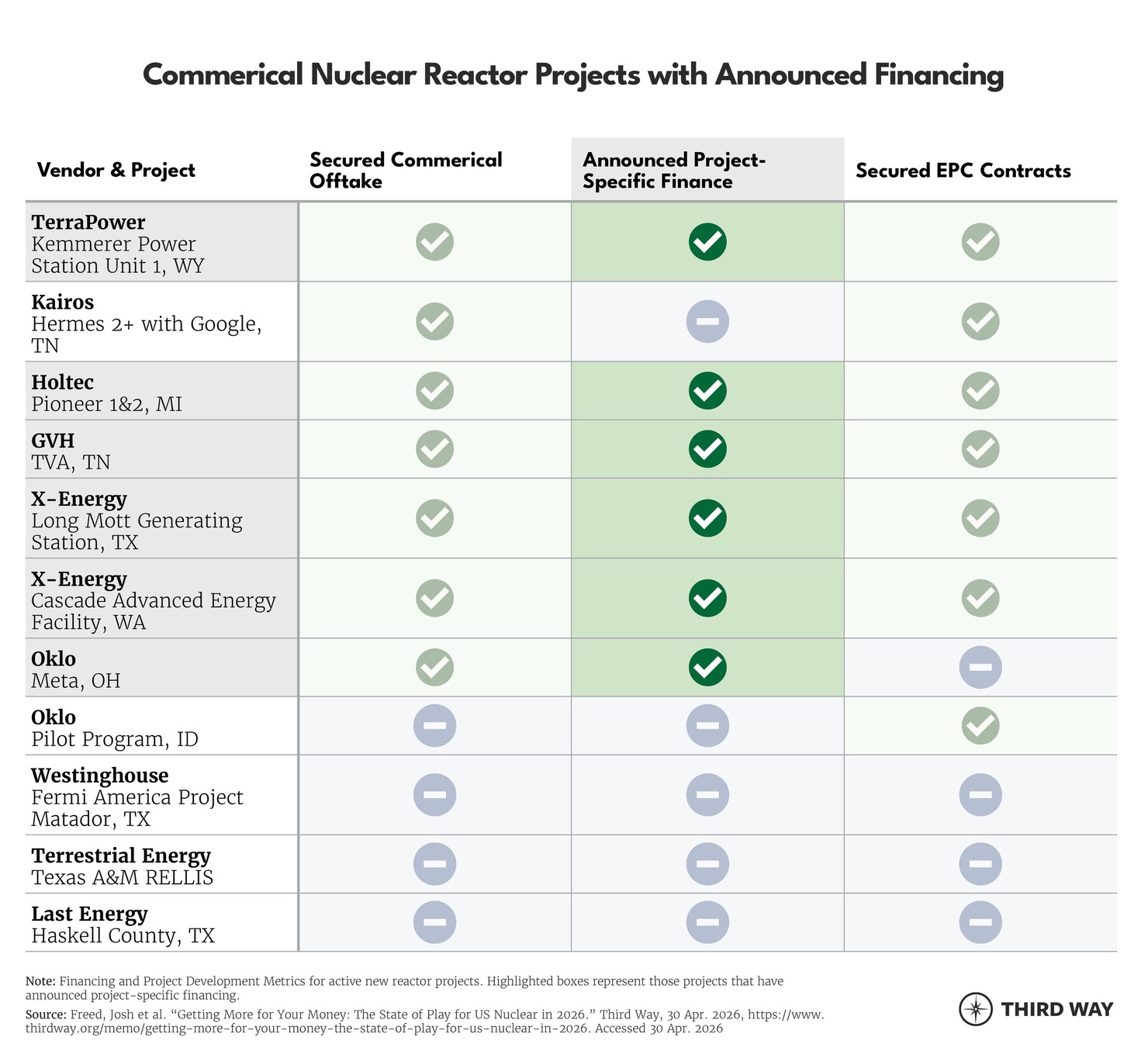

Even with robust public or private investment in a company, the mere existence of capital (whether equity or loans) is not a sufficient measure of a project’s success. A far more precise barometer: has funding been directed with the explicit intent of advancing a commercial project? Of the 22 projects surveyed, only 6 have publicly announced inflows of public or private capital towards an explicitly commercial endeavor, not just a test:

3. The Field is Overcrowded - Let It Narrow

The administration’s current approach incentivizes a more crowded nuclear market. That strategy is outdated. A crowded space can be a sign of a maturing industry, but the sector is fundamentally different than it was a decade ago. And the landscape assessment shows a group of leading developers starting to break away from the pack.

It may sound counterintuitive, but a narrowing field is ultimately good news for getting to 400 GW: attempting to commercialize every technology will leave projects sitting half-finished, without enough momentum to reach scaled deployment.

The projects closest to commercialization all received durable and consistent federal support. Across multiple administrations, government concentrated its commercialization efforts (funding, capacity, time) on executing a handful of projects based on bipartisan Congressional legislation.

Those projects—Advanced Reactor Demonstration Program (ARDP) and Generation III+ SMR Program awardees, among others—have continued to make progress towards commercialization because of sustained support from government. That federal spending drove additional private investment and partnerships.

The Trump administration relies heavily on Executive Orders to create a constant churn of announcements. Once they’ve made headlines with a flashy announcement from a developer, the Administration is on to the next, instead of building a durable foundation of federal support for projects on the roster.

It takes years to deploy commercial nuclear energy; that creates a mismatch between the duration of federal attention projects receive under the Trump administration and the timeline for project completion.

The Administration must tailor its approach and, instead of focusing on quick-turnarounds to make headlines, prioritize durable support for projects closest to deployment. That will encourage further narrowing of the market—and a better future for nuclear energy writ large

Conclusion

There has been astounding progress towards new nuclear energy over the last decade, with bipartisan support and increasingly positive public opinion encouraging the sector’s development. But getting new nuclear projects over the finish line is far more demanding.

To realize a resurgence of US nuclear, it’s not enough to simply scatter resources across a crowded space. To make good on federal and private sector investments and achieve the ambitious 400 GW goal, stakeholders in the nuclear space need to coalesce around the most viable commercial projects—based upon actual market signals, not just hype.

It’s that kind of consistency and focus that will realize the American nuclear revival.

Methodology

Our Approach

To survey current US new nuclear projects, Third Way reviewed open-source press releases, reporting, and other sources to aggregate the latest publicly accessible information. The resulting data offers a snapshot of the current state of play among active nuclear energy projects. While there is much activity across the nuclear ecosystem, this assessment focused on the fundamental commercial heart of the nuclear industry: the reactors themselves.

What Makes a Project?

Third Way included a reactor developer’s project (or a restart by an owner/operator) in the dataset if it had the following features to be sufficiently considered a distinct deployment effort rather than merely an expression of intent:

- Specific reactor technology

- A discrete new deployment opportunity for a commercial project or a project explicitly intended to create a pathway for future energy production (more than simply expressing intent to commercialize a technology broadly)

- Confirmed site selection

The larger data table includes planned reactor restarts and an intended existing plant completion project as well due to the potential for private and public sector funding, advanced engagement with the Nuclear Regulatory Commission, and impact on total GW added. It is assumed that other existing plants will continue to operate or pursue license renewals, continuing to contribute to the goal of 400GW.

The data collected fell into 3 major categories: (1) Reactor technology and design features, (2) federal engagement and licensing activity, and (3) project information. All data were sourced from publicly available sources and are aggregated here.

Metrics of Progress

The included projects represent different approaches to financing, technology advancement, and project development, but within the industry, there are some common project features that are pivotal to project progress. The assessment identified current key metrics of progress towards commercial deployment for new nuclear projects and assessed each project on the metrics reached based on expert input and trends among the projects racing to deploy. Many more metrics can support a project’s progress, but these key gates hold particular significance for a project. Altogether, meeting these metrics indicates that a project is technically validated, feasible for its specific location, capable of implementing a complex deployment plan, and sufficiently financed so as to indicate greater likelihood for successful project completion. They are as follows, in two broad categories:

1. Project Development and Financing

Complex supply chains, specialized expertise needs, capital intensity, long timelines, and other nuances of nuclear projects require a reactor developer or project developer to have excellent management of project development milestones and cooperation with development partners. Project development challenges can balloon costs and derail timelines to deployment, making related milestones essential for keeping a project on track.

Capital is one of the largest obstacles for new reactor projects. While money is beginning to flow into nuclear at large, that corporate-level fundraising doesn’t always translate directly into a project as it could be used for overhead, R&D, general design licensing engagements, etc. The more accurate assessment of capital raised to deploy a technology comes on a project-by-project basis. Any new project will need access to debt and/or equity for upfront costs pre-profit.

Achieving these project development and financing benchmarks indicates a serious and strategic approach to deployment:

- Secured offtake agreement/sale agreement: The gold-standard indicator of true demand for a project. Offtake agreements, unlike a Memorandum of Understanding (MOU) or Letter of Intent (LOI), are legally binding and indicate some discussion of terms. A power purchase agreement of some or all of the planned power production for a project or agreement to buy reactor units does not inherently mitigate upfront capital expenditure costs, but it represents the potential for long-term returns and indicates that there is demand for energy at a specific location. Of note, some reactor projects are not intended to sell the energy produced, but rather sell entire reactor units. This metric therefore also includes unit sale agreements.

- Secured EPC contract(s): commercial new nuclear projects are exercises in project risk allocation. For a project developer to focus on broader project coordination, fundraising, and deals with other project stakeholders, it will need to rely on experienced EPC contractors to manage construction and project delivery. While do-it-yourself approaches may work for small-scale tests, commercial-scale projects are too complex to effectively develop and construct solely in-house. Securing EPC contracts indicates that a developer has a serious plan for bringing blueprints to life. Perhaps more notably, it indicates sufficient funds to underpin high-capital contracts.

- Announced project-specific financing (government or private): Financial commitment to a project, whether public or private, indicates confidence in that particular deployment plan as much as it does for the technology itself. In a new market like the one for advanced reactors and SMRs, government investment has been essential to kickstart projects towards demonstrating commercial viability and further private sector financing. Federal funding has been essential for the nuclear industry at large, but any long-term commercial picture beyond federally-funded demonstrations needs private dollars. Meeting this metric indicates that a project entity is presently focusing on fundraising for upfront capital expenditures, or has already secured sufficient funding for a given project separate from the various corporate-level costs of research and development, design licensing, and overhead. This metric includes all types of federal funding that are directly related to a specific project, including cost-share awards, direct grants, and EDF loans. This metric does not include corporate-level fundraising announcements, as those may not be tied to specific projects.

2. NRC Licensing

The federal licensing process for a new nuclear facility is essential—a power reactor on the grid or other commercial reactor operation must be licensed by the NRC, and attempts to reach the commercial market will legally and ultimately require NRC approval. The licensing process includes multiple steps of technical safety and environmental review culminating in approvals to construct and operate a facility. The key metrics are:

- Submitted formal license application: the beginning of the licensing process. While many reactors and projects are the subject of pre-application activities, few entities have formally submitted applications for specific projects. Formal site-specific license submission (and submission acceptance), typically of either a construction permit application or combined operating license application, indicates that a specific site (and therefore project) is promising enough to commit significant time, effort, and fees to move through the NRC process.

- Received construction permit/approval: issuing a construction license. Receiving a construction permit means the NRC has approved the safety and environmental features of a project and represents the final licensing hurdle before beginning to construct the reactor. At this point, the likelihood of project completion increases significantly.

- Received operating license: Regardless of licensing pathway, all projects require as a final regulatory step approval to operate the reactor. This allows the operator to start up the facility. The review leading to issuance of an operating license also finalizes design and safety approvals.

Together, these metrics give a general picture of the path forward for a project, as the projects that have reached more of these milestones towards a commercial deployment are most mature in the race to produce energy for a consumer.

If you have questions about our methodology or data, or you want to provide public information about a project for our consideration, please email [email protected]