Memo Published April 8, 2026 · 9 minute read

Chinese EV Expansion Puts the Entire US Auto Industry at Risk—and Trump is Opening the Door To It

Takeaways

- The Chinese government has spent decades heavily subsidizing its auto industry, enabling its automakers to undercut global competitors and capture significant market share around the world, particularly in Europe and Latin America.

- Chinese automakers are now targeting the North American market. This poses a direct challenge to US manufacturers and raises broader concerns around economic security, supply chain resilience, and data privacy.

- Departing from bipartisan consensus and ignoring industry concerns, President Trump has signaled growing openness to Chinese investment in the US auto sector.

- Allowing Chinese automakers to establish a foothold in the U.S. market risks inviting the rapid decline of a strategically important domestic industry that has been a cornerstone of the American economy for over a century.

The US auto industry is approaching a crossroads. Over the past decade, China has surged to become the world’s largest producer of motor vehicles, rapidly expanding its presence across Europe, Asia, Africa, and Latin America. Backed by extensive state support, Chinese automakers export heavily subsidized electric, hybrid, and internal combustion engine vehicles at prices far below their true fair market value, distorting competition and undermining incumbent manufacturers.

In a concerning new stage of expansion, Chinese firms are now also establishing localized vehicle production and assembly operations in key markets around the world.

North America now stands as the last major market largely insulated from this wave of low-cost imports and localized production. But that’s starting to change.

Until recently, there was broad bipartisan alignment in the United States – and across North America – that Chinese auto imports posed a grave threat to national, economic, and data security. Lawmakers agreed that Chinese-made vehicles meant risking plant closures, job losses, a hollowed out domestic supply base, and even sabotage or surveillance. That consensus is now breaking down.

Trump’s tariff strategy has strained relationships with our neighbors and made China seem like a more stable trade partner. Canada has even begun lowering barriers to Chinese EVs, opening its market to Chinese automakers for the first time in history.

Rather than developing a strategy to counter China’s industrial expansion, President Trump has signaled a willingness to open the US market itself—inviting Chinese automakers to build electric vehicles in the United States.

“Let them come in,” he said in January, despite years of rallying against China’s unfair trade practices and promising to protect American industry.

How China’s Auto Companies Became a Threat

China’s rise to become the world’s dominant motor vehicle manufacturer took years to materialize. For decades, Beijing used massive state subsidies, protectionist domestic policies, and forced technology transfers—often involving US companies—to build globally competitive firms.

That effort was crystalized in 2015 with the launch of Made in China 2025, a sweeping industrial strategy designed to capture global market share in key advanced manufacturing sectors. Beijing’s push into electric and hybrid vehicles became part of a deliberate, state-directed effort to position Chinese firms as the leaders of the global auto industry. But the objective was far broader than just EVs and hybrids – it was long-term control over the future of global automotive manufacturing, its supply chains, and the innovative technologies that underpin it.

Beijing threw enormous financial support into this strategy. One study by the Center for Strategic and International Studies estimated that Chinese government support for the EV industry totaled over $230 billion USD between 2009 and 2023, excluding the substantial subsidies also offered to other upstream sectors like critical raw materials, mineral processing, and battery manufacturing, which Chinese companies also dominate.1

In addition to extensive state support, some Chinese automakers have faced scrutiny over labor practices used to further reduce costs. In 2025, the Brazilian government sued the Chinese carmaker BYD over alleged human trafficking violations and poor working conditions involving more than 200 migrant Chinese workers—conditions authorities described as “analogous to slavery” at the company’s flagship factory. Human rights groups have also reported evidence of forced labor at BYD facilities in Hungary.

With a powerful combination of technological capability and significant cost advantages, Chinese vehicles have rapidly improved in design, software, and performance—often rivaling or surpassing Western competitors. The price advantages can be stark: BYD’s cheapest EV model can be sold for as little as $10,000 in some markets, while a comparable model from a US automaker could cost two to three times as much.2

Chinese firms now account for more than one-third of global auto sales last year, up from just three percent in 2000.3

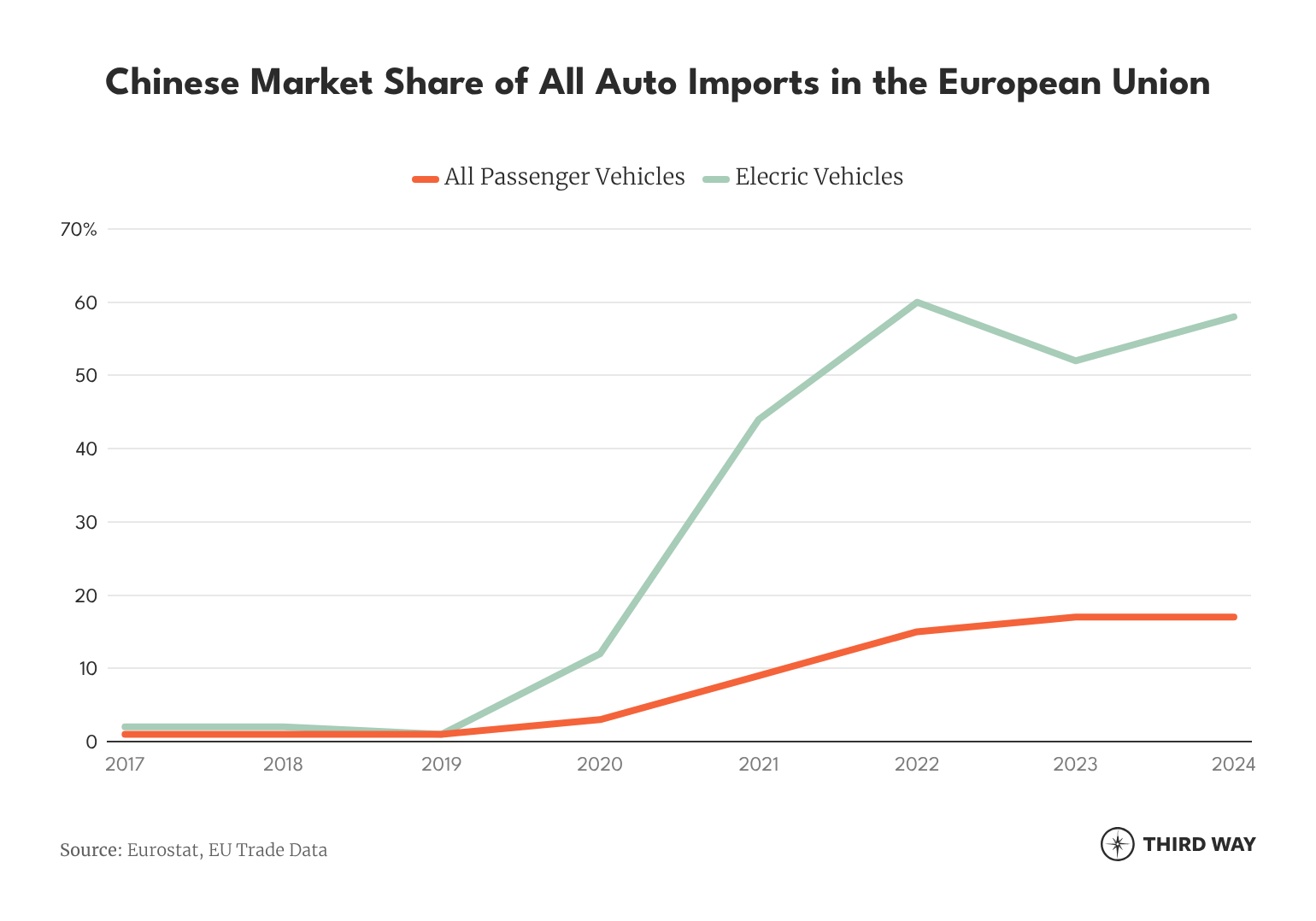

That explosive growth has created massive overcapacity in China’s domestic auto industry, forcing manufacturers to aggressively and successfully expand overseas. In Europe, for example, one in in ten cars sold today is now made by a Chinese brand – up from virtually nonexistent levels a decade ago.

Chinese firms have made even faster progress in developing markets with more relaxed trade regimes. In Thailand, Chinese brands account for more than 70 percent of EV sales, while in Brazil—where Chinese automakers only entered the market a decade ago—roughly 80 percent of EV sales are Chinese models.

How the Threat Could Materialize in the United States

The United States is the only major auto market in the world where Chinese firms lack a meaningful foothold, due entirely to strong trade and regulatory barriers. Tariffs on Chinese vehicles exceed 100 percent and new Department of Commerce rules restrict the types of Chinese software and hardware allowed in vehicles sold in America.

These barriers now seem increasingly vulnerable as the Trump Administration softens its stance on protecting the domestic auto industry.

There are two ways Chinese automakers could exploit this if the Trump Administration allows it: indirect access through North America and direct investment in US manufacturing or assembly operations.

North American Backdoor

The most immediate risk runs through Canada and Mexico, where growing footprints could allow Chinese automakers to circumvent US tariffs. Under the USMCA rules of origin, vehicles manufactured in Mexico or Canada with at least 75 percent North American content can enter the US market tariff-free. That creates a clear pathway for Chinese firms to use localized production facilities in Canada or Mexico to bypass US trade barriers.

Though Canada has established initial import caps on Chinese vehicles for now, its erosion of tariffs and other trade barriers means that cheap Chinese imports could flood the Canadian market at a rapid rate. This also opens the door to localized production by Chinese firms in Canada, which could quickly start cutting into American companies’ market share.

Meanwhile, Mexico has already become a major entry point, with Chinese-made vehicles accounting for a growing share of its domestic market and Chinese firms investing in production capacity.4 Though Mexico announced it would raise tariffs on Chinese cars to 50 percent effective January 1 of this year, it may come as too little too late.

Chinese EVs now account for over 70 percent of Mexico’s EV sales and over 20% of all auto sales, and Beijing has already threatened retaliation for what it calls unfair investment and trade barriers being imposed on its auto industry.

Foreign Direct Investment in the US

The second pathway is foreign direct investment, a strategy that the Trump administration appears to be increasingly open to. While foreign investment and open competition should be welcomed in principle, Chinese automakers do not operate on fair market terms and can effectively operate as instruments of their government. They are heavily subsidized, vertically integrated, and often willing to accept minimal profits—or even losses—to gain market share in support of strategic priorities set by the Chinese government.

Critically, these investments would not create new demand—they would displace it. Chinese-owned plants would compete directly with existing US facilities, putting pressure on domestic manufacturers, threatening jobs, and shifting high-value R&D and engineering work overseas.

Trump’s Approach is Making the Problem Worse

Sweeping tariffs alone – the Trump Administration’s apparent solution to all trade problems – are not a strategy for combatting China. They have increased the cost consumer goods, food, and industrial inputs for American households and businesses while doing nothing to strengthen domestic manufacturing competitiveness or the position of US automakers seeking to compete against Chinese EVs and other vehicles.

In fact, the Trump Administration and Congressional Republicans have deliberately obstructed the EV industry over the past year. They have cut consumer and commercial lease incentives, halted domestic battery manufacturing projects, paused charging infrastructure investments, and weakened fuel economy standards that encouraged EV adoption.

This administration and its allies have worsened the competitiveness gap for American manufacturers.

Without the financial incentive to innovate or invest in new EV production capacity alongside internal combustion engine vehicles, US automakers will be left behind as Chinese firms continue dominating, with substantially more backing from their national government.

Meanwhile, the administration has antagonized Canada and Mexico instead of finding a unified North American approach to preventing Chinese firms from exploiting trade loopholes. Worse, Trump has pushed our neighbors towards deeper economic engagement with China and dismissed the USMCA—an agreement his administration crafted—as irrelevant to US interests.

Coupled with his openness to Chinese automakers building directly in the United States, it is clear that the Trump administration lacks any semblance of a plan for preserving the long-term ability of the domestic auto industry to compete on EVs.

What the US Should Do Instead

The United States cannot rely on trade barriers alone, nor can it compete without more federal investment and a stable policy environment. To strengthen the auto industry’s competitiveness while manage competition with Chinese firms, the US needs a new strategy, including:

- Making a strong North American auto industry central to long-term US economic and national security policy.

- Restoring consumer incentives tied to domestically produced EVs, helping American EV production scale.

- Significant investment in domestic charging infrastructure, battery manufacturing capacity, and critical mineral and mineral processing supply chains to reduce dependency on China.

- Supercharging US research and development activities to develop next-generation innovations in battery technologies that surpass Chinese equivalents.

- Maintaining strategic tariffs on Chinese EVs to counter market distortions as domestic production capacity scales up.

- Close coordination and alignment with Canada and Mexico to prevent Chinese auto and battery firms from entering North America.

- Setting reasonable and achievable emissions and fuel economy standards that provide a predictable incentive for US companies to invest in innovation.

It would be a strategic mistake to open up the market to Chinese firms without a comprehensive strategy like this in place.