Memo Published February 11, 2013 · Updated February 11, 2013 · 6 minute read

Iceberg Ahead: The Looming Deficit Threat in 2013 CBO Report

David Brown

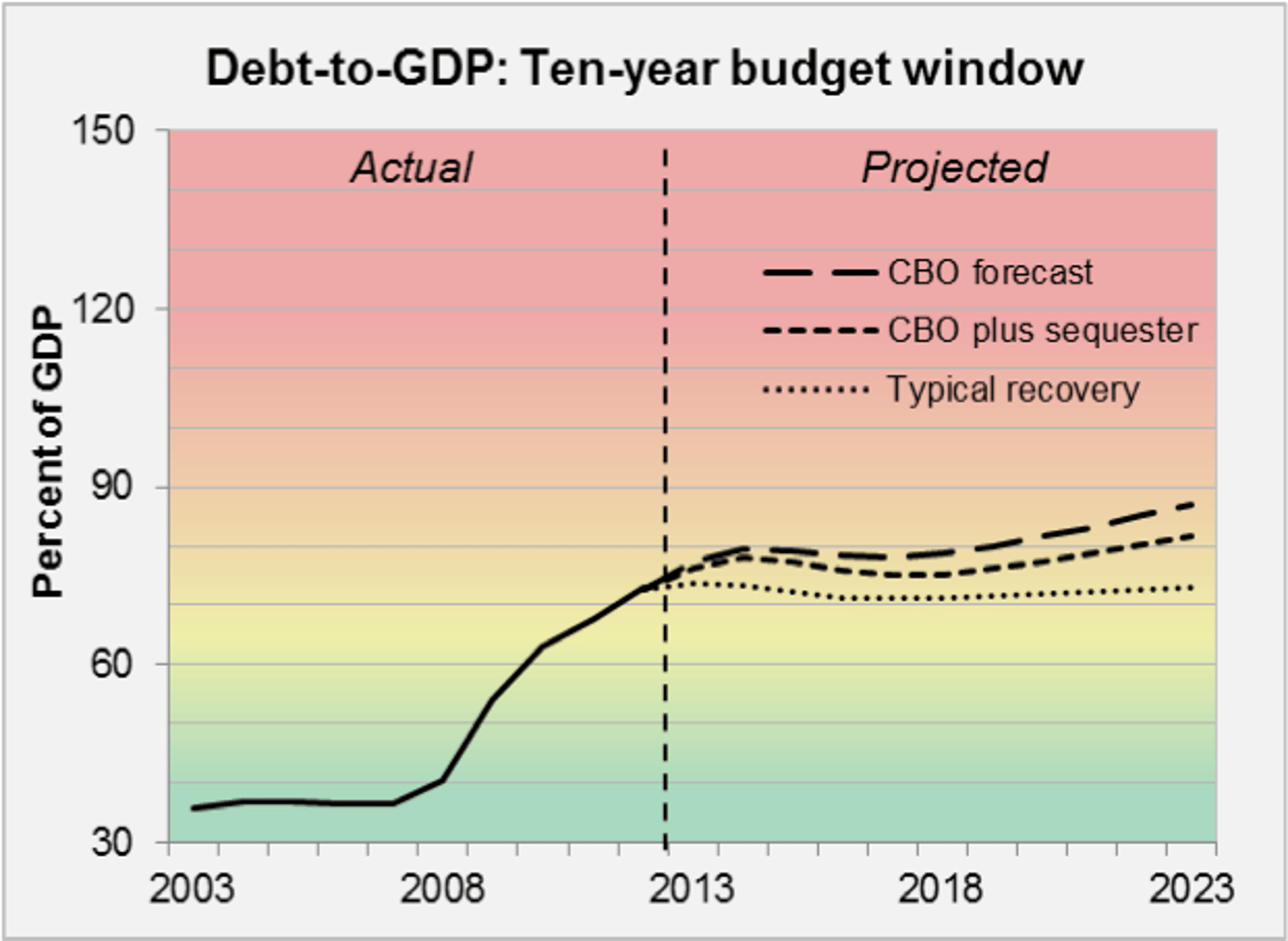

While some in Washington are patting themselves on the back over a new CBO report, which pegged this year’s deficit below $1 trillion, evident in the data is a troubling reality: Congress and the White House are sailing straight towards an iceberg—a debt load that equals 82% of our GDP in 2023 even if sequestration goes through. At a time when our economy is improving, our debt relative to GDP in ten years will be twice its average over the last 40 years. But that’s not even the most disturbing problem.

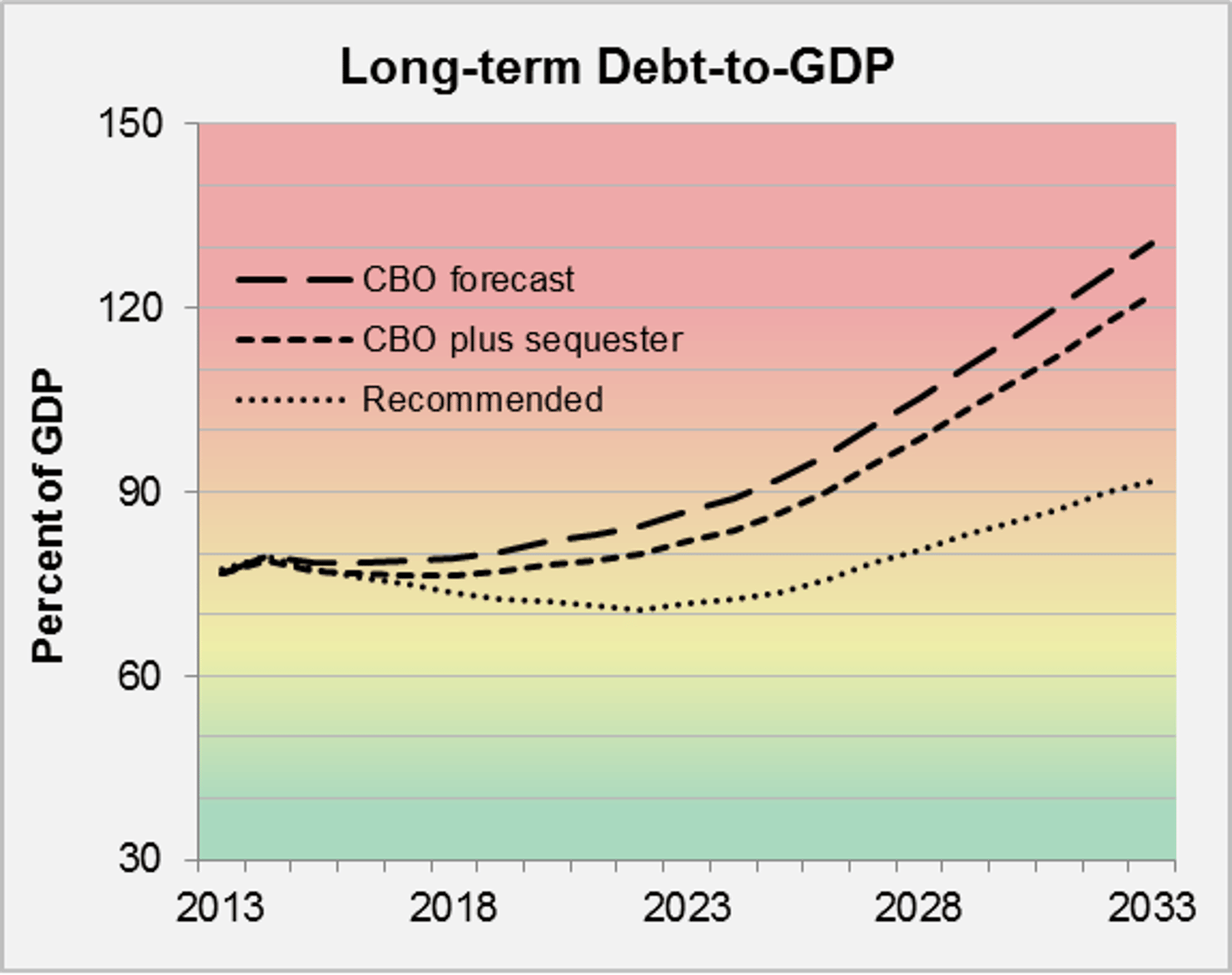

The next five to eight years represent the eye of the budget storm—the calm period before the baby boomer retirement costs really kick in, because by 2033, even with sequestration, the debt-to-GDP ratio will reach an unprecedented 122%.1 Thus, the next decade is the time to improve the budget outlook—mainly by beginning to tackle the growing burden of social insurance programs.

To steer clear of the iceberg, the White House and Congress must replace the sequester with a smarter package of deficit savings of roughly twice the size, about $1.9 trillion before interest savings. And rather than cut deeply into growth-inducing domestic discretionary spending, the package must include fixes to social insurance programs, allowing savings to grow larger the following decade.

How will the debt change in the coming decade?

According to CBO, the federal debt will rise steadily this decade, from 73% of GDP this year to 87% in 2023. That projection reflects the CBO’s most realistic assumptions about Congress: that it will observe the spending caps it set in 2011 but cancel the sequester, that it will continue increasing Medicare reimbursement rates for doctors, and that it will keep extending temporary tax breaks.

This debt path is alarming for two reasons. First, the level of debt will remain exceptionally high by any standard. The most often agreed upon healthy limit is 60% of GDP. And the average U.S. debt level of the last four decades—decades that saw robust economic growth—was even lower, at 39%. Second, the debt will continue to rise in spite of the anticipated recovery. It is acceptable—and preferable—that the debt increases during a slowdown. But after an economy recovers, the debt, relative to GDP, should fall. For example, when the economy grows at 3.4%, as the CBO forecasts for 2014, debt-to-GDP typically falls by half a percent.2 But on its current path, debt-to-GDP will rise by 3% in 2014. Furthermore, even after the economy returns to its full potential in 2017, deficits are large and continue to grow, from $750 billion that year to $1.3 trillion by 2023.

What if we allow sequestration?

Allowing sequestration—or replacing it with equivalent savings—would reduce primary deficits over the next ten years by a total of $950 billion. That level of savings would help slow the debt’s rate of growth, but it is far short of actually stabilizing the debt, much less reducing it. Even with sequestration, debt-to-GDP in 2023 would be an alarming 82% and rising.

How will the debt change after ten years?

The ten-year forecast only shows the tip of the iceberg. Projecting just a few years beyond 2023, CBO data reveals stormy seas in the mid-2020s. If social insurance programs—which are the source of long-term spending growth—remain unaddressed, a severe deficit problem begins. As the baby boomers enter their seventies, Medicare costs swell. Large deficits require rampant new borrowing, raising the cost of servicing the debt. So while deficits are an alarming 5% of GDP in 2023, they rise to an uncontrollable 9% of the economy in 2028. That is a near doubling of annual deficits relative to the size of the economy in just five years, in what is assumed to be a healthy, steadily growing economy. And sustaining a strong economy with that level of debt and deficits may be implausible.

How do we safely avoid this iceberg?

There is good news in the report, and it is this: It will not take yeoman efforts to get back to safe seas. To avert a fiscal crisis, Congress must produce savings roughly twice the size of the sequester, and it must do so in large part by making the major social insurance programs solvent—something we all know needs to be done.

Here’s how we would do it:

- Replace the sequester with better cuts. The non-defense sequester should be replaced at least one-to-one with mandatory program savings, primarily from fixes to Medicare. Defense cuts should continue but without the sequester’s restrictions.

- Lock in new revenue from tax reform. Congress must establish an expedited process for tax reform that simplifies the individual tax code and raises $500 billion in revenue. We suggest phasing in a cap on deductions for those with more than $250,000 in income (the cap would exclude charitable deductions). We would also apply chain-weighted CPI to the tax brackets.

- Authorize a Social Security commission. A select panel should propose a plan for 75-year solvency, and Congress should be required to vote on its recommendations with a simple majority by 2015. As a start, chain-weighted CPI that protects long-term beneficiaries should be done immediately.

- Defuse future debt limit battles by linking to deficit targets. Congress should both raise the debt limit for two years and reform it, so that the debt limit automatically rises if the debt meets specified annual targets.

This plan locks in phased deficit reduction. Entitlement and tax reform would establish savings targets immediately, and the resulting policies would take effect on a rolling basis this decade. The Social Security commission would focus on the long term, ensuring both solvency and a healthier unified budget deficit in future decades. And the debt limit solution would permanently impose a reasonable check on deficits without threatening the nation’s credit. This plan would also eliminate all cuts to growth-creating domestic discretionary programs.

Such a package would not completely solve our debt problem. But it would be a major course correction, preventing future leaders from choosing between a debt crisis and drastic austerity. It would leave our debt-to-GDP ratio far too high through 2033 but at least under 90%. It would take very little money out of the economy while America is still in recovery-mode from the recession. And it would ensure that among the world’s major advanced economies, the United States would be in the best fiscal shape.