Report Published October 19, 2020 · 22 minute read

It’s Time for a New Contract on Work

Jillian McGrath, Kelsey Berkowitz, & Gabe Horwitz

What should a person get from work? What should happen to help people through an inevitable spell of bad luck or a recession? What should it mean to work for pay but not be anyone’s employee? Should work provide not just wages and benefits, but also wealth? How should family responsibilities interact with work and pay? What parts of our current contract on work are vestiges of views on race, gender, and family structure that are either outright offensive or no longer apply?

We’ve had two once-in-a-century economic shocks in the last 12 years that leveled the country and put tens of millions of Americans at the brink of ruin. These shocks also laid bare what was already apparent during better times: we have two economies in America—one where work is sufficiently rewarded and another where the bond between work and a good life has grown tenuous. Corporate profits have risen, and that has benefitted many. But worker paychecks in the middle and lower wages have stayed stubbornly still. Globalization and technological changes have created wealth and opportunity, but it has also hurt people and places, requiring constant upskilling or even career change as workforce development remains an afterthought. Gig work has exploded and provided a new source of income for millions, but protections and benefits for workers in non-traditional work arrangements are non-existent. Going into the pandemic, women outnumbered men in the workforce and had more opportunities than generations ago, but our childcare system and caregiver policies are appendages and wholly inadequate. We live longer but overly rely on individual initiative for people to have enough to enjoy retirement. Union membership has gone down along with the security and benefits it provided. And systemic racism and discrimination remain a headwind against opportunities for people of color and continues in the workplace.

None of this is accidental or inevitable; much of it is the consequence of a 21st century economy relying on a 20th century contract on work. While that old contract was not perfect, it offered many a peace of mind—a sense that work would lead to a good life. Yet, as the economy evolved, the contract on work didn’t, creating a historic loss of confidence in American capitalism as the foundational promise of broadly shared prosperity and equality of opportunity. For example, today Black households have roughly the same sliver of wealth compared to White households as in the 1960s when the Civil Rights Act passed.1 And that is before COVID-19. Thirty million people still don’t have health insurance, and tens of millions more are under-insured, despite most of them working.2 Half of the workforce doesn’t have private retirement savings, and women, workers of color, part-time workers, and small business employees are less likely to have an employer-sponsored retirement plan.3And half of American families are struggling with childcare and paying prices that resemble college tuition.4

Eventually, we will emerge from the pandemic, but the post-COVID economy will look different. Where and how people work will change. We are witnessing the unprecedented collapse of small business. The businesses that survive and move forward will form a different private sector landscape. These changes must shake up our thinking and drive us to construct a new and equitable contract on work that rebuilds the bond between work and a good life. This new contract—forged between workers, employers, and government—must reward work and reimagine every aspect of compensation from work—wages and salaries, health care, retirement contributions, skill acquisition, paid family leave, and childcare, and helping those who have lost their jobs survive the blow and regain the dignity of work once again. This new contract must also address the inequities between races in America, or we will have neglected once again to fulfill the promise of opportunity that we have broken to millions in the past.

In this paper, we offer a critique of the current contract on work and describe how and why it is failing to provide a path to prosperity and security for most Americans. In sum, it:

- Provides too little. The contract on work has eroded over time, so it’s not robust enough to ensure that work provides stability and a good life.

- Is frequently unjust. The contract on work has glaring racial and gender disparities.

- Leaves too many people out. The contract on work hasn’t been updated over time to reflect the modern workforce, leaving too many people out.

- Is too hard to navigate and access. Many parts of the contract on work are difficult to use, sometimes deliberately.

We also outline what a new contract on work could look like with a fuller paper on the topic to come. The structure of a modern contract must meet the structure of the 21st century economy. It should help people make the most of good times and weather the bad times. The new contract should recognize that these critiques are in fact deep structural issues, not cyclical interruptions. And it should ensure that work leads to a good, stable life for people of all races, genders, and family structure so that hope and optimism for all outweigh fear and anxiety.

1. Provides too little.

The contract on work has eroded over time, so it’s not robust enough to ensure that work provides stability and a good life.

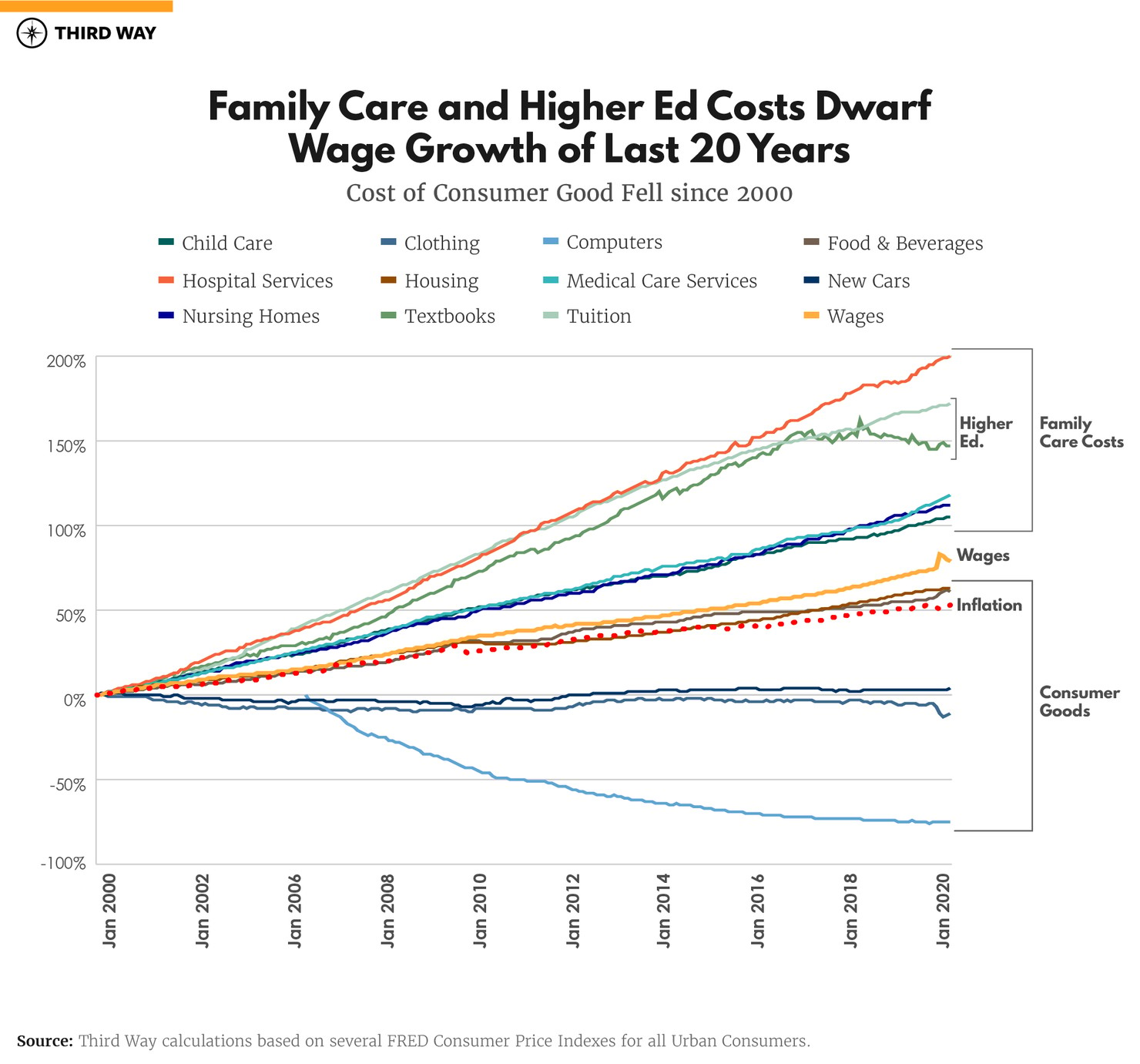

In decades past, many working families enjoyed a peace of mind—that stable work provided a life free of unreasonable financial stress. This relationship between work and stability has degraded over time to a crisis point, and families who work hard today are struggling to stay afloat and enjoy the promise of generations past. This is due, in large part, to wages failing to keep up with rising family care costs, and too few jobs providing middle-class wages to begin with—leading to the rise of working poor families across the country.

For decades, wage security in America has tracked far behind costs associated with securing family stability: hospital and medical care, childcare, nursing home care, and college tuition. While consumer good prices have fallen relative to wages, the costs that keep a family up at night have risen considerably.

The federal minimum wage hasn’t been raised in over a decade, setting the wage floor for the 21 states that have no minimum wage of their own. In real dollars, the national minimum wage in 2020 pays less than in all but six of the last 60 years.5 If the minimum wage kept pace with productivity growth since 1968, minimum wage workers today would make over $21 per hour—almost $14/hour more than the present $7.25 federal minimum. Instead, federal minimum wage earners today make 29% less than minimum wage earners 50 years ago after adjusting for inflation.6

Nationwide, just 38% of jobs pay enough on their own to afford a middle-class life or better for a dual-income earning family with children.7One-in-seven essential workers rely on the Supplemental Nutrition Assistance Program to fill the gap between poverty wages and livable income.8 Working families are increasingly forced rely on traditional safety net programs to put food on the table at home, speaking to the how low the quality of work has crumbled.

Meanwhile, wage gains have been skewed toward those at the top of the income distribution. Between 2000 and 2019, real hourly wages, excluding transfers, for workers at the 95th wage percentile grew by 31%. By contrast, wages grew 7% for those at the 50th percentile and grew just 11% for those at the 10th percentile. Even at the 70th percentile, wage growth of the past two decades hovered at just 8%, meaning outside of the top earners, wages have underperformed.9

Since 2009, benefits have grown by over 15% for workers at the 90th wage percentile, 5% for workers at the 50th wage percentile, and are below 2009 levels for low-wage workers at the 10th wage percentile according to an analysis of BLS data by economist Jared Bernstein.

Since 2009, benefits have grown by over 15% for workers at the 90th wage percentile, 5% for workers at the 50th wage percentile, and are below 2009 levels for low-wage workers at the 10th wage percentile according to an analysis of BLS data by economist Jared Bernstein.11

While the contract eroded especially for those at the bottom, the cost of necessities ballooned. Since 2009, health insurance premiums have risen 54% and deductibles have risen 162%.12 Spending on childcare exploded 2,000% in the last four decades.13 Only half of workers are lucky enough to have private retirement savings at all, but the typical amount saved is nowhere near enough to retire comfortably—just $40,000.14 Of the 51 million adults aged 65 and over in the United States, one-in-seven live in poverty.15

As costs rose and wages fell, middle-class and working families borrowed more. Personal debt, specifically non-housing debt, rose precipitously in the past two decades as families felt the squeeze between meager paychecks and necessary costs. Average non-housing debt owed by middle-income families, those making between $53,000-$98,000 per year, rose about 33% in the past 12 years. Student loan debt showed the starkest increase, as college tuition grew out of control after the Great Recession.16

The decline in wages and benefits is the result of decades of policy neglect and wage inequality gone unchecked capitalism creates prosperity, but only when coupled with a comprehensive set of policies to protect the vulnerable when the market falls short. We are long overdue for an update on these protective policies and need to reevaluate the consequences of deference to the free market at the expense of family prosperity.

2. Frequently unjust.

The contract on work has glaring racial and gender disparities.

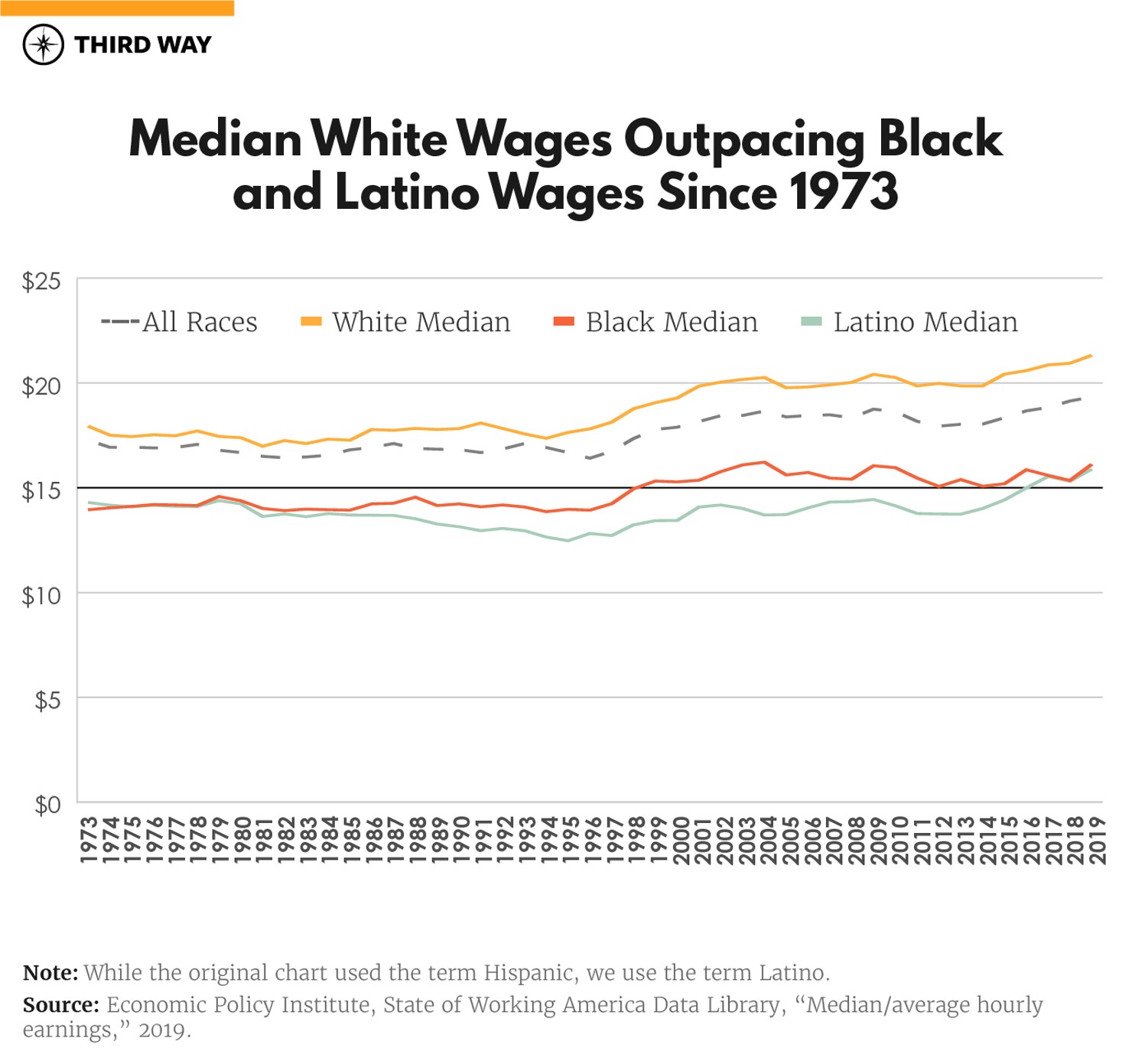

Everywhere you look, the contract on work is full of inequities—starting with pay. Exhibit A: Latino and Black workers earn less than whites. In 2018, median weekly earnings of full-time wage and salary workers were $680 for Latinos, $694 for Blacks, and $916 for whites.17 Blacks make up 13.4% of the population but were 18% of minimum wage workers in 2018.18 Fifty-seven percent of minimum wage workers are women ages 20 and up.19 Black and Latino workers also earn less than whites even after accounting for differences in educational attainment. White workers 25 years and over with college degrees have median earnings of $61,000 a year, while the same pool of Black workers with degrees earn $50,000 and Latinos earn $49,000. Whites without high school diplomas earn more than Blacks who have them ($31,466 compared to $30,437).20

Access to benefits through employers is also highly uneven depending on a worker’s race or gender. Latino and Black workers as well as women are overrepresented in low-wage jobs, which are less likely to provide benefits.21 For example, health insurance coverage has expanded to cover more people since the passage of the Affordable Care Act, but uninsured rates remain higher among nonelderly Native Americans, Latinos, and Blacks.22 Native Americans, Blacks, and Latino workers are significantly less likely to receive health insurance coverage through their employers than white and Asian workers.23

Low-wage workers, women, workers of color, part-time workers, and small business employees are less likely to have an employer-sponsored retirement plan.24 In 2016, 60% of white families had retirement accounts, compared to 34% of Black families and 30% of Latino families.

Of families who had retirement savings, the median value of retirement accounts for white families was $77,000, compared to $25,000 for Black families and $23,000 for Latino families.25

Women participate in retirement plans at the same rate as men, but the gender pay gap contributes to a gender gap in retirement income. Women on average are paid 80% of what men are paid during their careers, and then go on to receive 80% of the retirement income that men receive.26 Women make up two-thirds of the part-time workforce, and the part-time workforce is less likely to have access to and be eligible for employer-sponsored retirement plans.27

The supports needed to allow working parents to participate in the workforce are also uneven based on race and gender. Too many working families struggle to find affordable childcare. Half of US families reported finding childcare with difficulty, or not finding it at all. Black, Latino, Asian, and Native Hawaiian or Pacific Islander families in particular report struggling to find childcare due to barriers like cost, location, and lack of slots.28 Childcare subsidies, which help families afford childcare, don’t match the need that exists. Out of 13.6 million children eligible for childcare subsidies in 2015, just 15% received subsidies.29

This lack of affordable childcare slots hurts working families, single parents, and particularly women, who outnumbered men in the workforce going into the pandemic.30 Eighty-nine percent of mothers who found a childcare program were employed, compared to 77% of mothers who didn’t find a childcare program. This is particularly problematic for Black and Latina mothers, who are more likely than white mothers to be the primary earner in their households. Women also disproportionately work in jobs where hours vary and may struggle to find affordable childcare that meets their scheduling needs.31

3. Leaves too many people out.

The contract on work hasn’t been updated over time to reflect the modern workforce, leaving too many people out.

The current contract on work was designed for the economy of the 20th century, one where unions, pensions, and nuclear families were prevalent. The economy has fundamentally changed, but the contract has not, meaning more and more workers are shut out from its benefits.

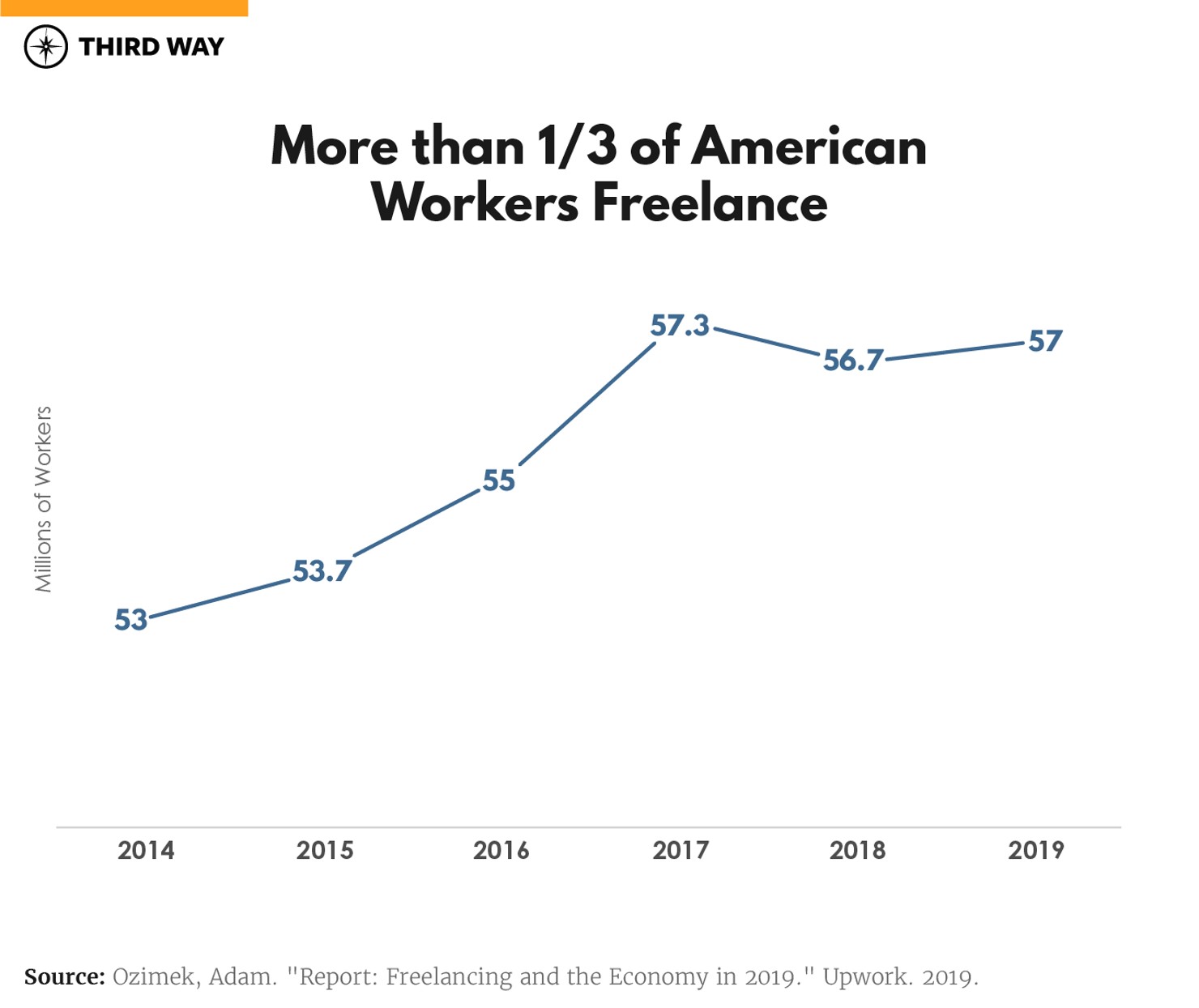

In nearly two-of-three families with kids under the age of 18, women are now the primary or co-breadwinners. In fact, in over 40% of families with kids under 18, the mother is the sole or primary breadwinner.32 Female earnings have never been more vital to family security in America, yet the current contract on work does little to support working mothers. More than 35 million workers engaged in the gig economy before the onset of the pandemic, and more workers regularly engage in freelance work (about 35% of the labor force at 57 million).33 But, no federal safety net exists for low-wage gig or freelance work, leaving tens of millions of workers without sick leave, minimum wage pay, family leave, health benefits, and more.

The gig economy represents a fundamental shift in the labor market in recent years, but even in traditional industries, worker representation fell to record lows. Unions represent just one-in-10 workers, receding from its historic high at 35% in 1954.34 The American economy shifted away from goods producing toward service providing in recent decades, and with it, unionization stagnated. Public policy failed to adapt to this shift, leaving too many workers exposed to exploitation.

During downturns, such as the historic recession we currently find ourselves in, the old contract on work leaves even more people out. Workers are particularly vulnerable to losing their jobs and sources of income during downturns, but our unemployment insurance and shared work structure shut the door on too many. Our unemployment insurance system is woefully antiquated, causing mass delays in getting benefits to families that are most vulnerable. It also fails to cover all gig work and self-employment, which is a significant blind spot. The United States has state-run shared work programs that help keep people on the payroll during downturns, but these programs are underused, and employers are often not aware of them.

The COVID recession has shed even more light on the massive risk of failing to provide an adequate safety net for small business owners and entrepreneurs. More than seven months following the onset of pandemic-related business owners, it is painfully clear that we must do more. No federal program exists to safeguard and protect small business owners as well, meaning our primary job creators shoulder disproportionate risk of financial devastation during times of crisis. Even during boom times, access to venture capital is typically concentrated among college-educated white, male entrepreneurs. Of venture-backed entrepreneurs, only 9% are women, 2% are Latino, and 1% are Black.35 Decisionmakers at VC firms are predominantly white and male, and this lack of diversity feeds into investment decisions.36

And if you’re a worker who wants to upgrade your skills or gain new ones to adapt to new technologies, you’re often on your own. The contract on work leaves out those who need help affording skills training programs to remain competitive in the labor market or keep up with the changing demands of their jobs. Half of unemployed Americans believe they need more education or training for the jobs they want, but only a quarter took a class or pursued additional training in 2016. Of those that didn’t seek out these opportunities, almost two-thirds said they couldn’t afford to do so.37

Even if you lose your job, you’re not guaranteed access to retraining funds. Individuals who lose their jobs may be able to access training funds through the Workforce Innovation and Opportunity Act (WIOA), but access is subject to funding availability. Adjusted for inflation, WIOA funding to the states has fallen by about 40% since 2001.38 WIOA formula funds were about $2.82 billion in FY 2020, but not all of this funding goes toward training.39

Many employers provide or sponsor training for their employees, but these training opportunities remain inconsistent across employers and are not equally available to all employees. Training is more common at larger firms, for employees with higher levels of educational attainment, and for employees who are white.40

4. Too hard to navigate and access.

Many parts of the contract on work are difficult to use, sometimes deliberately.

All benefits provided by the contract on work, whether they come from employers or the government, should be accessible, yet too much of our system today is the opposite. Health care, for example, is hard to shop for, price compare, and understand. Many people who don’t work in the health care field struggle to understand what the different parts of a health insurance plan are, such as deductibles or coinsurance. They may also have a hard time running the numbers to determine what a plan will cost them in a given year compared to other plans, or how much protection a plan offers in the event of a medical emergency. On top of this, it can be difficult to access tools to help make informed decisions or to seek guidance from experts.41 Navigators and assisters can help consumers shop for plans in the Affordable Care Act Marketplaces, but these critical roles have faced insufficient funding, and funding varies by state.42

Applying for assistance from programs that people need to be able to work or make it through periods of job loss—like unemployment insurance or childcare—often requires people to go through antiquated, complex systems. Applicants may have to visit offices in person and take time off work to do so. Applications can take a month or more to be approved. After being approved, people may have to recertify their eligibility, and the variable hours and earnings of many low-wage jobs can inadvertently kick workers and their families off programs. All these hurdles make it hard for workers and families to access the assistance they’re eligible for.43

Take unemployment benefits. Even before the pandemic, it was difficult to actually qualify for unemployment benefits. States have cut the number of weeks people could receive benefits, made it harder to qualify for benefits, put more of the application burden on individual workers instead of employers, and cut benefit amounts. At the start of the coronavirus pandemic, states were woefully unprepared to meet the deluge of demand for UI due to extremely outdated administration systems, resulting in deep backlogs, crashed websites, and unmet need across the country. The result has been many people struggling to receive income support at times in their lives when they need it the most.44 In 2019, the average UI recipiency rate across all states was 28%, down from 40% in 2009.45 Months into the pandemic, people who have been deemed eligible for UI are still waiting to receive their first unemployment checks in states like Arizona, California, and Texas.46

It’s also maddening to navigate the various worker training programs needed to obtain well-paying careers. The proliferation of learning options and credentials makes it harder for people to know which credential is best for their career goals or whether it will have value in the labor market. Racial, ethnic, and socioeconomic disparities persist in educational attainment and labor market outcomes.47 This won’t change unless we make it easier for people to navigate credential programs and convey the skills they have mastered. Yet the proliferation of credentials has caused widespread confusion about their quality. Employers, training institutions, and learners currently don’t get enough information on the DNA of a credential—that is, the competencies the credential-holder can be expected to have. Learners who want to get new skills may not know which credential is best for their career goals or how to assess the value of a particular credential.48

On top of this, it can be difficult for people to access individualized career services, such as one-on-one career counseling, that can help them flesh out their career plans and navigate the morass of credentialing options available to them. Of the adult and dislocated workers who received services at an American Job Center in 2018, only 58% received some type of individualized career service, including one-on-one career counseling.49

The current menu of programs available to help workers thrive in a 21st century economy is completely inadequate, the result of decades of neglect. Too often, policymakers made the deliberate choice to restrict access to spare themselves the trouble of properly caring for Americans. Just take state unemployment insurance systems which were often built to assume applications are fraudulent in order to limit access to benefits. As the director of Michigan’s Unemployment Insurance Agency puts it, “it’s built to assume you’re guilty and make you prove that you’re innocent.”50 Over 1 million Michiganders have filed for unemployment insurance since the onset of the coronavirus pandemic, but only 26% have received benefits in large part due to a system designed to slow and deny struggling workers the benefits they’re entitled.51

A New Contract on Work

To ensure that work can support a good life, a new contract must be forged between workers, employers, and government—one that rebuilds the bond between work and prosperity. An upcoming paper will lay out what a new contract on work could look like, but we have sketched out the contours of such an approach below. A new contract on work will guarantee:

Higher pay:

- A meaningful increase in the minimum wage that rises every year with inflation.

- A substantial expansion of the Earned Income Tax Credit (EITC) to make it more generous and reach more people.52

Stable, secure, and affordable health care:

- A cap on health care premiums, deductibles, and copays for everyone based on income.53

- Universal health care coverage by automatically enrolling everyone not insured in an affordable plan.54

Support for working parents:

- Out-of-pocket caps on the amount any family has to spend on childcare as a percentage of their income.

- A bigger and refundable Child Tax Credit.

Wealth for retirement:

- An employer-provided contribution to a private retirement account separate and on top of Social Security.55

Support for entrepreneurs:

- Equity capital for small businesses in over-looked areas to ensure that minority- and women-owned businesses can thrive.56

- More lending to small businesses by quadrupling the cap on SBA 7a loans, lower fees for businesses, and increase guarantee amounts.57

- Permanent access to unemployment insurance benefits for entrepreneurs.

Worker protections:

- A minimum package of benefits for gig workers, including health care, retirement, paid leave, and disability insurance.

- An easier path for employees to collectively bargain, get overtime salary, have fair scheduling protections, get paid leave, and not be constrained by noncompete agreements.

- More support for formerly incarcerated individuals to access quality employment.

Access to skills throughout a career:

- Access to apprenticeships for anyone that wants one with state institutes that link employers, training providers, and workers.58

- An expansion of unemployment insurance to include training vouchers in addition to income support for the unemployed.

- More generous Pell Grants and expanded eligibility to DREAMers, incarcerated individuals, and more.

- An expansion of high-quality workforce training programs that are accessible to everyone and responsive to employer hiring and skill needs.

Support during economic downturns:

- An Emergency Payroll Subsidy that helps employers keep workers on the payroll during recessions.59

- Higher unemployment insurance benefits and a modernized registration system to make it easier for individuals to get support.

Conclusion

The COVID-19 pandemic exacerbated deep structural issues in our country. Notably, we have two economies in America—one that provides prosperity for too few, and another where the bond between work and a good life has broken down. And this trend is far from new. For decades, we have been using a 20th century contract on work in a vastly different 21st century economy.

It’s time for a new contract on work forged between workers, employers, and government that brings dignity back to work, gives everyone a real shot at prosperity, and addresses the racism and discrimination throughout the economy. Americans know they deserve more from work and from their government. It’s time to deliver on this promise.