Newsletter Published March 20, 2026 · 8 minute read

On the Grid: A Crude Awakening

Hi Friend!

Welcome back to On the Grid, Third Way’s bi-weekly newsletter, where we’ll recap how we’re working to deploy every clean energy technology as quickly and affordably as possible.

We’re excited to have you join us!

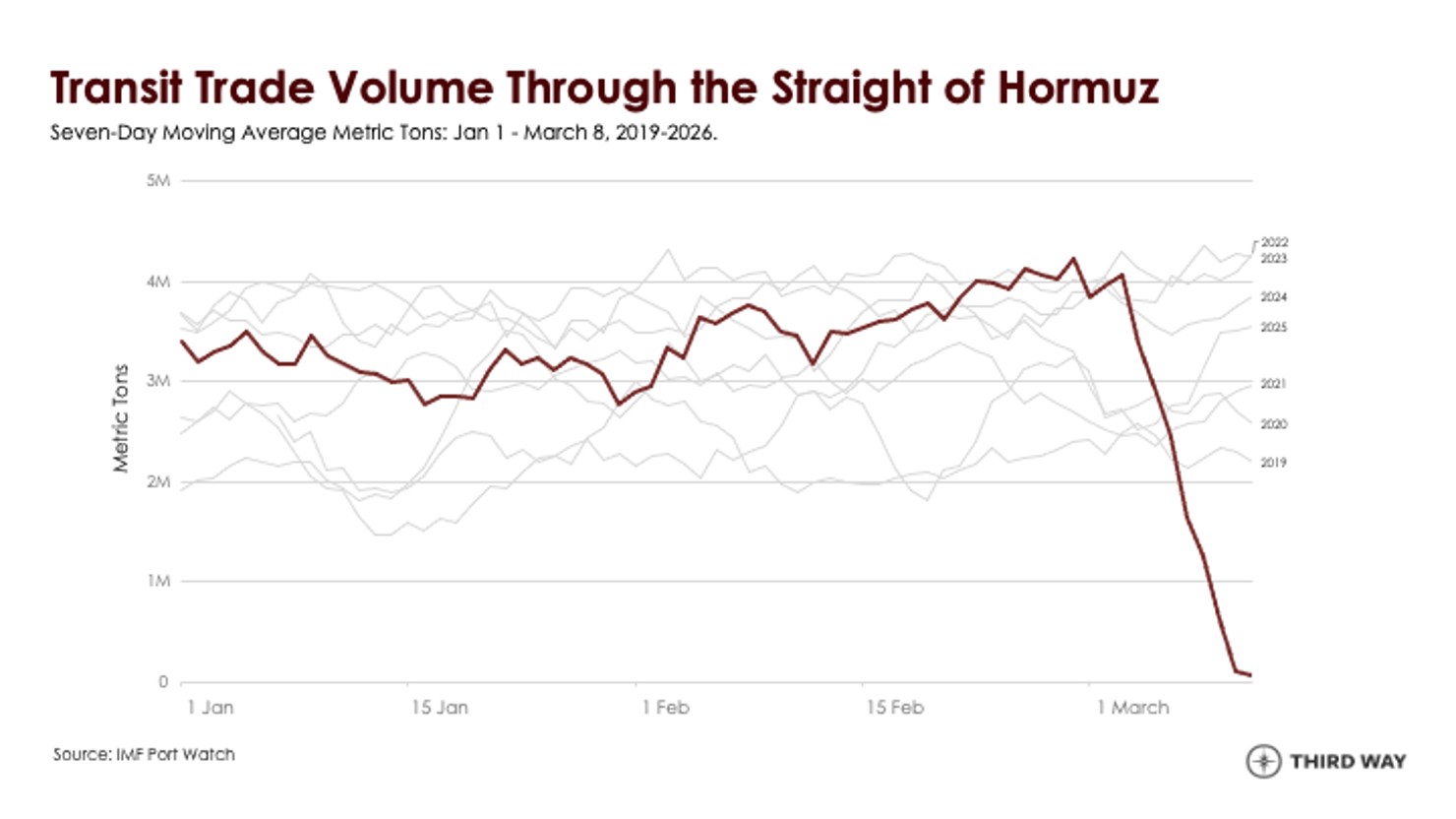

Three weeks into “Operation Epic Fury,” it’s clear the administration did not prepare for the wide-ranging impacts on energy markets. As we wrote earlier this month, the initial strikes on Iran triggered an immediate energy shock: Tehran moved to choke off the Strait of Hormuz, Qatar halted LNG production, and global markets were forced to price in a crisis with no clear trajectory.

Since then, the conflict has spread across the Persian Gulf, drawn in allied energy infrastructure, triggered a chain of retaliatory strikes, and pushed global energy markets into sustained volatility.

None of this should have been surprising. Energy infrastructure–refineries, pipelines, power systems–has always been a target in war. What is different here is where the fighting is happening.

Entering A New Era: This war is taking place inside the heart of the global energy system. The Persian Gulf accounts for more than a quarter of global seaborne oil and a fifth of global petroleum consumption, and holds the bulk of the world's spare production capacity. It’s also important to note that the type of infrastructure being drawn into the conflict is a serious escalation. Attacks on South Pars, the world's largest natural gas field, are fundamentally different from targeting infrastructure such as pipelines, export terminals, and refineries. The latter disrupts flows and can be rerouted or repaired over time, whereas attacking the production base itself threatens supply at the source and can take years to recover. Crossing that line changes how markets respond and how long disruption lasts.

The US is Poorly Prepared: A conflict in the Gulf targeting energy infrastructure carries an obvious risk, and preparing for that risk means coordinating with major producers to stabilize flows, aligning military actions with economic objectives, and maintaining the capacity to respond as markets move.

The Trump administration has made little effort to do so. Instead, the administration entered the conflict having fired the oil market advisors responsible for maintaining relationships with Gulf oil producers and foreign energy ministries, and with no visible framework for supply coordination or clearly articulated war aims to justify the risks being taken. Now, faced with tightening markets, it is turning to easing pressure on Russia as a backdoor way to manage rising prices. This is a move that is enriching Russia even as it shares intelligence with Iran to target US forces in the region and continues to wage an illegal war against Ukraine. The move has been condemned by Europe and underscores the absence of a coherent strategy. The US is even considering lifting sanctions on Iran–the country it is currently bombing.

What's Next? In a democracy, it really matters how you go to war and how you wage it. The Trump administration has utterly failed to meet this bar. It has not made its case to the public, sought approval or a declaration of war from Congress, prepared the country for a conflict that goes far beyond limited airstrikes, built sufficient alliances, or defined clear objectives and the terms for victory.

Nearly three weeks into the war, the administration has provided no visible plan for how to stabilize energy markets as escalation continues. Instead, what we see is a set of choices that, taken together, increase US exposure and raise prices for families.

What is the United States seeking to achieve? Because at the moment, there’s no end in sight, and consequences keep piling up–higher prices, tighter supply, and a more unstable global energy system. In most wars, risks are understood as the price of pursuing a goal. Here, the risks and costs are clear, but the goal is not.

Data centers have quickly become one of the most consequential forces reshaping the American economy. Driven by the explosion of AI, cloud computing, and digital services, demand for data infrastructure is surging, and hyperscalers are racing to build massive new facilities across the country. Today’s data centers are resource-intensive, requiring massive amounts of electricity, water for cooling, land, and specialized hardware. And utilities are scrambling to meet projected energy demand, fast-tracking new generation and transmission projects that will shape energy systems for decades.

How Does This Impact Energy? The growing demand from data centers is colliding with a grid that simply wasn’t built for this level of load growth. To catch up, utilities are rethinking their generation portfolios, extending the life of existing plants, and accelerating new buildouts. And when even traditionally anti-nuclear groups like the Natural Resources Defense Council signal an openness to keeping existing nuclear plants online to meet surging demand, it’s a sign of just how much the landscape is shifting.

What Do Americans Think About Data Centers? New polling from Third Way shows that a clear majority of Americans believe the rapid growth of data centers is contributing to higher electricity prices in their communities. But at the same time, Americans haven’t embraced drastic proposals to ban data centers altogether and would prefer to increase regulations on tech companies to ensure they’re paying the full cost of data center buildout, including the impact on the electric grid. Americans recognize, either implicitly or explicitly, that these facilities are part of the modern economy and are tied to broader technological leadership. They may not like data centers, but they understand the necessity.

What Comes Next? The question at hand for policymakers is how to manage data center growth–how to allocate costs fairly, protect consumers from sharp rate increases, and ensure the economic benefits are broadly shared. That means grappling with who pays for grid upgrades, how to structure rates for large energy users, and how to align data center development with long-term energy planning. Our team is continuing to closely track these dynamics.

Over the next three decades, global electricity demand is projected to exceed 54,000 TWh annually, with roughly 25,500 TWh coming from new demand alone–equivalent to adding more than six United States’ worth of power consumption. But this surge isn’t happening evenly across the world. According to new analysis from Third Way and Energy for Growth Hub, more than 70% of it is set to come from emerging and middle-income economies that are industrializing, expanding manufacturing, and building out their grids in real time.

In many of these countries, the energy systems that will support that growth are still taking shape. Governments are making decisions now about the infrastructure that will underpin economic growth for decades. And increasingly, nuclear power is entering that conversation as a practical option.

What Does That Mean For Nuclear? Today, just 27 countries operate commercial nuclear power plants, but a much larger group is moving toward deployment. Another 12 countries already have viable markets despite not yet having reactors, and an additional 10 are putting the regulatory frameworks and government capacity in place and could be ready by 2030. Over time, that number grows substantially: by 2050, as many as 99 countries could be positioned to deploy nuclear power. Just as important is where demand is concentrated. More than 85% of new electricity demand will occur in countries that are either already “ready” for nuclear energy or could be ready within the next decade. The fastest-growing electricity markets are also becoming viable nuclear markets.

That combination drives the scale of the opportunity. Under baseline assumptions, nuclear could supply thousands of terawatt-hours of new electricity demand by 2050, corresponding to a market worth roughly $380 billion annually. And if nuclear plays a larger role in replacing coal or meeting new demand from electrification, that market is likely even bigger.

What We’re Doing: This is not a typical commodity market. Nuclear projects involve long timelines, large capital investments, and decades-long relationships around fuel supply, operations, and maintenance. And countries entering the nuclear market for the first time are looking for partners that can deliver on financing, construction, fuel supply, and long-term support. While the US may have world-class nuclear technology, right now, Russia and China are better positioned to meet this emerging demand. Operating state-backed models that package these elements together and lowering the barrier to entry for countries interested in nuclear, Russia and China hold an advantage in a market where relationships are locked in for decades.

If the United States wants to compete, it will need to approach nuclear exports as a strategic priority. That means coordinating across agencies, strengthening export financing, and working with allies to offer credible, full-service alternatives to state-backed competitors. In the global nuclear race, leadership will go to the countries that can deliver projects, not just propose them. The demand is growing, and countries are looking to build. The question is whether the United States is prepared to compete for that market or cede it to others.

- Tim Levin, in The Atlantic, argues that the Iran war’s impact on gas prices has renewed interest in electric vehicles as a hedge against fuel volatility and suggests that Americans are unlikely to adopt EVs for environmental reasons, rather than a kind of insurance policy against geopolitical instability.

- Rhodium Group and MIT’s Clean Investment Monitor expand from a US focus to a global one, highlighting how governments in the US, China, and Europe are using subsidies and industrial policy to build domestic clean energy industries.

- Daniel Sternoff, on Columbia’s Energy Exchange podcast, talks with Anne-Sophie Corbeau, research scholar at the Center on Global Energy Policy, about the impacts of the war in Iran on global energy security.