Report Published September 5, 2023 · 15 minute read

Shock Therapy: How to Treat Out-of-Control Hospital Prices through Collective Negotiation

David Kendall, Jacqueline Garry Lampert, & Darbin Wofford

Takeaways

Hospitals are charging private health plans more than twice as much as Medicare. Out-of-control hospital prices are part of a vicious cycle where hospital consolidation drives up prices and subverts the competition needed to keep costs in check. In turn, higher costs undermine the adequacy of Medicare payments to hospitals, which leads more hospitals to consolidate. To stop this, policy makers should enable states, employers, unions, and health plans to negotiate in large groups in areas where prices are out of control. Congress should direct the Federal Trade Commission to set up the terms for collective negotiation to counteract the forces that have driven hospital consolidation to unsustainable levels.

To understand the depth of the problems with health care, look no further than the stunning prices private health plans pay to hospitals. A recent study found that insurers paid more than two times Medicare rates for hospital care in 2020.1 In South Carolina, West Virginia, Florida, Wisconsin, and Wyoming it was three times Medicare rates.2 Northbay Hospital Group in Fairfield, CA charged 13 times more than Medicare for outpatient care.3

Hospital prices paid by private health plans are out of control. Consolidation in hospital markets has driven up prices and made hospitals less competitive. Without competition, hospitals’ costs have also risen. Higher costs are why hospitals lose money on Medicare, not because Medicare rates are insufficient. Their push to cover these higher costs through higher prices also increases the cost of taxpayer support for private health insurance plans. Hospitals have succeeded by manipulating the fee-for-service payment system, which doesn’t hold them accountable for the cost and quality of care.4

Below, we explain five key problems with hospital prices:

- Consolidation is driving up prices.

- Declining competition subverts cost control.

- Higher costs undermine the adequacy of Medicare payments.

- Hospitals’ pursuit of high prices drains tax dollars through higher industry subsidies.

- Fee-for-service is a flawed payment scheme.

We then propose a form of shock therapy to treat these deeply entrenched problems all at once by letting states, private employers, unions that provide health benefits, and health plans negotiate lower prices collectively. It would offer private payers the chance to deal with the problem of high prices directly and avoid the need for the government to publicly negotiate prices.

This report is part of a series called Fixing America’s Broken Hospitals, which seeks to explore and modernize a foundation of our health care system. A raft of structural issues, including lack of competition, misaligned incentives, and outdated safety net policies, have led to unsustainable practices. The result is too many instances of hospitals charging unchecked prices, using questionable billing and aggressive debt collection practices, abusing public programs, and failing to identify and serve community needs. Our work will shed light on issues facing hospitals and advance proposals so they can have a financially and socially sustainable future.

Problem 1: Consolidation is driving up hospital prices.

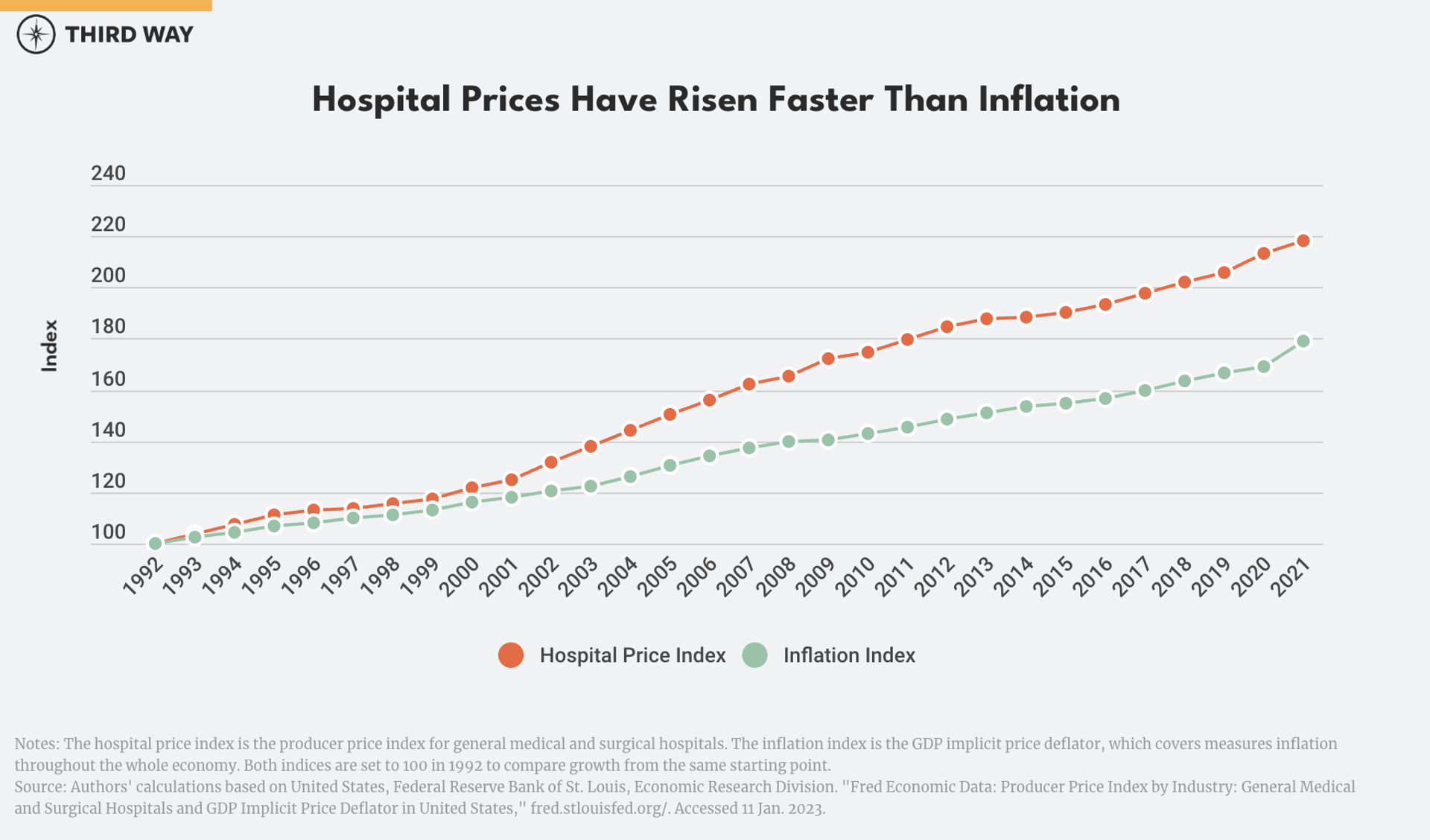

Hospital prices have risen faster than inflation in 25 of the last 30 years.5 A $10,000 hospital procedure in 1992 would cost $4,ooo more today after adjusting for inflation.

And hospital price inflation has been even worse for people with private insurance, including employment-based coverage. One study found that prices for inpatient care at hospitals increased twice as much for private insurance compared to Medicare and Medicaid from the middle of 2014 through the first quarter of 2018.6 The average cost of a standard stay in a hospital was $19,975 for private insurance compared to $11,868 for Medicare and $9,071 for Medicaid in 2015.7 That’s consistent with research from RAND that private health plans paid over two times more than Medicare rates for inpatient and outpatient hospital care in 2020.8

Hospital consolidation has gone hand in hand with rising prices. In 1970, 90% of hospitals were independent, community-based institutions; today only one-third are independent.9 Mergers and acquisitions have created ever larger health care systems. The 10 largest systems now control 24% of the hospital market.10 Smaller chains account for most of the rest. Economists have found that four of five hospital markets are highly concentrated based on federal antitrust standards.11

For people with employment-based coverage, hospital prices are 8.3% higher on average in markets with one to three hospitals compared to markets with four or more hospitals.

Consolidation is driving up prices.12 For people with employment-based coverage, hospital prices are 8.3% higher on average in markets with one to three hospitals compared to markets with four or more hospitals.13 Those higher prices afflict half the country. High prices are a problem in unconsolidated markets, too.14 Billing abuses, anticompetitive business practices, and the lack of accountability for health outcomes and costs contribute to the problem.

Problem 2: Hospital consolidation subverts cost control.

In a market economy, competition keeps costs in check. But hospitals have used consolidation and other tactics to avoid competition in private insurance markets where, unlike Medicare, their prices are not regulated. As a result, hospitals’ costs go up because they are unchecked.15

Hospitals claim that consolidation lowers costs.16 Indeed, other types of businesses can spread out overhead costs as they scale up. But just the opposite occurs with hospitals because of the lack of competition. Independent analysis has shown that costs go down only for mergers that cut across regions.17 Hospital mergers within a consolidated market do not drive down costs. Specific costs like operating margins for non-profit hospitals and administrative overhead go up in consolidated markets (as indicated by how much hospitals charge private payers above Medicare prices).18 In contrast, spending for patient care does not rise by as much in those cases. Hospitals have so much market power that they typically charge private payers 50% above their costs.19

Specific costs like operating margins for non-profit hospitals and administrative overhead go up in consolidated markets.

Despite decades of consolidation, the cost of hospital overhead has not budged. From 1996 to 2018, overhead (which includes administration and capital investment) remained at just under half of total costs.20 Other costs are rising like labor and supplies because of inflation, but consolidation has diminished hospitals’ incentive to find creative ways to handle the increases. Other factors in hospitals’ budgets also vary. For example, a recent drop in investment income explains why many hospitals have slim margins right now.21

Problem 3: Higher costs undermine the adequacy of Medicare payments.

Many hospitals make money on Medicare despite claims to the contrary.22 When they face pressure on their prices from private payers, they get lean by finding ways to be more efficient. That means they lower their costs to the point where they can make money from Medicare (whose rates are typically lower than private payers’ rates). When consolidation eliminates financial pressure and increases their market power, hospitals can charge private payers more and the extra revenue goes into higher costs or profits. The median hospital in the United States would break even if they were paid Medicare rates based on their current expenses.23 More would make money on Medicare with competitive pressure to keep expenses in check.

Here's how the Medicare Payment Advisory Commission (known as MedPAC) explains it:

“We find that costs do vary in response to financial pressure and that low margins on Medicare patients can result from a high cost structure that has developed in reaction to high private-payer rates. In other words, when providers (particularly nonprofit providers) receive high payment rates from insurers, they face less pressure to keep their costs low, and so, all other things being equal, their Medicare margins are low because their costs are high.”24

“All other things being equal, [hospitals’] Medicare margins are low because their costs are high.” – MedPAC

Each year, MedPAC identifies a group of “relatively efficient hospitals,” which have lower than average costs and meet a threshold standard for quality of care. In the most recent data available from 2021, this group had a 1% margin (profit) on Medicare payments (including COVID relief funds).25 Over the last ten years, the median efficient hospital has broken even on Medicare while having a 7% margin overall compared to all other hospitals, which have lost 7% on Medicare with a 6% margin on all their care.26 In other words, efficient hospitals with higher margins on Medicare also have higher margins overall. Other research shows that efficiency is the key to improving margins, which is within every hospital’s reach by using well established quality improvements methods like Six Sigma.27

Problem 4: Hospitals’ pursuit of high prices drains tax dollars through higher industry subsidies.

When hospitals increase their prices, insurers increase premium prices or reduce coverage to cover their costs and make a profit.28 Even employers that fund their own insurance plans aren’t safe. When employers and insurers cannot negotiate lower prices for health care providers, they pass higher prices on to employees in the form of higher premiums, higher deductibles, and less generous benefits overall. These high health costs fall disproportionately on Black and Hispanic adults, people with lower incomes, and those without insurance.29

Taxpayers also take a hit from higher premiums for private health plans. Higher premiums increase federal spending on ACA tax credits and reduce federal revenue due to the tax exclusion for employer-sponsored health insurance.30 The Congressional Budget Office has estimated that lowering prices for hospital and physician services by 1% would save the federal government $4.8 billion in 2032.31 Lowering prices by 8% in concentrated markets (with only one to three hospitals) would save as much as $19 billion in 2023 (assuming similar price reductions for physician services).32

In addition, the recent ban on surprise billing is less effective because of high commercial prices driven up by hospital consolidation. The No Surprises Act seeks to protect patients from surprise bills generated when patients unwittingly receive care from an out-of-network provider at an in-network facility. It does this by, among other things, creating a dispute resolution process to help providers and insurers reach agreement on the price of the services.33 A key component of the process involves determining the median in-network rate as of January 31, 2019 for the service and increasing it by the rate of inflation each year (using the consumer price index for all urban consumers, CPI-U). Pegging the 2019 price to inflation should slow the rate of price increases over time. However, this policy also locks in high prices in consolidated markets and potentially squeezes the remaining markets where prices might have been low in 2019.

Problem 5: Fee-for-service is a flawed payment scheme.

While hospital consolidation has weakened competition, it wasn’t that strong to begin with. That’s because the payment system for hospitals and physicians is fundamentally flawed.

That current payment model is fee-for-service. That means health care providers get paid separately for each service or product with no one in charge of patient outcomes or total cost. Despite efforts to move toward paying for the quality of a service rather than the quantity, fee-for-service still accounts for 62% of total health care dollars.34 The majority of hospitals and health systems see more than half of their revenue come from fee-for-service payments.35

Fee-for-service payments distort patient care and drive up health care prices.36 Fee-for-service billing occurs on a piecemeal basis, with more than 10,000 individual items or services for which providers can bill. Health care purchasers can’t know in advance exactly how they will be billed, so they have little chance to compare provider price and quality to make meaningful choices.

As a result, hospitals do not have a sustainable business model. In this distorted system, providers can seek more revenue by increasing the price of each service. To do that, providers need leverage to charge higher prices. That is why mergers and other paths to market dominance have become critical to hospitals’ survival and show no signs of letting up.37 Moreover, during the Covid pandemic, hospitals were at the mercy of federal financial support because patients couldn’t come to the hospital. In contrast, revenue for providers, like Accountable Care Organizations, was more stable during Covid because their payments depended on the number of people they take care of each year, not the volume of services they deliver.38 The fee-for-service payment system is simply not sustainable.

The Solution: Collective Negotiation

Each of the problems above would benefit from specific policy changes as Third Way and others have proposed.39 One solution, however, would build on and encompass them all: collective negotiation.

Currently, antitrust law restricts employers and health plans from coordinating their purchasing strategies. That’s because in a normal functioning market, a large, single buyer dominating the purchase of all the goods in a market (called a monopsony) is as much an economic no-no as a monopoly. But the hospital market is not functioning as a normal market; it has major failures as noted above. It needs a shock to the system.

That’s why the federal government should empower states and the people who are paying the hospital bills across the country to act collectively and take on hospital prices. Like collective bargaining for workers, where individuals band together to negotiate with employers using exemptions from antitrust law, collective negotiations would give private and public employers, unions, and health plans a haven from antitrust law to work together and negotiate as a large group with hospitals that charge high prices. In regions where insurers already constitute a large negotiating block, prices are 5% to 19% lower.40 Here is how Congress can authorize collective negotiation:

First, empower states to deploy collective negotiations as a tool to fight hospital prices. A recent transparency rule requires hospitals to disclose their prices for services paid by employers, unions, and health plans. That information allows everyone to see which hospital services have the highest prices. Although reporting is improving, many hospitals are not yet fully compliant. Until hospitals report their prices as required, they should be automatically subject to collective negotiation. States would have the first shot at authorizing and overseeing collective negotiations for those hospitals that have not fully disclosed their prices and for hospitals with high prices as disclosed under the transparency rule. They can bring a substantial block of business to the table with Medicaid and a purchasing pool that combines state and local government employees, as more than half of states have done.41

State-based collective negotiation would also address the ways some states have allowed hospitals to use certificate of public advantage laws to skirt federal anti-trust review.42 Congress should give the FTC authority to require states with a certificate of public advantage law to deploy collective negotiations as a counterbalance to state-approved mergers or ban them outright. To enable state action, the FTC should set the terms for collective negotiation, like standards for triggering when collective negotiations should start and end, and guardrails to prevent prices and quality measures from falling below national benchmarks (regionally adjusted) or decreasing competition.

Second, let the FTC establish collective negotiations across states. If a state does not act or if market consolidation extends across state lines, the FTC should authorize and oversee collective negotiation directly with employers, unions, and health plans. Payers would petition the FTC to collectively negotiate in areas or sets of services with high prices as the FTC identifies. Such authority would expire after prices fell and new forms of competition like value-based payments took hold. The FTC would also ensure that savings from lower prices are passed through to consumers in equitable ways and that collective negotiation would not threaten access or quality of care.

Given the complexity and novelty of collective negotiations, the FTC would likely want to conduct some test cases before scaling it up fully. But ultimately, this new tool would allow the FTC to fight existing hospital monopolies and consolidation without having to use the cumbersome process of undoing mergers.

Third, create a permanent exemption for collective negotiations on value-based contracts. While a focus on prices is critical, a long-term solution also needs to focus on the outcomes of health care delivery. That’s where value-based contracts come into play. They hold providers accountable for the quality and quantity of care for a given price, which is overall value. Such value-based payments include accountable care organization payments in Medicare and capitated payments from private health plans. But having incomplete data or ineffective metrics for the value of care can be a barrier to their adoption.43 That’s why purchasers need to coordinate on the terms for value-based contracts without running afoul of anti-trust rules. This exemption would be permanent because it does not risk price-setting by purchasers.

Hospitals need a strong push away from high-priced, fee-for-service health care and towards organizations that are accountable for the total cost of care and patients’ outcomes.

Fourth, set a back-up plan if collective negotiation fails. If employers, unions, or health plans do not step up to collectively negotiate, then Congress should tap the Administration to publicly negotiate. The Administration would conduct negotiations regionally, leaving in place any private collective negotiations that were successful at the local level. If hospital prices in a region exceeded a percentage of Medicare prices (e.g., 200%), then the Department of Health and Human Services would negotiate a limit on fee-for-service, out-of-network prices. This would have the effect of capping what hospitals could charge patients and private health plans as they set their preferred provider lists. This cap would not, however, directly affect price negotiations over value-based payments other than to focus competition on comprehensive care instead of the piecemeal care delivered under fee-for-service.

Conclusion

Collective negotiation by purchasers can be an effective tool in dealing with local market conditions. Health care consolidation varies across and within states, as does pricing. Even a backup federal plan for price negotiations will have to address the variation in local markets. Collective negotiation can also support ideologically diverse approaches to health care costs. It can enhance the efforts of left-leaning states such as Massachusetts and Rhode Island, which have programs to limit prices across public and private payers.44 Similarly, association health plans, often favored by right-leaning advocates, could be vehicles for organizing collective negotiations across state line.45

Hospitals need a strong push away from high-priced, fee-for-service health care and towards organizations that are accountable for the total cost of care and patients’ outcomes. A new business model would give them a predictable revenue stream and incentives to hold down costs and improve quality—just like the competitive forces that shape the rest of the economy.