Report Published December 19, 2022 · 14 minute read

Chronic Care Cost Cap

Nicole Tapay, David Kendall, & Ladan Ahmadi

Takeaways

People with chronic health conditions often face a lengthy struggle to afford the care they need. Too often, they can be devasted financially despite having health care coverage. To change this, people with chronic conditions should have a health care cost cap based on a percentage of their income. This would provide meaningful relief from out-of-pocket (OOP) expenses for those individuals and families who pay a particularly high share of their income on health care costs for more than one year in a row. And it would be targeted at low- and middle-income individuals and families.

In a story far too common in America, millions of patients suffer financially because of health care costs.1 Within two months of getting an alarming mammogram, a woman can be billed $8,150 to cover the costs of related diagnostic tests.2 Her health plan would cover all the costs of treatment for breast cancer after these tests because she already paid for expenses up to her out-of-pocket maximum. But in the following year, she will have to pay that same amount again for ongoing treatment and testing. With a typical income of $42,000, she will spend 1/5 of her income on health care two years in a row.3 Her savings will be gone, and she will be in debt. One more year of high costs will likely push her into bankruptcy.

She is not alone. People with cancer, HIV-AIDS, and numerous other chronic and some non-chronic conditions often face a lengthy struggle to afford the care they need to stay healthy and live as normal a life as possible. Tragically, some give up on their care because they cannot afford it. In a poll looking at how health care costs affect Americans’ medical decisions and personal finances, 44% reported not going to a doctor when sick or injured and 32% said they did not fill a prescription or took less than the prescribed dose of medicine because of costs.4 They can also face high costs year after year. Ten million working age adults in the United States have a family that spends more than 5% of their household income on medical bills for two years in a row.5

While the Affordable Care Act increased coverage and reduced out-of-pocket costs for millions through a cap on these costs, the job is not done.6 In the Inflation Reduction Act, Congress extended the cap on everyone’s premiums in the health insurance exchanges at 8.5% of their income or less through 2025. It also capped insulin costs at $35 per month and all drug costs at $2,000 annually for Medicare beneficiaries. The next step is to expand protections for out-of-pocket costs, especially for individuals who face high health care costs for multiple years in a row regardless of their chronic conditions. In this report, we explore the financial challenge people with chronic and other conditions face and propose a chronic care cost cap to solve it.

The Problem: High Costs not Covered by Insurance

The number of Americans exposed to unlimited health care costs has fallen significantly since the implementation of the Affordable Care Act. Those without coverage decreased from 45 million in 2013 to 28 million in 2020.7 The ACA and the Inflation Reduction Act also cap premium costs for people who buy their own coverage on the ACA exchanges with a premium tax credit, limiting premiums to 8.5% of income, or less at lower income levels.8 The ACA further caps out-of-pocket (OOP) costs for all by requiring health plans to set a maximum annual limit.9 The ACA also provides for coverage of much of the deductible, copayments, and other out-of-pocket costs for those with incomes between 100% and 250% of poverty under a program called cost-sharing reduction.10

Yet, even with that substantial progress, people with chronic conditions and others continue to face a huge burden from health care costs. Contributing to this are three separate problems:

Problem #1: Deductibles and out-of-pocket costs are rising.

Increasing deductibles and OOP costs are leaving more and more people underinsured, which means they have insurance but without enough financial protection for their health needs. According to the Commonwealth Fund, 29% of the insured were underinsured in 2018, up from 12% in 2003.11 That is partly because the burden of deductibles for covered workers has increased by 111% in the last 10 years, which reflects both the increased use of deductibles and the growth in their average size.12

Most insurance policies require patients to pay a portion of their expenses until they reach a pre-set, specified dollar amount, which is the out-of-pocket maximum or cap. The ACA out-of-pocket maximum improved protection for many. Only 82% of those with single employer coverage had a cap in 2010, compared to 100% in 2020, according to one national survey.13

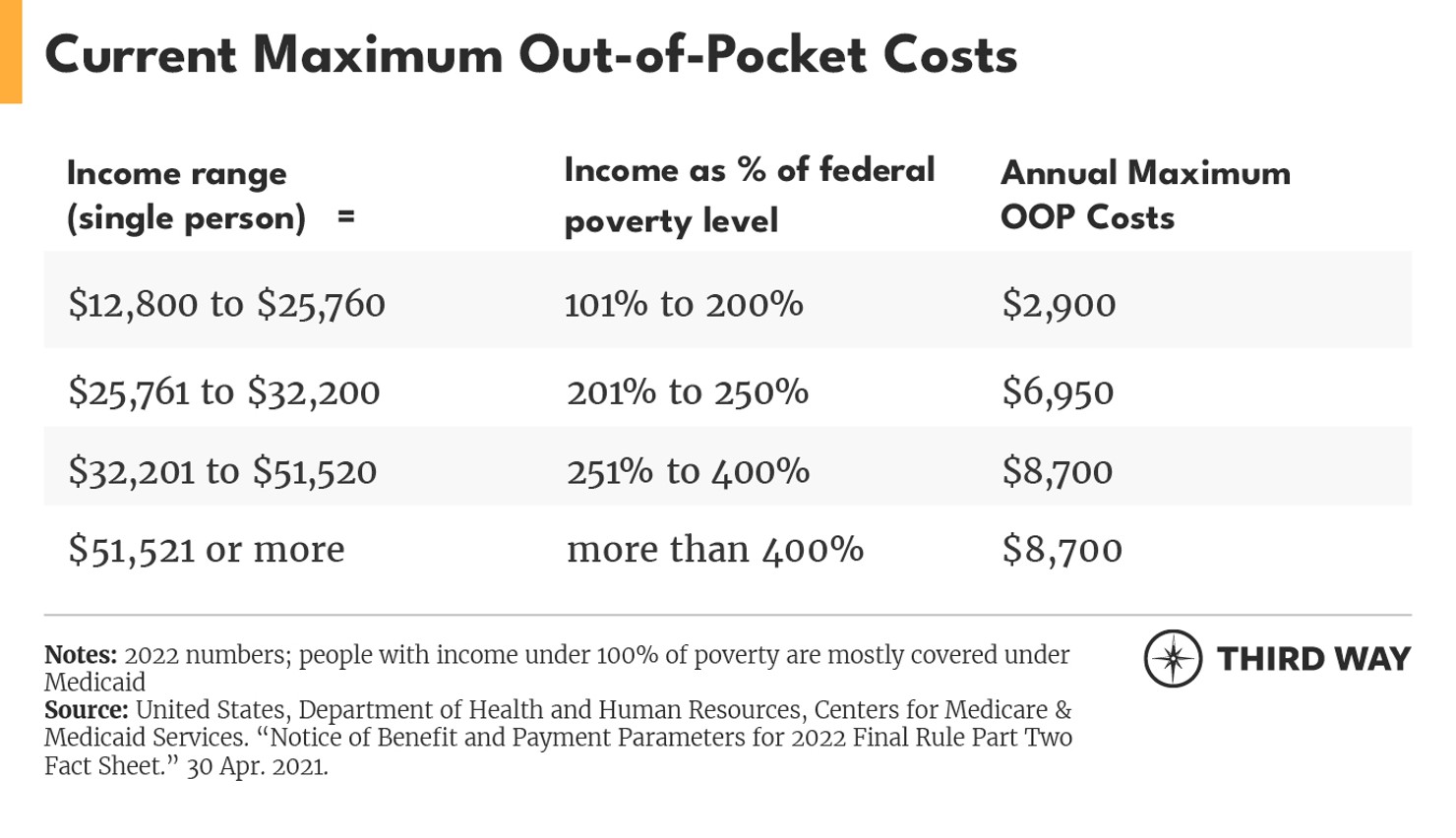

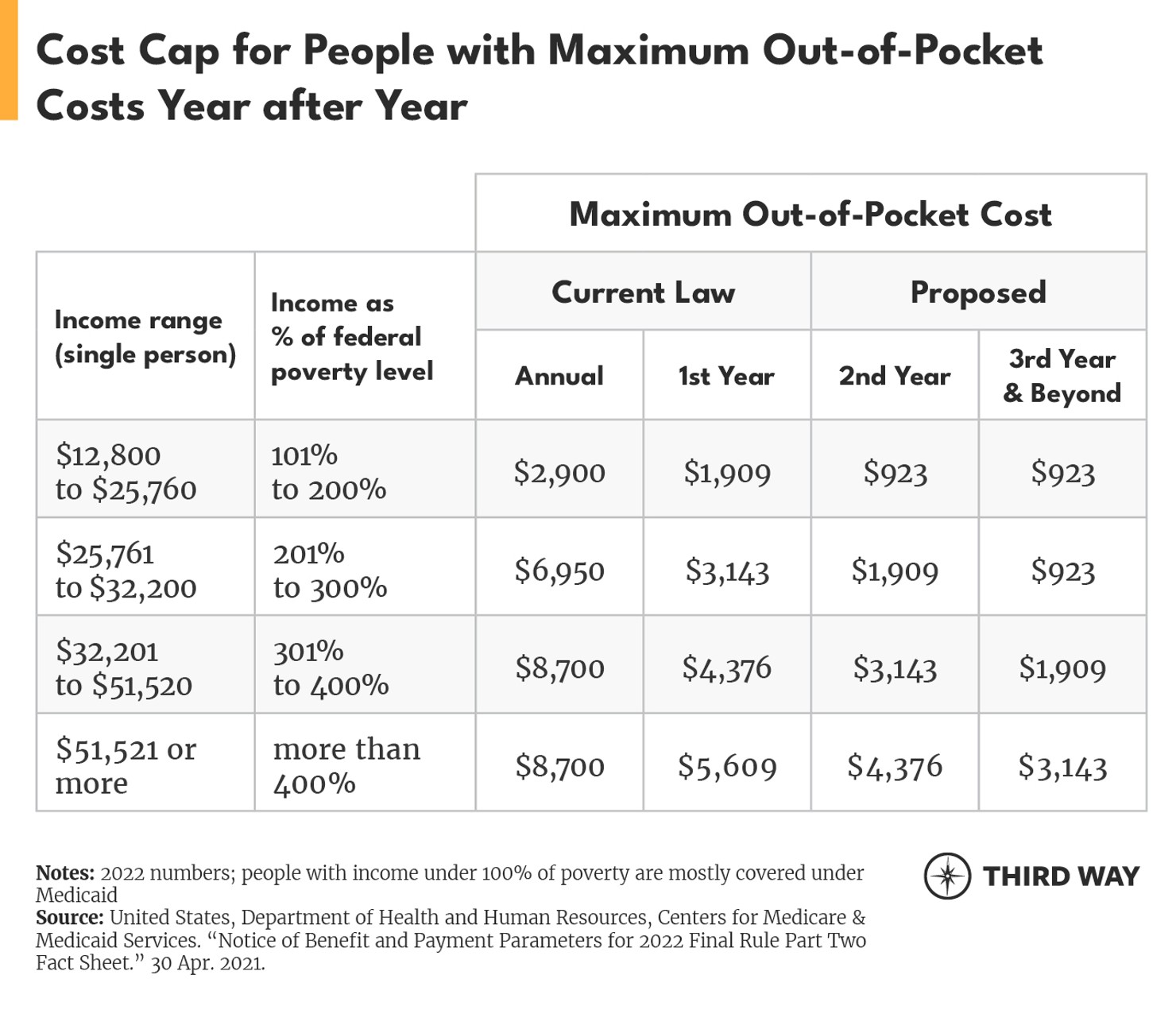

However, out-of-pocket maximums are often still too high for many people as shown in the chart below. 14 Current annual out-of-pocket maximums for 2022 cap expenses at $8,700 for an individual and $17,400 for two or more people. For those eligible for cost-sharing reductions (available to lower-income individuals and families in exchange-based health plans), the OOP maximum cannot exceed $2,900-$6,950 for an individual, or $5,800-$13,900 for a family, depending on income.15 That means those at 100% of poverty must sometimes spend 23% of their income on OOP costs in one year and those above 20o% FPL must spend as much as 27%.

Members of Congress, led by Senator Jeanne Shaheen, have introduced legislation to lower those OOP cost caps.16 But a big coverage gap would remain. The caps are triggered annually and reset at the beginning of each policy year, leaving patients vulnerable to repeated cycles of high health care costs.

Some employer and individual policies have more generous coverage than plans with the relatively high OOP limits allowed under the ACA.17 Nonetheless, with the variation in enrollee financial liability in both the individual and employer markets, high OOP limits is making the underinsurance problem worse.

Problem #2: Out-of-pocket costs hit a small number of people disproportionately.

Insufficient insurance coverage is an even bigger problem for those with ongoing health care needs that recur year after year, which the annual OOP maximums do not address. In 2016, 5% of the population accounted for half of all health care spending. Out-of-pocket spending is similarly concentrated, with just over 1% of the population accounting for nearly 21% of out-of-pocket spending and 49% of out-of-pocket spending attributable to the top 5% of spenders.18

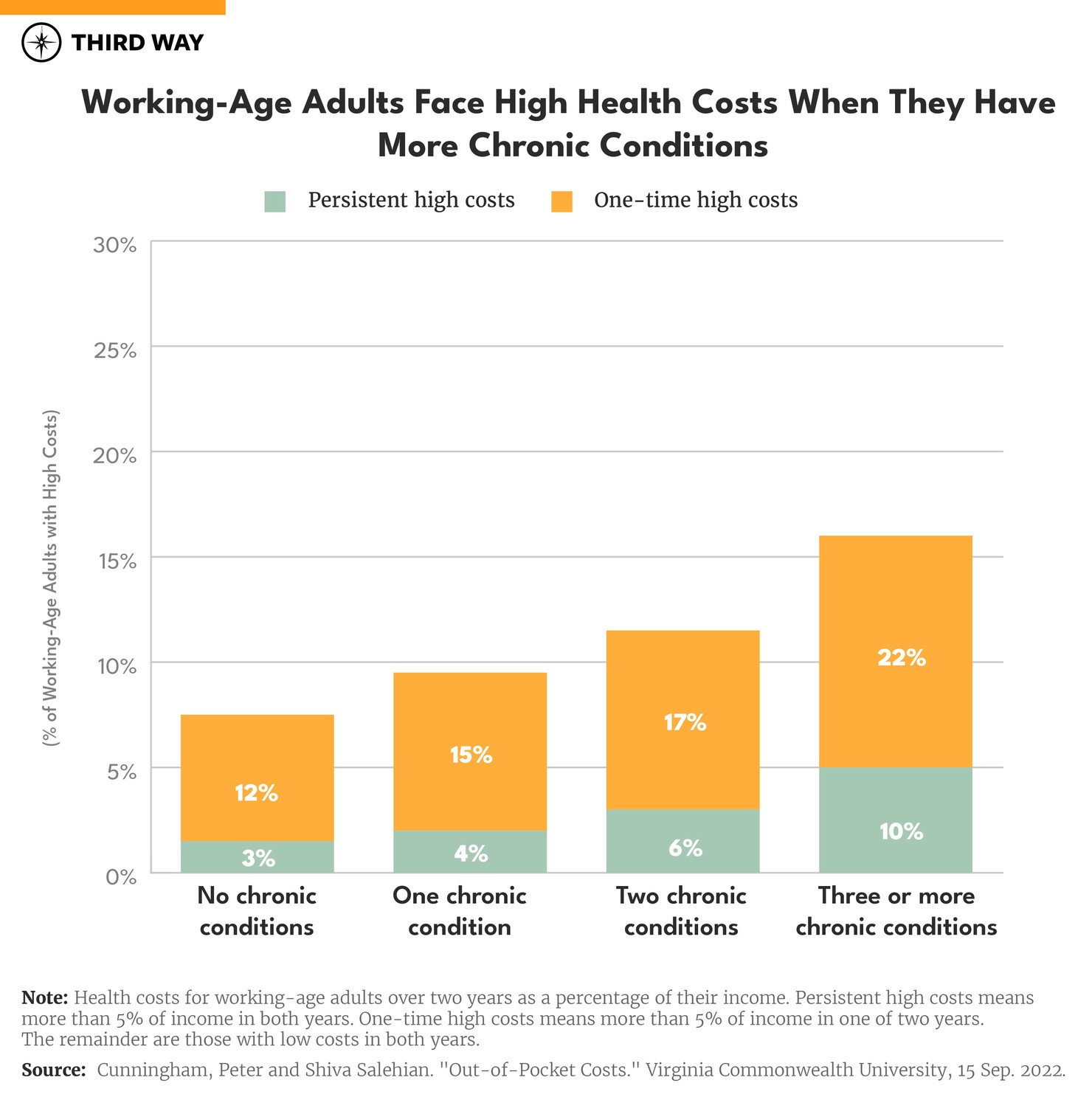

Annual OOP limits are not designed to protect people with a chronic condition. Among working-age adults without a chronic condition, 3% will have persistent high OOP costs, but for those with three or more chronic conditions, the portion with persistent high costs more than triples to 10% as show in the chart below.19 Persistent high OOP costs are those that exceed 5% of a person’s income for two years in a row. This problem of persistent high OOP costs affects 5% of working-age adults.20 Persistent high costs are particularly likely for people with heart disease, cancer, diabetes, cerebrovascular disease, osteoarthritis, and endocrine disorders.21

For an even smaller subset of the population, costs are even higher. The average annual spending for 1% of people in employer coverage with very high costs for three consecutive years (2015-2017) was $88,000. Certain conditions, including HIV, cystic fibrosis, multiple sclerosis, rheumatoid arthritis, and leukemia, increased the odds of persistently high health spending.22 Those patients likely faced high OOP costs due to their health condition.

Problem #3: High out-of-pocket costs cause financial toxicity and limit access to care.

The term “financial toxicity,” or financial distress, describes how out-of-pocket expenses can create financial distress for patients.23 Cancer patients confront particular challenges in this area. They have a higher risk of financial toxicity and adverse effects due to high out-of-pocket health care costs when compared with patients with many other chronic diseases. For cancer patients, high out-of-pocket costs are associated with financial hardship, negative clinical outcomes, lower health-related quality of life, and reduced treatment adherence.24 They also face financial costs that go beyond health care coverage like long-term care expenses and the loss of income due to illness.

For cancer patients, high out-of-pocket costs are associated with financial hardship, negative clinical outcomes, lower health-related quality of life, and reduced treatment adherence.

The risk of financial toxicity goes beyond those with cancer. People with a wide range of chronic conditions are affected. For example, 70% of people with more than $1,000 in out-of-pocket spending on drugs in large employer plans have an endocrine disorder like diabetes or obesity.25 Other chronic conditions associated with high OOP drug spending include musculoskeletal disorders and circulatory conditions.26 Just having to meet a high deductible at the beginning of the year can be a big impediment for patients. That problem has led to proposals to smooth out deductible payments throughout the year.27

Out-of-pocket costs can also impose a larger burden depending on income. A Commonwealth Fund study found that 10.3 million working-age adults and children—6.8% of those in nonelderly households with employer coverage—had high out-of-pocket costs relative to income. This study considered spending to be “high” if it accounted for 10% or more of household income, or 5% or more for households below 200% of the federal poverty level.28

While higher deductibles and OOP payments have curbed some unneeded care by making patients more cost conscious, they have also caused patients to cut back on needed care, often in irrational ways.29 A study of the impact of cost-sharing on some patients in the Medicare prescription drug program found that small increases in cost led patients to cut back on highly beneficial drugs, ultimately leading to more deaths.30 For prescription drugs, nearly one-in-ten adults reported delaying or forgoing a prescription due to costs and 26% of those taking prescription drugs reported difficulty affording their medications.31 One percent of those under age 65 spent $5,000 per year or more on out-of-pocket health care costs in 2017.32

The Solution: A Chronic Care Cost Cap

People faced with chronic conditions should be protected with a health care cost cap that limits their exposure to costs based on a percentage of their income. This would provide relief from expenses for those individuals and families who pay a particularly high share of their income on out-of-pocket health care costs for more than one year in a row. And it would be targeted at low- and middle-income individuals and families using the tiers of protection established in the ACA.

Here is how a chronic care cost cap would work:

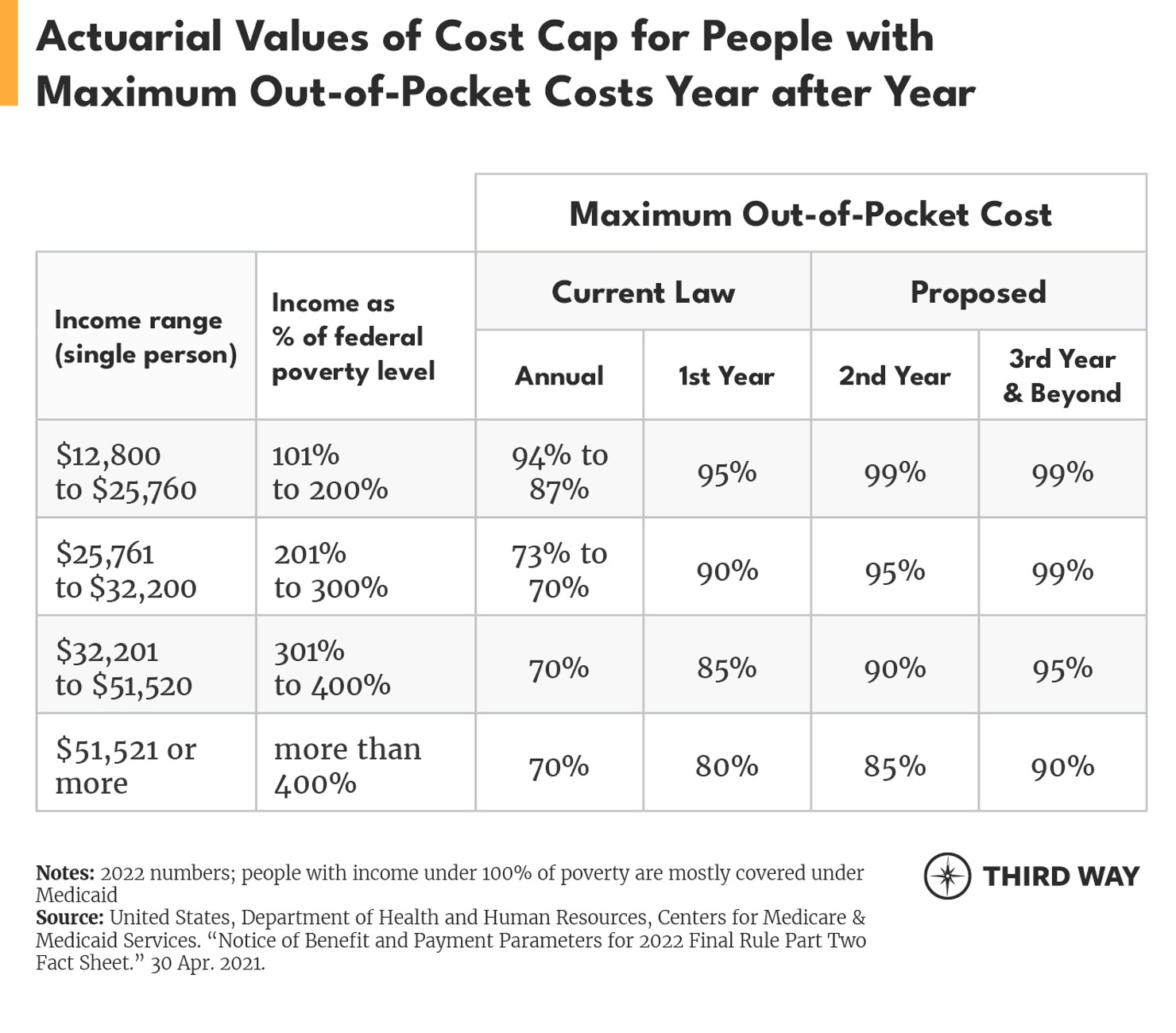

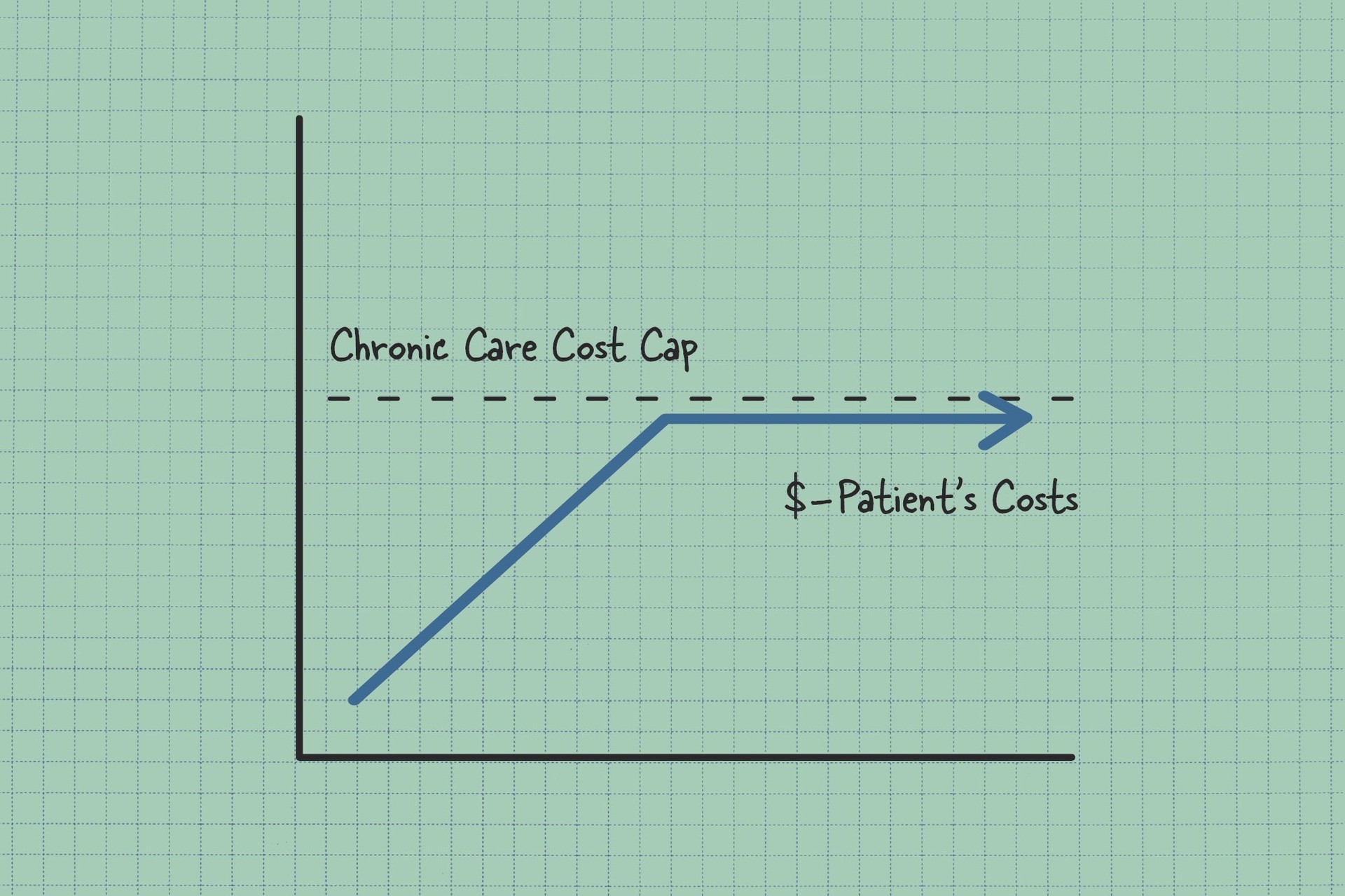

- The chronic care cost cap would kick in the year after a patient with a chronic condition hits their OOP maximum.

- OOP maximums would gradually decrease for three years before leveling off at the lower rate. These would phase down differently depending on income, as shown below.

- The insured would always have to pay at least 1% of the average cost of care covered by their health plan in any year regardless of how much protection they receive.

For example, a person with high costs year after year and an income of $38,400 would have a maximum OOP limit of $3,143 in the first year and then $1,909 in the second year, which is 5% of their income. In the third and following years, the maximum would be $923, which is 2% of their income. See appendix for more details.

To protect people with chronic conditions and make this cap a reality, Congress would need to take five steps:

- Improve existing ACA caps. Congress should improve the existing cost caps under the ACA for out-of-pocket costs in a single year.33 The Shaheen legislation would change the standard plan used for determining the level of financial protection from a silver plan, which covers 70% of costs, to a gold plan, which covers 80% of costs. That change would reduce OOP costs significantly for most people purchasing coverage through the exchanges according to a study by the Urban Institute.34

- Boost eligibility. Congress should extend eligibility for cost-sharing reductions to individuals who reach their out-of-pocket maximum (not counting premium payments or out-of-network expenses). Individuals would indicate their eligibility on their application for coverage through the exchanges. To verify eligibility, health plans would indicate on the IRS Form 1095-B for health coverage if one of their enrollees reached the out-of-pocket maximum. Initially, the tax credit would be available to health plans offering coverage through the exchanges. Extending the tax credit to employer-based coverage would be contingent on first creating a cost cap for employer-based coverage as Third Way has previously proposed.35 The tax credit could be limited to only those with specific conditions to limit the federal cost of the tax credit, but even some people with only an acute condition, like a major injury, can face two or more years of high OOP costs.

- Provide direct funding for the chronic care cost cap. Current federal funding for cost-sharing reductions is provided indirectly through health plans that raise the premiums for silver plans to cover the costs, a process known as silver loading.36 The chronic care cost cap should be provided explicitly like most other tax credits. It should also be advanceable and refundable like the premium tax credits under the ACA.

- Promote value-based insurance design. Cost-sharing requirements can often present an obstacle for patients to get the care they need. An innovative way to design coverage involves lowering or eliminating cost-sharing to improve patients’ health or save money in the long-term by preventing a chronic disease from getting out of control. For example, Congresswomen Lauren Underwood has proposed eliminating cost-sharing for many chronic care services.37 At the same time, the Center for Medicare and Medicaid Innovation is in the middle of an eight-year effort to test value-based insurance design.38 To build off both those efforts, Congress could take an important step by establishing a permanent, independent evaluation of the health and economic benefits of lowering or eliminating cost-sharing for chronic care. It could work like the United States Preventive Care Task Force whose ratings of preventive care services with an “A” or “B” causes those services to be covered for free in most health plans.

- Update risk adjustment. Congress should mandate that the US Department of Health & Human Services (HHS) not penalize a health plan if their enrollees have higher overall health costs, as is likely to be the case if they have a disproportionate share of enrollees who hit the OOP cap, through an existing process called risk adjustment. Risk adjustment provides higher payments to health plans who on average enroll more people with higher health costs.

- Update current tax laws. The chronic care cost cap would replace the current tax deduction for certain medical expenses. This deduction permits those who itemize deductions to deduct qualified medical expenses that exceed 7.5% of their adjusted gross income.39 Initially, the elimination of the deduction would apply to people who have a chronic care cost cap in the exchanges. As the chronic care cost cap extends to everyone, the existing tax deduction would be fully eliminated. The fiscal cost of the cap could be further offset by increasing cost-sharing on low-value care.40

Conclusion

The ACA significantly improved the availability of health coverage in the United States and reduced the number of Americans without health insurance. It also instituted a cap on OOP costs—an invaluable tool to protect individuals that must be expanded to reach more people in need. However, high out-of-pocket health expenses present financial challenges for the chronically ill and those with ongoing health care costs, especially if these costs represent a high share of their income. The expansion of the ACA’s OOP cost cap to include a chronic care cost cap would provide these populations with similar financial protections to those of their healthier, insured counterparts and would also reduce the income-related burden of such costs.

Appendix

Cost caps for out-of-pocket expenses are based on the actuarial value of health coverage. Actuarial value is the percentage of total health care costs that the average person would have to pay out-of-pocket. For example, a silver plan on the exchanges has a 70% actuarial value, which means the average person in the plan would have coverage for 70% of their costs. A plan with a higher actuarial value covers more of a person’s out-of-pocket costs. Health plans have flexibility in how they set copayments and deductibles for the required actuarial value.

The chart below shows the actuarial values for the current and proposed cost caps, which would be the legal requirement for a health plan’s coverage of people in each income level in the exchanges.