Memo Published March 30, 2026 · 8 minute read

State Loans Could Help Fill the Graduate School Affordability Gap

Federal and private loans are common ways for students to finance their tuition, but there is another lending option that often goes overlooked: state-based education loans. Since Congress capped federal graduate borrowing and eliminated the Graduate PLUS (Grad PLUS) loan program, students will be looking for new options to finance their education. For some, state loans could be an appealing option.

Thirteen states have established loan programs to support residents’ postsecondary education. In five others, students can access loans from private companies that specialize in student lending for residents, though these are not formally affiliated with state governments or agencies. Some state-based loans offer better interest rates and repayment options in comparison to the traditional private market.1 Thoughtfully designed state-sponsored graduate loan programs offer an opportunity for states to bolster existing loan offerings or establish new ones to ensure sustained access to graduate education as federal support recedes.

Existing State Loan Options for Graduate Students

In 17 states, students can find state-specific loan options to pursue graduate school, and each program is operated slightly differently. In some cases, a state agency directly organizes and operates the loan program. For example, the Alaska Commission on Postsecondary Education, Alaska’s higher education agency, oversees the Supplemental Student Education Loan.2 Others have established quasi-governmental organizations to oversee loan programs. Rhode Island has outsourced its student loans to the Rhode Island Student Loan Authority (RISLA) since 1981.3 RISLA is a “non-profit quasi-state organization” that administers loans and financial support to Rhode Island’s students.4 Oklahoma uses a similar model. The Oklahoma Higher Education Loan Program, a public trust that was created by the Oklahoma legislature in 1972, supports college affordability by administering loans.5 Additionally, in some states, residents can take out loans from private companies that market themselves as state-based loan options. The South Carolina Student Loan, for example, offers loans to any graduate student in South Carolina and residents studying out of state, but these options are not run or created by state governments or agencies.6

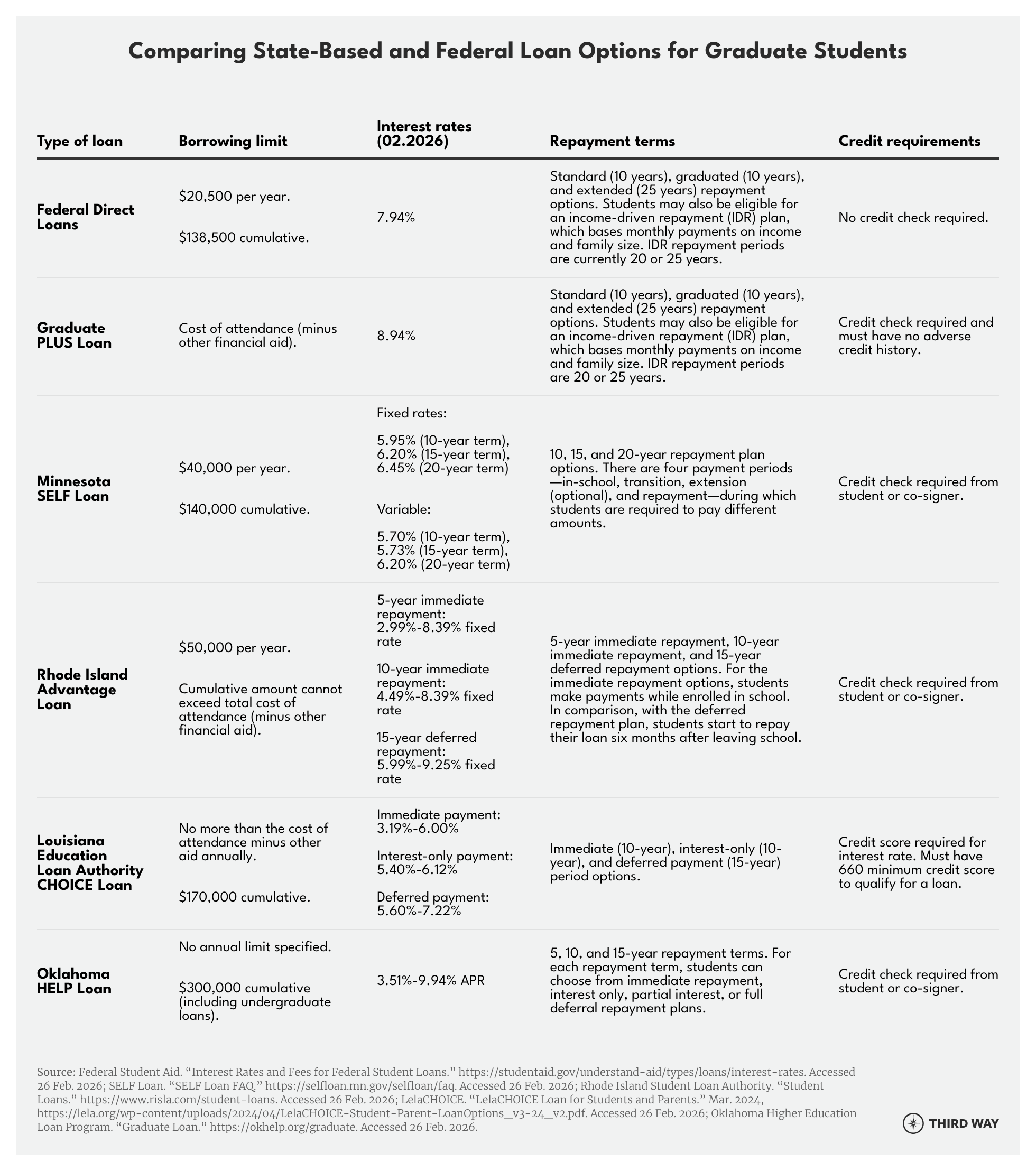

Some state-based loans offer lower interest rates and better repayment terms than traditional private loans.7 The table below compares federal Direct Loans, Grad PLUS, and four state loan options.

As these examples show, each program has different eligibility criteria and terms—residency, credit, enrollment status, and institutional requirements. For example, some programs offer loans just to their own residents, while others will also lend to non-resident students pursuing their education in the given state. Loan limits also vary greatly across programs. Alaska’s program is capped at a cumulative $96,000, while Oklahoma’s maximum is $300,000.8

For students who qualify for lower interest rates, state loans can be an affordable option that offers a manageable timeline for repayment. However, since interest rates and repayment terms are often credit-based, these loans may be most appealing for students and families who are in a stronger financial standing. For Louisianans, the Louisiana Education Loan Authority website clearly outlines students’ interest rate options based on their credit score.9 As seen in the table above, borrowers with a credit score of 800 or above can qualify for a loan with a rate as low as 3.19%, while those with a lower score may have a rate as high as 7.22%.10 Unlike federal loan options, where all borrowers have the same interest rate, terms for state options can vary widely across borrowers. It is critical that students and families review all the terms of the loan and compare their options.

How States Finance Student Loan Programs

States that oversee their own graduate student loans usually finance the loans with bonds. Bonds can be thought of as an “IOU” to investors that enable the state to set up what functions as a self-sustaining or revolving fund for students to tap and repay. States will take out a bond (usually a revenue bond that is tax-exempt) to finance the loans, and the bond is repaid from loan repayments and interest revenue.11 Minnesota, for example, finances its Student Educational Loan Fund (SELF) loans from revenue bonds, and the program does not receive any state appropriations.12 This model allows Minnesota to offer long-term, low-interest funding to its residents.13 Similarly, the Louisiana Public Facilities Authority (LPFA), a non-profit trust established by Louisiana, issues bonds to the Louisiana Education Loan Authority to finance student loans.14 The LPFA has never received state appropriated funds.15 The major advantage to using bonds is that funding tends to be stable year-to-year, and bonds can allow states to determine fixed interest rates that are constant throughout the lifetime of the loan.16

A few states rely on direct appropriations, rather than bonds, to fund their student loan programs. Relying on state appropriations can be a more challenging option, since this method requires consistent buy-in from the legislature and funding can thus change year to year. However, Kansas has succeeded with this model to support medical students. Kansas has a targeted student loan program that supports medical students attending the University of Kansas who are pursuing primary care or psychiatry.17 As part of the loan’s terms, students agree to practice medicine full-time in Kansas after their residency, helping to address local workforce needs.18 If a student completes their specified full-time medical practice, the remainder of the loan is forgiven.19 Funding for the Kansas Medical Student Loan (KMSL) is tied to state statute, which makes it relatively stable.

Connecticut is currently exploring an option to bolster its graduate loan offerings through state funding. The Connecticut Higher Education Supplemental Loan Authority (CHESLA) currently administers student loans for undergraduate and graduate students, which are financed by tax-exempt bonds.20 To meet the increasing need for more graduate student loan options, CHESLA announced that it plans to expand its graduate lending program.21 Officials plan to fund the loans through a bond and state allocations, which would be a different approach than Connecticut has historically used.22 As Connecticut develops and executes its plan, it may serve as a model for other states looking to expand loan options for graduate students.

Opportunities for States to Develop and Expand Loan Options

Starting this summer, the graduate lending landscape will look very different, as incoming graduate students will not have access to Grad PLUS loans and federal graduate loans will be capped. While state loans have previously provided gap financing for students, they now may need to fill in larger gaps for more students who no longer have access to the same federal loan dollars. Though they face significant budget constraints, states are in a unique position to support their students’ access to valuable degrees, and if able, may see value in exploring new funding opportunities to generate more graduate loans or target support for high-demand graduate programs.23 This will be an especially important consideration for states with a large graduate education market or a workforce that demands high numbers of professionals with graduate degrees.

States that currently run their own loan programs can consider dedicating more resources to graduate education. Most states that offer graduate loans also lend to undergraduate students, whose loan options were not heavily impacted by the recent federal policy changes; they may consider shifting some of their available funding from undergraduates to graduate students and prioritizing graduate students in the loan application process. States may also have undersubscribed loan funding from undergraduate loans that could be dedicated to graduate borrowers. These options would not require the state to generate any additional funding sources. Instead, it would allocate existing resources to the students with the greatest gaps after federal aid is maxed out.

Additionally, states could request appropriations from their legislatures to fund loans for graduate students. While most rely on bonds to finance loan programs, appropriated funding could be worth the investment for states whose economies heavily rely on the higher education industry. This is the route that Connecticut is pursuing: leaders are asking the state for $10 million in appropriations that would complement funding from bonds to expand loan options for graduate students.24 Connecticut is home to 36 colleges and universities, which train thousands of graduate students every year.25 States that similarly house many institutions and students could consider a comparable model, requesting state allocations to support a new or existing loan program.

Loan program eligibility can also be tailored to meet specific workforce needs. States can design loans for graduate degrees that are in high demand, rather than offering them to students pursuing any discipline. As mentioned, Kansas does this with their loans for medical students pursuing primary care or psychiatry, since the state needs more doctors in these specialties. The loan terms require students to practice medicine in Kansas after their residency, which ensures that these students will fill in workforce gaps. In this way, state loan programs can be designed to address workforce shortages, whether it be for doctors, nurses, or teachers. These targeted interventions can support employers and communities, while accounting for its resources and budget context.

Conclusion

States have an increasingly important role to play as students patchwork their financing options to pursue graduate education. Without an unlimited pot of federal loans, state loan programs could boost affordability (especially in comparison to traditional private loans) and support local workforce needs. State agencies and leaders must come together to determine whether their state should explore expanded graduate loan options, identify funding sources, and tailor eligibility requirements to meet students’ needs and workforce demands.