Memo Published June 23, 2020 · 20 minute read

Incentivizing Instructional Spending: Lessons for Higher Ed from the Medical Loss Ratio

Shelbe Klebs

The recent global outbreak of the novel coronavirus, known as COVID-19, ushered unprecedented new challenges into the higher education sector. Institutions found themselves swiftly and unexpectedly at a decision point: do they continue to operate as normal with the risk of widespread infection, or do they send their students home and move to remote education to stop the spread? Many institutions across the country made the very difficult decision to send students home and close their campuses, forcing both students and their professors to adapt quickly to a new virtual learning environment. The virus’s quick movement meant this shift had to happen with no warning and with makeshift technology infrastructures that were not prepared for the sudden influx of students.1These sudden changes have undoubtedly raised questions about the quality of instruction students will receive as they move entirely into an online world.

As we slide further into an economic recession, there will likely be an influx of students entering or re-entering the postsecondary pipeline to gain the skills they’ll need to find employment prospects that will hopefully lead to more stable and secure jobs. And we’ve already seen Congress step in to provide support to institutions in this time of crisis—with more likely to come.2These investments will only increase our need to get a solid picture of the spending choices of federally funded institutions to make sure that both students and taxpayers are getting the value for which they are paying.

One way to shed light on that question is to require that taxpayer-funded institutions spend a certain proportion of those funds on student instruction.3As new proposals of this nature emerge, including one from Senator Chris Murphy (D-CT) and at the state level in places like Maryland, Maine, and New York, it makes sense to see where else in federal policy we see similar concepts—and what we can learn from how those taxpayer protection mechanisms have worked in other industries. Luckily, a comparable idea already exists in law in the healthcare sector, known as the medical loss ratio (MLR). This memo explains what the MLR is and highlights key lessons from the provision that policymakers and advocates may want to adopt as they craft and implement a similar structure to hold higher education institutions accountable to spend in ways that actually benefit students.

What is the Medical Loss Ratio?

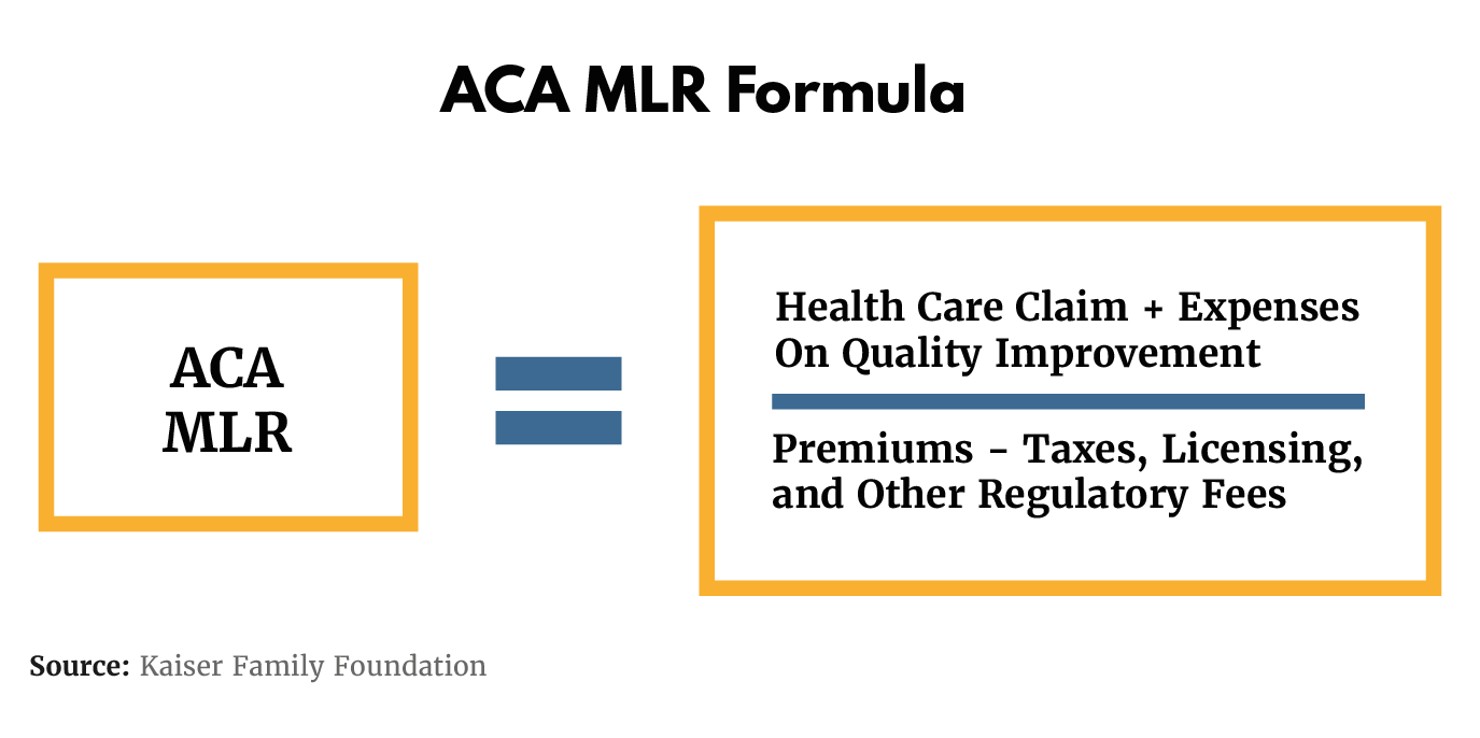

The medical loss ratio was included in the Affordable Care Act (ACA) in 2010, and a decade later is now a standard part of the federal regulation of health insurers. This consumer protection provision limits the amount of premium dollars insurers can spend on costs unrelated to medical care. According to the ACA, non-medical care includes things like administration, marketing, CEO salaries, or profits.4To calculate the MLR, the healthcare sector is split into three markets: large group (selling policies to groups of 100 people or more), small group (selling policies to groups of less than 100 people), and individual.5For the individual and small group markets, insurers must spend a minimum of 80% of their premium income on claims for medical care or quality improvement with the remaining 20% left over for unrelated costs. That means if a person pays $200 in premiums every month, $160 must go toward actual medical care. Insurers for large group markets must spend 85% on care or quality improvements and only 15% on unrelated costs. These percentages are averaged over three years, which helps prevent market instability by giving insurers time to adjust during fiscally challenging years.6And while these are the federal minimum MLR thresholds, some states set a higher MLR to provide additional consumer protections. For example, Massachusetts has an MLR of 88% and New York is 82% for individual and small group markets. The MLR is still 85% for large group markets in these states.

MLRs ensure that insurance companies put a majority of consumers’ premium dollars toward the actual provision of health care, instead of toward a CEO’s profits or advertising. Prior to the ACA, there were few rules around how healthcare insurance plans could spend their premium dollars. Some states set state-specific guidelines insurers had to follow, but it varied, leaving many insurers to decide on their own. In practice, this meant that if an insurer spent a significant amount of premium dollars on administrative costs or CEO salaries, there was nothing consumers could do about it unless they changed health plans, which many couldn’t do because of their pre-existing conditions. And although many insurers were already in compliance with the MLR before its implementation, bad behavior permeated the industry. According to one study by the Government Accountability Office (GAO), only 43% of insurers in the individual market spent 80% or more of premium dollars on medical care or quality improvement in the year prior to the MLR’s implementation—leaving the door open for federal intervention.7

How Consumers Benefit from the MLR

If insurers fail to meet the minimum percentages outlined in the MLR, they must legally rebate the excess dollars back to policyholders, employers for employer-sponsored plans, or individuals for individual market plans via checks that are sent annually in the fall.8Rebates are calculated for each market, on a state-by-state basis, and the exact amount of each policyholder’s rebate is based on the (pre-subsidy) premiums for that person’s plan.. In 2019, $1.37 billion in rebates were sent to consumers, including 56% going directly to the individual market.9The amount of the rebate varies widely; in 2019, the average national rebate was $154, but the highest average rebate was in Kansas, where 25,000 people received an average of $1,081.10

The ultimate goal of the MLR is to increase transparency for consumers by requiring insurers to not only track but publicly report the number of premium dollars spent on medical care and quality improvement in each state where they operate.11To accomplish this goal, insurers have to first and foremost agree on set definitions for what is considered medical care and quality improvement. Medical care can include activities such as clinical services, prescription drugs, hospital stays, primary care appointments, and other services for which medical care providers would submit claims to an insurance company. Quality improvement is considered any activity that leads to improved patient outcomes, patient safety, health technology, provider credentialing, and prevents readmission of patients to hospitals.12The MLR also gives insurers, medical providers, employers, and consumers better clarity on insurance claims and how premium dollars are spent.

What Higher Education Can Learn from the MLR

With a better understanding of what the MLR is, it’s easy to see how it could be comparable to the similar concept of instructional spending in higher education. Our current higher education system often fails to produce good outcomes for students, as our country’s low graduation rates and poor loan outcomes can attest.13And right now, taxpayers spend billions annually on getting students into college, but there is little incentive for schools to help get them through it. An instructional spending requirement could help provide increased clarity and transparency about what instruction at the postsecondary level means, as well as incentivizing institutions to invest more in their students’ instruction and, in the long-term, their success. To help maximize its chances of success, there are five key lessons that higher education should consider from the experience of the healthcare sector with the MLR.

Lesson 1: Clearly Define What We are Measuring.

What Happened in Health Care: As part of the implementation of the ACA, the federal government was required to set minimums defining what the medical loss ratio would be for each type of insurer. But to do this, there first needed to be clear and agreed-upon definitions of what constituted medical care to accurately capture which expenses would fall on either side of the medical loss ratio itself. To ensure consistency and buy-in from insurers, Congress tasked the National Association of Insurance Commissioners (NAIC) with setting the single MLR formula used for all insurers and creating uniform definitions for the medical care and quality improvement activities that count toward the spending requirement.14In the healthcare sector, NAIC is a well-established and accepted “standard-setting and regulatory support organization,” made up of both elected and appointed state insurance commissioners who have a track record of setting standards and identifying best practices for health insurance regulation in the U.S.15During this process, NAIC also established five quality improvement objectives designed to encourage insurers to maintain programs that result in better health outcomes for consumers, including improving health outcomes, preventing hospital readmissions, improving patient safety and reducing errors, promoting health and wellness, and improving healthcare quality through technology.16Because NAIC has a strong reputation and is well-respected within the healthcare space, the MLR formula, common definitions, and objectives were accepted by insurers with relative ease.

Lesson for Higher Ed: During the crafting of the ACA, policymakers recognized the importance of clearly and consistently defining what’s being counted. Shared, noncontroversial definitions that have wide buy-in can help with the implementation of new policies—especially ones in which questions of fairness, transparency in the process, or sanctions are involved. Unfortunately, this is something that higher education distinctly lacks at the moment. The reason to look at instructional spending is to ensure that students are receiving a high-quality education. But how should we define “instruction”? To date, there has been a lack of agreement, and lobbying efforts by several associations representing institutions have prevented us from having a good way to measure the options because of our incomplete data system.17

Despite these roadblocks, some stakeholders have attempted to forge ahead to answer the questions surrounding instructional spending. Senator Murphy (D), for example, proposed applying an instructional spending screen to examine what institutions with poor completion and post-enrollment outcomes are spending on instruction.18Similarly, groups like The Century Foundation proposed a way to calculate instructional spending with formulas using data from the Integrated Postsecondary Education Data System (IPEDS) that would integrate metrics into the instructional spending screen like student services, academic support, and institutional support.19However, the data reported to IPEDS can be difficult to use consistently and fairly because data reporting varies by sector. And, these proposals have not been broadly adopted. We don’t have agreement in higher education on how to define instruction, so we don’t even collect all the data we need to determine who is spending what on their students. If we are to use an MLR-like formula when it comes to dollars spent on higher education, we must develop a common definition of instruction, so we can then measure and enforce the use of those dollars.

Lesson 2: Create a Federal Floor, Not a Ceiling.

What Happened in Health Care: The MLR sent a clear message to insurance plans that a large majority of premium dollars must go toward the provision of actual health care. That’s because when purchasing insurance plans, individuals and employers reasonably expect that the bulk of their payments will directly benefit them, not cover administrative fees or pad the bank accounts of CEOs. To make this floor crystal clear for insurers, the MLR sets a federal bottom line prohibiting insurers from spending more than 15-20% (depending on the market) on non-medical care expenses. Any insurer that fails to meet this minimum threshold is then given the opportunity to improve their ratio before being subject to sanctions.

Lesson for Higher Ed: The clear lesson that higher ed can draw from the MLR is to set a federal floor that underscores exactly what level of spending is unacceptable to spend on costs that are not directly benefiting students, such as marketing and recruitment fees. For many proposals, this level is around a minimum of 33% spent on instruction, indicating that schools would have a legal obligation to put a minimum of one-third of their tuition and fee revenue toward student instruction. Given the varying levels of capacity and resources institutions have, setting a floor is a more fair and viable option than requiring schools to spend a certain amount on instruction. As stewards of taxpayer dollars, it is also more reasonable for the federal government to set a minimum standard of what institutions cannot spend their money on, rather than dictate what they must spend their money on. This is especially true given the studies that show spending large amounts of tuition and fee revenue on marketing and recruitment, for example, do little to benefit the students attending the institution.20

Lesson 3: Understand that Differentiation is Key.

What Happened in Health Care: The ability to adapt to the new regulations was key for a smooth implementation of the MLR. Because insurance companies can hold plans in all three markets (large, small, and individual), some insurers were required to adapt to MLR requirements that varied slightly between each plan. In most cases, those who held plans in large group markets were most likely to comply with the MLR because the large group insurers have the staff and capacity to adjust quickly to regulatory changes. On the other hand, insurers in small group and individual markets had a harder time adjusting to the changes and were less likely to meet the new standards immediately upon its implementation.21In 2010, one report from the GAO found that 70% of small market insurers met the MLR standards before adjusting to the new regulations compared to 77% in the large group market. But that same report found that less than half of insurers in the individual market were able to meet the requirements.22In many cases, this was due to inherent differences between insurers in the three markets. The larger insurers had an easier time adjusting because of their size and easier access to resources which the small and individual insurers lacked. Still, the flexibility built into the law for insurers operating in different markets set most insurers up to comply.

However, despite many of these challenges, most insurers across markets were able to meet the new MLR requirements and the number that didn’t was small.23Implementation was eased, in part, because there were differentiated standards for different insurance markets (80% for small group and individual and 85% for large group). This recognized/illustrated the different capabilities between insurers holding plans in different markets. All insurers were expected to comply with their market’s MLR by 2014, but the federal government did little to ensure they could meet the requirements. The federal government only allowed state adjustments, discussed below, which gave insurers and states more time to implement the changes. But, 303 insurance plans still issued rebates in 2014.24Much of the onus was put on insurers themselves to adjust. There could have been more flexibility built into the law and more resources and capacity could be given to those having a harder time meeting the new requirements.

Lesson for Higher Ed: Some higher education institutions will inherently have an easier time adjusting to new policies than others. This could be due to their larger size or holding significantly more resources. For example, institutions with large endowments that can be relied on in times of change or significant upheaval, like with the onset of COVID-19, may have an easier time responding to the implementation of new policies and can quickly reallocate resources toward instruction if they fall below a particular threshold. Therefore, policymakers need to take a lesson from what the healthcare sector did not do and focus federal resources to the institutions that need it most. These institutions may be smaller institutions or institutions serving a unique population of students who lack the resources they need to adequately meet an instructional spending accountability framework in real-time. Like in healthcare, differentiating the instructional spending requirement—while still providing a minimum threshold of quality—across institutions with varying resources and capacity could be an important way to acknowledge the needs and capabilities of institutions with different means and missions. Some institutions with greater resources could be held to a slightly higher instructional spending ratio in the same way that large group insurers are as a way to prevent institutions with significant means from moving money around to skirt the rule.

In many ways, the introduction of an instructional spending accountability framework could help policymakers determine which institutions are choosing to spend their tuition and fee revenue on student instruction—and which may have the resources but are choosing not to—in order to help further identify the institutions that need additional capacity and resources from the federal government. Similar to the MLR and the fewer than 30% of large group and small group insurance companies affected, many institutions would likely never be impacted by the instructional spending screen (one estimate shows that fewer than 5% of institutions would be impacted by this change) because they provide adequate instruction and have the resources to be nimble in times of significant change, like in trying to move curriculum online in a matter of weeks.25But some institutions don’t have those options, and this will help Congress get federal dollars into the hands of institutions that need the help the most.

Lesson 4: Realize It’s Not a Zero-Sum Game.

What Happened in Health Care: It’s important to note that the MLR requirement was not a zero-sum game for insurers. The MLR did not require insurers to be measured against each other in any way, but instead, to only be measured against themselves. The MLR holds each insurer to a minimum under the same standard based on the sector it is in and it is the responsibility of each insurer to meet that standard for each plan it holds in each state. Holding each insurer to the same standard without comparisons across insurers does not tie them to the performance of others. It also frees them from competing with insurers who may have different resources available to them. This is crucial because insurers are made up of different sizes, serve different populations, and have different resources at their disposal—yet a minimum threshold ensures that no insurance company can use those differences as an excuse to provide substandard service to their customers.

Lesson for Higher Ed: It is no secret that the higher education industry is diverse and meets varying needs. Each sector has different resources, serves different populations across the country, and has different missions. For this reason, it is important that an instructional spending accountability framework does not pit institutions against each other but should only be used to measure institutions against their own performance in spending an adequate amount of tuition revenue and fees on instruction. Many institutions have varying resource levels; the average tuition and fees at a community college are $3,730 but the average at a private, non-profit four-year institution are $36,880 for the 2019-20 school year.26But an instructional spending screen would not require all institutions, even within the same sector, to spend a predetermined dollar amount on instruction, but rather a percentage of their own tuition and fee revenue, whether that ends up being $1,200 per student at the average community college or $12,100 per student at the average four-year private non-profit school. The idea is simply to hold each institution to the same standard to determine if each institution is serving its students well. This will help factor in the differences between institutions and the intentional choices they are making in serving students and spending on instruction.

Lesson 5: Phase in New Policies and Sanctions Over Time.

What Happened in Health Care: Initially, there were concerns that implementing the MLR would destabilize the insurance market or drive insurers out of business. To address these concerns, certain states most at risk of destabilization were eased into the requirements by setting lower thresholds. After this phase-in period, if insurers still did not meet the requirements, they would face penalties. After three years they would be banned from signing up new customers and after five years the federal government could terminate the contracts for the healthcare plans in violation.27For example, these thresholds started as low as 65% in Maine but gradually increased over time until all states were meeting the federal requirements of 80% for small-group and individual insurers and 85% for large-group insurers by 2014.28In total, seven states received approval from the U.S. Department of Health and Human Services for adjustments that allowed them to ease into the requirements. One of these approved states was Georgia, which started with a 70% MLR in 2011, went up to 75% in 2012, and reached 80% in 2013. Gradual implementation of the new regulation gave states and insurers more leeway during implementation. Insurers used this time to rework their business models and change their spending patterns.29Eventually, all states met the federal threshold with some meeting even stricter requirements in states that set higher MLR requirements and the market remained stable.

Lesson for Higher Ed: Phasing in an instructional spending accountability framework over time can have a similar impact on higher education as it did in the healthcare insurance market. Suddenly requiring institutions to meet a spending threshold could be challenging for institutions with limited resources or for those who are far off from the federally-set percentage. A phase-in period over two or three years will give institutions more time to adjust and make changes in their spending priorities. For example, Senator Murphy’s instructional spending proposal requires institutions to spend at least one-third of its tuition and fee revenue on the direct instruction of students.30Phasing this plan in over several years could start with requiring 25% spent on instruction in the first year, increasing to 30% in the second year, and finally reaching 33% in the third year. In these uncertain and confusing times, institutions will be faced with tough decisions about how to allocate their likely shrinking tuition and revenue budgets. Yet, this is also the time in which it is more important than ever that institutions are prioritizing instruction so that students and taxpayers receive a return on their higher education investments. Phasing in an accountability framework that helps ensure students are receiving the instruction they pay for will maintain some stability in the market and is a useful lesson policymakers can take from insurance regulation.

Conclusion

There is one word that well describes what is happening to both higher education and the broader country over the last couple of months: change. It’s a time of scary and unanticipated shifts for students, faculty, and institutions across the country, and there is a growing need to make sure institutions continue to serve students well and provide high-quality instruction, especially as an increasing amount of that instruction will happen online. To do that, we will need clear definitions of what this instruction should look like and clear ways to measure whether student tuition and stimulus package dollars are going toward helping students—not padding institutions’ bottom lines. Higher education can look to other sectors—like healthcare—to draw valuable lessons about how to implement this kind of direct services screen. The healthcare sector, and the MLR in particular, can provide policymakers a map for how to regulate instructional spending in a way that will benefit students and produce the least amount of upheaval to institutions that are making responsible decisions with taxpayer dollars. Congress should consider these lessons when thinking about how to direct taxpayer dollars to federally funded institutions so that students know their tuition is truly going toward the cost of education in this new age of COVID-19.