Memo Published October 6, 2021 · 7 minute read

CDFIs: What Are They and How Do They Work?

Meco Shoulders

Credit and capital are the life blood of small businesses and often dictate whether a business can get off the ground, expand, and thrive. But capital continues to be a significant problem for small businesses, especially those that are owned by women and people of color. Most firms of color did not receive all the funding they needed, even after completing more financing applications.1 Minority-owned businesses, specifically Black and Hispanic businesses, are considered riskier than their white counterparts.2 And historic racism from financial institutions towards communities of color that need access to credit and capital has also led to a lack of trust.

Consider Carmen Tapio, CEO of North End Teleservices, LLC, a contact center providing services to government agencies and commercial businesses in Omaha, Nebraska. Tapio was denied relief from a traditional banking institution that she had a well-established relationship with prior to the pandemic.3 Her black-owned business generates millions in revenue, yet the lender said they were focusing more on large corporations. After multiple attempts, Tapio turned to an entity called a community development financial institution (CDFI) and received the necessary aid to maintain business operations.

Tapio isn’t alone. While community organizations have helped provide financial services for over a century, community development financial institutions were specifically created 48 years ago to make financial services more accessible and affordable for underserved communities.4 In this memo, we look at the different types of CDFIs, the government’s role, and how they are working when it comes to supporting small businesses.

What are CDFIs and how do they work?

CDFIs primarily focus on providing capital and financial services to businesses, individuals, and organizations that are often overlooked in both urban and rural communities. While traditional banking institutions may see risks or lower returns by focusing on these communities, CDFIs are designed to foster economic opportunity and revitalize neighborhoods.5 They provide financial assistance, technical assistance, and often more affordable products that meet the needs of the communities they serve.

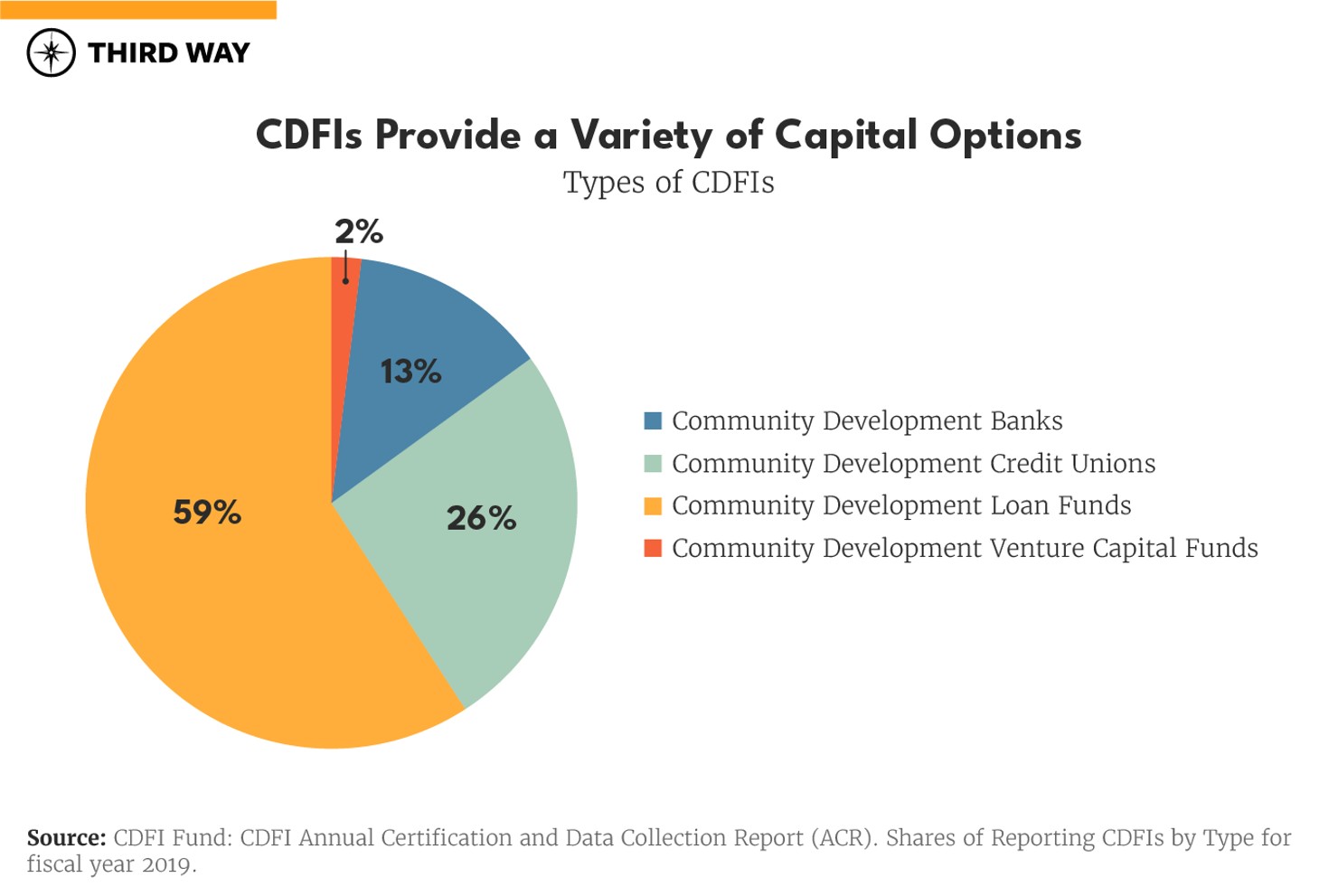

Different types of CDFIs

While their missions are very similar, not all CDFIs are the same. Different types include:

- Community Development Banks: For-profit corporations that issue investment capital to borrowers in distressed communities. Their typical borrowers are local entrepreneurs, non-profits, small businesses, and real estate developers.

- Community Development Credit Unions (CDCUs): Member-owned nonprofit financial institutions that offer consumer banking products, credit counseling, and business planning to low-income individuals.6 CDCUs tend to be located inside minority communities.7

- Community Development Loan Funds (CDLFs): Mostly nonprofit funds that work with individual and institutional investors to provide pre-development, business start-up, and expansion loans to business developers in low-income communities.8 Loan funds can have various specialties such as small businesses, microbusinesses, housing development, and community service organizations.9

- Community Development Venture Capital Funds (CDVC): Both for-profit and nonprofit funds which can spur job creation and entrepreneurial activity by providing commercial equity investments to small and medium-sized business in distressed communities.10

What’s the federal government’s role in CDFIs?

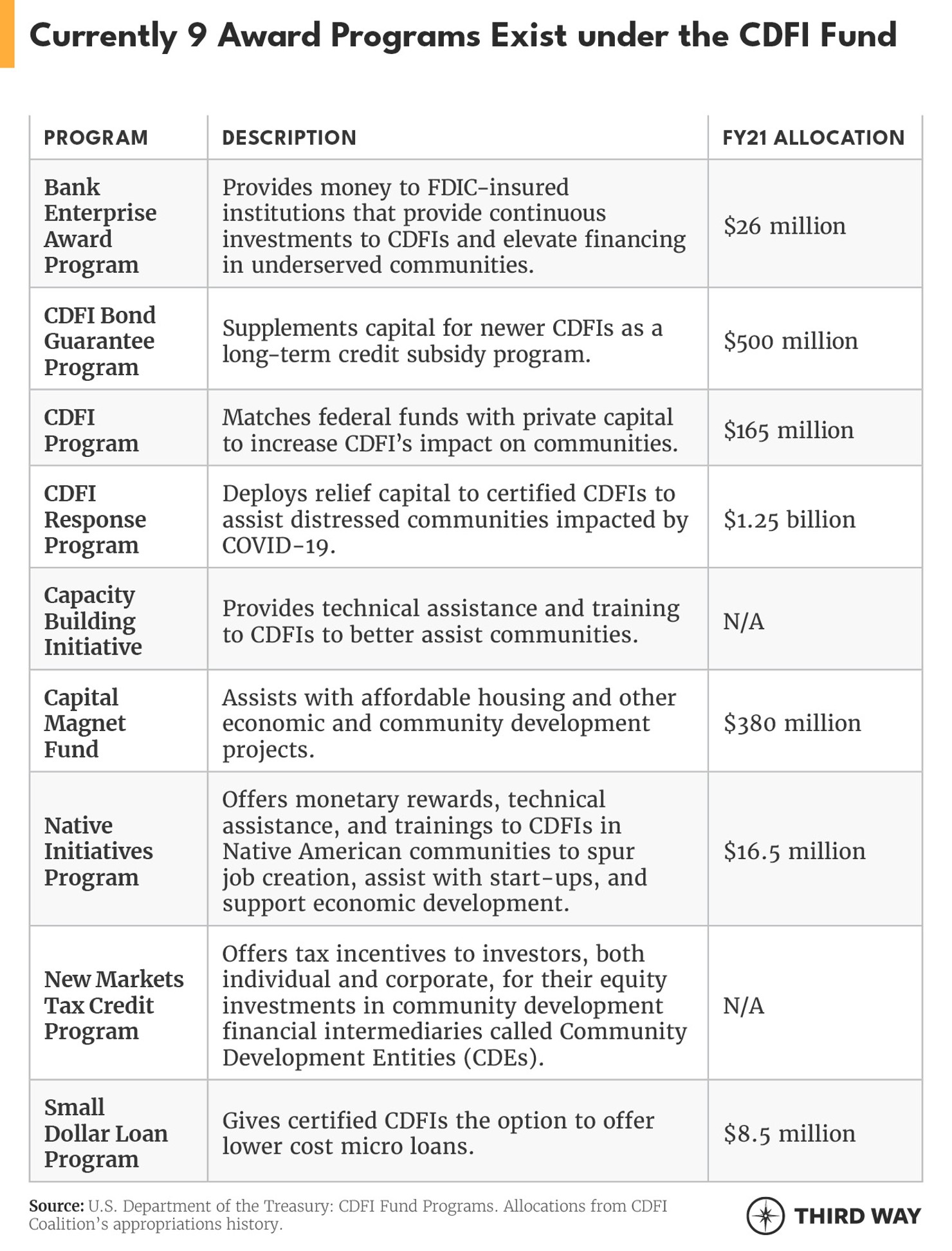

The federal government supports CDFIs by awarding funding and tax credits to institutions certified under the U.S. Department of Treasury’s CDFI Fund. Certified CDFIs are mandated to provide no less than 60% of their lending to support underserved communities.11 Financial institutions must be legally established upon applying for the CDFI certification.12They must be first responders to low-income and underserved communities and cannot be owned by any form of government.13 The CDFI Fund received $270 million for FY 2021.14

How has that federal role changed over time?

In the late 1970s, Congress responded to redlining practices in low- and moderate-income communities by enacting the Community Reinvestment Act (CRA) which, in part, established the very first CDFI.15 Then, in 1994, the Clinton Administration championed the Riegle Community Development and Regulatory Improvement Act which served as a foundation for modern CDFIs. The bill created the CDFI Fund, removed more barriers for small businesses, and focused on capital and credit for overlooked borrowers.16

In 2010, Congress passed the Small Business Jobs Act of 2010. The law created the State Small Business Credit Initiative, which allowed CDFIs to distribute funds to small businesses during the financial crash. At that time, much of the $1.5 billion program dollars flowed into communities through CDFIs. Earlier this year, Congress re-authorized the SSBCI for the first time since it expired in 2017, injecting $10 billion into the program under the American Rescue Plan.

Five things to consider about CDFIs.

CDFIs have had a long enough track record to give us a sense of what’s working and what could be improved. As we look back over the last four decades, several trends stick out:

1. CDFIs reach populations in this country that are often missed by traditional lenders. Eighty-four percent of CDFI customers are low-income, 60% are people of color, 50% are women, and 28% live in a rural area.17 This reach is especially important since many of these communities are left out of traditional lending options.18 Both Black and Hispanic people are unbanked nearly three times more than white people, meaning they are far more likely to not have a checking, savings, or money market account.19 Further, Black people are three times more likely to use substitute financial options like check cashing services than their white counterparts, while Hispanic people are twice as likely.20

2. CDFIs often provide technical assistance and support. While access to capital is critical, many small businesses also need other forms of assistance. CDFIs provided development services to over 1 million people in 2018, including financial education and business technical assistance.21 One-of-three CDFIs provide technical assistance and 25% provide loans for on-the-job training and recruitment services.22 Others act as mentors for small business owners and entrepreneurs—helping them meet goals, build networks, and retain jobs.23

3. CDFIs were essential to getting pandemic relief out to minority small businesses. Federal funds were directed to CDFIs during round two of the Paycheck Protection Program in part because of initial failures of the program to help many small businesses owned by people of color. The CDFI Rapid Relief Program received $1.25 billion to support underserved communities—making lending more available for more than 800 CDFIs.24 With federal funds, CDFIs were able to make more smaller dollar loans to distressed businesses as well as offer more loan deferments, forbearances, and modifications with flexible terms.25

While there are clear benefits, there are also areas for improvement:

4. CDFIs cannot meet the demand for their services.26 CDFIs want to expand, but new capital or other support options are needed. In 2018, 32% of surveyed CDFIs received qualified loan requests that could not be fulfilled, according to Federal Reserve data.27 And during that year, 73% of surveyed CDFIs experienced an increase in demand for their financial products, with expectations for further demand increases.28 Much of CDFIs’ ability to supply financial products are limited by the federal government and investors—making it difficult to meet the demand of underserved communities.29

5. CDFIs have trouble with staffing which limits products and services.30 A Federal Reserve CDFI Survey found that more than 80% of CDFIs stated that limited staff hinders their performance and 44% indicated a lack of necessary skills.31 In addition, CDFIs are often small. While the median number of employees in a CDFI is 15, 38% have fewer than 10 employees and there’s even a CDFI being operated with only one part-time employee, according to the survey.32 In all, two-in-three CDFIs say that they are too capacity constrained to do everything they would like to do.33

Conclusion

CDFIs can be unsung heroes to the residents and businesses of low-income communities and communities of color. They are successfully providing financial support and technical assistance to women and minority-owned businesses. And CDFIs made huge strides to assist fighting the economic damage of the COVID-19 pandemic. However, data continues to reveal the need for more support, and further investment in CDFIs could better equip them to meet the needs of their local communities. Policymakers should consider bolstering these institutions so they can continue being champions to the communities they serve.