Report Published April 21, 2026 · 7 minute read

The Missing Middle: When Capital Constrains Growth

A familiar story across America: a growing small business with $3 million in revenue wins a new contract. It’s a breakthrough—but fulfilling it requires $350,000 upfront to cover payroll, inventory, and ramp-up costs. Their lender offers only a fraction of what they need or demands additional documentation or collateral that the business owner can’t provide. Faster online financing exists, but the cost of capital is too high to support real growth.

The result is frustratingly predictable: a viable business turns down work or delays expansion—not for lack of customers, but for lack of the right financing.

Variations of this scenario play out across industries and geographies. At its core, this missing middle is a Goldilocks problem: financing options are either too small to support growth or too large, rigid, and complex to be accessible and affordable. What is missing is flexible, moderate-sized financing for ready-to-scale, mid-size businesses.

The missing middle in capital markets is not a story of weak demand or unusually risky borrowers. Instead, it reflects a gap in financial products and processes. Many firms seeking moderate-sized financing are profitable, yet still struggle to access affordable, right-sized capital.

This report explains why the missing middle financing gap persists. Drawing on national survey data, we show that demand for growth-oriented and flexible credit is strong, but financing shortfalls remain common. We then identify four recurring constraints that prevent supply and demand from aligning at moderate deal sizes: documentation, collateral, timing, and market structure.

Where is the Product Gap?

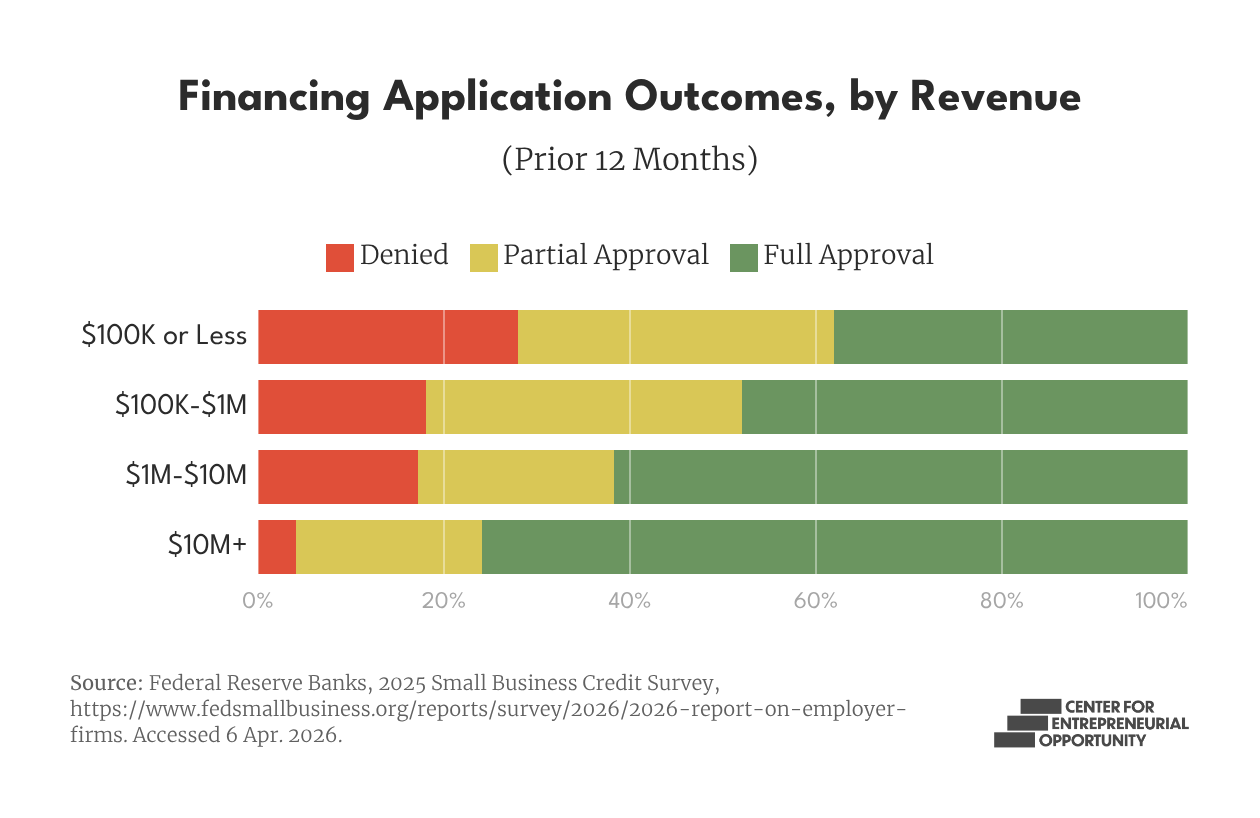

Growing a small business is hard. Only a small share of firms reach the $1 million revenue threshold, and even fewer reach $10 million.1 Access to right-sized, flexible, and affordable growth capital is frequently cited as a barrier.2

Stepping back, the small business capital market largely operates at two ends. Community lenders and Community Development Financial Institutions (CDFIs) are structured to deliver smaller, standardized loans, while banks and institutional capital typically focus on larger deals that justify fixed underwriting and monitoring costs.

The Federal Deposit Insurance Corporation’s Small Business Lending Report highlights the challenges small banks face when making moderate-sized loans. Larger loans represent a greater share of a small bank’s portfolio, increasing risk concentration. As loan sizes grow, approval requirements and internal oversight also increase. These additional layers emerge more quickly at smaller institutions, which operate with smaller balance sheets. Few providers offer, or specialize in, moderate-sized financing. As a result, many viable firms lack appropriate financing at precisely the moment it could enable their growth.3

Many mid-revenue firms ($1 million-$10 million) that apply for financing receive less than they request or are denied entirely. Among those reporting difficulty accessing affordable capital, roughly half delayed or halted expansion plans as a result.4

4 Capital Constraints for Middle Market Firms

The missing middle results from four recurring constraints that complicate efforts to make moderate-size deals: documentation, collateral, timing, and market structure.

Paperwork as a Barrier

The first, and most immediate, constraint is documentation. As financing needs grow, lenders require more information on financial history, formal reporting, and diligence than many emerging firms are prepared to provide. This often includes multiple years of business tax returns, audited or professionally prepared financial statements, and detailed cash-flow projections. Even when performance is strong, growing firms may not have these formalized or readily available.

Picture a profitable residential landscaping business that has an opportunity to take on commercial clients—work that requires more workers and additional equipment. Without audited or bank-ready financials, however, it cannot access the financing needed to make those investments.

Asset-light Firms Get Left Out

Mortgages and car loans are standardized and replicable because the asset itself serves as clear collateral: it has a defined market value, can be easily appraised, and can be seized or sold if the borrower defaults. Business assets are rarely as straightforward, so lenders often require a personal guarantee in lieu of (or alongside) collateral.

This is where the constraint arises: profitable firms can repay, but they lack easily valued, collateralizable assets that simplify lending and keep it affordable. As a result, lenders struggle to provide larger amounts of affordable working capital that can support growth. While specialized asset-based lending and receivables financing exist, these tools are not universally available across regions or industries.

Think about an IT services group that wants to take on a new contract but needs capital to hire and deploy additional staff. The firm may be able to use their invoices as a substitute for collateral, but that option is not available at scale or in every market. Without access to an innovative capital provider, the company may have to delay expansion.

Growth is Lumpy—Financing is Not

Timing constraints arise in two ways: during growth moments and through normal business volatility.

Growth often requires capital before returns materialize. Taking on a bigger contract or entering a new market may require hiring more workers or buying more equipment—costs that must be paid before they generate new revenue.

At the same time, lenders often interpret uneven cash flow as a sign of higher risk, even when it is standard for an industry. Accounting firms are busier in tax season, retail stores are busier around the holidays, farms are dependent on seasonal crop cycles, and contractors might be working on 60- or 90-day pay cycles. These patterns are normal, yet they are often treated as risks in underwriting. Flexible tools—such as revolving lines of credit, which function like a credit card—are often essential.5

Limited Infrastructure for Moderate Deals

Market structure can also constrain access to capital for both borrowers and lenders.

In capital deserts, limited competition can make it difficult to find flexible, right-sized financing at an affordable price. Even in areas that are not technically a capital desert, the presence of lenders does not mean that all the community’s financing needs are met.

Industry structure can create additional barriers. Firms with a small number of customers or a concentrated market are often treated as having higher risk by lenders because demand appears less diversified. Yet in many industries, this concentration is entirely normal. An aerospace parts manufacturer, for example, may only have a handful of customers, but that does not limit its capacity to innovate or grow. Likewise, a food service business that relies heavily on contracts with a local school district may have significant growth potential, even if its customer base appears narrow.

Conclusion

The missing middle is not a story about risky borrowers or weak demand—it reflects a structural failure in capital markets to serve viable, growth-oriented firms at moderate deal sizes.

Community lenders and CDFIs are designed for smaller loans, while banks and institutional capital typically focus on larger ones. Firms seeking capital in the middle are often left with products that are too small, too expensive, or too rigid to support real growth. Four key constraints drive this gap: documentation requirements that outpace what scaling firms can provide, collateral standards that exclude asset-light businesses, timing mismatches that penalize seasonal and contract-driven revenue cycles, and market structures that limit competition and lender capacity.

Until these constraints are addressed, profitable businesses will continue to turn down contracts, delay hiring, and slow expansion. Closing this gap will require innovative financing solutions designed around how growth-stage firms operate.