Report Published November 12, 2015 · Updated November 12, 2015 · 12 minute read

Housing Finance Part 2: The Guarantee

A 30-year old walks into a bank seeking a $200,000 home loan. The interest rate is 4% and the term is 30 years. The borrower seems like a capable person. She has a job, an education, and some student loans that she pays on time each month. But beyond that, the bank doesn’t know too much about her prospects. It seems like lending to her is a big risk. And actually, when you really think about it, what bank would ever possibly want to lend to her? Suppose she loses her job, or the economy takes a dive, or she becomes injured or ill and cannot work? Sure, the bank has the house as collateral, but the real estate business is a tough one for a bank to be in.

The truth is that the affordable 30-year fixed-rate mortgage to which Americans have grown accustomed is largely the product of a government guarantee. This guarantee has been at the core of the American housing market for decades. And until the financial crisis, there wasn’t much serious congressional effort to alter how guarantees work in our country. But now there is.

This memo is second in a three-part series explaining housing finance and the role government-sponsored enterprises (GSEs) play in capital markets. In our first paper, we explain securitization and how it keeps the housing finance wheels turning. This paper explains the role of guarantees in housing finance and explores what really keeps the housing finance system affordable and working.

What Are The Biggest Mortgage Finance Risks?

A new reality of the post-financial crisis world is that access to mortgage credit is particularly tight—the median credit score for borrowers is about half a percentage point higher than its pre-crisis level, and national surveys of loan officers show a wave of credit tightening.1 This means lenders are demanding higher credit scores from borrowers than in the past and charging more for loans relative to the 10-year Treasury yield than before. In finance terms, the market has “repriced” mortgage risk.

But even during normal conditions, a mortgage is still a large and illiquid asset—that is, it is both pricey and difficult to turn into cash on a moment’s notice, unlike a Treasury bond or common stock. The risks most commonly associated with mortgages are credit risk (the risk that individuals will default on their mortgage), interest rate risk (the risk that rates will change up or down), and prepayment risk (the risk that a borrower will pay off the loan early, abruptly ending the steady cash flow).2 The government is involved in the “market” for all three of these risks.

This situation isn’t unique to the United States. There is a variety of ways countries deal with the risks associated with mortgage lending. They include having a government mortgage insurer, government guarantees of mortgage securities, and government-sponsored enterprises that buy up private mortgages. The U.S. is the only major country in the world to have all three.3

- The Federal Housing Administration (FHA) directly insures private mortgages issued by banks.

- Ginnie Mae provides explicit guarantees on mortgage securities (mortgages that are packaged by banks and sold to investors).

- Fannie Mae and Freddie Mac, as government-sponsored enterprises, provide guarantees on securities which also have an implicit guarantee from the federal government.

The U.S. has all three because of our love affair with the affordable, pre-payable, 30-year fixed-rate mortgage. France is the only other major country to have long-term fixed-rate mortgages comprise the majority of its market. But even these French products stop short of products in the U.S.: they include pre-payment penalties which transfer the cost of this risk to mortgage borrowers.4

As discussed in a previous paper, development of the mortgage securitization market in the 1970s revolutionized how capital flows into the housing markets. The mass purchasing, pooling, slicing and then selling of mortgage securities by large institutional investors and GSEs created an avenue for everyday investors to gain exposure to the housing market. It also created room for banks to issue more home loans. But securitization has its flaws because information does not flow perfectly to investors. In the old days, issuing a mortgage was a personal experience between a mortgage lender and borrower. Nowadays, investors rely on someone else’s judgment and assurance that they issued a mortgage to a creditworthy borrower. So to remedy these imperfections, the system also relies heavily on government guarantees and the ratings issued by credit rating agencies like S&P, Moody’s, and Fitch. In the next section, we discuss how government guarantees and credit ratings interact in the housing finance system.

Who Guarantees U.S. Mortgages?

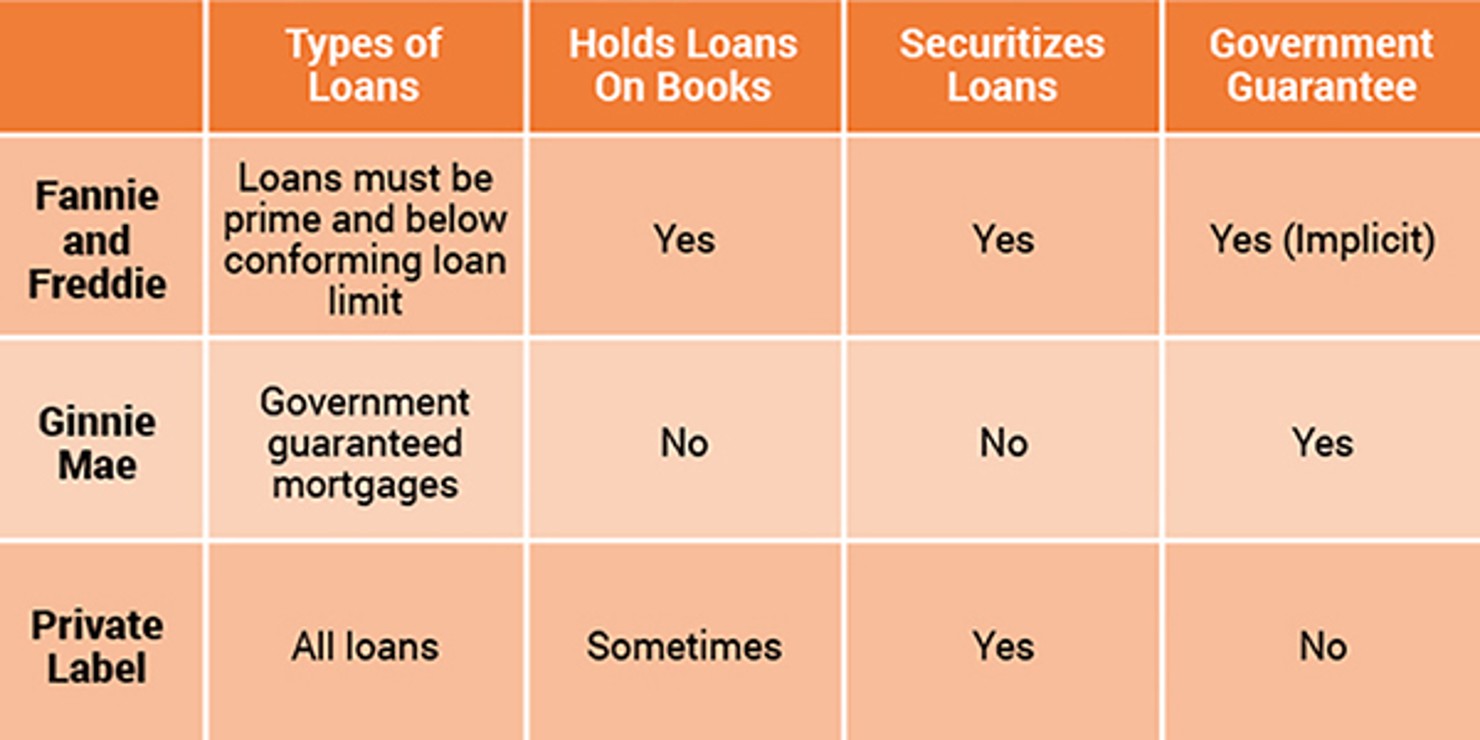

There are varying degrees of guarantees offered in the housing market which allow for this housing finance wheel to keep turning. Depending on who securitizes the pool of mortgages, the guarantee changes. The three main players in this arena are: (1) the GSEs (Fannie Mae and Freddie Mac), (2) Ginnie Mae, and (3) the private market. The following table shows their involvement in housing finance and what level of guarantees they provide:

Fannie Mae and Freddie Mac: The Implicit Government Guarantee Fannie and Freddie were created by the government but are not run by it. They are private companies that issue stock, have boards of directors and CEOs, and strive to maximize returns for shareholders. However, because they are government-created, they also have a congressionally mandated regulator and a public goal of supporting a vibrant market for home mortgages. In that way, they are a cross between a private company and a government agency.

Fannie Mae and Freddie Mac guarantees have been supported for decades by their companies’ assets—not the Treasury. The purpose of a GSE guarantee is to instill confidence in investors that the home loans backing the securities they own will safely provide payments throughout the life of a loan. Even though the GSE guarantee is not backed by a formal government promise, many people (and many GSE critics) believed that such a promise was implied. Indeed, there was a commonly accepted view before the crisis that the government would never let Fannie or Freddie go under.5 In its own way, if “too big to fail” applied to any financial institution in America, Fannie and Freddie seemed to be the first in line. This is why GSEs have an “implicit guarantee.” And because of this implicit government guarantee, the GSEs had and will continue to have a competitive advantage in the markets because no institution (or government) has deeper pockets than the U.S. Treasury.

Those claiming that the GSEs had an implicit guarantee were right. In 2008, Fannie and Freddie teetered on the brink of bankruptcy. Instead of letting them fail, the government bailed them out to the tune of $187 billion in taxpayer dollars. The government then placed these two GSEs into conservatorship and the implicit guarantee became explicit.

What the GSEs Do

GSEs essentially pool and manage risk. They do this for credit risk by pooling regional risks into diverse pools and then insuring those risks. In return, the GSEs will charge a g-fee—a cost often passed on to the borrower in higher mortgage rates. The g-fee is the biggest source of revenue for the GSEs. The GSEs also manage interest rate and prepayment risk through the issuance of callable debt (interest rate risk) and the purchase of MBS securities (prepayment risk), earning a spread. The combination of these risk management tools results in greater liquidity. The greater liquidity in the MBS market means wider participation by investors and lower mortgage rates for homeowners.

Ginnie Mae: The Explicit Government Guarantee Ginnie Mae provides explicit guarantees for the federal government’s mortgage programs. The biggest recipients of Ginnie Mae guarantees are the Federal Housing Administration (FHA) and the Department of Veteran Affairs (VA).6 Ginnie Mae doesn’t buy or sell loans, nor does it issue MBS like Fannie and Freddie. Instead, it provides guarantees to investors who purchase a loan administered by government agencies, such as the FHA and VA. By guaranteeing such loans—when other institutions bundle and sell securities using these loans as the underlying asset—Ginnie Mae is ensuring that those securities will make timely payments of principal and interest. In this situation, the federal government is absorbing the heightened levels of default risk these homeowners carry with them. In turn, this allows programs like those at FHA and VA to offer low down payments and affordable interest rates, helping to serve homebuyers who otherwise could not secure a home loan.

FHA was created to meet the needs of risky borrowers, those who didn’t meet the standards set by Fannie and Freddie or couldn’t make the large down payment needed to purchase a home (FHA allows borrowers to make down payments as little as 3.5%). FHA’s work is targeted to this relatively small group of borrowers and makes up a very narrow portion of the overall housing finance market. But if this explicit guarantee wasn’t in place, a federal program like the FHA would be unsustainable.

Another “Guarantee”: the To-Be-Announced Market

It is very common in the U.S. for lenders to give mortgage applicants the option to lock in mortgage rates for a period of 30 to 90 days while buyers and sellers haggle over prices, terms, and closing dates. How is this done when there is risk that interest rates will change? Answer: through the ”to-be-announced” (TBA) market. This is a highly specialized forward contract market meant exclusively for trading Fannie, Freddie, and Ginnie mortgage-backed securities. This market is second only to Treasuries in daily trading volumes in the U.S. bond markets.7

A forward contract is an agreement to exchange a security (or product) for an agreed upon cash payment at a specific date in the future. Contracts like these were originally created to allow farmers to lock in the price of their crop for the upcoming season, bringing a price guarantee to both farmers and businesses. In a TBA trade, the seller of MBS will agree to exchange a fixed amount of MBS for a lump payment on a future date, typically no longer than a few months in the future. However, what’s different is that the seller doesn’t need to specify which mortgages will be pooled together. This gives the aggregator the flexibility and time to pool mortgages. When the future date arrives, the cash and security change hands. So even though these securities are backed by thousands of unique mortgages, the securities are considered fungible from the trade date to the settlement date. This homogeneity is made possible by the shared government guarantee each MBS receives and the standardization of underwriting and securitization practices within Fannie, Freddie, and Ginnie.

Why does this matter? Some worry that radical GSE reform might disrupt this market. Without the GSEs, investors would be forced to analyze independently each mortgage pool embedded in each TBA contract crippling a key feature of the TBA market—liquidity. This shows that in reforming the GSEs, it’s very possible to create unintended consequences that could gum up the housing market.

Private Label: No Government Guarantee The last group involved in the issuance of MBS in the housing finance world is the private markets. This group is commonly referred to as the private label securitization (PLS) market. Historically, PLS has served as a filler for the two spaces in the housing market where the government is not involved: (1) large loans that exceed the limits of the GSEs (these are called jumbo loans), and (2) for individuals who lack the proper credit scores set by the FHA—typically subprime borrowers.8 The PLS market has no guarantees so to instill confidence into investors, the PLS market relies heavily on the credit rating agencies—S&P, Moody’s, and Fitch—to rate securities.

Before the crisis, investor confidence in PLS issuances that included subprime mortgages was bolstered by the high-grade credit ratings that S&P, Moody’s and Fitch gave to MBS products. Partly on the strength of such ratings, firms like Lehman Brothers issued subprime MBS without hesitation, winding up with dangerously outsized exposures when housing prices collapsed.9 Amid this fallout, investors lost faith in the ratings issued for these MBS. This development effectively ended the private market’s participation in mortgage securities.

The Dormancy of the PLS Market

Today, the PLS market remains virtually nonexistent—less than 1% of all MBS issuance came from the PLS market in February 2015. The largest factor contributing to this dormancy is fear. Investors are simply hesitant to reenter the market having been burned so badly by subprime MBS in the crisis. There are three other secondary factors worth noting. First, to counteract this exit by investors, the federal government expanded several housing programs into areas usually covered in the PLS market. By adjusting the eligibility requirements for these programs up or down, the government has crowded out parts of the PLS market. Second, there is uncertainty regarding MBS-related regulations by the Consumer Financial Protection Bureau, Treasury and other agencies. Some investors are simply waiting until these rules are finalized. Finally, Congress’s hesitation on GSE reform hangs over investors’ heads. But again, the biggest explanation of the shrunken size of the PLS market is fear. Rebuilding that trust will simply take time.

Conclusion

Many argue that the duopoly of Fannie Mae and Freddie Mac has concentrated too much credit risk in these quasi-governmental entities; they say large swaths of risk must be transferred back to the private markets. However, since the crisis, the GSEs (and their conservatorship status) have been left untouched. There is broad agreement that the status quo is unacceptable and the housing finance system needs reforms. Few disagree that housing finance reform should revive non-government guarantees and the dormant PLS market.

In our final paper in this series, we discuss the role of GSEs in the capital markets and what fundamental questions policymakers should ask in order to fix the problem of guarantees.