Report Published December 7, 2015 · Updated December 7, 2015 · 15 minute read

An Introduction to the Fiduciary Rule Debate: Explaining the Best Interest Contract Exemption

Takeaways

- Those who give investment advice are held to different standards depending on what types of services are provided, how they are paid, and what types of accounts they serve. Some standards, including the fiduciary standard, require advisers to put their clients’ interests first. Often times, advisers follow a less rigid standard, which requires their advice to be suitable for a client.

- The Department of Labor (DoL) is nearing the final version of a rule that would expand its fiduciary standard to many more advisers, requiring advisers to reveal conflicts of interest in their compensation and take steps to mitigate those conflicts, among other things.

- DoL and some consumer groups say the rule is necessary to protect consumers’ retirement funds and will lead to them paying less in investment fees.

- Many who work in financial services support expanding protections to consumers, but say DoL’s rule is so cumbersome that it will become more difficult for consumers to access advice altogether.

Several decades ago, most Americans who had private retirement savings held it in the form of a defined benefit pension. Major investment decisions were made by a worker’s employer, who was responsible for making payments to retirees. Fast forward to 2013, when more than 53 million Americans had a 401(k), a type of defined contribution plan.1 Of the nearly $24.7 trillion Americans have saved for retirement, $4.2 trillion are in 401(k) accounts and $7.4 trillion are in Individual Retirement Accounts (IRAs), making these some of the most popular retirement saving tools.2 The growing prominence of 401(k)s and IRAs means families, more than ever, are responsible for making more decisions about their retirement savings.

One of the many decisions retirement savers can make is to roll over an employer-provided 401(k) plan to an IRA. Many Americans in 2012 alone made such a decision, resulting in the total value of IRAs exceeding $300 billion.3

The regulations that govern retirement savings advice allow for multiple types of standards to apply to different types of advisers in different situations. Consumers are subject to these varying standards in the course of using ordinary retirement savings products. Most policymakers agree that a single standard should encompass the entirety of retirement savings world. This debate has uncorked heated arguments over arcane terms like fiduciary and suitability. The Administration wants investment advice, no matter who is providing it, to adhere to a fiduciary standard; the finance industry supports expanding protections to consumers, but feels this rule, as written, is unworkable.

In this paper, we give an overview of the proposed change and the core arguments of those for and against the change.

The Standards

401(k)s and IRAs are similar. They are tax-preferred investment vehicles that individuals hold until retirement. More than 77 million Americans actively participate in a 401(k), have an IRA, or both.4 One major difference between the two investment vehicles is 401(k)s can only be offered through employers and are managed by a plan administrator. IRAs can also be offered by employers, but are often opened by an individual without any linkage to an employer.

Should these savers get advice on any of these products from a financial adviser, determining what standard of care their adviser is held to is what’s being debated today. But this was also something Congress attempted to tackle in 1974 when it passed the Employee Retirement Income Security Act (ERISA). ERISA is an extensive law and a critical pillar of employee protection in America.5 Under the jurisdiction of DoL, ERISA prevents the pension abuses that were quite common before President Ford signed the law in 1974. Before ERISA, employers would skirt commitments they made to retiring employees by filing for bankruptcy, underfunding their pensions, or simply firing employees approaching retirement.6

But the retirement savings landscape has dramatically changed since the 1970s, and much retirement advice is now given outside of ERISA’s scope. A key element as to whether advisers’ advice is required to be held to the ERISA fiduciary standard is if the advice that is provided is deemed investment advice according to ERISA rules (more on this in the next section, “Determining What Is Investment Advice”). If the glove fits and ERISA applies, then the investment advice is held to the more rigid, rule-based world of ERISA regulation. If the glove doesn’t fit, then the advice is subject to a patchwork of regulators that includes the Securities and Exchange Commission (SEC), Financial Industry Regulatory Authority (FINRA), and state insurance regulators, among others.

Layered on top of these rules are ones governing the advisers themselves—separate from the rules governing the advice they give. This second layer of protection for consumers is a byproduct of Great Depression-Era laws, among others, where advisers are required to act in the best interests of clients.7 But, unlike the rules governing advice, the ones governing advisers are not as rigid. An adviser meets his or her fiduciary duty after providing disclosures.8

These varying layers of regulations and the patchwork of regulatory bodies could remain happily separate but for one problem. There are scenarios in which unknowing savers will crisscross between the different worlds. One example of that is when 401(k) holders roll over their plans into IRAs. This, along with many other scenarios, put savers in unfamiliar territory in which the adviser doesn’t have to provide advice that is in the best interest of their client.

Determining What Is Investment Advice

Today’s law starts by saying that all advisers have to provide investors advice that is in their best interest, no matter what type of investment vehicle the individual holds. This is thanks to ERISA.9 This standard is referred to as the fiduciary standard. When an adviser’s advice is held to a fiduciary standard this means the adviser is required, by law, to put their clients’ interests first. ERISA also makes it difficult for an adviser acting as a fiduciary to receive commissions as compensation.10

But as written today, ERISA regulations fail to cover every advice-giving situation because of how the words “investment advice” are defined. A key component to ERISA’s regulation of advice is determining whether or not that advice is subject to ERISA “investment advice” regulation. Today, this determination is made by a 5-part “investment advice test.” This test has been in place at DoL ever since ERISA was enacted in the 1970s. If the advice passes this test, then the advice must adhere to ERISA’s fiduciary standard. But at times, this test isn’t passed. One example is when an adviser provides advice infrequently, then that advice doesn’t have to meet the fiduciary standard. Another example is when the saver makes investment decisions based on multiple sources, not the advice of one, primary adviser.

The advice to roll over a 401(k) isn’t held to a fiduciary standard since the rollover is considered a one-time “advice-giving” event. Instead, in this example, the adviser is held to a separate standard regulated by a myriad of federal and state entities with the most likely source for regulation being SEC and FINRA’s suitability standard. But even though the standard sounds like it’s lacking in consumer protections (since advisers need not put their client’s interests first), the finance industry points to two things when it comes to rollovers. First, each of these regulators have rigorous standards on their own that protect clients from bad actors. Second, given that the client is moving to a much more portable account (an IRA), changing the regulatory threshold only makes sense.

The Compensation

The main goal of DoL’s proposed rule is to root out conflicted advice. As defined by the Council of Economic Advisers (CEA), advice becomes conflicted when the adviser’s pay is contingent upon an action taken by the saver.11 If advisers are compensated only when they steer money into one fund over another, they face an incentive to make decisions that may not be in the best interest of the client. One of the more common conflict scenarios is as follows: A firm has a fund it wants its advisers to sell and is offering a bonus to its advisers for every time they get one of their clients to invest in that fund. Even though that fund might carry larger fees than otherwise similar products, the adviser still steers those dollars into the fund that pays the bonus.12

Today’s investment advice framework is structured so that if advice falls within ERISA’s scope, these conflicts do not exist. It does so by prohibiting certain transactions, among other things. In contrast, other non-ERISA regulators allow conflicts to exist largely because they see these conflicts as not harming investors. But the question remains: who’s right? Can conflicts really exist without hurting savers?

This brings us to a CEA study that is at the center of this debate. According to the CEA, investors lose over $17 billion a year in retirement savings because they are being steered to higher-fee products due to conflicted advice.13 The DoL contends its fiduciary rule will weed out conflicts and recoup a sizeable chunk of that $17 billion for investors. Opponents argue, however, that the $17 billion figure is unsubstantiated and doesn’t include many unintended costs of the rule. They argue that investors receiving any advice, conflicted or not, actually outperform investors on the whole and are better off in commission-based accounts. They also point out that CEA’s analysis isn’t placing a larger price tag on the value human investment advice has for ordinary investors.14

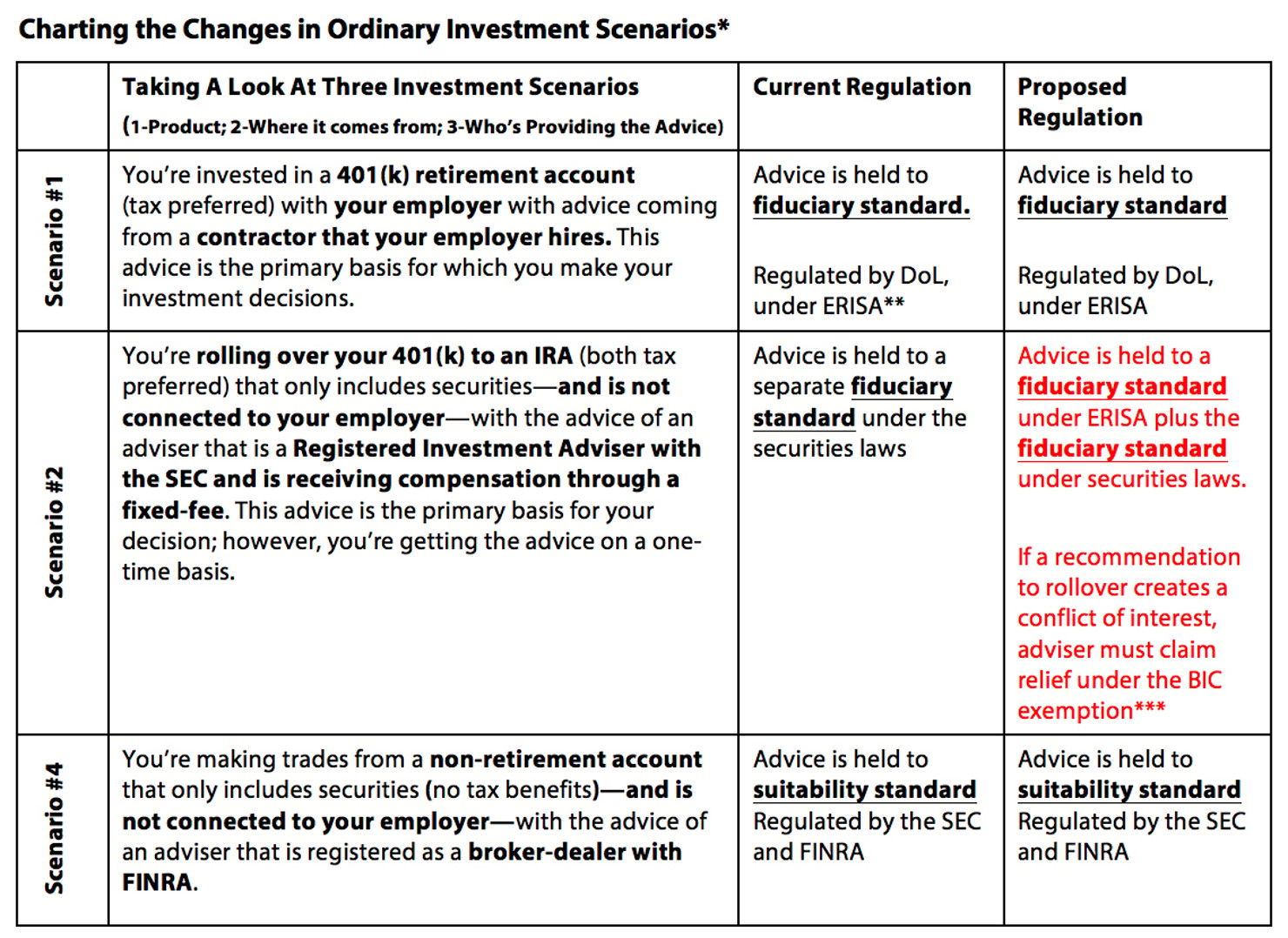

Below, we chart out three ordinary investment scenarios and summarize how the proposed fiduciary rule affects each.

*This chart is meant to illustrate 3 common investment scenarios. This chart does not encompass the full range of scenarios being impacted by this rule.

**ERISA has legal jurisdiction over all retirement savings accounts, but, with the regulations written as they are today, certain advisers are exempt from having to hold their advice to the fiduciary level. In scenarios 1 and 2, it’s important to note that the advice “is the primary basis for your investment decision” (#1) versus the advice “is the primary basis for your decision, but its advice you only use on a one-time basis” (#2). This distinction highlights the 5-part “investment advice” test ERISA currently uses to determine what is considered “investment advice.” If the advice in Scenario #1 was only used on a one-time basis, the advice from the contractor would instead likely be held to the suitability standard since part of the 5-part test isn’t passed.

***In tomorrow’s world, as written, the DoL is throwing the 5-part test out the window and redefining what “investment advice” is so it is broader and covers more interactions. If the adviser is providing any retirement advice—no matter how infrequent it is (i.e. Rollover)—the advice is held to a fiduciary standard. However, there are exemptions. If the adviser has “conflicts” (as defined by ERISA) then the adviser must claim relief under the Best Interest Contract Exemption. This contract states they’ll act in the best-interests of their client, reveal conflicts, and are working to mitigate said conflicts, among other things.

The Sticking Point: The Best Interest Contract Exemption

The goal of DoL’s rulemaking is to eliminate conflicted advice from advisers by redefining what retirement investment advice is. This redefinition essentially means that more interactions with savers will be considered situations where investment advice is provided, meaning more interactions will be subject to ERISA’s fiduciary standard. The DoL recognizes that with this redefinition it will be dramatically reshaping the retirement savings world, especially commissions-based compensation. Instead of completely banning commissions under the rule, DoL proposes that advisers be allowed to continue to receive commissions so long as they enter into a Best Interest Contract (BIC) Exemption. This contract, among other things, must confirm that the adviser is acting in the client’s best interest, is working to mitigate existing conflicts, and reveal any conflicts.

Opponents of the proposed BIC Exemption have four main criticisms:

• Criticism #1—The BIC Exemption isn’t principles-based:

The idea of a BIC Exemption stems from the belief that principles-based regulation is better for investment advice than today’s rules-based approach. Put another way, principles-based regulations focus on general guidelines that must be followed, whereas a rules-based approach focuses on a very prescriptive set of guidelines that must be followed. Even though DoL claims it has proposed a principles-based BIC, critics argue that is not the case.15 As written, the rule is unworkable because it is too cumbersome and expensive to comply with for advisers who receive commissions, critics say.

• Criticism #2—High costs will keep ordinary investors from getting advice:

Critics argue that investment advisers play a valuable role in helping ordinary investors prepare for retirement. They advise investors not to sell during panics or cash out their retirement plans early. They reallocate portfolios when risks in the market change. And they give practical advice and education when it comes to managing one’s financial resources. As written, the critics argue that class-action lawsuits will be much easier to file—primarily due to the disclosure requirements embedded in the BIC Exemption.16 Additionally, getting a company’s paperwork, internal processes and personnel “fiduciary ready” is very costly. This overly cumbersome and confusing rule might result in advisers exiting this market altogether, especially for advisers providing services to small businesses (less than 100 employees).17

• Criticism #3—The DoL Rule inhibits progress on a Uniform Best Interest Standard:

The financial industry has stated that it supports subjecting financial advisers to a best interest standard. Most advisers believe they currently act in their clients’ best interest on a daily basis, irrespective of the legal standard under which they operate. However, opponents posit that the DoL’s standard goes beyond a simple best interest standard. Financial advisers will thus be faced with operating under vastly different standards for retirement accounts as compared to non-retirement accounts. They argue that the better solution would be for the SEC to subject all accounts to a clear, simple, best interest standard.

• Criticism #4—The Best Interest Contract Exemption is unworkable:

The exemption requires new clients to sign a contract before any advice can be delivered. Critics feel this would have a chilling effect on an adviser’s ability to do business and provide essential services like educating prospective clients. Instead of limiting a saver’s choices, critics argue that we should be doing everything in our power to do the opposite.

Supporters of the BIC Exemption feel otherwise:

• Rebuttal #1—A Strong BIC Exemption is the only way to mitigate conflicts:

The only way to weed out conflicts of interest is through a strong BIC. As written, this is a principles-based approach to regulating. The rule still allows for commissions-based business models to exist.18 More importantly, the rule is doing nothing to force businesses to change from a commissions-based relationship with their client—that decision is a business decision.

Retirement savings are a family’s livelihood. If savers get burned on a new car or TV, they lose a few hundred dollars one time. If savers get burned by a poor choice when rolling over a 401(k) to an IRA, that loss could have huge, long-run ramifications. A small loss today might compound into to tens of thousands of dollars 20 years from now. Supporters of the Administration’s rule argues that it is the government’s role to step in and protect investors from getting burned.

• Rebuttal #2—Ordinary investors need products that are in their best interest:

Investors should know if the advice they receive benefits the adviser financially, supporters argue. Because other standards like the suitability standard are deliberately flexible allowing conflicts to exist, it is impossible for consumers to know when someone is providing advice that’s in their best interest.

Supporters argue that by exposing these costs, investors will be better equipped to make decisions about their retirement savings. Supporters also argue that some products currently being offered are incapable of ever being in the best interest of ordinary investors, like non-traded REITs.19

• Rebuttal #3—The financial adviser industry will adapt:

Are those impacted by this rule really going to walk away from billions of dollars’ worth of business because they can no longer provide more lucrative products? Supporters point to the fact that the BIC Exemption isn’t outlawing commissions-based compensation; instead it’s simply telling advisers they must enter into a contract before being compensated in such a manner.

• Rebuttal #4—Consumers can still get education:

An adviser can still learn about the client’s situation and educate the client, so long as no investment advice is provided. The contract would need to be in place before any recommendations are made.20

What’s Next?

The DoL closed its second public comment period on September 24, 2015 after a four-day hearing in August. Some predict that the final rule will be published by early 2016, with it becoming fully enforceable by the time President Obama leaves office in January 2017.