House Budget Committee. “What They Are Saying: President Trump Congratulates House Republicans on Passage of the One Big Beautiful Bill Act.” House Budget Committee, 27 May 2025. https://budget.house.gov/press-release/what-they-are-saying-president-trump-congratulates-house-republicans-on-passage-of-the-one-big-beautiful-bill-act. Accessed 18 March 2026.

Third Way calculations based on Congressional Budget Office. “The Budget and Economic Outlook: 2026 to 2036.” Congressional Budget Office, 11 Feb. 2026, www.cbo.gov/publication/62105. Accessed 18 March 2026.

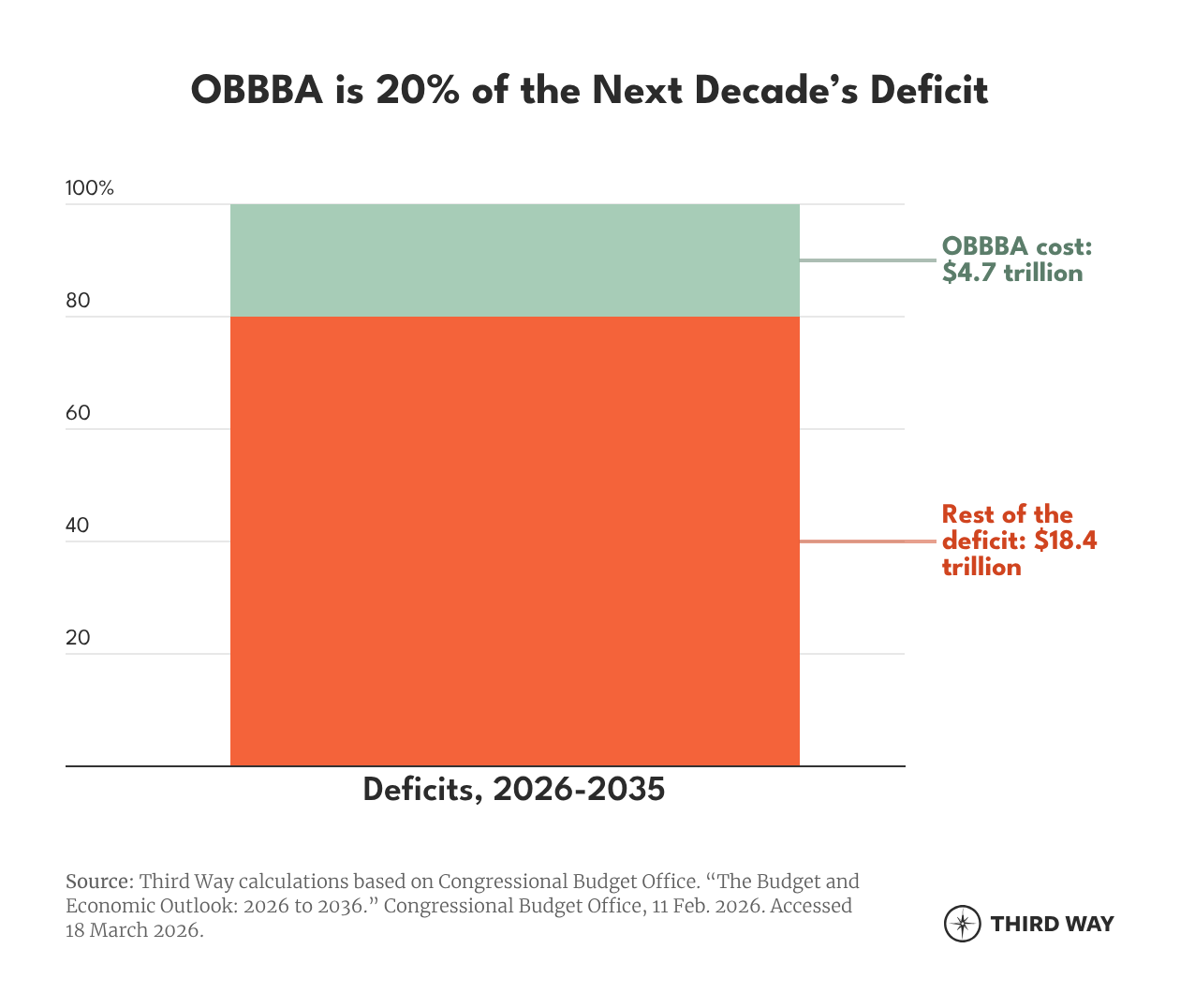

CBO’s $4.7 trillion cost estimate for OBBBA includes the budget effects from FY 2026 through FY 2035. Deficits for the FY 2026-35 budget window are estimated at $23.1 trillion, leading to the 20% of deficits calculation.

CBO’s budget window goes through FY 2036, and these debt and deficit numbers reflect that timeframe.

See Congressional Budget Office. “The Budget and Economic Outlook: 2026 to 2036.” Congressional Budget Office, 11 Feb. 2026, www.cbo.gov/publication/62105. Accessed 18 March 2026.

To be sure, CBO calculates a full budget window out to FY 2036. For the 10-year period of 2027-2036, deficits would total $24.4 trillion.

Congressional Budget Office. “Estimated Budgetary Effects of Public Law 119-21, to Provide for Reconciliation Pursuant to Title II of H. Con. Res. 14, Relative to CBO’s January 2025 Baseline.” Congressional Budget Office, 21 July 2025, https://www.cbo.gov/publication/61570. Accessed 18 March 2026.

Congressional Budget Office. “The Budget and Economic Outlook: 2026 to 2036.” Congressional Budget Office, 11 Feb. 2026, www.cbo.gov/publication/62105. Accessed 18 March 2026.

Congressional Budget Office. “The Budget and Economic Outlook: 2026 to 2036.” Congressional Budget Office, 11 Feb. 2026, www.cbo.gov/publication/62105. Accessed 18 March 2026.

Congressional Budget Office. “The Budget and Economic Outlook: 2026 to 2036, Table 5-1.” Congressional Budget Office, 11 Feb. 2026, www.cbo.gov/publication/62105. Accessed 18 March 2026.

Congressional Budget Office. “The Budget and Economic Outlook: 2026 to 2036, Table 5-1.” Congressional Budget Office, 11 Feb. 2026, www.cbo.gov/publication/62105. Accessed 18 March 2026.

Spectrum auctions made up another 5% of the cuts; reductions to energy-related tax credits made up another 4%.

Congressional Budget Office. “The Budget and Economic Outlook: 2026 to 2036, Table 5-1.” Congressional Budget Office, 11 Feb. 2026, www.cbo.gov/publication/62105. Accessed 18 March 2026.

Supreme Court of the United States, "Learning Resources, Inc. v. Trump, No. 24-1287 (U.S. February 20, 2026)," Supreme Court of the United States, https://www.supremecourt.gov/opinions/25pdf/24-1287_4gcj.pdf. Accessed 18 March 2026.

CBO estimated $3.4 trillion in technical changes attributed to customs duties over the FY 2026-2035 period, nearly $1.3 trillion short of the cost of OBBBA over that same budget window. Estimates released after the SCOTUS ruling showed a revenue reduction of $1.5-$1.8 trillion over that same time period, stemming from the invalidation of the Trump administration’s International Emergency Economic Powers Act (IEEPA) tariffs.

To be sure, the Trump administration is still pursuing tariffs through different parts of federal law, including temporary tariffs under Section 122 of the Trade Act of 1974. Those new temporary tariffs could raise up to $1.3 trillion over 2026-2035, or $1.1 trillion on a dynamic basis. If the tariffs were extended permanently, they could raise up to $2.2 trillion, or $1.9 trillion on a dynamic basis.

CBO also issued an update to its baseline estimates in early March in response to the tariff ruling. It estimates an increase in total deficits of $2.0 trillion over the period of FY 2026-2036, including a $1.6 trillion increase in primary deficits and $400 billion in debt-servicing costs. This update does not include the effects of new Section 122 tariffs.

For more information, see Committee for a Responsible Federal Budget, "SCOTUS Tariff Ruling Could Add $2.4 Trillion to the Debt," Committee for a Responsible Federal Budget, 20 February 2026, https://www.crfb.org/blogs/scotus-tariff-ruling-could-add-24-trillion-debt. Accessed 18 March 2026. And; Committee for a Responsible Federal Budget, "How Much Will Trump’s New 10% (or 15%) Tariffs Raise?" Committee for a Responsible Federal Budget, 4 March 2026, https://www.crfb.org/blogs/how-much-will-trumps-new-10-or-15-tariffs-raise. Accessed 18 March 2026. And; Congressional Budget Office, "An Update About CBO’s Projections of the Budgetary Effects of Tariffs," Congressional Budget Office, 5 March 2026, https://www.cbo.gov/publication/62210. Accessed 18 March 2026. And; Tax Foundation, "Trump Tariffs & Trade War: Tariff Tracker," Tax Foundation, 13 March 2026, https://taxfoundation.org/research/all/federal/trump-tariffs-trade-war/. Accessed 18 March 2026. And; The Budget Lab at Yale, "State of U.S. Tariffs: SCOTUS Ruling Update," The Budget Lab at Yale, 20 February 2026, https://budgetlab.yale.edu/research/state-us-tariffs-scotus-ruling-update. Accessed 18 March 2026. And; The Budget Lab at Yale, "State of Tariffs: February 21, 2026," The Budget Lab at Yale, 21 February 2026, https://budgetlab.yale.edu/research/state-tariffs-february-21-2026. Accessed 18 March 2026.

Congressional Budget Office. “The Budget and Economic Outlook: 2026 to 2036.” Congressional Budget Office, 11 Feb. 2026, www.cbo.gov/publication/62105. Accessed 18 March 2026.

The Congressional Budget Office (CBO) estimates that the 2025 reconciliation act would boost real GDP by an average of 0.7% annually over the 2025-2034 period relative to its baseline. In the near term, this growth is driven primarily by increased demand for goods and services, which also puts modest upward pressure on inflation and lowers the unemployment rate. Over the longer term, economic gains are expected to come from increases in labor supply, investment, and productivity. However, the stronger economic activity and higher federal borrowing associated with the law also lead to higher interest rates throughout the period.

Despite modest macroeconomic benefits, the law is still projected to substantially increase deficits. Before accounting for macroeconomic feedback, deficits would rise by about $4.1 trillion over the 2025-2034 period; with feedback effects included, the increase is slightly larger—$4.2 trillion—because higher interest costs more than offset deficit reduction from stronger growth. While macroeconomic changes are estimated to reduce primary deficits by $280 billion through higher revenues, those gains are outweighed by a $405 billion increase in net interest costs, driven largely by higher rates and a rising debt-to-GDP ratio—for a net deficit-increasing effect of $125 billion.

In short: The bill’s short-term growth effects partly come from demand, but its long-term effects are dampened by crowding out. OBBBA amplifies an existing drag on long-term growth, even as it boosts demand in the short run.