Report Published February 1, 2017 · Updated February 1, 2017 · 30 minute read

Post-Corporate: the Disappearing Corporation in the New Economy

WHAT’S NEXT?

Every day the news media reports what has happened on the stock market. Big swings, in either direction, are big news, because the overall health of the market is an important indicator of what is happening in the broader economy. Thus, it is critical that policymakers understand what has been happening to the stock market itself. A new paper by Jerry Davis describes a startling trend—“For the past 20 years, public corporations in the United States have been disappearing. The number of U.S.-based companies listed on Nasdaq and the New York Stock Exchange has dropped by over half since 1996.” And while the dot.com bust and the financial crisis had something to do with this, the trends have continued. “The number of new entrants,” Davis writes, “does not come close to matching the exits.”

The questions are: Why? and Does it matter? In a carefully argued essay, Davis looks at the kinds of companies that have exited the stock market. The simple answer, over-regulation, cannot explain the decline. The more fundamental explanation is that there has been a change in the kind of businesses we are creating today; they have more access to other forms of capital, firms no longer need to build assets because they can rent them, and thus, “Scaling up and scaling down, are much simpler than they were in the heyday of the traditional corporation.” Davis concludes that “the public corporation was an ideal vehicle for the 20th-century economy, characterized by long-lived assets and economies of scale. But it is increasingly out of sync with the 21st-century economy.”

The disappearance of the corporation, however, is not without consequences. “The firms that have gone public since 2000 rarely create employment at a large scale; the median firm to IPO after 2000 created just 51 jobs globally.” “In 2015,” Davis writes, “the combined workforces of Facebook, Yelp, Zynga, LinkedIn, Zillow, Tableau, Zulily and Box were smaller than the number of people who lost their jobs when Circuit City was liquidated in 2009.”

Moreover, the old-fashioned corporation served a social purpose. It was the source of long career ladders and stability, of health care and retirement savings for millions. Davis doesn’t think the old corporation is coming back, which poses a big question for policymakers— how do we promote economic security and mobility in a post-corporate economy?

“Post-Corporate” is the latest in a series of ahead-of-the-curve, groundbreaking pieces published through Third Way’s NEXT initiative. NEXT is made up of in-depth, commissioned academic research papers that look at trends that will shape policy over the coming decades. Each paper dives into one aspect of middle class prosperity—such as education, retirement, achievement, or the safety net. We seek to answer the central domestic policy challenge of the 21st century: how to ensure American middle class prosperity and individual success in an era of ever-intensifying globalization and technological upheaval. And by doing that, we’ll be able to help push the conversation toward a new, more modern understanding of America’s middle class challenges—and spur fresh ideas for a new era.

Jonathan Cowan

President, Third Way

Dr. Elaine C. Kamarck

Resident Scholar, Third Way

***

Introduction

In 2015, the combined global workforces of Facebook, Yelp, Zynga, LinkedIn, Zillow, Tableau, Zulily, and Box were smaller than the number of people who lost their jobs when Circuit City was liquidated in 2009. Throw in Google, and it was still less than the number who worked at Blockbuster in 2005.1

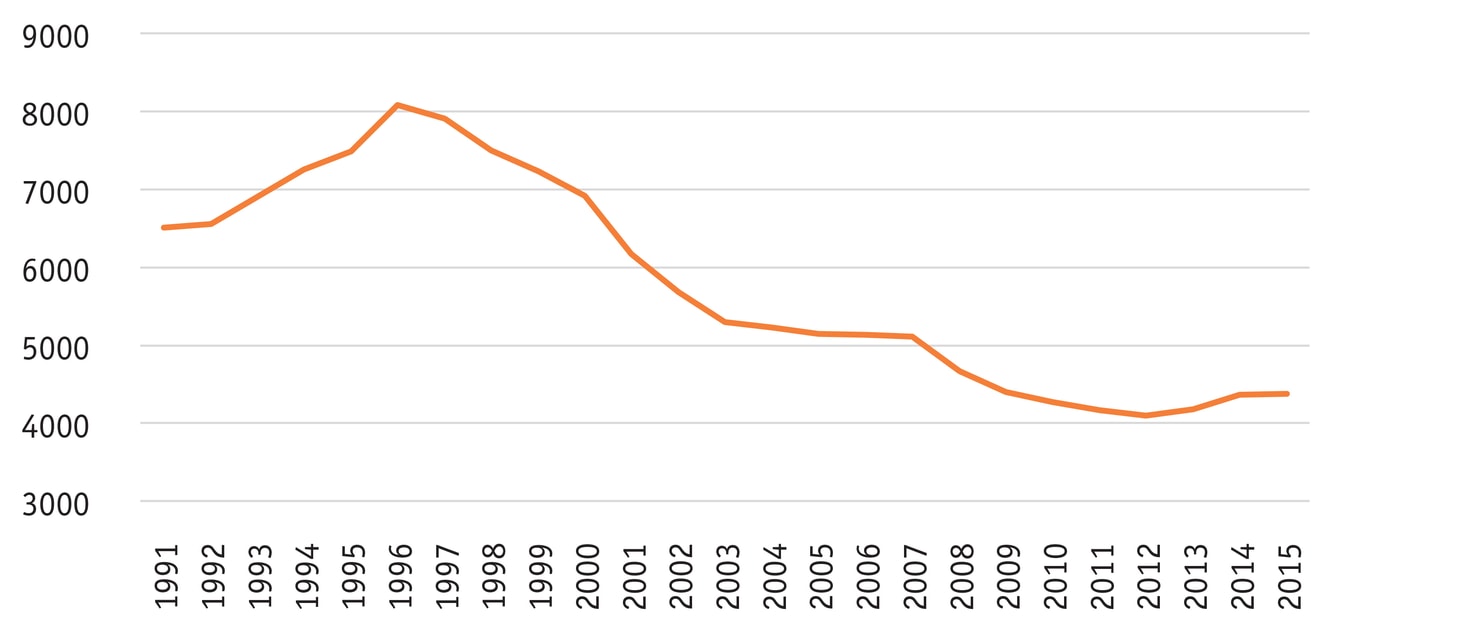

For the past 20 years, public corporations in the United States have been disappearing. The number of U.S.-based companies listed on Nasdaq and the New York Stock Exchange has dropped by over half since 1996. The dot-com bust of 2000 and the financial crisis of 2008 account for some of this decline, yet the downward trend has continued with little let-up, even as the markets have reached record highs. The number of IPOs in the past five years is less than the number in 1996 alone. Something has gone wrong with the public corporation in the United States.

Figure 1: American corporations listed on U.S. stock markets, 1991-2015

Source: World Bank

Why are corporations disappearing? And should we care? Certainly, America’s financiers and CEOs are worried. The leaders of the biggest institutional investors (BlackRock, Vanguard, Fidelity, and others); the CEOs of GE, GM, Verizon, and JP Morgan Chase; and Berkshire Hathaway’s Warren Buffett met in July 2016 to consider what has gone wrong with corporate America. They subsequently released an open letter that began: “The health of America’s public corporations and financial markets—and public trust in both—is critical to economic growth and a better financial future for American workers, retirees, and investors.”2 The group proposed a set of what they termed “commonsense principles of corporate governance” aimed at restoring trust in the corporation and, presumably, encouraging more firms to go public.3 Yet, by some standards, corporate governance has never been better, and it is hard to see, however worthy it may be to add more independent directors to corporate boards, or treat stock options as an expense, that this will fix what ails the American corporation. The problem is much more fundamental than issues of corporate governance.

In this paper, I examine which public corporations have vanished, where new ones are coming from, and why we don’t have more. I analyze comprehensive data on publicly listed corporations, initial public offerings (IPOs), and de-listings, and describe which industries have lost the most public firms, and why. I also describe some of the social consequences of the vanishing corporation. To telegraph my conclusion, the public corporation was an ideal vehicle for the 20th- century economy, characterized by long-lived assets and economies of scale. But it is increasingly out of sync with the 21st century economy. Public policy needs to take the new shape of the economy seriously if it hopes to create “economic growth and a better financial future for American workers.”

What kinds of corporations left the markets?

To explain the shrinking number of listed corporations, we need to examine both the disappearance of existing companies and their limited replacement with new entrants. Some of the firms that have left the market are household names. Enron and Worldcom imploded during the wave of fraud that accompanied the dot-com collapse. Lehman Brothers, Wachovia, Washington Mutual, and Countrywide were wiped out during the financial meltdown of 2008. Safeway and Albertsons were taken private by private equity firms, and may eventually go public again. Borders and Circuit City were liquidated, unable to compete with Amazon. We have also seen the emergence of a number of new entrants and new industries such as web search (Google), social media (Facebook), and various IT-enabled services (e.g., Yelp). Many newer startups (Uber, Lyft, AirBnb) have stayed private, although they could have fueled a flourishing IPO market. But these high-visibility examples may not represent the larger trends. To understand broad changes in the market we need more systematic data.

To discover which industries contributed the most losses, I analyzed data on all U.S.-based corporations listed on Nasdaq and the New York Stock Exchange from 2000 onwards. Data came from the Center for Research on Securities Prices (CRSP) and Compustat, gathered from the Wharton Research Data Services.4 Data from CRSP distinguish mergers from other reasons for leaving the market, such as liquidations and bankruptcies, but in practice these are often related, as firms in rapid decline are often snapped up by acquirers. For the purpose of this article, firms leaving the market are divided into those that left due to merger and those that were delisted for other reasons (particularly bankruptcy and going private).

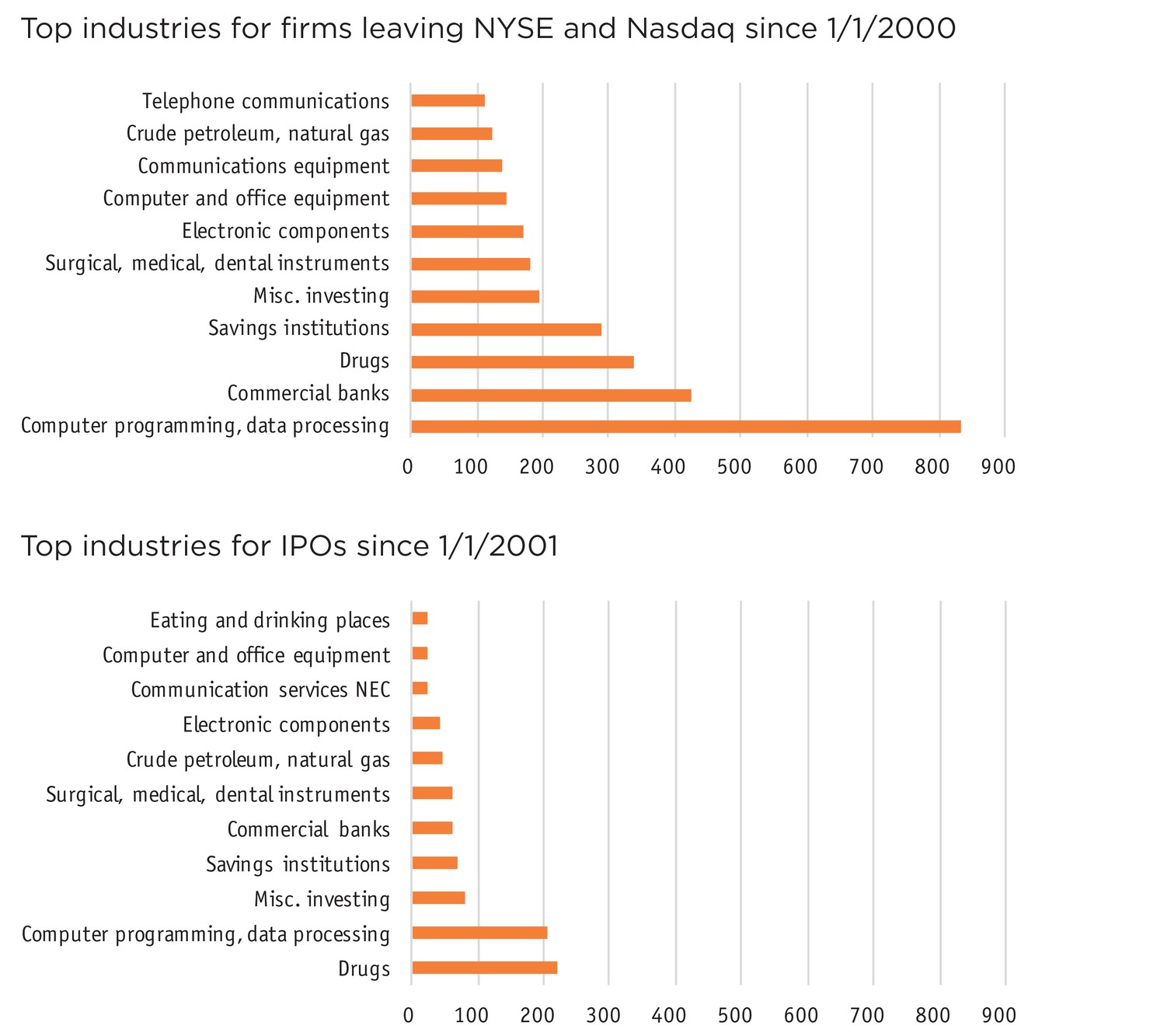

Figure 2 compares those industries that have seen the greatest number of exits from Nasdaq and the New York Stock Exchange since the beginning of 2000 and those that have contributed the most IPOs since the start of 2001. (2000 was a transitional year, with both a large number of IPOs early on and a large number of exits after the Nasdaq crash that began in March.) There is considerable overlap among the lists, with software, drugs/biotech, and banking providing the largest sources of both entries and exits. But it is also evident that exits far outstripped entries in each of these sectors.

Figure 2: Top industries for stock market exits and entrants since 2000

Source: Center for Research on Securities Prices

Time series data on the reasons for exit in each industry provide a more fine-grained picture. In short, the burst of the Internet bubble in 2000 was by far the biggest single source of de-listings, with large-scale departures among firms in software and telecoms. Banking saw a long-delayed and ongoing wave of consolidation beginning in the mid-1990s, as well as a spate of bank failures during the 2008 financial crisis. The computer and electronics manufacturing industry was largely offshored in the early part of the new century, although many of the big brands still design and market in the U.S. And the pharmaceutical industry has seen both consolidation and a large number of acquisitions in biotech and medical devices. In every case, the number of new entrants does not come close to matching the exits: there is little reason to expect hundreds of new software firms or commercial banks to list on the markets in the foreseeable future.

Burst of the internet bubble

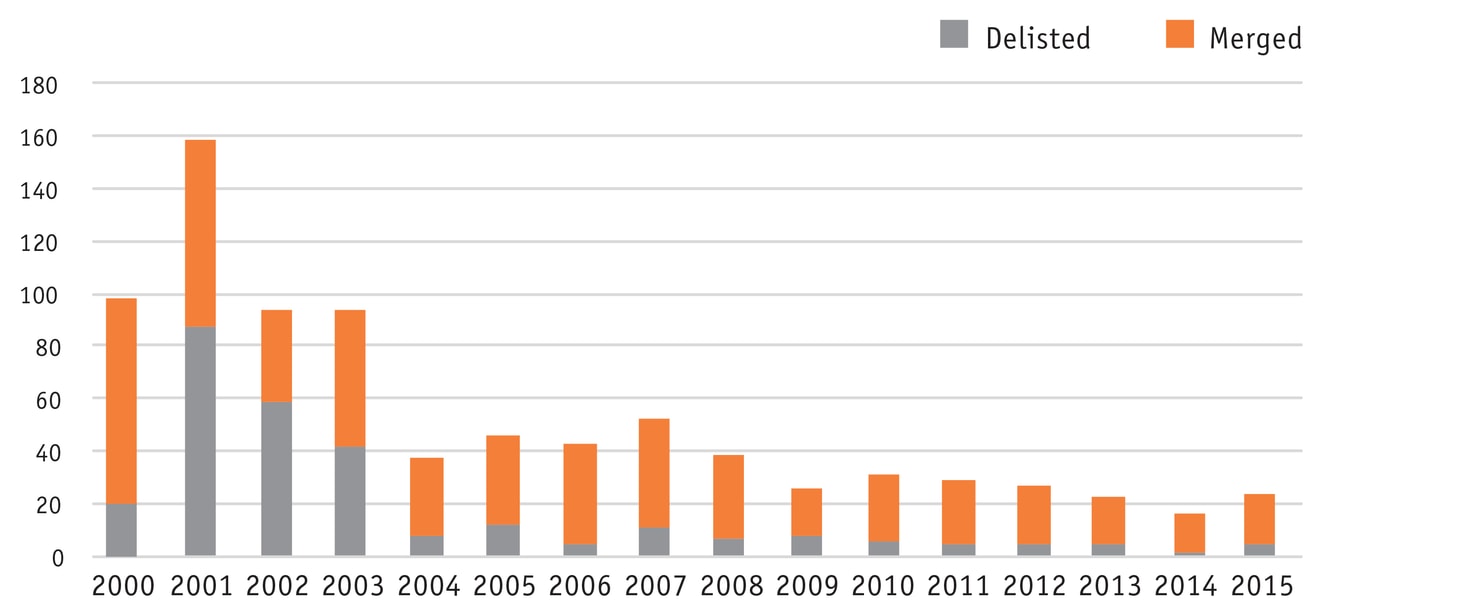

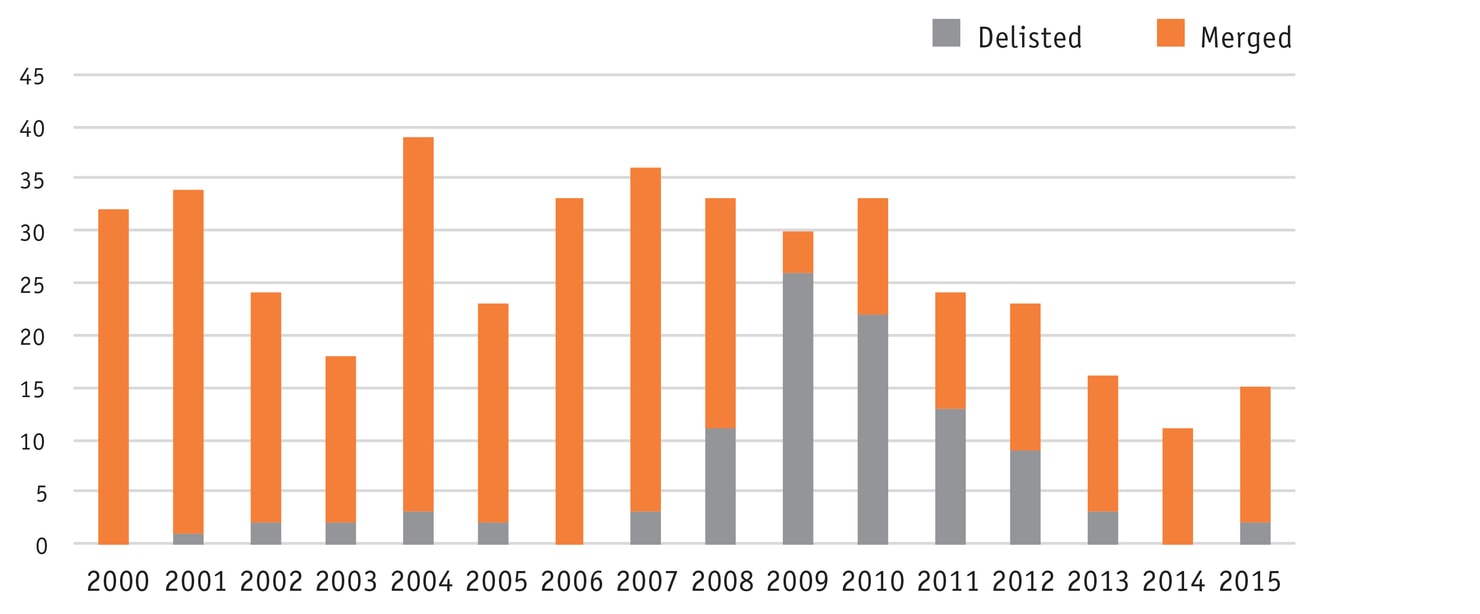

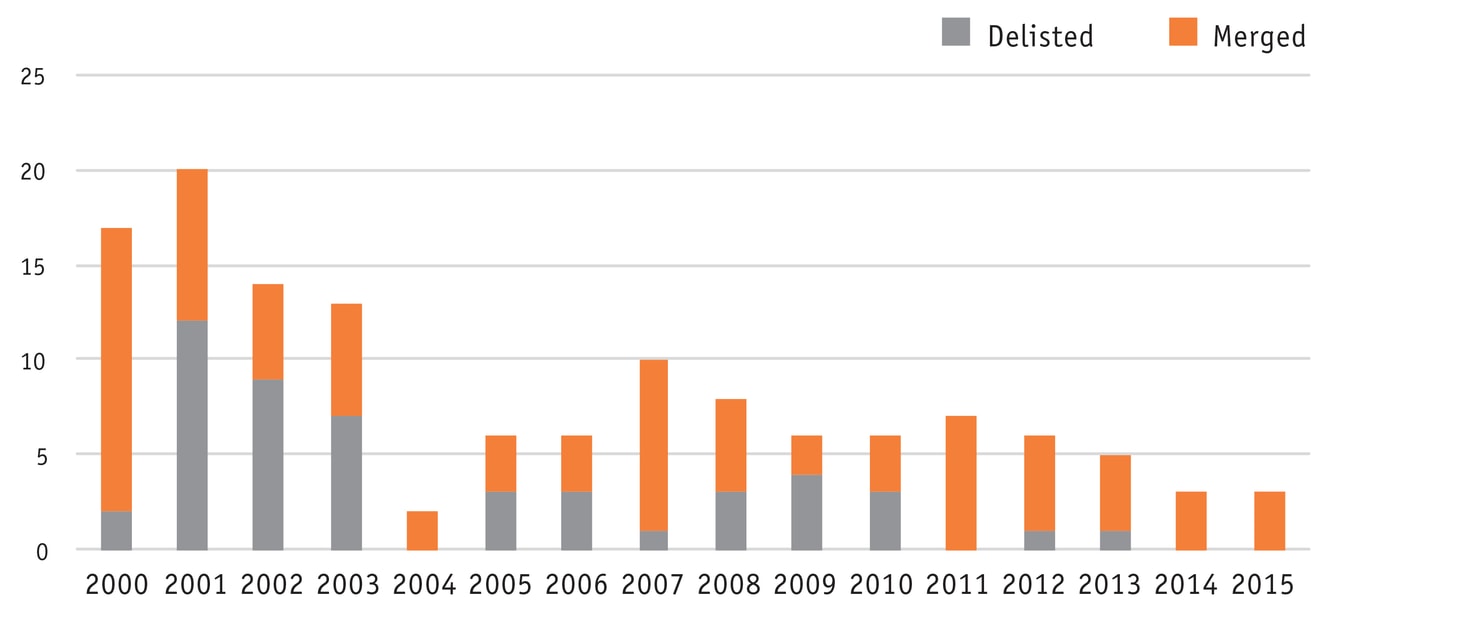

By far the biggest source of exits from the market was in software and online services (SIC code 737, “Computer programming and data processing”). As Figure 3 shows, the dot-com collapse that started in March 2000 led to hundreds of firms leaving the market between 2000 and 2003, most due to de-listings. Leavers included firms like DrKoop.com, Lycos, and the late, lamented Pets.com.

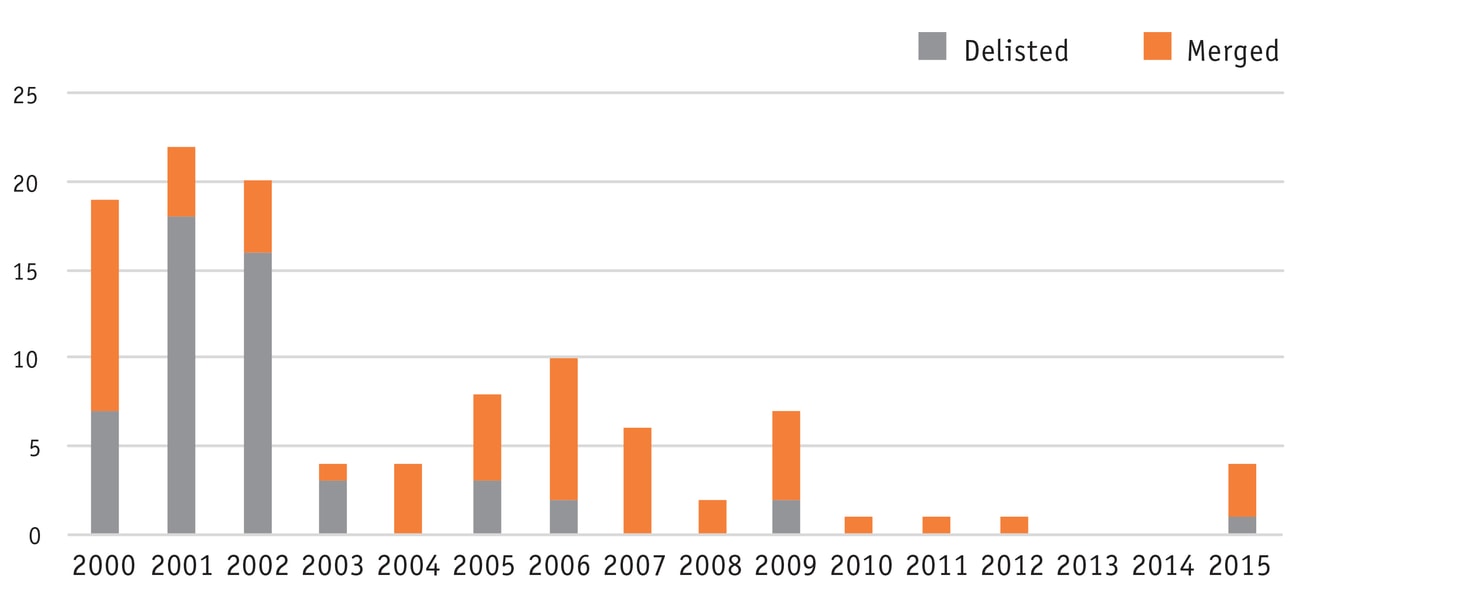

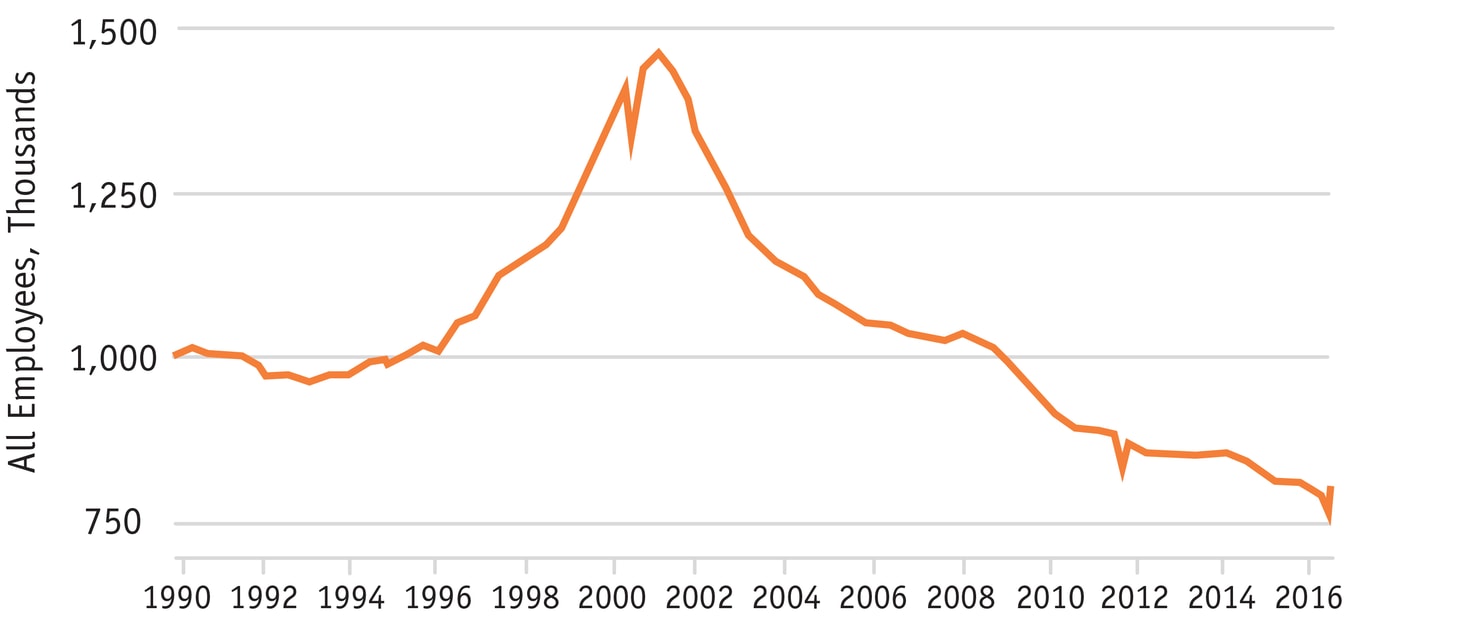

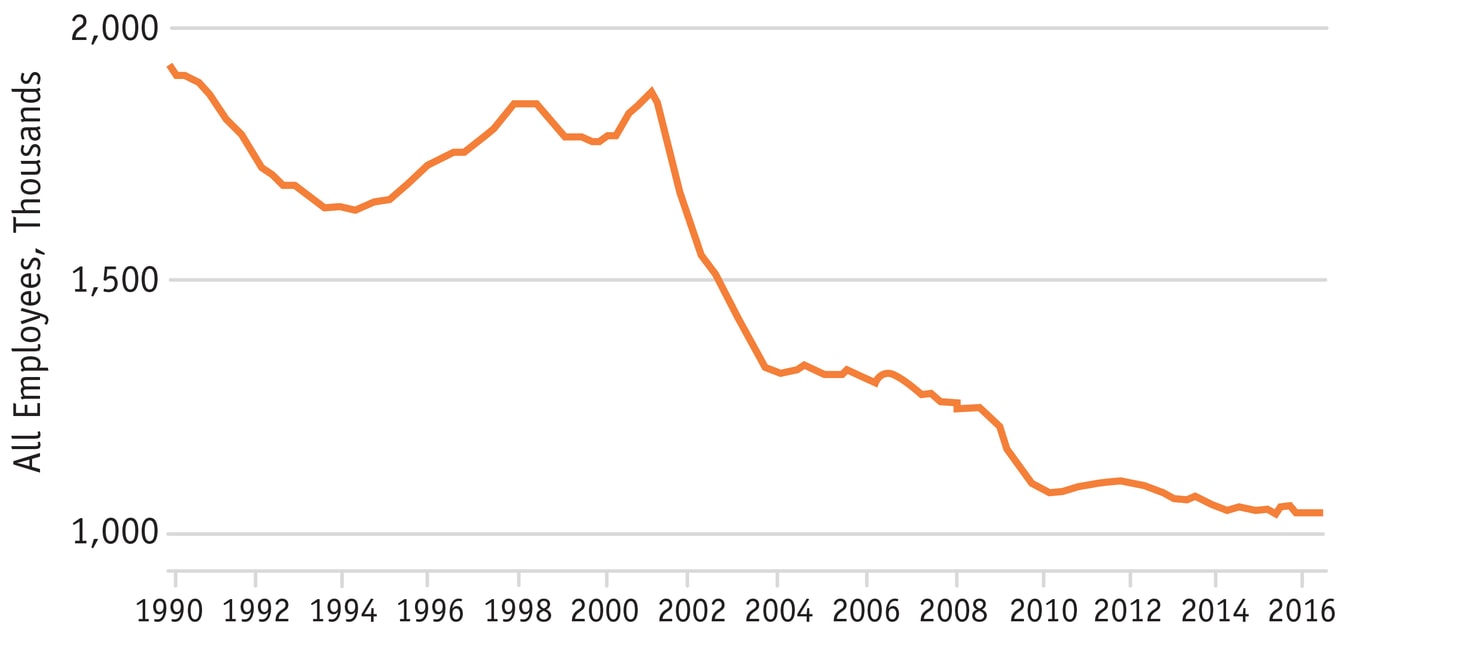

Software and online services was not the only industry affected, however, as the telecom industry (SIC codes 481, “Telephone communications”) saw dozens of exits during this period, including Adelphia, Worldcom, and Williams Communications. Between them, the firms in these two industries accounted for nearly one-fifth of the market departures since 2000. As Figure 5 shows, telecoms saw a dramatic boom in employment leading up to the turn of the century, and an even more dramatic decline since, with little sign of recovery.

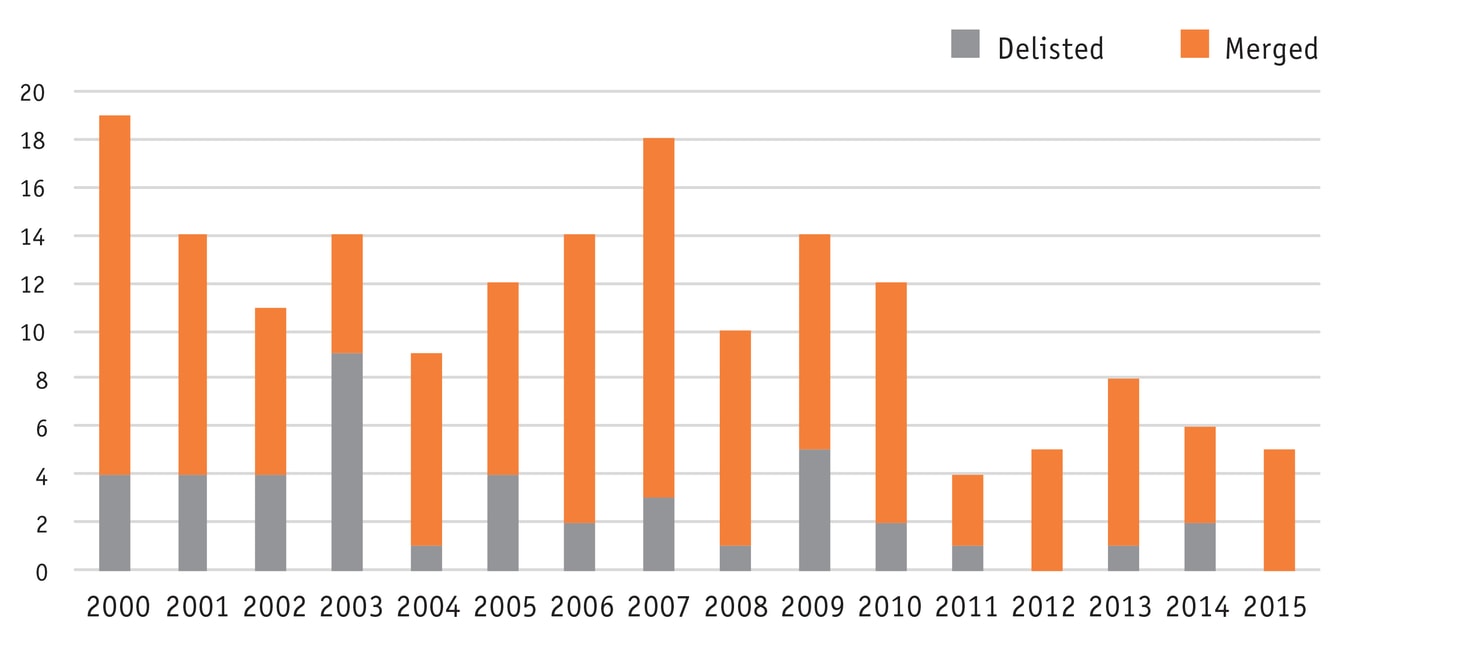

Figure 3: Mergers and delistings, 2000-2015: Computer programming and data processing

Figure 4: Mergers and delistings, 2000-2015: Telephone communications

Figure 5: Employment in Telecommunications, 1990-2016

Source: Bureau of Labor Statistics

Consolidation and collapse in banking

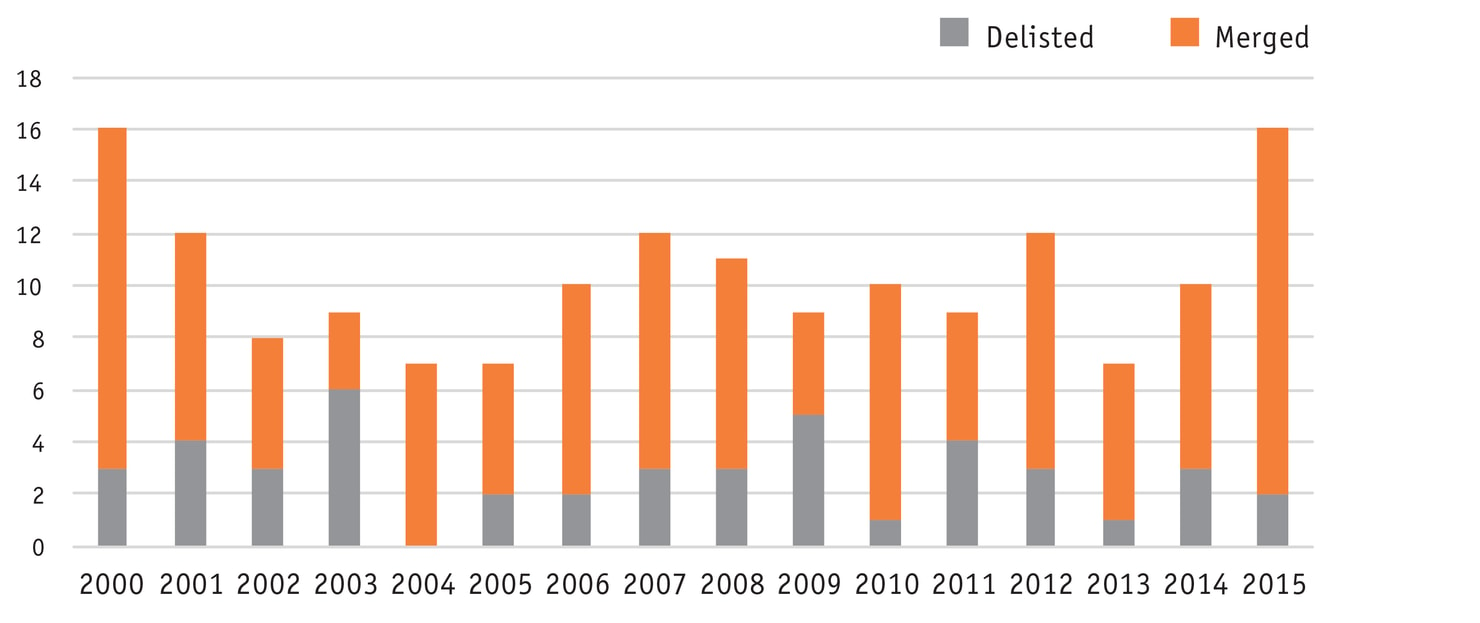

Banking (SIC code 602, “Commercial banks” and SIC code 603, “Savings institutions”) has seen nearly continuous exits from the markets since 2000. Prior to 2008, this was overwhelmingly due to industry consolidation through mergers. The U.S. has historically had a wildly fragmented banking system. After the financial reforms of the 1930s, investment banking (underwriting and dealing in securities) was legally separated from commercial banking (making loans to businesses), and commercial banks continued to be constrained to operate at a state level rather than a national level. Savings banks (which primarily lent to consumers for mortgages) were also relatively small and localized. Thus, the U.S. had more than 12,000 commercial banks and more than 4,000 savings banks in 1980.5 By comparison, Canada’s banking system was dominated by a mere half-dozen major national players.

The Riegle-Neal Act of 1994 allowed banks to acquire competitors across state lines, and the repeal of Glass-Steagall in 1999 allowed commercial banks and investment banks to combine. As a result, America’s banking industry underwent a long-delayed consolidation through a vast wave of mergers, which ultimately yielded the Big Four “universal banks” of today: JP Morgan Chase, Citigroup, Bank of America, and Wells Fargo. Each does both investment banking and commercial banking and operates branches nationwide—something that would have been legally forbidden 25 years ago. Because of the sheer number of banks in the U.S., consolidation has been a generation-long project, resulting in a continuous decline in the number of listed banks.

In 2008, the mortgage meltdown led to a wave of bank failures not seen since the 1930s, further shrinking the industry’s footprint in the markets. Along with the disappearance of big investment banks like Bear Stearns, Lehman Brothers, and Merrill Lynch, both commercial and savings banks (Wachovia, Washington Mutual) and free-standing mortgage providers (Countrywide, New Century) either failed or were forced into mergers. One legacy of this movement is that American banking is more concentrated today than it has ever been in its history.6

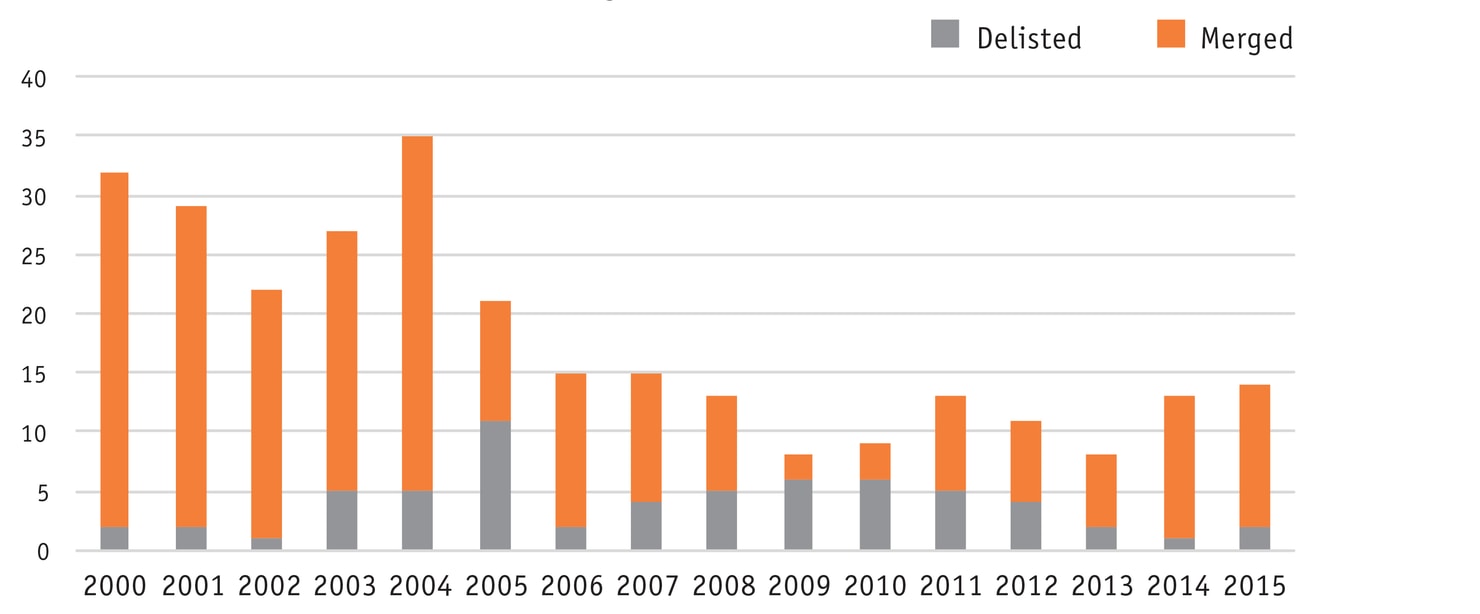

Figure 6: Mergers and delistings, 2000-2015: Commercial banks

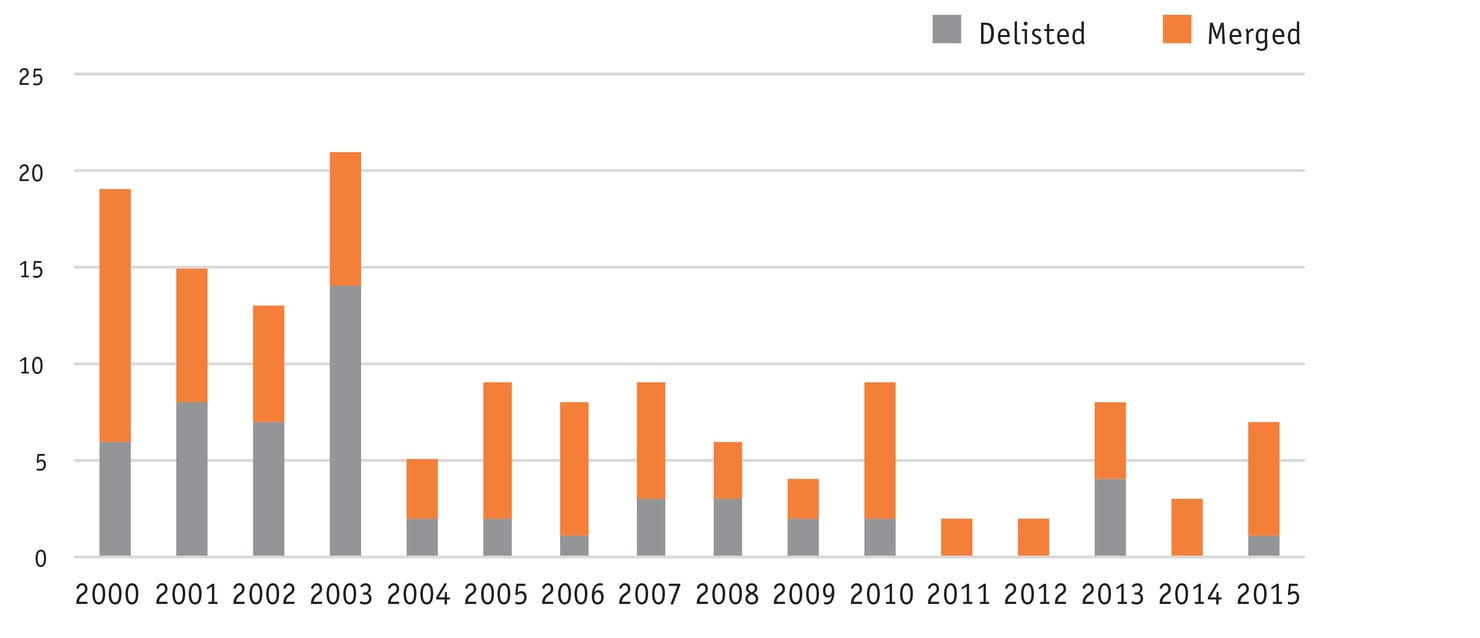

Figure 7: Mergers and delistings, 2000-2015: Savings institutions

Offshoring of electronics

The computer industry (SIC code 357, “Computer and office equipment”), communications equipment (SIC code 366, “Communications equipment”), and electronic components such as semiconductors (SIC code 367, “Electronic components and accessories”) have seen both consolidation (e.g., HP’s acquisition of Compaq) and large-scale business failures since 2000. One factor underlying these dynamics is the nearly universal offshoring of electronics manufacturing and assembly. Figure 11 shows total U.S. employment in the “Computer and electronic products” industry. (The Bureau of Labor Statistics uses its own industry classification scheme that combines computers, electronic products, and communications equipment into a single large category.) Note the precipitous drop in employment between the end of 2000 and the end of 2003, when U.S. jobs in this sector declined by over 500,000. Since the turn of the century, employment in electronics manufacturing has declined by 44%. Research by economist Susan Houseman and colleagues confirms that, although U.S. brands like Apple, Hewlett Packard, and Dell continue to have large market shares, production is done overwhelmingly by overseas vendors such as Foxconn. The U.S. still has significant capacity in high-end semiconductors, but the center of gravity in electronics production now is China.7

As we will see, one of the reasons there are fewer IPOs today is that—like the garment industry—industry players in electronics find it less costly to hire turnkey manufacturing service providers overseas rather than building their own factories.

Figure 8: Mergers and delistings, 2000-2015: Computer and office equipment

Figure 9: Mergers and delistings, 2000-2015: Communications equipment

Figure 10: Mergers and delistings, 2000-2015: Electronic components and accessories

Figure 11: Employment in computer and electronic products, 1990-2016

Source: Bureau of Labor Statistics

The pharma vortex

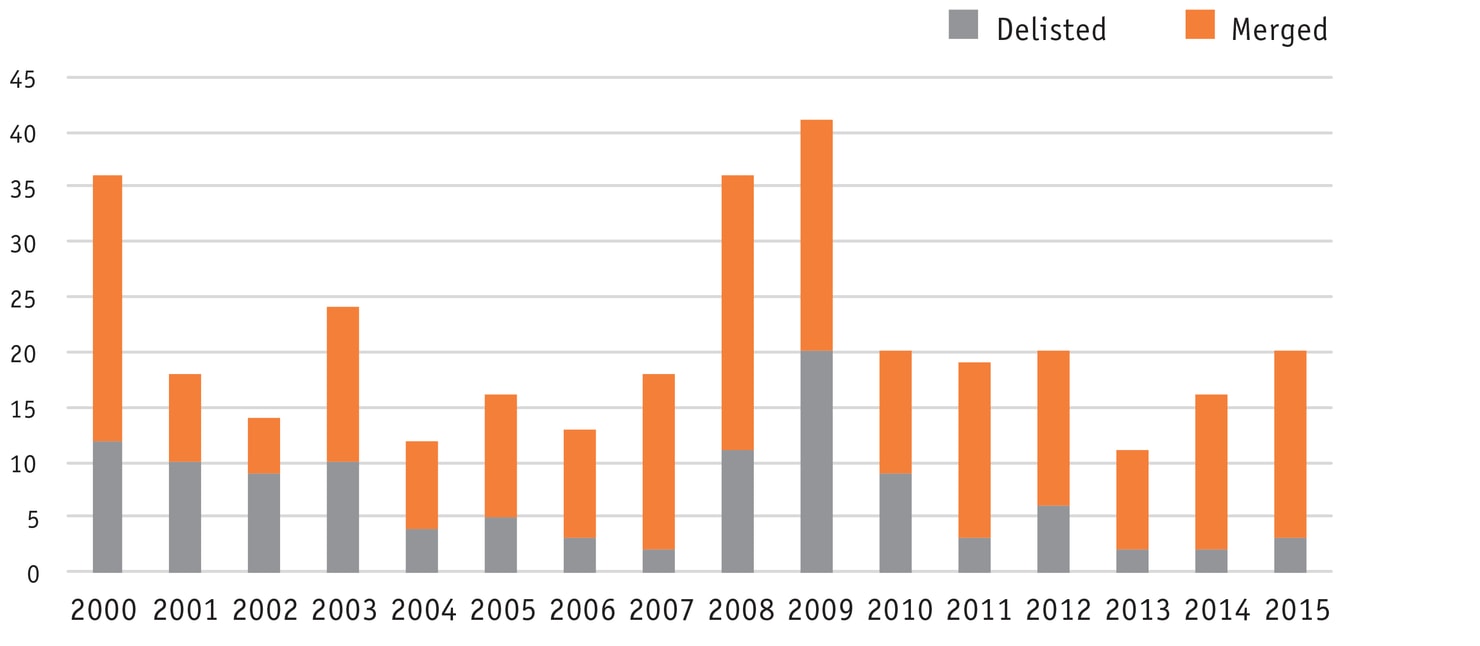

The fourth broad sector that contributed to the decline in listed firms in the U.S. is drugs and medical devices. The “Drugs” industry (SIC code 283) includes both traditional pharmaceutical firms like Pfizer (SIC code 2834, “Pharmaceutical preparations”) and biotech firms like Amgen (SIC code 2836, “Biological products, except diagnostic substances”). Like banking, pharma has seen substantial consolidation and concentration. For example, Pfizer acquired pharmaceutical giants Warner-Lambert (2000), Pharmacia (2003), and Wyeth (2009), along with a number of smaller biotech firms. Pharma firms have also been active in acquiring medical device firms (SIC code 384, “Surgical, medical, and dental instruments”). For instance, in summer 2016, Abbott announced plans to acquire pacemaker manufacturer St. Jude Medical.8 In some sense, biotech and medical devices are the “farm team” for pharma: when risky startups mature, they are often bought by large pharmaceutical companies.

Figure 12: Mergers and delistings, 2000-2015: Drugs (pharmaceuticals; biotech)

Figure 13: Mergers and delistings, 2000-2015: Surgical, medical, and dental instruments

A handful of large pharma companies have also merged with a smaller foreign company. This legal practice, called an inversion, entails merging with an overseas company and retaining foreign incorporation status for tax reasons. Ireland is a particularly popular legal domicile for firms whose value derives from intellectual property. Pharma companies that have merged with an Irish company in recent years include Actavis (which subsequently acquired U.S.-based Allergan, Inc. and changed its name to Allergan PLC), Perrigo, and several smaller players. Medical device maker Medtronic also merged with Covidien, itself a spinoff of (Ireland-based) Tyco International. Pfizer recently sought to buy Allergan and change its legal domicile to Ireland but backed out in April due to new Treasury rules aimed at curbing inversions. Although inversions are not sufficient to explain a large part of the loss of U.S.-based listings, Ireland’s tax advantages have lured several big names outside of pharma, including Accenture, Cooper Industries, Eaton, Ingersoll-Rand, Seagate, and Trane.

It is notable that there is no single explanation for why firms leave the markets. Rather, each of the four sectors with the biggest loss of U.S. listings has its own unique story, pointing to different “culprits”: the burst of the Internet bubble; the de-regulation of finance; offshoring and the growth of China as a manufacturing hub for electronics; and economies of scale that encourage consolidation in pharmaceuticals. It is also worth nothing that in many cases, companies that went private or bankrupt returned to the market (e.g., General Motors, along with several of its big suppliers). Sometimes this happens repeatedly, as with US Airways, which went bankrupt and was delisted in 2002, returned to the markets in 2003, went bankrupt and was delisted again in 2004, merged with America West in 2005 (which re-branded as “US Airways”), and was acquired by American Airlines in 2013. Indeed, the prospect of going public again is essential to many or most going-private transactions.

The muted market for IPOs after 2000

IPOs are often portrayed as a milestone of success in the life of a startup, and the vitality of the IPO market is an indicator of the health and future prospects of the underlying economy. Yet the IPO market in the U.S. has never returned to the manic pace of the 1990s.

Normally, the number of IPOs rises and falls with the broader stock market. A bull market is an inducement for firms to go public. Yet, although the market has been on a tear since it bottomed out in 2009, there were fewer IPOs from 2011 to 2016 than there were in 1996 alone. Market indices reached record highs in 2016, yet it has been the slowest year for IPOs since before the crash in 2009.9

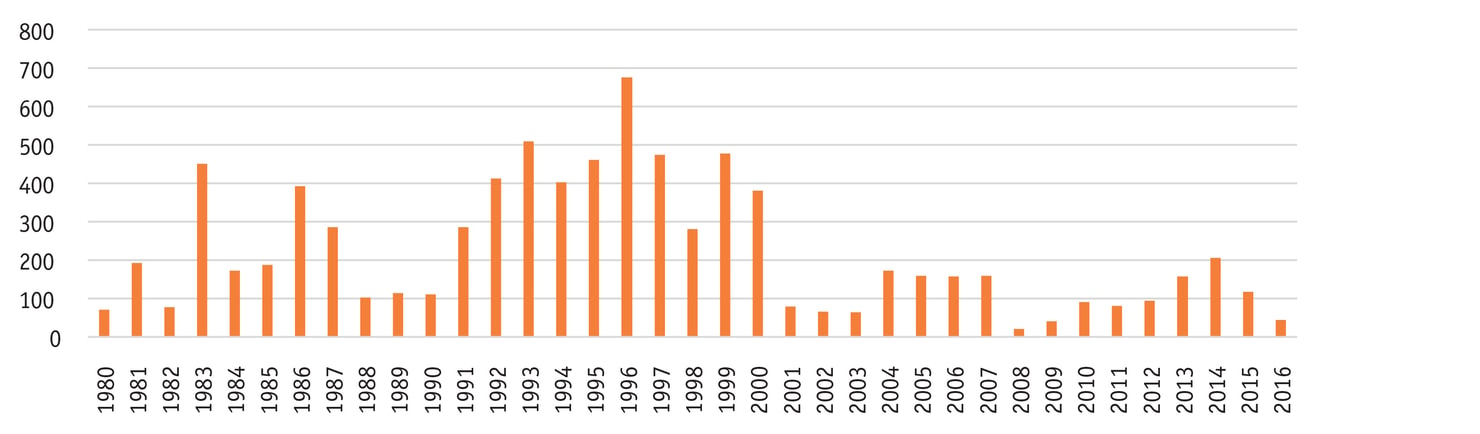

Figure 14: U.S. initial public offerings per year, 1980-2016

Source: Prof. Jay Ritter, University of Florida, and New York Times

What’s behind the IPO drought? Some commentators point to the financial regulations that followed the dot-com collapse—particularly the Sarbanes-Oxley Act of 2002—and the Dodd-Frank Act that followed the 2008 financial meltdown. Critics believe that these acts, aimed at protecting investors, went too far and raised costly barriers to going public. Marc Andreessen, co-founder of Netscape and now a venture capitalist, said: “The irony of Sarbanes-Oxley was that it was intended to prevent more Enrons and Worldcoms, but it ended up being a gigantic tax on small companies ... The compliance and reporting requirements are extremely burdensome for a small company. It requires fleets of lawyers and accountants who come in and do years of work ... It’s biased enormously toward companies that are big enough to hire fleets of lawyers and accountants, biased against companies that are very young and for whom there’s still a lot of variability.”10

Government over-regulation is a popular scapegoat among those who would prefer more autonomy. In this case, however, we have convincing counter-evidence. In April 2012, President Obama signed the JOBS (Jumpstart Our Business Startups) Act, which allowed “emerging growth” firms (those with less than $1 billion in revenues) to go public with substantially lower disclosure and regulatory requirements. Well over 90% of firms that go public have revenues below $1 billion. If over-regulation is the issue, then the JOBS Act should have yielded a flood of IPOs. Instead, if anything, the market is even more muted. One study found that the JOBS Act increased the annual number of IPOs by just 21 over what would have been expected.11 Moreover, biotech is the single biggest source of IPOs since the passage of the JOBS Act. If the aim was to create jobs, then biotech is clearly the wrong place to look: the median biotech firm in 2015 had just 61 employees.12

Andreessen points to another factor discouraging firms from going public: the demands of activist investors and short-sellers. He notes: “[F]or young companies, everything is connected: stock price, employee morale, ability to recruit new employees, ability to retain employees, ability to sign customer contracts, ability to raise debt financing, ability to deal with regulators. Every single part of your business ends up being connected, and it ends up being tied back to your stock price.”13 For small firms, the volatility of the markets since 2008 may simply create too much uncertainty to be worth it.

The markets have indeed become more demanding for listed firms. The Economist noted in 2015 that 15% of the S&P 500 had been targeted by activists since the financial crash. “Since 2011 activists have helped depose the CEOs of Procter & Gamble and Microsoft, and fought for the break up of Motorola, eBay and Yahoo ... They have won board seats at PepsiCo, orchestrated a huge round of consolidation across the pharmaceutical industry, and taken on Dow Chemicals and DuPont."14 It is clear that public firms of all sizes face daunting demands that raise substantial barriers to listing on a stock market

In short, over-regulation cannot explain the muted IPO market, and activist investors have perhaps raised the bar for going public. But this still does not explain the drastic absolute decline in listed corporations.

What explains the declining number of corporations in the U.S.?

It is worth asking why we have public corporations in the first place. Why are firms funded by stock markets? Public corporations grew up in the U.S. with the railroads and expanded with large-scale manufacturers (US Steel, General Motors), infrastructure firms (AT&T), and retailers (Sears). In each case, the vast scale of operations required large investments in assets like real estate, rolling stock, factories, and stores. If the cheapest way to make cars is in giant vertically integrated factories in Detroit, then the stock market is a good way to raise capital to build those factories and hire people to staff them, and the public corporation is an ideal vehicle to raise the funds.

But the corporations going public today often have very little in the way of dedicated assets. Even global giants like Facebook do not go public primarily to fund their operations. Consider what Facebook’s prospectus reveals under “Use of proceeds”:

“The principal purposes of our initial public offering are to create a public market for our Class A common stock and thereby enable future access to the public equity markets by us and our employees, obtain additional capital, and facilitate an orderly distribution of shares for the selling stockholders. We intend to use the net proceeds to us from our initial public offering for working capital and other general corporate purposes; however, we do not currently have any specific uses of the net proceeds planned...Pending other uses, we intend to invest the proceeds to us in investment-grade, interest-bearing securities such as money market funds, certificates of deposit, or direct or guaranteed obligations of the U.S. government, or hold as cash.”15

Venture capitalists, early employees, and other investors wanted a way to cash out, and Facebook was bumping up against a regulatory limit on how many stockholders a private company could have. Moreover, Facebook stock would be a useful currency for making acquisitions. But these are very different reasons for going public than “raising capital.”

Facebook is not an anomaly. Many newly public companies are light on assets and employees and do not go public in order to invest in factories or stores or infrastructure. Blockbuster, which was delisted in 2010 and liquidated, had 84,000 employees and more than 9,000 stores at its peak. Netflix, which arguably drove Blockbuster out of business, has 3,700 employees and rents server space from Amazon, even as it expands globally. Zillow has 2,200 employees; Yelp has 3,800; and Facebook, with a market capitalization of more than $350 billion, has just 13,000 employees globally. (Each of these firms has an unknown but potentially large number of non-employee contractors.)

What gives? In my view, two main factors explain this disjuncture: contemporary firms don’t need capital the way their predecessors did, and there are alternative sources to the public markets. First, across many sectors, firms today do not need to build and own assets because they can rent them, from design to manufacturing to marketing and distribution. Even employees can be “rented” through temp agencies or online services like Upwork.

In a widely read piece in The New Yorker, Nathan Heller describes a discussion with a venture capitalist who described the plummeting cost of starting a business:

“Once, an entrepreneur would go to a venture capitalist for an initial five-million-dollar funding round—money that was necessary for hardware costs, software costs, marketing, distribution, customer service, sales, and so on. Now there are online alternatives. ‘In 2005, the whole thing exploded,’ [an informant] told me. ‘Hardware? No, now you just put it on Amazon or Rackspace. Software? It’s all open-source. Distribution? It’s the App Store, it’s Facebook. Customer service? It’s Twitter--just respond to your best customers on Twitter and Get Satisfaction. Sales and marketing? It’s Google AdWords, AdSense. So the cost to build and launch a product went from five million…to one million…to five hundred thousand…and it’s now to fifty thousand’” (Heller, 2013).16

Thus, Flip was the best-selling portable video camera in 2009, with 100 employees in San Francisco. Vizio was the best-selling television brand in the U.S. in 2010, with a staff of 200 in Irvine. If you can send your specifications to Alibaba, you can become a major electronics firm too, without having to leave your apartment.

It’s not just in technology: if you want to launch a new beer, or pet food, or tomato sauce brand, there are generic vendors happy to produce your recipe and get it to store shelves. If you want to start an airline, there are used jets in the Arizona desert waiting to be leased and consultants eager to help you complete the government paperwork. If you want to start a bank, Infosys has a “bank in a box” suite of software called Finacle, providing all the functionality people need through an online service.

Of course this won’t work for every industry. Jet engine manufacturing, petroleum refining, power-hungry server farms, or networks of warehouses still require capital in bulk. But across a large and growing range of industries, it’s cheaper to rent rather than buy, even up to very large scales. Why go public if you can fund a major business with your credit card? And Uber has demonstrated that is is possible to mobilize a vast workforce of non-employee contractors in a brief period. Most expect Uber to move toward autonomous vehicles in the future, but rather than enduring vast layoffs and costly severance payments, they can simply disable the driver app. Scaling up and scaling down are much simpler today than they were in the heyday of the traditional corporation.

Second, private equity provides an alternative means of intermediating capital that is often more appealing than the public markets. Large firms that go private (e.g., Chrysler, Dell) very often rely on private equity, which provides a vehicle to gather large amounts of capital from institutional investors, pensions, endowments, and wealthy individuals. The amounts involved rival the public markets. The New York Times reports that “Since the 2008 financial crisis, private equity firms have gone from managing $1 trillion to managing $4.3 trillion—more than the value of Germany’s gross domestic product.”17

Private equity is by no means a panacea for the pathologies of the public markets, as Eileen Appelbaum and Rosemary Batt amply document in their book Private Equity at Work.18 But it is clear that public markets are no longer the only source of capital on a large scale.

It is worth remembering that going public is not an end in itself, but a means to fund business. Perhaps the loss of public companies and the drought of IPOs is not as worrying as some think; business gets done whether the firms involved are listed on stock markets or not. Are there reasons to be anxious about the loss of public corporations?

The consequences of vanishing corporations

The idea that entrepreneurs can start businesses for a few bucks—maybe even in their dorm rooms—sounds appealing. Perhaps a few more Michael Dells or Mark Zuckerbergs can kickstart economic growth. (Surely repealing the “death tax” will bring empire-builders out of the woodwork?) But some of the benefits we derived from traditional public corporations are unlikely to return.

First, the changing shape of the corporation is connected to the changing shape of the employment relation and the fraying social safety net. At its peak, AT&T employed nearly a million people; GM had 800,000 employees; GE had 400,000. These firms provided solid, long-term, well-remunerated employment. The firms that have gone public since 2000 rarely create employment at large scale; the median firm to IPO after 2000 created just 51 jobs globally, and with rare exceptions (e.g., Alphabet/Google, with 62,000 employees), the jobs are in low-wage, low-opportunity sectors like retail and food service.

Indeed, although corporations are often accused of contributing to inequality, my prior research shows that the opposite is true: There is a nearly perfect negative relation between the size of the largest corporate employers in the U.S. and the Gini index of inequality. That is, income equality at the national level rises and falls with the size of major corporate employers. When corporations grew bigger in the 1960s, inequality declined; when corporations were taken over and busted up in the 1980s, inequality rose; and as outsourcing and offshoring took hold in the 1990s, inequality increased even more.19 (This turns out to be true around the world: nations with the lowest inequality, such as Denmark and Japan, tend to have the biggest corporations, while those with the highest inequality, such as Colombia, Brazil, and South Africa, tend to have small domestic corporations.)

Employment stability, income mobility, and inequality are tough problems, and it is unlikely that economics will allow us to return to an anomalous golden age of the corporation. But the U.S. is also uniquely reliant on corporations for providing a social safety net for their employees and their dependents. Unlike most of the rich world, the U.S. expects employers to provide health insurance and retirement security. The problems with America’s health care sector are well-documented. Somewhat less known is how the transition from traditional corporate pensions to 401(k) plans has left a generation of Baby Boomers severely under-prepared for retirement. Clearly, the disappearance of corporations is leaving major holes in the social safety net.

Second, the loss of public corporations leaves fewer policy levers at the Federal level. Big and concentrated firms are easier targets for regulation. During the Nixon Administration, the 25 biggest U.S. corporations employed nearly 10% of the civilian workforce. When OSHA wanted to improve workplace safety, or the Consumer Product Safety Commission wanted to ensure safer products, or the EPA wanted to curb big polluters, or the EEOC sought to reduce workplace discrimination, they could target a few of the biggest firms and have a large and immediate impact, particularly when these big firms encouraged their major suppliers to follow their lead. Moreover, because corporate law is made at the state level rather than the federal level, Congress has less leverage over businesses that are not publicly traded. Many Congressional efforts to rein in business happen through securities law and regulation. The long title of the Foreign Corrupt Practices Act of 1977, aimed at curbing bribery of foreign officials, is “An Act to amend the Securities Exchange Act of 1934 to make it unlawful for an issuer of securities registered pursuant to section 12 of such Act or an issuer required to file reports pursuant to section 15(d) of such Act to make certain payments to foreign officials and other foreign persons, to require such issuers to maintain accurate records, and for other purposes.” Thus, it primarily applied to firms listed on U.S. markets (although its reach has been extended). Similarly, the “conflict minerals” provision of the Dodd-Frank Act of 2010, which requires firms to disclose whether their products contain minerals mined in the Democratic Republic of Congo that might fund warlords, applies to Hewlett Packard (which is listed on the stock market) but not Dell (which is private).

Conclusion

The public corporation is an increasingly outdated way of organizing the economy in the U.S. Information and communication technologies and the emergence of generic service providers enable firms to rent capacity, including labor, on an as-needed basis. As a result, many firms do not require long-term capital on a large enough scale to justify the expense of going public. Public markets are volatile and demanding; alternative ways of raising capital are increasingly available. These are the master trends underlying the decline in public corporations.

From the perspective of an entrepreneur, this means that the parts to create a business are like Lego blocks that can be snapped together and scaled up or down as needed. From a consumer’s perspective, this means that every day brings new products and services delivered in new ways. But from the perspective of labor, this creates a precarious world of increasing inequality, lower mobility, and a ragged social safety net. And there is little reason to expect large-scale corporations like we saw in the 20th century to re-emerge in the 21st. Twitter is not going to turn into AT&T, with long career ladders and health insurance for retirees. Uber will never have as many employees as General Motors, whether it goes public or not.

What can public policy do? First, the underlying problem is not too few public corporations, but ensuring economic security. Family farms were still central to the American economy at the turn of the 20th century, but it would have made little sense to address the emerging problems of industrialization by focusing on policies promoting family farms. Similarly, large-scale corporations are a 20th century vehicle that may not be suited to the 21st century. Policy should aim to promote economic security and mobility in a post-corporate economy.

ABOUT THE AUTHOR

Jerry Davis received his PhD from the Graduate School of Business at Stanford University and taught at Northwestern and Columbia before moving to the University of Michigan, where he is the Gilbert and Ruth Whitaker Professor of Business Administration and Professor of Sociology. He has published widely in management, sociology, and finance. His books include Social Movements and Organization Theory (Cambridge University Press, 2005); Organizations and Organizing (Pearson Prentice Hall, 2007); Managed by the Markets: How Finance Reshaped America (Oxford University Press, 2009); Changing your Company from the Inside Out: A Guide for Social Intrapreneurs (Harvard Business Review Press, 2015); and The Vanishing American Corporation: Navigating the Hazards of a New Economy (Berrett Koehler, 2016). He is Co-Director of the Interdisciplinary Committee on Organization Studies (ICOS) at the University of Michigan.

Davis’s research is broadly concerned with the effects of finance on society, changes in the corporate economy, and new forms of organization. Recent writings examine how ideas about corporate social responsibility have evolved to meet changes in the structures and geographic footprint of multinational corporations; whether “shareholder capitalism” is still a viable model for economic development; how income inequality in an economy is related to corporate size and structure; why theories about organizations do (or do not) progress; how architecture shapes social networks and innovation in organizations; why stock markets spread to some countries and not others; and whether there exist viable organizational alternatives to shareholder-owned corporations in the United States.